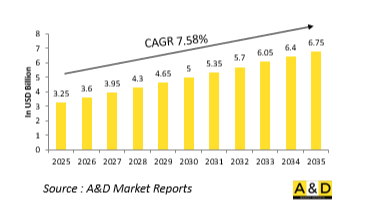

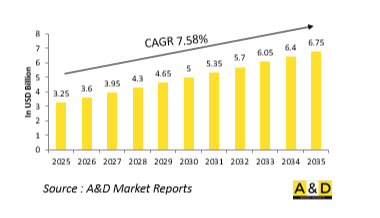

세계의 엔진 및 엔진 부품 시험용 리그 시장 규모는 2025년 32억 5,000만 달러에서 예측 기간 중 7.58%의 CAGR로 추이하며, 2035년에는 67억 5,000만 달러로 성장할 것으로 예측됩니다.

세계 방산 분야에서 엔진 및 엔진 부품의 엄격한 시험은 군용 차량, 항공기, 함정, 무인 시스템의 신뢰성, 성능, 안전성을 보장하기 위한 기반이 되고 있습니다. 시험용 리그는 실제 운용 조건을 모사하기 위해 설계된 특수 시스템으로, 엔진의 내구성, 내열성, 출력, 연비, 통합 적합성 등을 실지 배치 전에 검증하기 위한 중요한 툴입니다. 이 시스템은 극한의 온도 변화, 고도 변화, 진동 패턴, 가변 부하와 같은 가혹한 운영 환경을 재현합니다. 전투기용 터보제트 엔진부터 장갑차의 디젤 동력계까지 국방 전용 엔진 시험 장비는 군용 표준에서 요구하는 고유한 기준과 허용 오차를 충족하도록 설계되어 있습니다. 상업용 항공 및 자동차 분야와 달리 국방 분야의 엔진 테스트는 기밀 요구 사항, 다용도 운영 및 더 큰 스트레스 조건을 수반하는 경우가 많기 때문에 높은 유연성, 방대한 데이터 처리 능력 및 장시간 테스트에 대한 대응력이 요구됩니다. 특히 하이브리드 전기 추진 및 초음속 성능과 같은 새로운 추진 시스템의 복잡성으로 인해 차세대 방위 프로그램을 지원하기 위한 시험용 리그의 인프라 확장 및 현대화에 대한 전 세계적인 관심이 높아지고 있습니다.

기술의 발전은 방산 분야의 엔진 및 부품 시험 방법을 크게 변화시키고 있습니다. 특히 중요한 변화 중 하나는 시험 장비에 첨단 계측 및 제어 시스템이 통합되어 실시간 진단, 고해상도 데이터 수집 및 예측 분석이 가능해졌습니다는 점입니다. 디지털 트윈 기술을 통해 엔지니어는 엔진 시스템의 가상 복제본을 생성하고 이를 실제 리그 테스트 결과와 비교하여 성능 저하, 성능 편차 및 유지보수 시나리오를 시뮬레이션할 수 있습니다. 또한 자동화 및 적응형 피드백 루프의 도입으로 테스트 장비는 실시간 성능 지표를 기반으로 스트레스 수준, 연료 구성, 공기 흐름, 열 조건을 자동으로 조정할 수 있으며, 사람의 개입을 줄이면서 테스트 정확도를 향상시킬 수 있습니다. 광섬유 스트레인 게이지, 압전 압력 센서, 레이저 도플러 유량계와 같은 첨단 센서의 도입으로 하중 하에서의 미세한 기계적 변화와 동적 반응에 대한 감지 능력도 향상되었습니다. 또한 폐루프식 유체 시스템과 연소 시뮬레이터를 활용하여 다양한 고도 및 기후 조건에서의 운영 환경을 높은 재현성으로 모의할 수 있게 되었습니다. 스크럼 제트 및 전기 보조 터빈과 같은 새로운 추진 기술의 등장은 공기역학적, 전기적, 열역학적 테스트 기능을 통합한 새로운 테스트 장비의 설계를 촉진하고 있습니다. 이러한 혁신은 기존의 정적이고 수동 조작 중심의 테스트 환경에서 지능적이고 상호 연결된 환경으로의 전환을 가속화하여 엔진 인증 프로세스의 속도와 신뢰성을 최적화하는 데 도움을 주고 있습니다.

