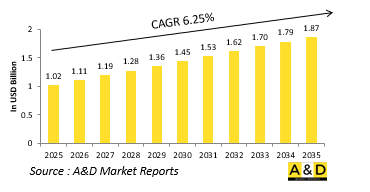

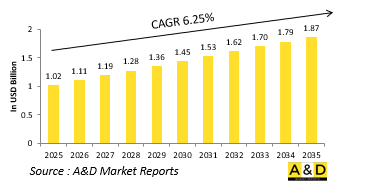

세계 PCB 테스트 시스템 시장 규모는 2025년에 10억 2,000만 달러, 2035년에는 18억 7,000만 달러에 달할 것으로 예상되며, 예측 기간인 2025-2035년 6.25%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

세계 군용 PCB(인쇄 회로 기판) 테스트 시스템은 국방 용도에 사용되는 전자 부품의 신뢰성과 성능을 보장하는 데 중요한 역할을 하고 있습니다. 이러한 테스트 시스템은 군사 환경에서 흔히 발생하는 극한의 환경 및 작동 조건에서 PCB의 기능, 내구성 및 컴플라이언스를 평가하는 데 필수적입니다. 통신 시스템 및 레이더에서 무기 유도 및 내비게이션에 이르기까지 국방 플랫폼은 첨단 전자 장비에 대한 의존도가 높아지고 있으며, 정밀하고 견고한 PCB 테스트 솔루션에 대한 수요가 크게 증가하고 있습니다. 군용 PCB는 내열성, 충격, 진동, 전자기 간섭에 대한 엄격한 기준을 충족해야 하므로 철저한 테스트가 필수적입니다. 자율 시스템, 전자전, 네트워크 중심 작전 등 현대 전쟁 기술의 보급과 함께 PCB 테스트는 그 어느 때보다 군사 시스템의 라이프 사이클에 통합되어 있습니다. 전 세계적인 국방 현대화에 대한 투자와 군용 하드웨어의 전자 컨텐츠 증가는 이 부문의 성장을 더욱 촉진하고 있습니다.

기술의 발전으로 군용 PCB 테스트 시스템의 환경이 크게 변화하여 더 빠르고, 더 정확하고, 고도로 자동화된 테스트 프로세스가 가능해졌으며, AI 및 머신러닝의 혁신이 테스트 플랫폼에 통합되기 시작하여 예측 유지 보수 및 실시간 고장 진단을 용이하게 하고 있습니다. 또한, 고속 디지털 RF 테스트 기능의 채택은 차세대 군용 통신 및 센서 시스템에 사용되는 복잡한 다층 PCB의 검증에 필수적이며, 5G, 레이더 시스템 및 전자 대책 장비의 등장으로 테스트 기술은 더 높은 주파수 범위와 더 정교한 테스트 알고리즘을 향해 나아가고 있습니다. 또한, 부품의 소형화와 SoC 아키텍처의 채택이 증가함에 따라 더 미세한 해상도의 테스트 범위의 확대가 요구되고 있습니다. 환경 테스트 및 스트레스 테스트 기술도 발전하여 PCB의 복원력을 평가하기 위한 전장 조건의 시뮬레이션이 개선되었습니다. 군사 작전이 점점 더 데이터 중심적이고 전자 장비에 의존하게 됨에 따라 이러한 혁신은 테스트 정확도를 향상시킬 뿐만 아니라 미션 크리티컬 시스템의 수명주기 비용과 다운타임을 감소시키고 있습니다.

여러 가지 요인이 전 세계 국방 분야에서 군용 PCB 테스트 시스템 수요와 진화를 촉진하고 있습니다. 가장 중요한 것은 최신 군사 장비의 복잡성과 전자 컨텐츠 증가로 인해 엄격하고 종합적인 테스트 프로토콜이 필요하게 되었습니다는 점입니다. 국방 현대화 프로그램, 특히 전자전, 무인 시스템, 보안 통신 네트워크와 같은 신기술에 대한 투자 증가는 정교한 PCB 검증 솔루션에 대한 수요를 증가시켰습니다. 또한, 미션 크리티컬한 작업에서 시스템 신뢰성에 대한 중요한 요구는 엄격한 테스트 표준의 구현을 촉진하고 있습니다. 전자파 간섭과 사이버 전쟁으로 인한 위협이 증가함에 따라 국방 기관은 전자기 호환성 및 보안을 보장하기 위해 첨단 테스트 시스템에 투자하고 있습니다. 군용 플랫폼의 전자기기 소형화, 고밀도화 추세는 정밀하고 적응성이 높은 테스트 시스템의 필요성을 증가시키고 있습니다. 규제 준수, 수명주기 관리, 상태 기준 보존으로의 전환은 첨단 테스트 솔루션에 대한 수요를 더욱 증가시켜 PCB 테스트 시스템을 방위용 일렉트로닉스 생태계의 필수적인 부분으로 만들고 있습니다.

