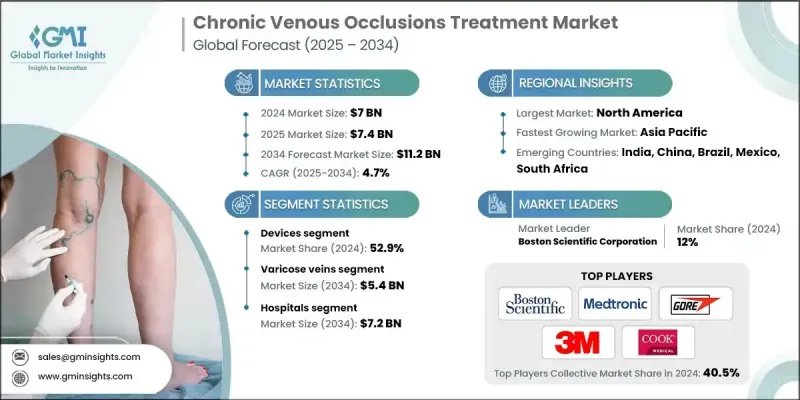

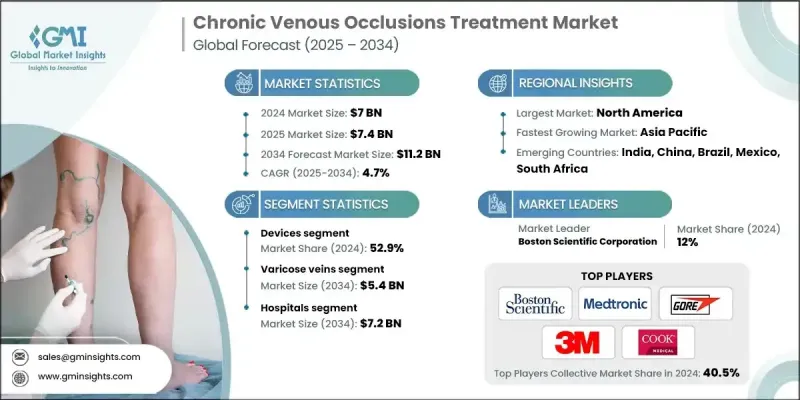

세계의 만성 정맥 폐색 치료 시장은 2024년 70억 달러로 평가되었으며 CAGR 4.7%로 성장해 2034년까지 112억 달러에 이를 것으로 추정됩니다.

꾸준한 성장의 배경으로는 정맥 질환 증가, 노인 인구 증가, 치료 접근법의 지속적인 기술 발전이 있습니다. 헬스케어 시스템이 환자의 예후 개선에 점점 더 중점을 두게 되는 가운데, 저침습 치료와 맞춤형 치료 전략의 채용이 큰 견인력이 되고 있습니다. 환자와 임상의 간의 의식이 높아짐에 따라 조기 진단과 적극적인 치료 계획이 널리 사용되고 있습니다. 헬스케어 캠페인, 환자 교육 프로그램, 상환 지원 확대가 업계 발전을 뒷받침하고 있습니다. 디지털 건강 기술과 전통적인 치료 모델의 융합은 치료 후 관리에도 변화를 가져왔습니다. 장비 제조업체, 의약품 개발 기업, 건강 관리 제공업체 등 밸류체인 전반의 기업이 전략적 파트너십을 맺고 혁신적인 솔루션을 도입하고 케어에 대한 접근성을 높이고 있습니다. 게다가 성숙한 경제권에서의 의료비 증가와 정책지원은 이 분야 전체의 미래 성장을 위한 견고한 기반을 구축하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 70억 달러 |

| 예측 금액 | 112억 달러 |

| CAGR | 4.7% |

만성 정맥 폐색 치료는 압박 요법, 의약품, 정맥 내 치료 및 디지털 모니터링 도구와 같은 다양한 접근법을 통해 장기 정맥 폐색 관리에 주력하고 있습니다. 이러한 치료는 정맥 혈류를 회복시키고, 합병증을 예방하고, 증상을 완화하며, 환자의 전반적인 삶의 질을 향상시킵니다. 근본적인 원인은 혈관의 흉터, 혈전증, 선천성 이상 등이 포함되는 경우가 많고, 이들이 장기적인 관리를 필요로 하는 만성적인 증상의 원인이 되고 있습니다.

2024년 장비 부문의 점유율은 52.9%였으며, 이는 저침습성 치료에 대한 선호도가 높아지고 고급 정맥내 치료 도구와 압박 시스템의 광범위한 사용으로 인해 발생합니다. 침습적인 외과 수술에서의 전환으로 회복이 빠르고 위험이 적은 치료법이 보급되고 있습니다. 절제 요법, 경화 요법, 최신 압박 착용과 같은 기술의 사용이 증가하고 있는 것은 이 동향을 반영합니다. 환자와 건강 관리 전문가 모두 일상 생활에 대한 지장을 최소화하고 효율적인 결과를 제공하는 솔루션을 점점 선호하고 있으며 최첨단 치료 장비에 대한 수요를 견인하고 있습니다.

