U.S. Midstream Water for Hydraulic Fracturing: Market Trends, Opportunities, and Forecasts, 2025-2030

상품코드:1834222

리서치사:Bluefield Research

발행일:2025년 10월

페이지 정보:영문 120+ Pages

라이선스 & 가격 (부가세 별도)

한글목차

지난 10년간 수압파쇄는 미국의 에너지 정세를 완전히 바꾸어 놓았고, 미국을 세계 최대의 석유 및 가스 생산국으로 자리매김했습니다. 펜실베니아에서 텍사스까지 각 지역의 셰일 매장량을 활용함으로써, 수압파쇄는 세계 에너지 안보의 초석이 되고 있습니다. 미국은 현재 전 세계 석유 생산량의 40%, 천연가스 생산량의 37%를 차지하고 있습니다.

이러한 변화를 위해서는 물의 공급, 처리, 재활용, 재사용, 폐기를 포함한 중수 관리가 필수적입니다. 수평 우물 굴착은 최대 5마일에 걸쳐 진행되며, 1,200만 갤런 이상의 물이 필요하기 때문에 전례 없이 많은 양의 물이 발생하게 됩니다. 2030년까지 수원지에서 생산되는 부수적인 물의 양은 하루 5,000만 배럴에 달할 것으로 예상되며, 이는 처분 시설에 더 많은 부담을 주고, 특히 텍사스와 뉴멕시코에 걸쳐 있는 퍼미안 분지와 같이 활동량이 많은 지역에서는 규제 당국의 감시가 더욱 엄격해질 것으로 예상됩니다.

이러한 상황 변화에 따라 탐사 및 생산 기업과 중수 관리 기업은 보다 통합적인 물 솔루션을 추구하고 있습니다. 급수 및 수반수 파이프라인은 트럭 운송을 대체할 수 있는 대안이 되고 있으며, 수반수 재활용은 2030년까지 프래킹 용수 수요의 77% 이상을 충당할 수 있는 잠재력을 가지고 있습니다. 이러한 변화는 물 가치사슬 전반에 걸친 M&A, 파트너십 등 통합 활동과 함께 경쟁 구도를 재편하고 있습니다.

본 보고서는 미국의 수압파쇄용 중수 시장을 조사하고, 유전 물 관리의 미래에 영향을 미치는 주요 기업의 전략, 시장 촉진요인 및 예측, 유역별 역학 등을 종합적으로 분석하였습니다.