세계의 PCB 테스트 시스템 시장에 대해 조사 분석했으며, 성장 촉진요인, 향후 10년간 시장 전망, 지역별 동향 등의 정보를 전해드립니다.

지역별

기술별

유형별

용도별

북미

성장 촉진요인, 억제요인, 과제

PEST

주요 기업

공급업체 Tier 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

미국

방위 프로그램

최신 뉴스

특허

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

The global PCB Test System market is estimated at USD 1.02 billion in 2025, projected to grow to USD 1.87 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 6.25% over the forecast period 2025-2035.

The global military PCB (Printed Circuit Board) test system plays a critical role in ensuring the reliability and performance of electronic components used in defense applications. These test systems are essential for evaluating the functionality, durability, and compliance of PCBs under extreme environmental and operational conditions typically encountered in military settings. As defense platforms become increasingly reliant on advanced electronics-ranging from communication systems and radar to weapons guidance and navigation-the demand for precise and robust PCB testing solutions has grown significantly. Military-grade PCBs must meet stringent standards for thermal resistance, shock, vibration, and electromagnetic interference, making thorough testing indispensable. With the proliferation of modern warfare technologies such as autonomous systems, electronic warfare, and network-centric operations, PCB testing is now more integrated into the lifecycle of military systems than ever before. Global investment in defense modernization and increasing electronic content in military hardware are further fueling the growth of this segment.

Advancements in technology have significantly reshaped the landscape of military PCB test systems, enabling faster, more accurate, and highly automated testing processes. Innovations in artificial intelligence and machine learning are beginning to be integrated into test platforms, facilitating predictive maintenance and real-time fault diagnostics. Additionally, the adoption of high-speed digital and RF test capabilities is essential for validating the complex, multilayered PCBs used in next-generation military communication and sensor systems. The emergence of 5G, radar systems, and electronic countermeasure equipment has pushed testing technologies toward higher frequency ranges and more sophisticated test algorithms. Furthermore, the miniaturization of components and the increasing use of system-on-chip architectures have demanded greater test coverage at finer resolutions. Environmental and stress testing technologies have also evolved, offering improved simulation of battlefield conditions to assess PCB resilience. As military operations become more data-driven and electronic-dependent, these technological innovations are not only enhancing test accuracy but also reducing lifecycle costs and downtime for mission-critical systems.

Several factors are driving the demand and evolution of military PCB test systems across global defense sectors. Foremost among these is the increasing complexity and electronic content of modern military equipment, which necessitates rigorous and comprehensive testing protocols. Rising investments in defense modernization programs, especially in emerging technologies like electronic warfare, unmanned systems, and secure communication networks, have created a parallel demand for sophisticated PCB validation solutions. Additionally, the critical need for system reliability in mission-critical operations drives the implementation of stringent testing standards. Growing threats from electronic interference and cyber warfare have also pushed defense agencies to invest in advanced testing systems to ensure electromagnetic compatibility and security. The trend toward miniaturized, high-density electronics in military platforms increases the necessity for precise and adaptable test systems. Regulatory compliance, lifecycle management, and the shift toward condition-based maintenance further contribute to the need for advanced testing solutions, making PCB test systems an integral part of the defense electronics ecosystem.

Regional dynamics play a significant role in shaping the military PCB test system market, with each region reflecting its unique defense priorities and technological capabilities. North America, led by the United States, remains a dominant player due to its robust defense budget and continuous focus on electronic warfare and modernization of military assets. The presence of key defense contractors and advanced research institutions in the region further accelerates the development and deployment of high-end PCB test systems. In Europe, countries like the UK, Germany, and France are investing in upgrading their defense electronics infrastructure, driving demand for advanced testing solutions tailored to NATO standards. The Asia-Pacific region is witnessing rapid growth, particularly in China, India, South Korea, and Japan, driven by increased defense spending, geopolitical tensions, and a growing domestic electronics manufacturing base. The Middle East, while still emerging in this domain, is focusing on localized defense production and maintenance capabilities, creating opportunities for regional test system providers. Africa and Latin America are at a nascent stage but show potential for growth as part of broader defense capability development initiatives.

The European Commission has announced €60 million in funding for the Common Armoured Vehicle System (CAVS) project under the EDIRPA program (European Defense Industry Reinforcement Instrument through Joint Procurement). This ambitious initiative seeks to develop a modern, standardized armored vehicle to strengthen the operational capabilities of the armed forces in Finland, Latvia, Sweden, and Germany. The CAVS project aims to meet increasing demands for troop mobility and protection, while promoting defense collaboration and equipment standardization among European nations.

By Region

By Technology

By Type

By Application

The 10-year Global PCB Tests Systems market analysis would give a detailed overview of Global PCB Tests Systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

The 10-year Global PCB Tests Systems market forecast of this market is covered in detailed across the segments which are mentioned above.

The regional Global PCB Tests Systems market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Hear from our experts their opinion of the possible analysis for this market.