정맥류 부문은 48.7%의 점유율을 차지하고 2034년까지 54억 달러에 이를 것으로 예측됩니다. 이 장점은 특히 노인과 앉아있는 라이프 스타일, 비만인 정맥 부전의 발생률이 높기 때문입니다. 정맥 내 레이저 및 고주파 절제술과 같은 저침습 솔루션으로의 전환은 시장 확대를 뒷받침하고 있습니다. 생활 습관과 관련된 요인과 사회적 의식 증가는 특히 40세 이상의 치료 희망 환자를 확대하고 있습니다.

2024년 북미 만성 정맥 폐색 치료 시장의 점유율은 40.1%이었습니다. 이 지역은 헬스케어 인프라가 정비되어 있어, 인지도가 높고, 신규 치료법의 조기 도입이 진행되고 있는 것이 주도적 지위에 공헌하고 있습니다. 만성부전 및 혈전증과 같은 정맥 합병증에 걸리기 쉬운 노인 인구 증가가 지속적인 수요에 박차를 가하고 있습니다. 또한 진단과 상환제도의 혁신도 이 지역 전체에서 첨단 치료의 강력한 보급을 지지하고 있습니다.

세계의 만성 정맥 폐색 치료 시장과 관련된 주요 기업은 Pfizer, Boston Scientific Corporation, Terumo, Medtronic, Tactile Medical, Coloplast, Gore, Bayer AG, Sanofi, Viatris, AngioDynamics, ConvaTec, Sciton, Leucadia Pharmaceuticals (Hikma), 3M, Cook Medical, and ConvaTec 등이 있습니다. 만성 정맥 폐색 치료 시장의 주요 기업은 안전성과 효능을 높이는 저침습 장치 및 신규 의약품 개발을 위한 연구 개발을 우선하고 있습니다. 전략적 M&A를 통해 제품 포트폴리오를 확장함으로써 기업은 보완적인 기술을 통합하고 시장 진입의 폭을 넓힐 수 있습니다. 또한 병원, 연구기관, 디지털 헬스 플랫폼과의 파트너십을 활용하여 환자 모니터링 및 장기적인 질병 관리를 개선하는 기업도 많습니다.

The Global Chronic Venous Occlusions Treatment Market was valued at USD 7 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 11.2 billion by 2034.

The steady growth is driven by a rising number of venous disorders, growing elderly populations, and continuous technological advancements across treatment approaches. With healthcare systems increasingly focused on improving patient outcomes, the adoption of minimally invasive therapies and personalized treatment strategies has gained significant traction. As awareness grows among both patients and clinicians, early diagnosis and proactive treatment planning are becoming more common. Healthcare campaigns, patient education programs, and expanded reimbursement support are helping propel industry development. The convergence of digital health technologies and traditional care models is also transforming post-treatment management. Companies across the value chain including device makers, pharmaceutical developers, and healthcare providers are forging strategic partnerships to introduce innovative solutions and enhance care accessibility. Additionally, increasing medical expenditure and policy support in mature economies have created a strong foundation for future growth across the sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 4.7% |

Chronic venous occlusions treatment focuses on managing long-term venous blockages through a range of approaches like compression therapy, pharmaceuticals, endovenous procedures, and digital monitoring tools. These treatments work to restore venous blood flow, prevent complications, reduce symptoms, and improve overall quality of life for affected patients. The underlying causes often include vascular scarring, thrombosis, and congenital abnormalities, which contribute to chronic symptoms requiring long-term management.

The devices segment held 52.9% share in 2024, attributed to the rising preference for less invasive treatments and broader use of advanced endovenous tools and compression systems. The shift away from invasive surgical options has led to the popularity of procedures with faster recovery and fewer risks. The growing use of techniques such as ablation therapy, sclerotherapy, and modern compression wear reflects this trend. Both patients and healthcare professionals increasingly favor solutions offering efficient outcomes with minimal disruption to daily life, driving demand for cutting-edge treatment devices.

The varicose veins segment held 48.7% share and is expected to reach USD 5.4 billion by 2034. This dominance is largely due to the high incidence of venous insufficiency, especially among older adults and those with sedentary lifestyles or obesity. The shift toward minimally invasive solutions like endovenous laser and radiofrequency ablation is reinforcing market expansion. Lifestyle-related factors and increasing public awareness are expanding the treatment-seeking patient base, particularly among individuals aged 40 and above.

North America Chronic Venous Occlusions Treatment Market held 40.1% share in 2024. The region's well-established healthcare infrastructure, high awareness levels, and early adoption of novel therapies contribute to its leadership position. A growing elderly population, more vulnerable to venous complications such as chronic insufficiency and thrombosis, is fueling continuous demand. Innovations in diagnostics and reimbursement systems have also supported strong uptake of advanced treatments throughout the region.

Key Players involved in the Global Chronic Venous Occlusions Treatment Market: Pfizer, Boston Scientific Corporation, Terumo, Medtronic, Tactile Medical, Coloplast, Gore, Bayer AG, Sanofi, Viatris, AngioDynamics, ConvaTec, Sciton, Leucadia Pharmaceuticals (Hikma), 3M, Cook Medical, and ConvaTec. Leading companies in the chronic venous occlusions treatment market are prioritizing R&D to develop minimally invasive devices and novel pharmaceuticals with enhanced safety and efficacy. Expanding product portfolios through strategic mergers and acquisitions allows firms to integrate complementary technologies and broaden market access. Many are leveraging partnerships with hospitals, research institutions, and digital health platforms to improve patient monitoring and long-term disease management.