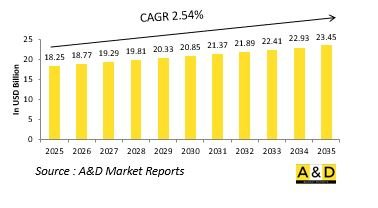

세계의 특수 목적 육상 차량 시장은 2025년 182억 5,000만 달러로 추정되며, 2035년까지 234억 5,000만 달러로 성장할 것으로 예측되고 있으며, 2025-2035년 연평균 복합 성장률(CAGR)은 2.54%가 될 것으로 보입니다.

방어용 특수 목적 육상 차량은 세계 방위 산업의 중요한 부문을 형성하고 표준 군사 플랫폼에서 효과적으로 해결할 수 없는 임무를 해결하기 위해 제조됩니다. 이러한 차량은 전술적인 기동성과 정찰부터 지휘, 기술 지원, 복구 작업에 이르기까지 특정 기능을 염두에 두고 설계되었습니다. 그 주요 강점은 다양한 지형과 임무 요건에 적응할 수 있는 능력에 있으며, 전투와 지원 역할 모두에 필수적입니다. 기존의 장갑차와 수송차와 달리 복잡한 환경에의 적합성을 높이기 위해서, 특수한 시스템, 장비, 구조적인 개조가 실시되고 있습니다. 시장은 전쟁과 안보 요구의 진화에 의해 형성됩니다. 현대 분쟁은 방어력과 화력뿐만 아니라 신속한 적응성, 물류 효율, 임무에 특화된 성능을 요구합니다. 그 결과, 이러한 차량의 설계와 조달은 모듈성, 생존성, 보다 광범위한 전략 네트워크와의 통합에 중점을 둡니다. 이 차량은 부대를 지원하고 공급망을 확보하며 도전 시나리오에서 부대의 기동성을 가능하게 하는 지상 수준의 백본 역할을 합니다. 적극적인 전투, 인도적 지원, 분쟁지에서의 인프라 수복에 전개되더라도, 방위용 특수 목적 육상 차량은 군가 능력, 회복력, 작전상의 범용성을 유지할 수 있도록 하는데 중요한 역할을 하고 있습니다.

방어 특수 임무기 형성에서 기술의 역할은 점차 현저해지고 있으며, 능력 강화와 임무의 유효성을 모두 추진하고 있습니다. 첨단 기술은 이러한 플랫폼을 고도로 네트워크화된 자산으로 변모시켜 정보 수집, 모니터링, 전자전, 통신 지원의 교차로에서 운영합니다. 최신 센서 제품군을 통합하면 전례 없는 정확도로 여러 영역에서의 활동을 감지, 추적 및 분석할 수 있는 능력을 제공합니다. 이러한 개선으로 부대는 복잡하고 갈등이 있는 환경에서도 상황 인식을 유지할 수 있습니다. 디지털화는 핵심 주제로, 실시간 정보 공유와 지상, 해군, 우주 자산과의 상호 운용성을 가능하게 합니다. 항공기는 이제 날아다니는 사령탑 역할을 하며, 중요한 정보를 즉시 의사결정자나 전선부대에게 전송합니다. 인공지능과 머신러닝과 같은 새로운 기술은 예측 통찰력을 제공하고 위협 감지 측면을 자동화함으로써 임무 계획 및 실행을 더욱 최적화합니다. 재료 과학과 추진력의 혁신도 그 날개를 담당하여 내구성의 연장과 효율의 향상을 가능하게 하고 있습니다. 게다가, 전자전과 사이버 보안 대책은 적이 통신과 센서의 성능을 방해하려고 할 수 있는 경쟁이 심한 전장에서 이러한 항공기가 계속 효과적이라는 것을 보장합니다. 이러한 진보를 종합하면 기술이 특수 임무기의 진화에 결정적인 영향을 미친다는 것을 알 수 있습니다.

방어용 특수 목적 육상 차량 수요는 안전 보장 요구, 운영 요구 사항 및 기술적 기회의 조합에 의해 형성됩니다. 성장을 가속하는 주요 요인은 위협 성격의 변화이며, 군은 보통 전과 비정규전 시나리오 모두에 대비해야 합니다. 특수 목적 차량은 이러한 다양성을 다루는 데 필요한 맞춤형 능력을 제공하며 표준 군용 플랫폼에서는 달성할 수 없는 강화된 보호, 기동성 및 임무별 장비를 제공합니다. 또 다른 원동력은 탄력성과 병력 보호의 필요성에 있습니다. 현대 분쟁에서는 매복과 즉석 폭발 장치와 같은 비대칭 전술이 종종 사용되기 때문에 고급 장갑, 방어 시스템, 높은 생존성 기준을 갖춘 차량이 필요합니다. 군는 또한 속도와 기동성의 중요성을 인식하고 있으며, 안전성을 손상시키지 않고 도시 경관, 원격지, 험한 지형에서 활동할 수 있는 차량이 필요합니다. 경제적, 물류적 고려가 수요를 더욱 형성하고 있습니다. 모듈형 차량과 멀티롤 차량은 라이프사이클 비용을 절감하고 여러 임무를 지원함으로써 플릿의 실용성을 극대화할 수 있기 때문에 매력적입니다. 전투뿐만 아니라 인도적 지원, 평화 유지 및 인프라 복구에서 군의 역할이 증가함에 따라 다용도 차량의 사례가 강화되었습니다. 이러한 국방적 필요성과 민생적인 유용성의 융합으로 시장은 전략적으로 중요한 위치를 차지하고 있습니다.