세계 엔진 및 엔진 부품 시험용 리그 시장은 여러 가지 전략적 및 계획적 요인으로 인해 성장과 혁신을 촉진하고 있습니다. 주요 촉진요인 중 하나는 6세대 전투기 및 장거리 공격용 드론과 같은 차세대 군용 항공기를 위해 개발되고 있는 첨단 추진 시스템의 보급입니다. 이러한 새로운 시스템은 기존보다 훨씬 더 정교한 테스트 환경을 필요로 합니다. 또한 극초음속 무기 및 재사용 가능한 우주 관련 시스템의 추진으로 인해 극심한 열 흐름, 고진동, 초고속 기류를 견딜 수 있는 시험용 리그에 대한 수요가 발생하고 있습니다. 또한 추진 시스템이 항공전자, 구조 재료, 미션 시스템과 통합되는 통합 플랫폼 설계의 흐름에 따라 개별 요소가 아닌 시스템 전체를 종합적으로 테스트할 수 있는 다용도 리그가 요구되고 있습니다. 또한 시뮬레이션을 활용한 검증을 통해 개발 주기를 단축하고 물리적 시제품 제작 비용을 줄이면서 시험 신뢰성을 높여야 할 필요성도 리그에 대한 투자를 촉진하고 있습니다. 방위 기관은 또한 레거시 시스템의 수명을 연장하기 위해 현대의 운영 요구사항에 맞는 부품의 업그레이드 및 개조를 평가할 수 있는 테스트 장비에 자금을 투자하고 있습니다. 최근 방산 분야에서도 지속가능성에 대한 관심이 높아지면서 엔진은 연비 효율과 배출가스 감소를 위해 재설계되고 있으며, 하이브리드 연소 모델과 바이오연료와의 호환성을 평가하기 위한 새로운 테스트 요구사항이 생겨나고 있습니다. 한편, 국방 조달 분야에서는 검증 가능한 데이터와 모듈성이 요구되고 있으며, OEM과 테스트 센터는 플러그 앤 플레이 기능과 표준화된 측정 프로토콜을 갖춘 리그를 개발하고 있습니다.

세계의 엔진 및 엔진 부품 시험용 리그 시장을 조사했으며, 시장의 현황, 기술 동향, 시장 영향요인의 분석, 시장 규모 추이·예측, 지역별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 목차

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 리포트의 정의

방위 분야용 엔진 및 엔진 부품 시험용 리그

유형별

플랫폼별

용도별

지역별

방위 분야용 엔진 및 엔진 부품 시험용 리그의 향후 10년간 분석

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 시장 예측

방위 분야용 엔진 및 엔진 부품 시험용 리그 시장의 동향·예측 : 지역별

북미

촉진요인, 제약, 과제

억제요인

주요 기업

공급업체 Tier의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 국가별 분석

미국

방위 프로그램

최신 뉴스

특허

현재 기술 성숙도

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 기회 매트릭스

방위 분야용 엔진 및 엔진 부품 시험용 리그 : 관련 전문가의 의견

The Global Rigs for engine and engine component testing market is estimated at USD 3.25 billion in 2025, projected to grow to USD 6.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 7.58% over the forecast period 2025-2035.

In the global defense sector, the rigorous testing of engines and engine components is foundational to ensuring the reliability, performance, and safety of military vehicles, aircraft, ships, and unmanned systems. Test rigs-specialized systems designed to simulate real-world operational conditions-serve as critical tools for validating engine durability, thermal resilience, power output, fuel efficiency, and integration compatibility before deployment. These systems replicate harsh operational environments, including extreme temperatures, altitude changes, vibration profiles, and varying loads. Whether testing turbojet engines for fighter aircraft or diesel powertrains for armored ground vehicles, defense-specific engine test rigs are built to accommodate the unique standards and tolerances required by military specifications. Unlike commercial aviation or automotive sectors, defense engine testing often involves classified requirements, multi-role usage, and greater stress profiles, making it essential for rigs to be highly configurable, data-intensive, and capable of extended-duration testing. The growing complexity of propulsion systems-particularly with hybrid-electric concepts and supersonic performance demands-has led to a surge in global interest in expanding and modernizing test rig infrastructure to support next-generation defense programs.

