신호정보(SIGINT) 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Signals Intelligence (SIGINT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

상품코드:1698311

리서치사:Global Market Insights Inc.

발행일:2025년 02월

페이지 정보:영문 175 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

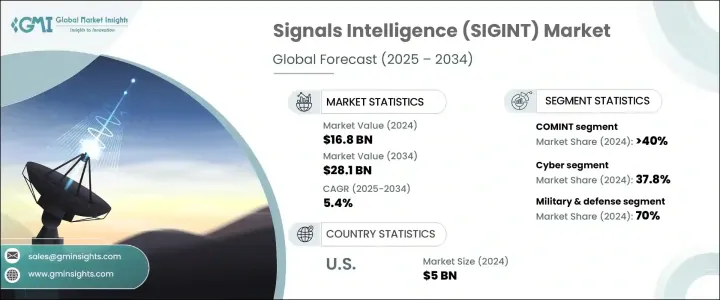

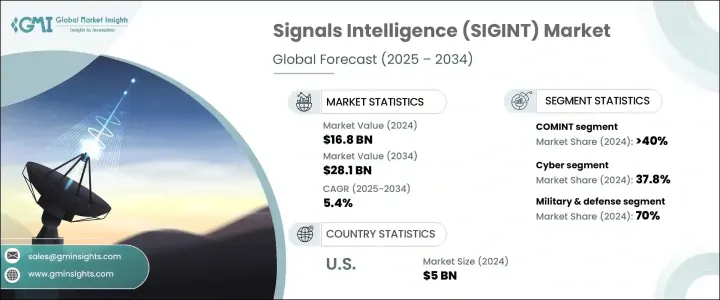

세계의 신호정보(SIGINT) 시장은 2024년에 168억 달러에 이르렀고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.4%를 나타낼 것으로 예측됩니다.

이러한 성장의 주요 요인은 인공지능(AI)과 센서 기술의 급속한 진보입니다. 필터링의 향상 등, 센서 기능의 강화에 의해 SIGINT 플랫폼의 감지 범위와 정밀도가 대폭 향상되어, 보다 효율적이고 정확한 정보 수집이 가능하게 되었습니다.

세계의 지정학적 긴장과 군사적 대립의 높아짐에 따라, SIGINT 시스템에 대한 수요는 증가하고 있습니다. 또, 전자전(EW)에 대한 우려로부터 시장도 확대하고 있어 전자적 위협에 대항하는 데 중요한 역할을 하고 있습니다. 특히 동유럽, 인도 태평양, 중동 등 지역에서는 위협이 계속 진화하고 있기 때문에 각국은 현대전에서의 경쟁을 유지하기 위해 SIGINT를 군사 전략에 통합하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

168억 달러

예측 금액

281억 달러

CAGR

5.4%

시장은 주로 통신 첩보(COMINT), 전자 첩보(ELINT), 대외 계측 신호 첩보(FISINT) 등 유형별로 구분됩니다. COMINT 솔루션은 음성, 텍스트, 암호화된 메시지의 가로채기 및 분석에 군사·안보기관에서의 이용이 증가하고 있어 실시간 위협 감지와 사이버 방어에서 중요한 역할을 하고 있습니다.

용도별로는 사이버 분야가 급성장하고 있으며 시장에서 큰 점유율을 차지하고 있습니다. 사이버 스파이와 디지털 전쟁에 의한 위협의 증대에 따라 중요 인프라 보호를 목적으로 한 사이버 SIGINT 기술에 대한 자금 제공이 급증하고 있습니다.

군사 및 방위 분야는 계속 신호정보(SIGINT) 시장을 독점하고 있으며, 2024년에는 시장 점유율 전체의 70% 가까이를 차지했습니다. 또한 각국 정부는 스파이 활동, 테러 대책, 국경 경비 활동에 SIGINT를 활용하고 있습니다.

북미는 세계의 신호정보(SIGINT) 시장을 선도하고 있으며, 미국은 2024년에 50억 달러의 큰 점유율을 차지했습니다.

목차

제1장 조사 방법과 조사 범위

조사 디자인

조사 접근

데이터 수집 방법

기본 추정과 계산

기준연도의 산출

시장추계의 주요 동향

예측 모델

1차 조사와 검증

1차 정보

데이터 마이닝 소스

시장 정의

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체의 상황

텔레매틱스 하드웨어 제공업체

소프트웨어 개발자

무선 통신사

시스템 통합업체

차량 관리 서비스 제공업체

이익률 분석

기술과 혁신의 전망

특허 분석

이용 사례

주요 뉴스와 대처

규제 상황

영향요인

성장 촉진요인

텔레매틱스와 IoT에 대한 수요 증가

엄격한 안전 및 배기가스 규제

E-Commerce 및 라스트마일 배송의 성장

전기 및 자율주행차의 채용 확대

업계의 잠재적 위험 및 과제

데이터 과다와 관리상의 우려

드라이버 관리 및 안전성 문제

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추계·예측 : 유형별(2021-2034년)