방위용 특수 목적 육상 차량의 지역별 수요는 각각 다른 작전 환경, 전략적 우선사항, 산업 능력을 반영하고 있습니다. 국경이 넓고 종종 분쟁이 발생하는 국가에서는 지속적인 모니터링과 신속한 반응 능력을 보장하는 정찰 차량과 순찰 차량이 우선합니다. 산, 사막, 밀림 등 지형이 심한 국가는 오프로드 내구성, 물류, 엔지니어링 작업에 최적화된 플랫폼을 요구합니다. 이러한 지리적 요인은 조달 선택에 큰 영향을 미치며 지역에 따라 요구 사항이 달라집니다. 기술 첨단 지역에서는 현대화와 디지털 시스템의 통합이 중요합니다. 군은 동맹군과의 상호 운용성을 보장하기 위해 모듈 구성, 고급 보호 대책 및 네트워크 대응 기능을 갖춘 차량을 선호합니다. 이와는 대조적으로 신흥국에서는 다양한 임무에 적응하면서 확실한 성능을 발휘하는 비용 효율적인 다목적 플랫폼이 선호되는 경우가 많습니다. 이 현실적인 접근 방식은 예산 제약과 전략 효과의 균형을 맞출 수 있습니다. 또한 비전투 임무도 지역 전략에 영향을 미치고 있습니다. 자연재해에 휩쓸리기 쉬운 지역에서는 구원이나 재건을 위해서 배치할 수 있는 차량에 투자하는 한편, 평화 유지에 종사하는 나라에서는 안정화 활동을 위한 기동성과 보호에 중점을 두고 있습니다. 국내 산업 능력도 중요한 역할을 하고 있으며, 자국에서의 개발을 중시하는 나라도 있고, 제휴나 수입을 추구하는 나라도 있습니다. 이러한 다양성에 의해 지역의 우선사항이나 세계의 동향에 맞추어 지역 시장이 발전해 가는 것입니다.

핀란드 국방군 물류 사령부(FDFLOGCOM)는 Patria XA-300(6X6) 장갑 병원 수송차 29량을 3,650만 유로(4,050만 달러)로 구입하여 확대 조달 계약의 최종 단계를 종료했습니다. 이 차량은 핀란드 육군의 작전 능력을 강화하고 2060년대까지 사용될 것으로 예상되는 현대적인 기동 자산을 제공합니다. 이번 주문은 최대 70 유닛의 추가 옵션을 포함한 2023년 계약의 최종 단계입니다. 이번 조달로 Patria XA-300의 모든 차량은 당초 91량을 대상으로 하고, 추가로 70량의 옵션을 붙인 당초 계약의 전 범위에 가까워지게 됩니다.

용도별

지역별

유형별

이 장에서는 10년간의 특수 목적 육상 차량 시장 분석을 통해 특수 목적 육상 차량 시장의 성장, 변화하는 동향, 기술 채용의 개요, 전체 시장의 매력 상세한 개요를 제공합니다.

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10개 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

이 시장의 10년간 예측은 위의 부문에 걸쳐 자세히 설명되어 있습니다.

이 부문은 지역별 특수 목적 육상 차량 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술 등의 측면을 망라하고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 자세히 다루고 있습니다. 지역 분석의 끝에는 주요 기업 프로파일링, 공급업체 상황, 기업 벤치마킹가 포함됩니다. 현재 시장 규모는 일반적인 시나리오를 기반으로 추정됩니다.

북미

촉진요인, 억제요인, 과제

PEST

주요 기업

공급자 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

이 장에서는 이 시장에서 주요 방어 프로그램을 다루며 이 시장에서 신청된 최신 뉴스와 특허에 대해서도 설명합니다. 또한 국가 수준의 10년간 시장 예측과 시나리오 분석에 대해서도 설명합니다.

미국

방어 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

기회 행렬은 독자가 이 시장에서 기회의 높은 부문을 이해하는 데 도움이 됩니다.

이 시장에서 가능한 분석에 대한 당사의 전문가의 의견을 제공합니다.

The Global Special Purpose Land Vehicles market is estimated at USD 18.25 billion in 2025, projected to grow to USD 23.45 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.54% over the forecast period 2025-2035.

