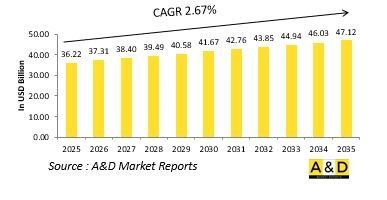

세계의 해군 수상 함정 시장 규모는 2025년에 362억 2,000만 달러로 추정되며, 2035년까지 471억 2,000만 달러로 성장할 것으로 예측되고 있으며, 예측 기간인 2025-2035년의 연평균 성장률(CAGR)은 2.67%에 달할 전망입니다.

해군 수상함정 시장은 해상 전력 투사, 억지력, 전략적 우위의 핵심으로 구축함, 호위함, 코르벳함, 초계함, 항공모함 등 다양한 플랫폼을 포괄하고 있습니다. 이 함정들은 각국이 항로를 확보하고, 해양 주권을 행사하고, 원정 임무를 수행하며, 새로운 안보 도전에 대응할 수 있도록 함으로써 해군 활동의 중추적인 역할을 합니다. 현대의 수상전투함은 첨단 센서, 무기체계, 지휘통제 능력을 갖추고 있으며, 다지역 환경에서 효과적으로 활동할 수 있습니다. 수상전투함은 대공, 대수상, 대잠수함전뿐만 아니라 인도적 지원, 재난구호, 해양안보 활동에서도 중요한 역할을 담당하고 있습니다. 해군 수상함정의 전략적 가치는 전투 능력뿐만 아니라 외교적 수단으로서의 역할도 수행하고 있으며, 연합훈련과 항행의 자유 작전을 통해 국가의 영향력을 과시하고 동맹 관계를 촉진하고 있습니다. 해양 위협이 점점 더 고도화됨에 따라 기술적으로 진보하고 여러 임무를 수행할 수 있는 함정에 대한 수요가 증가하고 있습니다. 각국은 운영의 유연성과 적응성을 보장하기 위해 모듈식 설계, 스텔스 기술, 네트워크 중심 시스템에 투자하고 있습니다. 지정학적 경쟁이 심화되고 해상 무역로의 전략적 중요성이 커지는 가운데, 해군 수상함정은 세계의 안정을 유지하고 해상에서 국익을 확보하는 데 있으며, 필수적인 존재로 자리매김하고 있습니다.

기술 혁신은 해군 수상함정의 설계, 능력, 운용 효과를 변화시키고 있습니다. 스텔스 기술의 발전으로 레이더 단면적이 감소하고 생존성이 향상되어 함정은 경쟁 환경에서도 발견되지 않고 활동할 수 있습니다. 통합전투체계와 네트워크 중심 아키텍처는 원활한 정보 공유와 공중, 해상, 육상, 우주 각 영역에 걸친 협동작전을 가능하게 합니다. 모듈식 설계와 개방형 아키텍처 설계를 채택하여 여러 임무에 맞게 함정을 재구성할 수 있으며, 운영 수명을 연장하고 업그레이드 비용을 절감할 수 있습니다. 하이브리드 전기 및 통합 전력 시스템을 포함한 추진력의 발전은 연료 효율성, 내구성, 첨단 센서 및 지향성 에너지 무기를 위한 전력 가용성을 향상시키고 있습니다. 자동화와 인공지능은 개인보호구(PPE)를 강화하고, 승무원의 작업 부하를 최적화하며, 예지보전을 가능하게 합니다. 또한 첨단 레이더, 소나, 전자전 시스템은 점점 더 복잡해지는 위협에 대한 감지, 추적, 교전 능력을 향상시키고 있습니다. 무인 지상 및 공중 차량과 수상 함정과의 통합은 작전 범위와 유연성을 더욱 확장하고 있습니다. 이러한 기술 개발로 해군의 수상전투함은 진화하는 위협에 신속하게 대응할 수 있는 첨단 적응력을 갖춘 다중 임무 플랫폼으로 재정의되고 있습니다. 그 결과, 현대의 수상함정은 복잡한 해양 안보 환경에서 더욱 강력하고 생존 가능하며 전략적으로 가치 있는 선박으로 거듭나고 있습니다.

