궤도상 위성 서비스 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

On-orbit Satellite Servicing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1665218

리서치사:Global Market Insights Inc.

발행일:2024년 12월

페이지 정보:영문 170 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

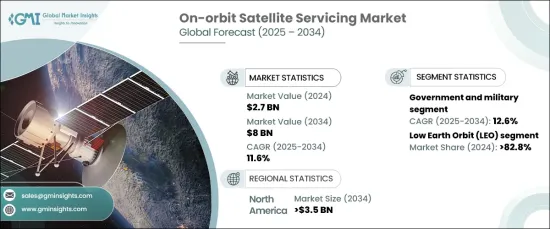

세계의 궤도상 위성 서비스 시장은 대폭적인 성장을 이루었고, 2024년에는 27억 달러에 이르렀으며, 2025-2034년까지 CAGR 11.6%로 성장할 것으로 예상됩니다.

이 급성장의 배경에는 운영 수명 연장, 발사 비용 절감, 성능 향상을 목적으로 위성 유지 보수, 수리 및 업그레이드에 대한 수요 증가가 있습니다. 커뮤니케이션, 지구관측, 방어 등 주요 용도로 위성 배치가 증가함에 따라 시장 성장 궤도가 더욱 가속화되고 있습니다.

궤도 유형별로 시장을 분석하면 저궤도(LEO)가 선도하고 있으며, 2024년 시장 점유율의 82.8%를 차지했습니다. LEO의 이점은 특히 세계의 광대역 방송 및 원격 감지에 초점을 맞춘 위성 성상도의 폭발적인 증가로 인한 것입니다. 이 궤도에 위성이 밀집되어 있기 때문에 로봇에 의한 연료 보급, 수리, 파편 제거 등의 혁신적인 솔루션이 필요합니다. 또한 LEO는 지구에 가깝기 때문에 빈번하고 비용 효율적인 서비스 임무를 수행하기 쉽고 위성 운영의 지속가능성과 효율성을 보장합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

27억 달러

예측 금액

80억 달러

CAGR

11.6%

최종 사용자별로 보면 궤도상 위성 서비스 시장은 정부 및 군사기관과 상업사업자로 구분됩니다. 2025-2034년의 예측 CAGR은 12.6%로 정부 및 군수 부문이 가장 급성장할 것으로 전망되고 있습니다. 정부가 중요한 우주 자산의 기능을 유지하고 국가 안보를 강화하고 교환 비용을 줄이려고 하기 때문에 위성 인프라에 대한 투자가 증가하고 있으며 이 수요에 박차를 가하고 있습니다. 게다가 관민들의 협력은 기술 진보를 촉진하고 이 부문의 성장을 가속화하는데 중요한 역할을 합니다.

북미는 세계의 궤도상 위성 서비스 시장을 독점하게 되어 2034년까지 35억 달러에 이를 전망입니다. 이 지역의 강한 지위는 우주 기술에 대한 엄청난 투자와 이 산업의 주요 진출기업의 확립 된 존재로 인해 발생합니다. 기술 혁신을 지원하는 정부 프로그램은 위성 통신 및 방위 솔루션 수요 증가와 함께 이 부문에서 북미의 리더십을 확고히 하고 있습니다. 게다가 이 지역의 지속가능한 우주개발에 대한 노력과 궤도상 서비스 기술의 약진이 시장에서의 지위를 한층 더 높이고 있습니다.

목차

제1장 조사 방법과 조사 범위

시장 범위와 정의

기본 추정과 계산

예측 계산

데이터 소스

1차 데이터

2차 자료

유료 정보원

공적 정보원

제2장 주요 요약

제3장 산업 인사이트

생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

변혁

미래의 전망

제조업체

유통업체

공급자의 상황

이익률 분석

주요 뉴스와 대처

규제 상황

영향요인

성장 촉진요인

위성 별자리와 우주 트래픽의 급증

위성 수명주기 연장으로 비용 절감

우주 로봇 공학과 자동화에 있어서의 돌파구

정부와 민간기업의 투자 확대

우주 파편 관리에 대한 관심 증가

산업의 잠재적 리스크 및 과제

높은 개발·운용 비용

기술적 복잡성과 운영 리스크

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업 점유율 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추정·예측 : 서비스별, 2021-2034년

