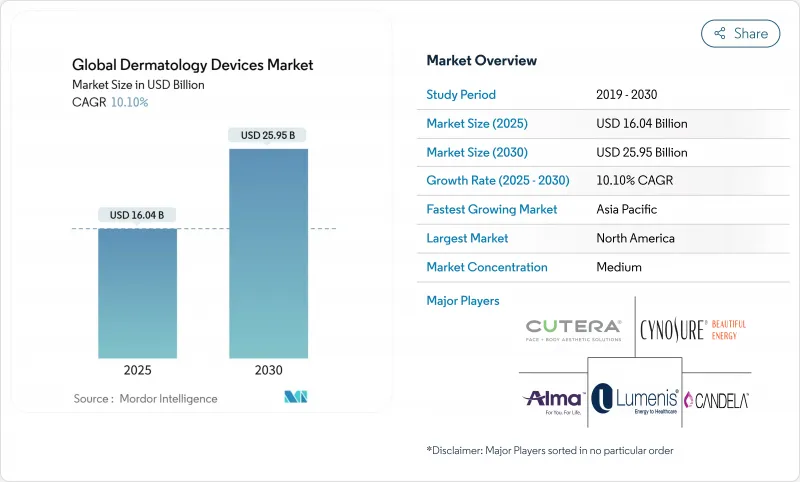

피부과 기기 시장은 2025년에 160억 4,000만 달러로 평가되고 CAGR 10.1%를 나타내 2030년에는 259억 5,000만 달러에 이를 전망입니다.

이 성장 궤도는 인공지능, 실시간 열 모니터링이 가능한 레이저, 원격 피부 과학 연결을 통해 가능해지는 반응적 치료에서 예측 진단으로의 명확한 전환을 반영합니다. 수요는 여전히 탈모와 병변 절제를 위한 확립된 치료에 집중하고 있지만, AI 유도 화상 진단에 의해 피부암의 조기 발견이 1차 케어에 도입되어 소개에 필요한 시간이 단축되어 환자 수가 확대되고 있습니다. 동시에 낮은 침습 미용에 대한 소비자의 취향은 클리닉, 메디컬 스파, 외래 수술 센터(ASC)에서의 시술량을 높은 수준으로 유지하고 있습니다. 지역에 따라 패턴이 다르다 : 북미는 진료 보상의 명확화로부터 혜택을 받지만, 아시아태평양은 가처분 소득 증가, 국내 제조업에 대한 정부의 지원, 전문의 네트워크의 확대를 배경으로, 가장 급속히 확대하고 있습니다. EU의 규제 강화와 메디케어의 진료 보상 인하는 기세를 깎지만, 견고한 품질 시스템과 다양한 수익 모델을 가진 기업에게 유리합니다.

피부암은 이미 미국 인구의 1/4로 퍼져 있어, 지금까지 전문의의 커버 범위가 한정되어 있던 지역에서의 발생이 가속하고 있습니다. 핸드헬드 스펙트로스카피 장치는 1차 케어의 트리아지의 지침이 되어, 표면 조사나 광선역학적 치료 램프와 같은 비외과적 치료 장치는 일단 절제가 필요했던 병변을 관리할 수 있게 합니다. 분수 CO2 레이저가 광선 장애를 감소시킨다는 학문적 증거는 예방 프로토콜을 지원하고 일상 진료에서 장비의 필요성을 강화합니다.

세계 수술 건수는 주사, 리서페이싱, 바디 컨터링으로 계속 이동하고 있습니다. 메디컬 스파 및 체인 클리닉은 병원에서의 조달 사이클을 피하고 유닛의 회전을 가속화하며 유연한 임대 및 사용 당 지불 모델로 공급업체에게 보상을 제공합니다. 장시간 작용하는 신경독과 생체 자극성 필러는 미용과 치료 적응을 더욱 얽히고 피부과 기기 시장을 효과적으로 확대합니다.