몇 가지 전략적 요구가 해군 수상함정 시장의 성장을 가속하고 있습니다. 지정학적 긴장과 영토 분쟁 증가는 각국이 해양 우위를 주장하고 국익을 보호하기 위해 수상 함대를 강화하도록 촉구하고 있습니다. 세계 무역로와 배타적 경제수역 확보의 중요성이 커지면서 첨단 수상전투함 투자에 박차를 가하고 있습니다. 멀티 도메인 작전 및 네트워크 중심 전쟁으로의 전환은 통합군 및 동맹군과 원활하게 통합할 수 있는 함정에 대한 수요를 창출하고 있습니다. 노후화된 함대를 고성능 모듈형 함정으로 대체하는 것을 목표로 하는 해군 현대화 계획은 시장 활동의 주요 촉진제가 되고 있습니다. 또한 대함 미사일, 군집 전술, 비대칭 해양 과제 등 고도화된 위협의 확산으로 인해 해군은 보다 민첩하고 생존성이 높으며 기술적으로 정교한 플랫폼의 채택을 요구하고 있습니다. 또한 해군의 원정 능력과 청해 능력에 대한 우선순위가 높아지면서 항속거리, 내구성, 임무 유연성이 높은 함정에 대한 수요가 증가하고 있습니다. 또한 국제 협력, 공동 개발 구상, 방위산업 파트너십은 능력 향상과 비용 분담을 지원하고 있습니다. 이러한 요인들을 종합하면 해상 우위를 달성하고, 전력을 투사하고, 점점 더 분쟁이 치열하고 복잡해지는 해역에서 안보를 유지하는 데 있으며, 수상함정의 전략적 중요성을 강조하고 있습니다.

해군 수상함정 시장은 안보 우선순위, 전략적 야망, 국방 현대화 목표의 영향을 받아 뚜렷한 지역적 추세를 보이고 있습니다. 북미에서는 스텔스성, 종합력, 첨단 무기체계를 강화한 차세대 구축함, 호위함, 항공모함에 중점적으로 투자하고 있습니다. 유럽 국가들은 신속한 배치, 동맹의 상호 운용성, 해상 안보 역량을 강화하기 위해 모듈형 함정 및 다중 임무 함정을 우선시하고 있습니다. 아시아태평양은 급속한 팽창을 경험하고 있으며, 각국은 수상 함대를 강화하고, 영유권을 주장하고, 항로를 확보하며, 역내 긴장이 고조되는 가운데 힘을 과시하고 있습니다. 중동의 해군은 전략적 수로, 해양 자산, 중요 인프라를 보호하기 위해 종종 유럽 및 미국 조선사와의 제휴를 통해 첨단 수상 전투함을 확보하고 있습니다. 라틴아메리카와 아프리카에서는 해안 방어, 해적 퇴치, 해상 법 집행 임무를 위해 비용 효율적인 순찰선 및 연안 함정을 중심으로 조달이 진행되고 있습니다. 어느 지역이든 국내 조선 능력과 기술이전 협정이 중요시되고 있는데, 이는 방산 자립을 추구하는 광범위한 움직임을 반영하는 것입니다. 공동 프로그램 및 다자간 훈련도 함대 개발의 우선순위를 형성하고 있습니다. 이러한 지역 역학은 국방 전략, 해양 안보, 그리고 세계 해역의 전략적 균형 유지에 있으며, 해군 수상함정의 중심적인 역할을 강조하고 있습니다.