주요 동향

액티브 파편 제거(ADR)와 궤도 조정

로봇 서비스

연료 보급

조립

제6장 시장 추정·예측 : 궤도 유형별, 2021-2034년

주요 동향

지구 저궤도(LEO)

중궤도(MEO)

정지궤도(GEO)

제7장 시장 추정·예측 : 위성 유형별, 2021-2034년

주요 동향

소형 위성(500Kg 이하)

중형 위성(501-1,000Kg)

대형 위성(1,000Kg 이상)

제8장 시장 추정·예측 : 최종 용도별, 2021-2034년

주요 동향

정부 및 군사기관

민간 사업자

제9장 시장 추정·예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

Airbus SE

Altius Space Machines, Inc.

Astroscale Holdings Inc.

Atomos Space

ClearSpace

Future Space Industries

High Earth Orbit Robotics

Hyoristic Innovations

Infinite Orbits

Lunasa Ltd.

Maxar Technologies

Momentus, Inc.

Nanoracks(Voyager Space)

Obruta Space Solutions Corp

Orbit Fab, Inc.

Orbitaid Aerospace Private Limited

Orion AST

Rogue Space Systems

Scout Aerospace LLC

Space Machines Company Pty Ltd

Tethers Unlimited, Inc.

Thales Alenia Space

Turion Space

JHS

영문 목차

영문목차

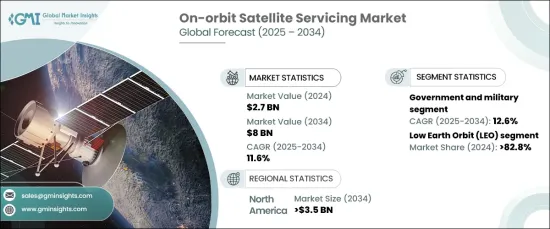

The Global On-Orbit Satellite Servicing Market is poised for significant growth, reaching USD 2.7 billion in 2024, with projections pointing to an impressive CAGR of 11.6% from 2025 to 2034. This rapid expansion is driven by the increasing demand for satellite maintenance, repair, and upgrades aimed at extending operational lifespans, cutting launch costs, and boosting performance. The rising deployment of satellites for key applications such as communications, Earth observation, and defense further accelerates the market's growth trajectory.

When analyzing the market by orbit type, Low Earth Orbit (LEO) takes the lead, commanding 82.8% of the market share in 2024. LEO's dominance can be attributed to the explosion of satellite constellations, particularly those focused on global broadband coverage and remote sensing. The dense satellite presence in this orbit necessitates innovative solutions, including robotic refueling, repair, and debris removal. Additionally, the proximity of LEO to Earth makes it easier to conduct frequent and cost-effective servicing missions, ensuring the sustainability and efficiency of satellite operations.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.7 Billion

Forecast Value

$8 Billion

CAGR

11.6%

In terms of end users, the on-orbit satellite servicing market is segmented into government and military entities and commercial operators. The government and military segment is expected to experience the fastest growth, with a forecasted CAGR of 12.6% during the 2025-2034 period. Increased investments in satellite infrastructure are fueling this demand as governments seek to preserve the functionality of critical space assets, enhance national security, and reduce replacement costs. Furthermore, collaborations between the public and private sectors are driving technological advancements, which will play a crucial role in accelerating the growth of this segment.

North America is set to dominate the global on-orbit satellite servicing market, with expectations to reach USD 3.5 billion by 2034. The region's strong position stems from substantial investments in space technologies and a well-established presence of key players in the industry. Government programs supporting innovation, coupled with increasing demand for satellite communication and defense solutions, are solidifying North America's leadership in this space. Additionally, the region's commitment to sustainable space practices and breakthroughs in in-orbit servicing technologies further enhances its market position.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definitions

1.2 Base estimates & calculations

1.3 Forecast calculations

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Supplier landscape

3.3 Profit margin analysis

3.4 Key news & initiatives

3.5 Regulatory landscape

3.6 Impact forces

3.6.1 Growth drivers

3.6.1.1 Surge in satellite constellations and space traffic

3.6.1.2 Cost savings through satellite lifecycle extension

3.6.1.3 Breakthroughs in space robotics and automation

3.6.1.4 Growing government and private sector investment