메디케어는 2025년 의사 전환 요인을 32.35달러로 낮추고 클리닉이 돈이 많이 드는 장비 구매를 연기하도록 촉구하고 있습니다. 상장 기업 여러 회사를 포함한 에너지 기반 장비 제조업체는 수익 감소를보고하고 부채와 간접비를 줄이기 위해 구조 조정을 시작했습니다. 저소득 국가에서는 자본 예산이 제한되어 있기 때문에 공급자는 정비된 시스템과 임대 모델을 이용하게 되어 프리미엄 플랫폼의 보급이 늦어지고 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

치료 시스템은 2024년 매출의 55.45%를 차지하며, 탈모 레이저, 혈관 병변 시스템, 고주파 바디 컨투어링이 그 중심이 되었습니다. 이 베이스에서는 경상적인 소모품과 서비스 계약이 2030년까지 예측 10.85%의 안정 성장을 유지할 것으로 예측됩니다. 그러나 진단 플랫폼은 AI 통합 분광법과 고해상도 더모스 카피에 견인되어 현재 가장 빠르게 개선되고 있습니다. 2025년에 출시된 이중 파장 분수 시스템은 이미지 피드백과 리서피싱 출력을 융합시켰으며, 하이브리드 설계가 이전 진단과 치료의 경직된 경계를 침식하고 있음을 보여줍니다. 엔트리 레벨 냉동 요법 장비는 1 차 진료와 수의학 틈새에 여전히 도움이되는 반면, 광선 역학 램프는 광선 역학 램프는 광선각화증에 대한 상환을 보장하는 종양학 코드를 받았습니다.

북미는 2024년 매출의 41.56%를 차지했습니다. 이 시장은 FDA의 명확한 패스웨이, 1인당 시술률의 높이, 선택적 치료에 대한 민간보험 적용 등의 이점을 누리고 있습니다. AI 진단제와 여드름 레이저에 대한 획기적인 지정은 진정한 혁신을 가속화하는 규제 당국의 의지를 보여줍니다. 그럼에도 불구하고 진료 보상을 줄이고 인력 부족이 성장을 억제할 수 있기 때문에 클리닉은 다양한 적응증과 견고한 서비스 지원을 갖춘 플랫폼을 선호합니다.

유럽은 두 번째이지만 MDR과 관련된 인증 병목 현상에 직면하고 있으며 규모와 공식적인 임상 데이터 저장소를 가진 기업이 유리합니다. 특히 독일, 프랑스, 영국에서는 경기의 역풍에도 불구하고 미용 의료 시술 건수가 계속 증가하고 있습니다. 공급업체는 컴플라이언스 부담을 줄이기 위해 장비 재고를 줄이기 때문에 여러 용도를 통합한 워크스테이션을 제공하는 공급업체가 인기를 얻고 있습니다.

아시아태평양은 성장 엔진이며 2030년까지 연평균 복합 성장률(CAGR)은 11.98%를 나타낼 것으로 예측됩니다. 중국은 생산을 현지화하고 국가의 상환 코드 승인을 가속화하는 정책에 힘입어 2029년까지 연평균 복합 성장률(CAGR) 8%를 나타내 556억 7,000만 달러를 목표로 하고 있습니다. 한국과 일본은 색소 침착과 아토피 피부염의 레이저 치료로 기술 채용을 선도하고 인도는 원격 의료 프로그램에서 저렴한 AI 피부경의 신속한 보급을 나타냅니다. 태국과 말레이시아의 도시 지역에서의 의료 관광은 리서피싱과 문신 제거에 대한 수요를 높이고 있습니다.

라틴아메리카와 중동은 멕시코, 브라질, 사우디아라비아, 아랍에미리트(UAE)의 민간 클리닉을 중심으로 한 자릿수 중반의 성장을 보여줍니다. 환율 변동과 수입 관세가 자본 설비 사이클에 영향을 미치고 임대에 대한 관심을 높이고 있습니다. 아프리카는 자금 조달과 전문의의 밀도가 제한적이기 때문에 늦었습니다. AI 트리아지를 이용한 모바일 원격 피부과 허브는 액세스 확대가 기대됩니다.

The dermatology devices market was valued at USD 16.04 billion in 2025 and is on track to reach USD 25.95 billion by 2030, advancing at a 10.1% CAGR.