고아 조선소(GSL) 및 콜카타의 가든리치 조선소(GRSE)와 총 97억 8,100만 루피 규모의 차세대 해상초계함(NGOPV) 11척(인도 IDDM) 구매 계약이 체결되었습니다. 이 11척 중 7척은 GSL이 독자적으로 설계, 개발, 제작하고 4척은 GRSE가 건조합니다. 인도는 2026년 9월에 시작될 예정입니다. 이들 함정의 도입으로 인도 해군의 작전 태세가 강화되어 대해적, 대침투, 대밀렵, 대인신매매, 비전투원 대피, 수색 및 구조(SAR), 해상 자산 보호 등의 임무를 지원할 수 있게 됩니다. 또한 이 건설 프로그램을 통해 7년 반 동안 약 1,100만 명의 일자리가 창출될 것으로 예측됩니다.

지역별

플랫폼별

용도별

이 장에서는 10년간 해군 수상함 시장 분석에 의해 해군 수상함 시장의 성장, 변화하는 동향, 기술 채택의 개요 및 전체적인 시장의 매력의 상세한 개요가 제공됩니다.

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10 기술과 이러한 기술이 시장 전체에 미칠 가능성이 있는 영향에 대해 설명합니다.

이 시장의 10년간 해군 수상함 시장 예측은 상기 부문 전체에 걸쳐서 상세하게 다루어지고 있습니다.

이 부문에서는 지역별 해군 수상 함정 시장의 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술이라는 측면을 다루고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 상세하게 다루고 있습니다. 지역 분석 최종 단계에서는 주요 기업의 프로파일링, 공급업체의 상황, 기업 벤치마킹 등에 대해 분석하고 있습니다. 현재 시장 규모는 일반 시나리오에 기반하여 추정되고 있습니다.

북미

촉진요인, 억제요인, 과제

PEST

주요 기업

공급업체 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

이 장에서는 이 시장의 주요 방위 프로그램을 다루고, 이 시장에서 신청된 최신 뉴스 및 특허에 대해서도 해설합니다. 또한 국가 레벨의 10년간 시장 예측과 시나리오 분석에 대해서도 해설합니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장에서의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

기회 매트릭스는 독자가 이 시장에서 기회가 높은 부문을 이해하는데 도움이 됩니다.

이 시장의 분석의 가능성에 대해 당사 전문가의 의견을 전해드립니다.

The Global Naval Surface Vessels market is estimated at USD 36.22 billion in 2025, projected to grow to USD 47.12 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.67% over the forecast period 2025-2035.

The defense naval surface vessels market is a cornerstone of maritime power projection, deterrence, and strategic dominance, encompassing a diverse range of platforms such as destroyers, frigates, corvettes, patrol vessels, and aircraft carriers. These vessels serve as the backbone of naval operations, enabling countries to secure sea lanes, enforce maritime sovereignty, conduct expeditionary missions, and respond to emerging security challenges. Modern surface combatants are equipped with advanced sensors, weapon systems, and command-and-control capabilities, allowing them to operate effectively in multi-domain environments. They play a crucial role in anti-air, anti-surface, and anti-submarine warfare, as well as in humanitarian assistance, disaster relief, and maritime security operations. The strategic value of naval surface vessels extends beyond combat capabilities-they also serve as diplomatic instruments, projecting national influence and fostering alliances through joint exercises and freedom of navigation operations. With maritime threats becoming increasingly sophisticated, the demand for technologically advanced, multi-mission-capable vessels is rising. Nations are investing in modular designs, stealth technologies, and network-centric systems to ensure operational flexibility and adaptability. As geopolitical competition intensifies and maritime trade routes gain strategic importance, naval surface vessels remain essential for maintaining global stability and securing national interests at sea.