Defense special purpose land vehicles form a vital segment of the global defense industry, built to serve missions that standard military platforms cannot address effectively. These vehicles are engineered with specific functions in mind, ranging from tactical mobility and reconnaissance to command, engineering support, and recovery operations. Their primary strength lies in their ability to adapt to diverse terrains and mission requirements, making them essential in both combat and support roles. Unlike conventional armored or transport vehicles, they are tailored with specialized systems, equipment, and structural modifications that enhance their suitability for complex environments. The market is shaped by the evolving nature of warfare and security needs. Modern conflicts demand not only protection and firepower but also rapid adaptability, logistical efficiency, and mission-specific performance. As a result, the design and procurement of such vehicles emphasize modularity, survivability, and integration with broader operational networks. They serve as the ground-level backbone that supports troops, ensures supply chains, and enables force mobility in challenging scenarios. Whether deployed for active combat, humanitarian assistance, or infrastructure repair in conflict zones, defense special purpose land vehicles play a crucial role in ensuring that armed forces remain capable, resilient, and operationally versatile.

The role of technology in shaping defense special mission aircraft has become increasingly pronounced, driving both capability enhancement and mission effectiveness. Advanced technologies are transforming these platforms into highly networked assets that operate at the intersection of intelligence gathering, surveillance, electronic warfare, and communication support. The integration of modern sensor suites provides the ability to detect, track, and analyze activity across multiple domains with unprecedented accuracy. These improvements allow forces to maintain situational awareness even in complex and contested environments. Digitalization is a central theme, enabling real-time information sharing and interoperability with ground, naval, and space assets. Aircraft now act as flying command centers, transmitting critical intelligence instantly to decision-makers and frontline units. Emerging technologies such as artificial intelligence and machine learning are further optimizing mission planning and execution by offering predictive insights and automating aspects of threat detection. Materials science and propulsion innovations have also played a role, allowing for extended endurance and improved efficiency. In addition, electronic warfare and cybersecurity measures are ensuring that these aircraft remain effective in highly competitive theaters where adversaries may attempt to disrupt communications or sensor performance. Collectively, these advancements highlight technology's decisive impact on the evolution of special mission aircraft.

The demand for defense special purpose land vehicles is shaped by a combination of security imperatives, operational requirements, and technological opportunities. A key factor driving growth is the changing nature of threats, where forces must be prepared for both conventional battles and irregular warfare scenarios. Special purpose vehicles provide the tailored capabilities needed to address this diversity, offering enhanced protection, mobility, and mission-specific equipment that cannot be achieved with standard military platforms. Another driver lies in the need for resilience and force protection. Modern conflicts often involve asymmetric tactics, such as ambushes and improvised explosive devices, which necessitate vehicles equipped with advanced armor, defensive systems, and high survivability standards. Militaries also recognize the importance of speed and maneuverability, requiring vehicles capable of operating in urban landscapes, remote areas, and rugged terrains without compromising safety. Economic and logistical considerations further shape demand. Modular and multi-role vehicles are appealing because they reduce lifecycle costs and maximize fleet utility by supporting multiple missions. Beyond combat, the growing role of armed forces in humanitarian aid, peacekeeping, and infrastructure restoration has strengthened the case for versatile vehicles. This blend of defense necessity and civil utility positions the market as strategically significant.

Regional demand for defense special purpose land vehicles reflects distinct operational environments, strategic priorities, and industrial capacities. Nations with expansive and often contested borders prioritize reconnaissance and patrol vehicles that ensure persistent monitoring and quick reaction capability. Countries with difficult terrain, such as mountains, deserts, or dense forests, seek platforms optimized for off-road endurance, logistics, and engineering tasks. These geographical factors heavily influence procurement choices, leading to diverse requirements across regions. In technologically advanced regions, emphasis is placed on modernization and the integration of digital systems. These militaries prioritize vehicles with modular configurations, advanced protection measures, and network-enabled capabilities to ensure interoperability with allied forces. By contrast, emerging economies often favor cost-efficient, multipurpose platforms that provide solid performance while remaining adaptable to various missions. This pragmatic approach allows them to balance budgetary constraints with operational effectiveness. Additionally, non-combat missions have influenced regional strategies. Areas prone to natural disasters invest in vehicles that can be deployed for relief and reconstruction, while countries engaged in peacekeeping focus on mobility and protection for stability operations. Domestic industrial capacity also plays a role, with some nations emphasizing indigenous development while others pursue partnerships or imports. This variety ensures that regional markets evolve in line with local priorities and global trends.

The Finnish Defence Forces Logistics Command (FDFLOGCOM) has completed the acquisition of 29 Patria XA-300 (6X6) armoured personnel carriers for €36.5 million ($40.5 million), concluding the final phase of an expanded procurement agreement. These vehicles will strengthen the Finnish Army's operational capability, providing modern mobility assets expected to remain in service through the 2060s. This order represents the concluding tranche of a 2023 agreement that included an option for up to 70 additional units. With this procurement, the total fleet of Patria XA-300s moves closer to the full scope of the original contract, which initially covered 91 vehicles with an option for 70 more.

By Application

By Region

By Type

The 10-year special purpose land vehicles market analysis would give a detailed overview of special purpose land vehicles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year special purpose land vehicles market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional special purpose land vehicles market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.