피부과 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Dermatology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1666917

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 135 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

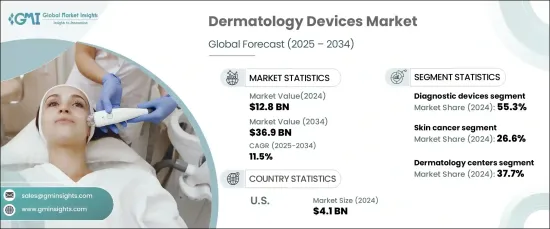

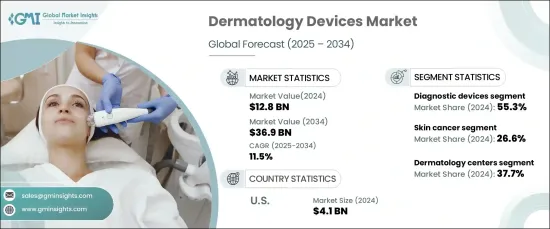

세계의 피부과 기기 시장은 2024년에 128억 달러가 되었고, 2025년부터 2034년에 걸쳐 11.5%라는 경이적인 CAGR로 성장할 것으로 예상되고 있습니다.

이 성장은 주로 피부암을 포함한 피부 질환의 유병률 증가와 신흥국의 스킨 케어에 대한 주목 증가에 기인합니다. 게다가, 피부과 기기의 기술적 진보가 이 시장 확대에 중요한 역할을 하고 있는 반면, 선진 지역에서는 미용 성형에 대한 수요가 높아지고 있습니다. 소비자가 피부 건강과 미용 치료를 우선시하는 동안 시장은 지속적인 성장을 이룰 것으로 보입니다.

이 시장은 진단 및 치료 기기로 분류되며, 모두 세계적으로 증가하는 피부 관련 건강 문제를 해결하는 데 중요한 역할을합니다. 진단 기기는 조기 및 정확한 발견에 필수적이며 영상 진단 시스템, 피부 거울, 생검 도구 등을 포함합니다. 한편, 치료 기기는 광 치료 시스템, 레이저, 마이크로 다마브레이션 장치, 동결 치료 기기, 전기 수술 기기, 지방 흡입 기기를 포함합니다. 2024년에는 진단 기기가 전체 시장의 55.3%를 차지하고 시장을 독점했습니다. 이는 습진이나 피부암 등의 증상을 적시에 특정할 필요성이 높아지고 있기 때문입니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

128억 달러

예측 금액

369억 달러

CAGR

11.5%

용도별로 피부과 기기는 피부암, 피부 회춘, 탈모, 바디 라인, 건선 및 기타 다양한 피부 질환의 치료에 널리 사용됩니다. 피부암 분야는 2024년 시장을 선도해 26.6%의 점유율을 차지했습니다. 이는 피부암 환자의 세계가 증가함에 따라 신뢰성이 높은 진단·치료 도구 수요가 높아지고 있기 때문입니다. 첨단 피부과 기기는 암성 병변과 전암성 병변을 모두 확인하는 데 필수적이며 조기 개입과 환자 결과 개선을 가능하게 합니다.

미국의 피부과 기기 시장은 2024년에 41억 달러가 되었으며 여전히 세계 최대입니다. 이 우위성은 미국에서의 흑색종 및 흑색종 이외의 피부암 발생률의 높이와 광범위한 의식 향상 프로그램 및 피부암 예방의 대처가 결합되어 가져온 것입니다. 또한 미국 FDA의 첨단 피부과 기기 승인은 최첨단 진단 및 치료 솔루션의 제공을 강화하고 시장의 지속적인 성장과 혁신에 기여하고 있습니다. 피부과 의료에 대한 수요가 높아짐에 따라 미국은 이 급성장 시장에서 중요한 선수로 남아 있을 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

업계에 미치는 영향요인

성장 촉진요인

세계의 피부 관련 질환 및 피부암의 이환율의 상승

신흥 국가의 스킨 케어에 대한 지출 증가

스킨케어 기기의 기술 진보

선진국의 미용시술 수요 증가

업계의 잠재적 리스크 및 과제

과도한 기기 비용

엄격한 규제 상황

성장 가능성 분석

규제 상황

기술적 전망

특허 분석

향후 시장 동향

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도(2024년)

