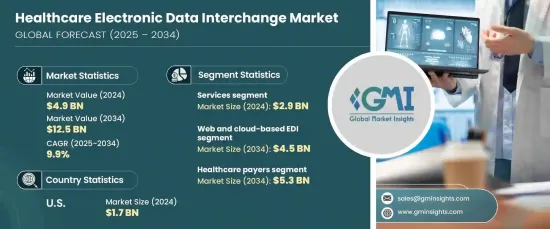

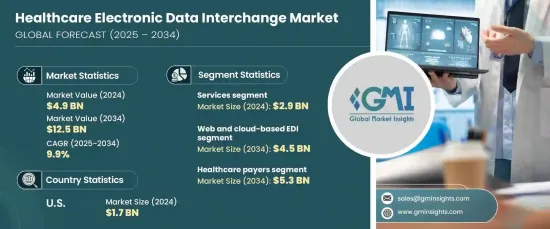

세계의 헬스케어 전자데이터교환 시장은 2024년 49억 달러로 평가되었으며, 2025년부터 2034년까지 9.9%의 연평균 복합 성장률(CAGR)로 현저한 성장을 이룰 것으로 예측됩니다.

이 시장 확대는 엄격한 규제의 의무화, 원활한 상호 운용성에 대한 수요 증가, 헬스케어 시스템의 관리 업무의 합리화 요구의 높아짐에 추진되어, 자동화된 전자데이터교환 솔루션의 채용이 증가하고 있는 것이 배경에 있습니다.

헬스케어 산업이 디지털 변환을 도입하는 동안 전자데이터교환 플랫폼은 지불자, 공급자 및 이해 관계자간의 안전하고 표준화된 효율적인 데이터 교환에 필수적인 도구로 부상하고 있습니다. 이러한 플랫폼은 수작업으로 비효율적인 프로세스를 제거하고 진화하는 규정에 대한 규정 준수를 보장하며 민감한 환자 정보를 보호합니다. 또한 클라우드 컴퓨팅과 AI를 활용한 분석의 진보로 정교하고 비용 효율적인 솔루션이 도입되어 모든 규모의 조직에 전자데이터교환 시스템의 매력이 확산되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 49억 달러 |

| 예측 금액 | 125억 달러 |

| CAGR | 9.9% |

헬스케어 전자데이터교환 시스템의 도입을 가속화하는 데 있어 정부의 규제와 업계 표준이 매우 중요한 역할을 하고 있습니다. 규제 프레임 워크는 안전한 데이터 교환의 필요성을 강조하고 헬스케어 기관에 워크 플로우의 현대화를 촉진합니다. 자동화된 전자데이터교환 솔루션은 헬스케어 에코시스템 전체의 효율적인 커뮤니케이션을 촉진하면서 프라이버시 및 보안 표준에 대한 완벽한 규정 준수를 보장합니다. 디지털화의 추진은 헬스케어 서비스 제공업체가 성능 최적화 및 비용 절감을 위한 압박을 강화하는 데 특히 중요하며 시장 확대를 더욱 강화하고 있습니다.

구성 요소별로 보면, 헬스케어 전자데이터교환 시장은 서비스와 솔루션으로 구분되어 서비스가 수익을 선도하고 있습니다. 서비스는 2024년에 29억 달러에 이르렀으며 업계의 시스템 통합, 사용자 정의, 교육 및 기술 지원에 대한 의존도가 반영되었습니다. 조직이 레거시 시스템에서 최신 전자데이터교환 플랫폼으로 마이그레이션할 때 이러한 서비스는 부드럽고 효율적인 통합 프로세스를 보장합니다. 전문 서비스에 대한 수요 증가는 상호 운용성 달성과 엄격한 규정 준수 요구 사항을 준수하기 위해 헬스케어 부서가 주력하고 있음을 뒷받침합니다. 이러한 추세는 운영 우수성을 추구하는 건강 관리 제공업체의 우선순위와 일치하여 기세를 늘릴 것으로 예상됩니다.

