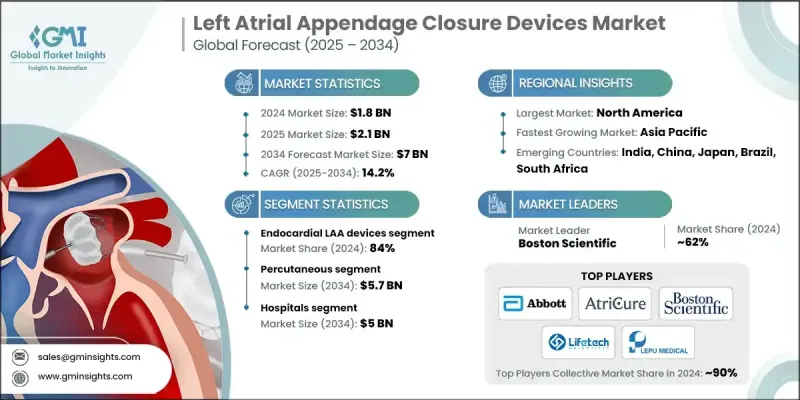

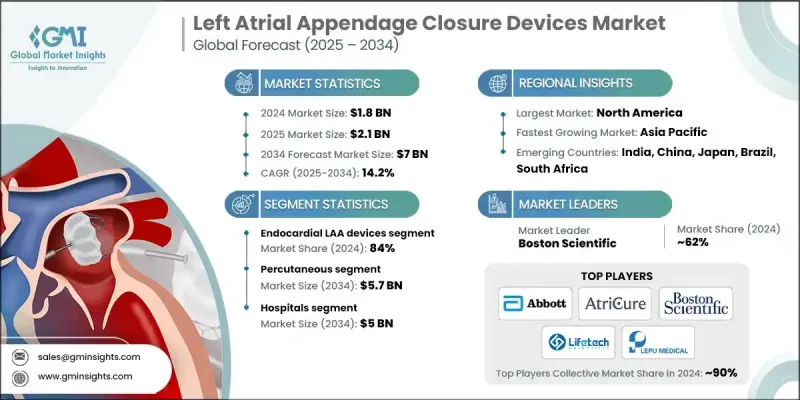

세계의 좌심방이 폐색 기기 시장은 2024년 18억 달러로 평가되었고 CAGR 14.2%로 성장해 2034년까지 70억 달러에 이를 것으로 추정되고 있습니다.

시장 확대의 배경으로는 심방세동의 이환율 상승, 침습성이 낮은 심혈관계 치료에 대한 선호도가 높아지고, 헬스케어 시스템 전체에서 상환 정책의 범위가 확대되기 때문입니다. 좌심방이 폐색 기기는 비판막증 심방세동으로 진단받은 환자에서 혈전 형성의 일반적인 부위인 좌심방이를 폐쇄하여 뇌졸중 위험을 줄이는 데 사용됩니다. 심방세동이, 특히 노인층에서 보다 일반적으로 됨에 따라, 이러한 뇌졸중 예방 솔루션에 대한 수요가 높아지고 있습니다. 세계 정부는 심방세동과 관련된 합병증과 관련된 장기 건강 관리 비용을 줄이기 위해 심혈관 치료에 대한 투자를 늘리고 있습니다. 또한 증가 자금은 일반 시민의 의식 향상 캠페인과 차세대 폐쇄 장비를 포함한 보다 진보된 치료 기술 연구를 지원합니다. 조기 진단과 혁신적인 기기 기반 치료 옵션을 강조함으로써 좌심방이 폐색 기기 산업은 전 세계적으로 유망한 전망을 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 18억 달러 |

| 예측 금액 | 70억 달러 |

| CAGR | 14.2% |

2024년 심장 내막형 좌심방이 폐색 기기 부문의 점유율은 84%였습니다. 이 기기는 강력한 임상시험의 실적, 의사의 광범위한 신뢰, 실제 세계에서의 성공적인 성공을 뒷받침하는 낮은 침습 접근법으로 널리 선택되었습니다. 이 디자인을 통해 의사는 카테터를 사용하는 절차로 좌심방이를 봉쇄하여 개심술을 필요로하지 않고 심방 세동 환자의 뇌졸중 위험을 줄일 수 있습니다. 이 분야는 회복에 필요한 시간이 짧고 장기적인 결과가 입증된 절차에 대한 수요가 높아지면서 계속 혜택을 받습니다.