주요 동향

COMINT(통신 정보)

ELINT(전자 정보)

FISINT(해외 계측 신호 정보)

제6장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

사이버

지상

공중

전투기

특수 임무 항공기

운송기

무인 항공기(UAV)

해군

선박

잠수함

무인 해상 차량(UMV)

우주

제7장 시장 추계·예측 : 모빌리티별(2021-2034년)

주요 동향

고정형

휴대용

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

군사 및 방위

정부 및 법 집행 기관

상업 및 민간 부문

제9장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

스페인

이탈리아

러시아

북유럽

아시아태평양

중국

인도

일본

한국

뉴질랜드

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

UAE

남아프리카

사우디아라비아

제10장 기업 프로파일

Airbus

BAE Systems

Boeing

Collins Aerospace

DRS RADA Technologies

Elbit Systems

General Atomics

General Dynamics

Hensoldt

Israel Aerospace Industries

L3Harris

Leonardo

Lockheed Martin

Mercury Systems

Northrop Grumman

Raytheon

Rohde &Schwarz

Saab

SRC

Thales

KTH

영문 목차

영문목차

The Global Signals Intelligence Market reached USD 16.8 billion in 2024 and is expected to grow at a CAGR of 5.4% from 2025 to 2034. This growth is primarily fueled by rapid advancements in artificial intelligence (AI) and sensor technologies. AI algorithms enhance the ability to process vast amounts of data quickly, allowing for faster identification of threats. Coupled with machine learning, these systems are becoming more adept at recognizing patterns and anomalies in communications and electronic signals. Enhanced sensor capabilities, such as improved sensitivity and filtering, have significantly increased the range and precision of SIGINT platforms, enabling more efficient and accurate intelligence collection. These advancements are reducing the reliance on human operators while boosting the effectiveness of both tactical and strategic intelligence operations.

The rising geopolitical tensions and military confrontations worldwide have escalated the demand for SIGINT systems, as countries are increasingly relying on these technologies to monitor adversaries and secure national defense. The market is also expanding due to concerns over electronic warfare (EW), with SIGINT playing a crucial role in countering jamming, spoofing, and other electronic threats. Countries are integrating SIGINT into their military strategies to maintain a competitive edge in modern warfare, especially as threats continue to evolve in regions like Eastern Europe, the Indo-Pacific, and the Middle East.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$16.8 Billion

Forecast Value

$28.1 Billion

CAGR

5.4%

The market is primarily segmented by types, including Communications Intelligence (COMINT), Electronic Intelligence (ELINT), and Foreign Instrumentation Signals Intelligence (FISINT). Among these, COMINT leads the market, accounting for over 40% of the total share in 2024. COMINT solutions are increasingly used by military and security agencies for intercepting and analyzing voice, text, and encrypted messages, which play a critical role in real-time threat detection and cyber defense.

In terms of applications, the cyber segment is witnessing rapid growth, capturing a significant share of the market. With the increasing threats from cyber espionage and digital warfare, there has been a surge in funding for cyber SIGINT technologies aimed at protecting critical infrastructure. Governments and defense agencies are heavily investing in automated, AI-driven systems to enhance real-time threat detection capabilities.

The military and defense sector continues to dominate the SIGINT market, accounting for nearly 70% of the total market share in 2024. The increasing demand for electronic warfare and threat detection solutions is driving significant growth in this sector. Additionally, governments are leveraging SIGINT for espionage, counterterrorism, and border security operations. The commercial sector is also adopting SIGINT technologies to safeguard against cyber threats and ensure secure communication.

North America leads the global SIGINT market, with the United States contributing a substantial share of USD 5 billion in 2024. The U.S. is making significant investments in AI-powered signal processing and data analytics to strengthen its defense and intelligence capabilities, ensuring robust national security.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimates

1.3 Forecast model

1.4 Primary research & validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market definitions

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Telematics hardware providers

3.2.2 Software developers

3.2.3 Wireless carriers

3.2.4 System integrators

3.2.5 Fleet management service providers

3.3 Profit margin analysis

3.4 Technology & innovation landscape

3.5 Patent analysis

3.6 Use cases

3.7 Key news & initiatives

3.8 Regulatory landscape

3.9 Impact forces

3.9.1 Growth drivers

3.9.1.1 Rising Demand for telematics & IoT

3.9.1.2 Stringent safety & emission regulations

3.9.1.3 Growth in e-commerce & last-mile delivery

3.9.1.4 Growing adoption of electric & autonomous vehicles