보고서 + 데이터 옵션

샘플 데이터 대시보드

소개할 기업

Antero Midstream Corporation

Apollo Global Management

Aqua Terra Water Management

Aquatech International

Bison Water Midstream

BlackBuck Resources

BlackRock Global Energy

Blackstone Energy Partners

Bosque Systems

Bregal Private Equity Partners

Caliber Midstream

Carlyle Group

Chevron

Clearlake Capital Group

CNX Resources

ConocoPhillips

Cresta Fund Management

Cudd Energy Services

Dalbo Holdings Inc

Deep Blue Midland Basin

Delek Logistic Partners

Devon Energy

Diamondback Energy

Dresser Utility Solutions

EIG Partners

EIV Capital, LLC

EnCap Flatrock Midstream

Energy Spectrum Capital

Enservco

EQT Partners

Eureka Resources

Evonik Industries

EVX Midstream Partners

ExxonMobil

Five Point Energy

Five Points Capital

Freestone Midstream

Genesis Park

GIC

Global Infrastructure Partners

Golden Gate Capital

Goodnight Midstream

Guggenheim Partners

Hess Midstream

I Squared Capital

Instar Asset Management

Key Energy Services

Kinetik

Layne Water Midstream

Lincolnshire Management

Magnetar Capital

Martin Midstream Partners

Martin Water Midstream

Matador Resources Company

Momentum Midstream

Morgan Stanley Energy Partners

NGL Water Solutions

Oasis Midstream Partners

Occidental Petroleum

Oneok

Permian Resources

Pilot Water Solutions

Plains All American

Platinum Equity

Post Oak Energy Capital

Quantum Energy Partners

Rattler Midstream LP

Riverside Company

RRIG Water Solutions

Select Water Solutions

Spectrum Water Technology

Steel Reef Infrastructure Corporation

Stonehill Environmental Partners

Summit Midstream Partners

Tailwater Capital

Tallgrass Energy Partners

Texas Pacific Land Corporation

TPG Capital

Trilantic Capital Partners

Veolia

Warburg Pincus

WaterBridge

Western Midstream Partners

Whiptail Midstream

White Deer Energy

XRI Water

Xylem

목차

섹션 1 - 석유 및 가스 상황의 정의

조사 방법 및 데이터 소스

중수 관리에 영향을 미치는 주요 요인

물 집약적 수압파쇄로 미국은 세계 최대 석유 생산국으로

미국, 세계 천연가스 공급국으로서의 역할 확보

석유 및 가스 가격의 변동이 전략을 형성

수평 시추 및 수압파쇄

수평 리그의 능력 : 깊이와 길이

수평 방향의 우물 길이는 물의 강도를 증가시킵니다.

시추 리그 수는 감소, 생산량은 계속 증가

미국 주요 셰일 분지 및 셰일층 지도

퍼미안 분지가 시추 리그 수와 활동을 뒷받침

파미안 분지의 비전통 가스 생산량 급증

시추 효율 저하로 신규 유정 완공 건수 소폭 감소

미국 LNG 수출 증가로 물 수요 증가

섹션 2 - 중수 시장의 촉진요인, 동향 및 과제

중수의 촉진요인과 영향

우물당 수압파쇄용수 사용량

우물 마감용수의 총 사용량은 꾸준히 증가

주요 유역 전체에서 우물물 공급 총량이 계속 증가

미국 서부와 남부에서 물 스트레스가 가장 심각하게 증가

폐기물 처리에 따른 지진 발생으로 물 재사용 확대 정책이 추진

연방정부 정책은 거의 변동 없음

주 및 지방 정책 개요

섹션 3 - 중수 시장 규모 및 예측

시장 예측 기법 개요

중수 가치사슬

가치사슬 전반에 걸친 중수 동향

예측 부문

석유 및 가스 부문의 물 관리 서비스 지출 : 유역별

우물당 물 사용량은 2030년까지 계속 증가할 것

재활용에 따른 물 수요 증가에 따른 물 공급량 증가

미국 유역 전체에서 수량이 증가할 것으로 예상

유역 재활용률은 완만하게 증가하여 폐기물을 상쇄할 것으로 예상

설비투자 증가는 인프라 확장의 신호

중수용 설비투자 세분화

재활용시설 설비투자 : 유형별, 규모별

미래의 물 솔루션과 서비스를 위한 혁신과 투자의 촉진요인

주요 기회 : 유역별, 주별(2025-2030년)

섹션 4 - 유역 및 셰일층 프로필

Anadarko

Appalachia

Bakken

Eagle Ford

Haynesville

Niobrara-DJ(Denver-Julesburg)

Permian

섹션 5 - 경쟁 상황

중수 경쟁 세트

중수 경쟁 포지셔닝

M&A 동향 : 경쟁 부문별(2020-2025년)

물 전문업체 M&A 활동 : 소유 유형별

시장 점유율 : 파이프라인 인프라의 지속적인 확대

물 관련 인수합병(2020-2025년)