Technological innovation is transforming the design, capabilities, and operational effectiveness of naval surface vessels. Advances in stealth technology are reducing radar cross-sections and enhancing survivability, allowing ships to operate undetected in contested environments. Integrated combat systems and network-centric architectures are enabling seamless information sharing and coordinated operations across air, sea, land, and space domains. The adoption of modular and open-architecture designs allows vessels to be reconfigured for multiple missions, extending their operational life and reducing upgrade costs. Propulsion advancements, including hybrid-electric and integrated power systems, are improving fuel efficiency, endurance, and power availability for advanced sensors and directed-energy weapons. Automation and artificial intelligence are enhancing Personal Protective Equipment, optimizing crew workload, and enabling predictive maintenance. Additionally, advanced radar, sonar, and electronic warfare systems are improving detection, tracking, and engagement capabilities against increasingly complex threats. The integration of unmanned surface and aerial vehicles with surface ships is further expanding operational reach and flexibility. These technological developments are redefining naval surface combatants as highly adaptive, multi-mission platforms capable of responding rapidly to evolving threats. As a result, modern surface vessels are becoming more capable, survivable, and strategically valuable in complex maritime security environments.

Several strategic imperatives are driving the growth of the naval surface vessels market. Rising geopolitical tensions and territorial disputes are prompting nations to strengthen their surface fleets to assert maritime dominance and protect national interests. The increasing importance of securing global trade routes and exclusive economic zones is fueling investments in advanced surface combatants. The shift toward multi-domain operations and network-centric warfare is creating demand for ships that can integrate seamlessly with joint and allied forces. Naval modernization programs aimed at replacing aging fleets with highly capable, modular vessels are a key driver of market activity. Additionally, the proliferation of advanced threats-including anti-ship missiles, swarm tactics, and asymmetric maritime challenges-is pushing navies to adopt more agile, survivable, and technologically sophisticated platforms. Expeditionary and blue-water naval capabilities are also gaining priority, driving the demand for vessels with greater range, endurance, and mission flexibility. Furthermore, international collaboration, joint development initiatives, and defense industrial partnerships are supporting capability enhancement and cost-sharing. These factors collectively highlight the strategic importance of surface vessels in achieving maritime superiority, projecting power, and maintaining security in increasingly contested and complex naval theaters.

The naval surface vessels market demonstrates distinct regional trends influenced by security priorities, strategic ambitions, and defense modernization goals. In North America, significant investments focus on next-generation destroyers, frigates, and carriers with enhanced stealth, integrated power, and advanced weapon systems. European countries are prioritizing modular and multi-mission vessels to enhance rapid deployment, alliance interoperability, and maritime security capabilities. The Asia-Pacific region is experiencing rapid expansion, with nations strengthening their surface fleets to assert territorial claims, secure sea lanes, and project power amid rising regional tensions. Middle Eastern navies are acquiring advanced surface combatants to protect strategic waterways, offshore assets, and critical infrastructure, often through partnerships with Western shipbuilders. In Latin America and Africa, procurement efforts are centered on cost-effective patrol and littoral vessels for coastal defense, counter-piracy, and maritime law enforcement missions. Across all regions, there is a strong emphasis on domestic shipbuilding capabilities and technology transfer agreements, reflecting a broader push for defense self-reliance. Collaborative programs and multinational exercises are also shaping fleet development priorities. These regional dynamics underscore the central role of naval surface vessels in national defense strategies, maritime security, and the maintenance of strategic balance across global waters.

A contract for the procurement of 11 Next Generation Offshore Patrol Vessels (NGOPVs) under the Buy (Indian-IDDM) category has been signed with Goa Shipyard Ltd (GSL) and Garden Reach Shipbuilders & Engineers (GRSE), Kolkata, at a total cost of Rs 9,781 crore. Of these 11 vessels, GSL will indigenously design, develop, and manufacture seven, while GRSE will build four. Deliveries are scheduled to begin in September 2026. The induction of these ships will enhance the Indian Navy's operational readiness, supporting missions such as anti-piracy, counter-infiltration, anti-poaching, anti-trafficking, non-combatant evacuation operations, search and rescue (SAR), and protection of offshore assets. The construction program is also expected to generate approximately 11 million man-days of employment over a span of seven and a half years.

By Region

By Platform

By Application

The 10-year naval surface vessels market analysis would give a detailed overview of naval surface vessels market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year naval surface vessels market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional naval surface vessels market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.