시장은 또한 전자데이터교환 부가가치 네트워크(VAN), 직접(포인트-투-포인트) 전자데이터교환, 웹 및 클라우드 기반 전자데이터교환, 모바일 전자데이터교환과 같은 배포 유형에 따라 세분화됩니다. 이 중 웹 및 클라우드 기반 전자데이터교환 솔루션은 2024년에 우위를 차지했으며, 이 부문은 2034년까지 45억 달러를 창출할 것으로 예상됩니다. 클라우드 기반 솔루션은 타의 추종을 불허하는 확장성과 비용 효율성을 제공하므로 건강 관리 조직은 상당한 하드웨어 투자 없이 업무를 확장할 수 있습니다. 이러한 시스템은 온프레미스 인프라를 유지하는 부담 없이 고급 도구에 대한 액세스를 요구하는 중소규모 헬스케어 기관에 특히 매력적입니다. 클라우드 기반 전자데이터교환는 유연성, 신뢰성 및 저렴한 가격으로 시장 성장의 기초가 되었습니다.

북미의 헬스케어 전자데이터교환 시장은 2024년 17억 달러를 차지했는데, 이는 표준화된 거래를 의무화하는 엄격한 규제 요건과 미국의 견조한 헬스케어 지출에 힘쓴 결과입니다. 업계가 데이터 중심의 혁신을 선호하는 가운데 디지털 인프라와 AI 중심의 분석에 대한 투자가 지속적으로 첨단 전자데이터교환 솔루션의 채택을 촉진하고 헬스케어 데이터 교환의 세계 상황을 재구성하고 있습니다.

The Global Healthcare Electronic Data Interchange Market, valued at USD 4.9 billion in 2024, is set to experience remarkable growth with a projected CAGR of 9.9% between 2025 and 2034. This expansion is driven by the increasing adoption of automated EDI solutions, propelled by stringent regulatory mandates, growing demand for seamless interoperability, and the rising need to streamline administrative operations in healthcare systems.

As the healthcare industry embraces digital transformation, EDI platforms emerge as indispensable tools for secure, standardized, and efficient data exchange between payers, providers, and stakeholders. These platforms eliminate the inefficiencies of manual processes, ensuring compliance with evolving regulations and safeguarding sensitive patient information. Furthermore, advancements in cloud computing and AI-powered analytics have introduced sophisticated, cost-effective solutions, broadening the appeal of EDI systems to organizations of all sizes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 9.9% |

Government regulations and industry standards play a pivotal role in accelerating the adoption of healthcare EDI systems. Regulatory frameworks emphasize the necessity for secure data exchange, prompting healthcare organizations to modernize their workflows. Automated EDI solutions ensure seamless compliance with privacy and security standards while fostering efficient communication across the healthcare ecosystem. This push toward digitization is particularly significant as healthcare providers grapple with mounting pressures to optimize performance and reduce costs, further driving the market's expansion.

In terms of components, the healthcare EDI market is segmented into services and solutions, with services leading the charge in revenue generation. Services reached USD 2.9 billion in 2024, reflecting the industry's reliance on system integration, customization, training, and technical support. As organizations transition from legacy systems to modern EDI platforms, these services ensure a smooth and efficient integration process. The rising demand for professional services underscores the healthcare sector's focus on achieving interoperability and adhering to stringent compliance requirements. This trend is expected to gain momentum, aligning with healthcare providers' priorities for operational excellence.

The market also segments based on deployment type, including EDI value-added networks (VANs), direct (point-to-point) EDI, web and cloud-based EDI, and mobile EDI. Among these, web and cloud-based EDI solutions dominated in 2024, and this segment is forecasted to generate USD 4.5 billion by 2034. Cloud-based solutions offer unmatched scalability and cost-efficiency, allowing healthcare organizations to expand operations without heavy hardware investments. These systems are particularly attractive to small and medium-sized providers seeking access to advanced tools without the burden of maintaining on-premises infrastructure. The flexibility, reliability, and affordability of cloud-based EDI make it a cornerstone of the market's growth trajectory.

North America accounted for USD 1.7 billion of the healthcare EDI market in 2024, fueled by strict regulatory requirements mandating standardized transactions and robust healthcare spending in the United States. As the industry prioritizes data-driven innovations, investments in digital infrastructure and AI-driven analytics continue to drive the adoption of advanced EDI solutions, reshaping the global landscape of healthcare data exchange.