Antero Midstream Corporation

Aqua Terra Water Management

Bison Water Midstream

Blackbuck Resources

Bosque Systems

CNX Water

Dalbo Holdings Inc

Deep Blue Midland Basin

Delek Logistics Partners, LP

Dresser Utility Solutions

EQT Corporation

Freestone Midstream

Goodnight Midstream

Hess Midstream

NGL Water Solutions

Layne Water Midstream

Martin Water Midstream

Pilot Water Solutions

RRIG Water Solutions

Select Water Solutions

Stonehill Environmental Partners

Tallgrass Water

Texas Pacific Land Corporation

WaterBridge

Western Midstream

XRI Water

KSM

영문 목차

영문목차

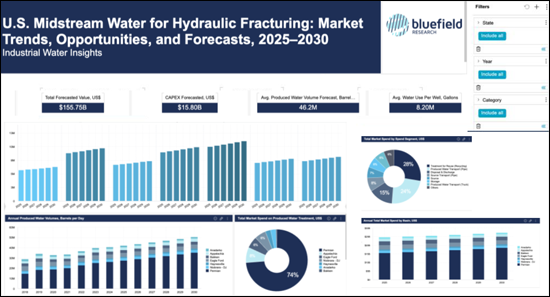

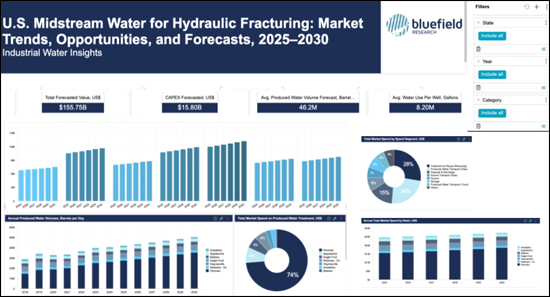

Over the last decade, hydraulic fracturing has transformed the U.S. energy landscape, establishing the country as the world's largest producer of oil and gas. By tapping into shale reserves across regions from Pennsylvania to Texas, fracking has become a cornerstone of global energy security. The U.S. now contributes nearly 40% of global oil production and 37% of natural gas production.

Midstream water management, which involves the supply, treatment, recycling, reuse, and disposal of water, is critical to this transformation. Horizontal well completions can extend up to five miles and require over 12 million gallons of water, resulting in unprecedented volumes of produced water. By 2030, the volume of produced water at wellheads is projected to reach 50 million barrels per day, placing additional stress on disposal facilities and fueling regulatory scrutiny, particularly in high-activity regions like the Permian Basin, which spans Texas and New Mexico.

In this evolving context, exploration and production companies and midstream water management players are pursuing more integrated water solutions. Water supply and produced water pipelines are becoming viable alternatives to trucking and produced water recycling is on track to meet over 77% of fracking water demand by 2030. These shifts, accompanied by consolidation efforts such as mergers and acquisitions and partnerships across the water value chain, are reshaping the competitive landscape.

This Insight Report provides a comprehensive analysis of U.S. midstream water management, encompassing market drivers and forecasts, basin-level dynamics, and the strategies of leading players that are influencing the future of oilfield water management.

Report+Data Option

SAMPLE DATA DASHBOARD

Data is a key component to this analysis. Our team has compiled relevant data dashboards.

Industrial Water Market Corporate Subscription seat holders can access related dashboards.

Companies Mentioned:

Antero Midstream Corporation

Apollo Global Management

Aqua Terra Water Management

Aquatech International

Bison Water Midstream

BlackBuck Resources

BlackRock Global Energy

Blackstone Energy Partners

Bosque Systems

Bregal Private Equity Partners

Caliber Midstream

Carlyle Group

Chevron

Clearlake Capital Group

CNX Resources

ConocoPhillips

Cresta Fund Management

Cudd Energy Services

Dalbo Holdings Inc

Deep Blue Midland Basin

Delek Logistic Partners

Devon Energy

Diamondback Energy

Dresser Utility Solutions

EIG Partners

EIV Capital, LLC

EnCap Flatrock Midstream

Energy Spectrum Capital

Enservco

EQT Partners

Eureka Resources

Evonik Industries

EVX Midstream Partners

ExxonMobil

Five Point Energy

Five Points Capital

Freestone Midstream

Genesis Park

GIC

Global Infrastructure Partners

Golden Gate Capital

Goodnight Midstream

Guggenheim Partners

Hess Midstream

I Squared Capital

Instar Asset Management

Key Energy Services

Kinetik

Layne Water Midstream

Lincolnshire Management

Magnetar Capital

Martin Midstream Partners

Martin Water Midstream

Matador Resources Company

Momentum Midstream

Morgan Stanley Energy Partners

NGL Water Solutions

Oasis Midstream Partners

Occidental Petroleum

Oneok

Permian Resources

Pilot Water Solutions

Plains All American

Platinum Equity

Post Oak Energy Capital

Quantum Energy Partners

Rattler Midstream LP

Riverside Company

RRIG Water Solutions

Select Water Solutions

Spectrum Water Technology

Steel Reef Infrastructure Corporation

Stonehill Environmental Partners

Summit Midstream Partners

Tailwater Capital

Tallgrass Energy Partners

Texas Pacific Land Corporation

TPG Capital

Trilantic Capital Partners

Veolia

Warburg Pincus

WaterBridge

Western Midstream Partners

Whiptail Midstream

White Deer Energy

XRI Water

Xylem

Table of Contents

Section 1 - Defining the Oil & Gas Landscape

Research Methodology and Data Sources

Key Factors Influencing Midstream Water Management

Water-Intensive Fracking Makes U.S. the Leading Global Oil Producer

U.S. Secures Role as Global Supplier of Natural Gas

Swings in Oil & Gas Prices Shape Strategies

Horizontal Drilling and Hydraulic Fracturing

Horizontal Rig Capabilities: Depths and Lengths

Horizontal Wellbore Lengths Increase Water Intensity

Rig Counts Decline, Production Continues to Climb

Mapping the Key U.S. Shale Basins and Plays

Permian Basin Underpins Drill Rig Counts and Activity

Permian Basin Surges in Unconventional Gas Production

New Well Completions Decline Slightly With Drilling Efficiencies

Increase in U.S. LNG Exports Drives Water Demand

Section 2 - Midstream Water Market Drivers, Trends, and Challenges

Midstream Water Drivers and Impacts

Hydraulic Fracturing Water Use per Well

Total Water Use for Well Completions Grew Steadily

Total Well Water Supply Volumes Continue to Grow Across Top Basins

Water Stress to Increase Most Acutely in Western and Southern U.S.

Seismic Events from Disposal Push Policy for Expanded Water Reuse

Federal Policy Remains Largely Unchanged

State & Local Policy Overview

Section 3 - Midstream Water Market Size and Forecasts

Market Forecast Methodology Overview

The Midstream Water Value Chain

Midstream Water Trends Across the Value Chain

Forecasted Segments

Oil & Gas Sector Spend on Water Management Services by Basin

Increasing Water Usage per Well Continues Through 2030

Water Demand Increasingly Supplied by Recycled Produced Water

Produced Water Volumes Set to Increase Across U.S. Basins

Basin Recycling Rates Projected to Grow Modestly, Offset Disposal

CAPEX Growth Signals Infrastructure Expansion

Segmenting Capital Expenditures for Midstream Water

CAPEX Recycling Facility Growth by Type and Size

Drivers of Innovation and Investment for Future Water Solutions & Services

Top Opportunities by Basin and State (2025-2030)

Section 4 - Basin & Shale Play Profiles

Anadarko

Appalachia

Bakken

Eagle Ford

Haynesville

Niobrara-DJ (Denver-Julesburg)

Permian

Section 5 - Competitive Landscape

Midstream Water Competitive Set

Midstream Water Competitive Positioning

M&A Trends by Competitive Segment (2020-2025)

Water Pure-Play M&A Activity by Ownership Type

Market Share: Pipeline Infrastructure Expansion to Continue