서론

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 전망

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

주요 동향

진단 기기

영상 기기

피부경

생검 기기

치료기기

광선치료기기(LED치료)

레이저

미세박피술 기기

냉동요법 기기

전기수술 기기

지방흡입 기기

제6장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

피부암

피부 회춘

제모

바디 컨투어링 및 피부 타이트닝

건선

기타 용도

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

피부과 센터

병원

클리닉

기타 최종 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제9장 기업 프로파일

Alma Lasers(Fosun Pharma)

Ambicare Health

Bausch Health Companies

Biolitec

Bruker Corporation

Candela Corporation

Canfield Scientific

Carl Zeiss

Cutera

Cynosure Lutronic

Genesis Biosystems

Heine Optotechnik

Hologic

Image Derm

Leica Microsystems

Lumenis

Michelson Diagnostics(VivoSight)

Olympus Corporation

KTH

영문 목차

영문목차

The Global Dermatology Devices Market was valued at USD 12.8 billion in 2024 and is expected to grow at an impressive CAGR of 11.5% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of skin diseases, including skin cancer, as well as the rising focus on skincare in emerging economies. Additionally, technological advancements in dermatology devices are playing a key role in the expansion of this market, while developed regions are seeing heightened demand for cosmetic procedures. As consumers continue to prioritize skin health and aesthetic treatments, the market is set for sustained growth.

The market is categorized into diagnostic and treatment devices, both of which serve critical roles in addressing the increasing incidence of skin-related health concerns globally. Diagnostic devices are essential for early and accurate detection and include imaging systems, dermatoscopes, and biopsy tools. Meanwhile, treatment devices encompass light therapy systems, lasers, microdermabrasion units, cryotherapy tools, electrosurgical equipment, and liposuction devices. In 2024, diagnostic devices dominated the market, accounting for 55.3% of the total share. This is attributed to the growing need for timely identification of conditions such as eczema and skin cancer, as early detection is key to successful treatment outcomes.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$12.8 Billion

Forecast Value

$36.9 Billion

CAGR

11.5%

In terms of application, dermatology devices are widely used in the treatment of skin cancer, skin rejuvenation, hair removal, body contouring, psoriasis, and various other dermatological conditions. The skin cancer segment led the market in 2024, commanding a significant 26.6% share. This is due to the global rise in skin cancer cases, driving the demand for reliable diagnostic and treatment tools. Advanced dermatology devices are indispensable in identifying both cancerous and precancerous lesions, allowing for early intervention and improved patient outcomes.

The U.S. dermatology devices market, with a valuation of USD 4.1 billion in 2024, remains the largest in the world. This dominance is driven by the high rates of melanoma and non-melanoma skin cancers in the U.S., combined with extensive awareness programs and skin cancer prevention initiatives. Furthermore, the approval of advanced dermatology devices by the U.S. FDA has bolstered the availability of cutting-edge diagnostic and treatment solutions, contributing to the market's continued growth and innovation. As the demand for dermatological care intensifies, the U.S. will remain a key player in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Base estimates and calculations

1.3.1 Base year calculation

1.3.2 Key trends for market estimation

1.4 Forecast model

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising incidence of skin associated diseases and skin cancer worldwide

3.2.1.2 Increasing expenditure on skin care in developing countries

3.2.1.3 Technological advancements in skincare devices

3.2.1.4 Growing demand for cosmetic procedures in developed countries

3.2.2 Industry pitfalls and challenges

3.2.2.1 Excessive equipment cost

3.2.2.2 Stringent regulatory landscape

3.3 Growth potential analysis

3.4 Regulatory landscape

3.5 Technological landscape

3.6 Patent analysis

3.7 Future market trends

3.8 Porter’s analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Competitive analysis of major market players

4.4 Competitive positioning matrix

4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Diagnostic devices

5.2.1 Imaging devices

5.2.2 Dermatoscopes

5.2.3 Biopsy devices

5.3 Treatment devices

5.3.1 Light therapy devices (LED therapy)

5.3.2 Lasers

5.3.3 Microdermabrasion devices

5.3.4 Cryotherapy devices

5.3.5 Electrosurgical equipment

5.3.6 Liposuction devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Skin cancer

6.3 Skin rejuvenation

6.4 Hair removal

6.5 Body contouring and skin tightening

6.6 Psoriasis

6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 Dermatology centers

7.3 Hospitals

7.4 Clinics

7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)