경피 부문은 적응성과 인터벤셔널 카디올로지 인프라의 가용성이 확대됨에 따라 2034년까지 57억 달러에 이를 것으로 예측됩니다. 이 방법은 경험이 풍부한 임상의와 최신 카테터실 기술을 지원하며 병원과 심장 치료 센터와 같은 다양한 환경에서 절차를 수행 할 수 있습니다. 액세스의 용이성과 절차 안전성의 넓이는 이 시장에서 지배적인 절차로서의 지위를 확고하게합니다.

2024년 북미 좌심방이 폐색 기기 점유율은 46.2%였습니다. 이 지역은 첨단 건강 관리 인프라, 견고한 연구 개발 및 일관된 임상시험 활동을 지원하는 심장 구조 치료의 혁신의 선두 주자입니다. 고도로 전문화된 의료 센터가 존재하고 심장 수술의 훈련에 대한 액세스가 확산되고 있다는 것은 수술의 성장을 지원합니다. 또한 AI를 활용한 수술전 계획과 디지털 감시 툴 등의 기술적 진보가 좌심방이 폐쇄 분야에서 북미의 리더십을 더욱 강화하고 있습니다.

좌심방이 폐색 기기 시장에서 적극적으로 경쟁하는 유명한 기업으로는 MicroPort, Medtronic, LEPU MEDICAL, Abbott, AtriCure, Boston Scientific, Lifetech 등이 있습니다. 좌심방이 폐색 기기 시장 진출기업은 발판을 굳히기 위한 전략적 노력을 실시했습니다. 대부분은 이식의 용이성, 절차의 안전성, 장기적인 효과를 향상시키는 차세대 기기를 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 기업은 보다 신속한 규제 당국의 승인을 받아 임상 검증을 강화하기 위해 임상시험 파이프라인을 확대하고 있습니다. 병원 및 연구센터와의 전략적 제휴는 현장 교육 및 데이터 공유를 통해 의사 채용을 확대하기 위해 진행되고 있습니다.

The Global Left Atrial Appendage Closure Devices Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 14.2% to reach USD 7 billion by 2034.

Market expansion is driven by the rising incidence of atrial fibrillation, the growing preference for minimally invasive cardiovascular procedures, and the increasing scope of reimbursement policies across healthcare systems. LAA closure devices are used to reduce stroke risk in individuals diagnosed with non-valvular atrial fibrillation by sealing off the left atrial appendage, a common site for clot formation in such patients. As atrial fibrillation becomes more common, especially in aging populations, demand for these stroke prevention solutions is climbing. Governments around the world are investing more in cardiovascular care to mitigate long-term healthcare costs tied to AF-related complications. Increased funding also supports public awareness campaigns and research into more advanced treatment technologies, including next-generation closure devices. The emphasis on early diagnosis and innovative device-based therapy options is shaping a promising outlook for the LAA closure devices industry on a global scale.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $7 Billion |

| CAGR | 14.2% |

In 2024, the endocardial LAA closure device segment held an 84% share. These devices are widely chosen for their minimally invasive approach, backed by strong clinical trial performance, broad physician confidence, and successful real-world applications. Their design allows physicians to seal off the LAA through catheter-based procedures, lowering stroke risk in atrial fibrillation patients without the need for open-heart surgery. The segment continues to benefit from rising demand for procedures that offer shorter recovery times and proven long-term outcomes.

The percutaneous segment is projected to reach USD 5.7 billion by 2034, driven by its adaptability and the growing availability of interventional cardiology infrastructure. This method allows the procedure to be performed in a range of settings, including hospitals and cardiac care centers, supported by experienced clinicians and modern cath lab technology. Its widespread accessibility and procedural safety are helping to cement its position as the dominant technique in the market.

North America Left Atrial Appendage Closure Devices Market held 46.2% share in 2024. The region is a leader in structural heart care innovation, supported by advanced healthcare infrastructure, robust R&D, and consistent clinical trial activity. The presence of highly specialized medical centers and widespread access to training in cardiac procedures supports procedural growth. In addition, technological advancements such as AI-assisted preoperative planning and digital monitoring tools further reinforce North America's leadership in the LAA closure space.

Prominent companies actively competing in the Left Atrial Appendage Closure Devices Market include MicroPort, Medtronic, LEPU MEDICAL, Abbott, AtriCure, Boston Scientific, and Lifetech. Companies in the left atrial appendage closure devices market are implementing strategic initiatives to strengthen their foothold. Many are heavily investing in R&D to develop next-generation devices that improve ease of implantation, procedural safety, and long-term efficacy. Firms are expanding clinical trial pipelines to gain faster regulatory approvals and enhance clinical validation. Strategic partnerships with hospitals and research centers are being pursued to broaden physician adoption through hands-on training and data sharing.