The growth trajectory reflects a clear migration from reactive care to predictive diagnostics enabled by artificial intelligence, lasers with real-time thermal monitoring, and tele-dermatology connectivity. Demand remains anchored in established treatments for hair removal and lesion ablation, yet AI-guided imaging now pushes earlier detection of skin cancers into primary-care settings, shortening referral times and expanding patient pools. At the same time, consumer appetite for minimally invasive aesthetics keeps procedure volumes high in clinics, medical spas, and ambulatory surgery centers. Regional patterns diverge: North America benefits from reimbursement clarity, but Asia-Pacific captures the fastest expansion on the back of rising disposable income, government support for domestic manufacturing, and widening specialist networks. Tightened EU regulations and Medicare fee cuts temper momentum, yet they also favor firms with robust quality systems and diversified revenue models.

Skin cancer already affects up to one quarter of the United States population, and incidence is accelerating in regions with historically limited specialist coverage IntechOpen. Earlier detection drives dual demand: handheld spectroscopy units guide primary-care triage, while non-surgical treatment devices-such as superficial radiation and photodynamic therapy lamps-allow clinicians to manage lesions that once required excision. Academic evidence that fractional CO2 lasers reduce actinic damage supports preventive protocols, reinforcing device necessity in routine practice PubMed.

Global procedure volumes continue to shift toward injectables, resurfacing, and body contouring. Medical spas and chain clinics bypass hospital procurement cycles, accelerating unit turnover and rewarding suppliers with flexible leasing or pay-per-use models. Longer-acting neurotoxins and biostimulatory fillers further intertwine cosmetic and therapeutic indications, effectively enlarging the dermatology devices market.

Medicare cut the 2025 physician conversion factor to USD 32.35, nudging clinics to defer large-ticket equipment purchases. Manufacturers of energy-based devices, including several publicly traded firms, reported revenue contraction and have initiated restructuring to trim debt and overhead. In lower-income countries, limited capital budgets push providers toward refurbished systems or rental models, slowing premium platform penetration.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Treatment systems represented 55.45% of revenue in 2024, anchored by hair-removal lasers, vascular lesion systems, and radiofrequency body-contouring. Within that base, recurring consumables and service contracts keep growth steady at a projected 10.85% through 2030. Yet diagnostic platforms are now the fastest improvers, led by AI-integrated spectroscopy and high-definition dermoscopy. A dual-wavelength fractional system launched in 2025 merges imaging feedback with resurfacing output, illustrating how hybrid designs erode the once-rigid boundary between diagnosis and therapy. Entry-level cryotherapy units still serve primary-care and veterinary niches, whereas photodynamic lamps gain oncology codes that secure reimbursement for actinic keratosis.

The Dermatology Devices Market Report Segments the Industry Into by Devices Type (Diagnostics Devices [Imaging Devices, Dermatoscopes, and More. ] and Treatment Devices [Light Therapy Devices, Lasers, and More. ]), by Application (Skin Cancer Diagnosis, Vascular Lesions, Acne, Psoriasis, and Tattoo Removal, and More. ), and by Geography( North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 41.56% of 2024 revenue. The market benefits from clear FDA pathways, high per-capita procedure rates, and private-insurance coverage of elective treatments. Breakthrough designations for AI diagnostics and acne lasers demonstrate regulatory willingness to speed true innovation. Still, reimbursement cuts and staffing gaps may temper growth, leading clinics to favor platforms with diversified indications and robust service support.

Europe ranks second but faces MDR-linked certification bottlenecks that advantage companies with scale and formal clinical-data repositories. Demand remains strong for pigment and vascular systems, especially in Germany, France, and the United Kingdom, where aesthetic procedure counts continue to climb despite economic headwinds. Because providers are pruning device inventories to limit compliance burden, vendors offering consolidated multi-application workstations gain traction.

Asia-Pacific is the growth engine, forecast at an 11.98% CAGR through 2030. China targets an 8% device CAGR to USD 55.67 billion by 2029, bolstered by policies that localize production and expedite national-reimbursement code approvals. Korea and Japan lead technology adoption in pigmentation and atopic-dermatitis laser therapy, while India shows quick uptake of affordable AI dermatoscopes in tele-health programs. Urban medical tourism in Thailand and Malaysia adds demand for resurfacing and tattoo removal.

Latin America and the Middle East deliver mid-single-digit gains centered on private clinics in Mexico, Brazil, Saudi Arabia, and the UAE. Currency swings and import duties affect capital-equipment cycles, driving interest in leasing. Africa lags, constrained by funding and limited specialist density; mobile tele-dermatology hubs using AI triage hold promise for incremental access expansion.