Technological advancements are transforming how engine and component testing is conducted in defense applications. One of the most significant shifts is the integration of advanced instrumentation and control systems into test rigs, enabling real-time diagnostics, high-resolution data capture, and predictive analytics. Digital twin technology allows engineers to create virtual replicas of engine systems, which are then tested against real-world rig results to simulate degradation, performance deviation, and maintenance scenarios. Furthermore, automation and adaptive feedback loops allow test rigs to adjust stress levels, fuel composition, airflow, and thermal conditions based on live performance metrics, reducing human intervention and increasing test accuracy. Advanced sensors, such as fiber-optic strain gauges, piezoelectric pressure transducers, and laser Doppler velocimetry tools, have also enhanced the ability to capture minute mechanical changes and dynamic responses under load. In addition, closed-loop fluid systems and combustion simulators are enabling high-fidelity replication of operational conditions across different altitudes and climates. Emerging propulsion technologies, including scramjets and electric-assisted turbines, are also prompting the design of novel rigs that combine aerodynamic, electrical, and thermodynamic testing capabilities in one integrated platform. These innovations have accelerated the shift from static, manually operated test setups to intelligent, interconnected environments that optimize both speed and reliability in engine qualification.

Several strategic and programmatic forces are driving growth and innovation in the global market for defense engine and component test rigs. A key driver is the proliferation of advanced propulsion systems being developed for next-generation military aircraft, such as sixth-generation fighters and long-range strike drones, which demand more sophisticated test environments than ever before. The push for hypersonic weapons and reusable space-based systems has created a demand for test rigs capable of withstanding intense heat flux, high vibration, and ultra-high-speed airflow. Additionally, the trend toward integrated platform design-where propulsion is no longer isolated from avionics, structural materials, and mission systems-has required a more holistic testing methodology that can be executed through versatile rig systems. Another important driver is the need to accelerate development cycles through simulation-backed validation, thereby reducing physical prototyping costs while increasing test confidence. Defense organizations are also investing in test rigs to extend the lifecycle of legacy systems by evaluating component upgrades and retrofits under modern operational demands. As sustainability gains traction even in the defense space, engines are being redesigned for greater efficiency and reduced emissions, creating new testing requirements for hybrid combustion models and biofuel compatibility. Meanwhile, defense procurement frameworks increasingly demand verifiable data and modularity, pushing OEMs and testing centers to equip their rigs with plug-and-play features and standardized measurement protocols.

Regional developments in defense engine testing reflect varied national defense priorities, industrial capabilities, and strategic goals. In North America, the United States continues to dominate in engine test rig development, with major defense contractors and research institutions operating sophisticated facilities for evaluating turbine engines, rotary propulsion units, and electric thrust systems. These include both military and dual-use platforms, with test cells equipped for high-altitude simulation, acoustic analysis, and combustion diagnostics. Canada, while smaller in scale, contributes to regional testing expertise with a focus on cold-weather engine validation and NATO-aligned requirements. In Europe, the UK, Germany, and France are leading investments in test rigs through programs like FCAS (Future Combat Air System) and Tempest, which include propulsion testbeds tailored for stealth-compatible and high-performance engines. European facilities often emphasize modularity and cross-national cooperation, reflecting the continent's integrated defense manufacturing environment. In the Asia-Pacific region, China is rapidly building independent capabilities in propulsion testing as part of its broader push for self-reliant military technology. China's investment in jet engine development has resulted in expansive test infrastructure built around high-thrust engines and long-range UAVs. India, through HAL and DRDO, is expanding indigenous testing capacity for engines like the Kaveri and for strategic projects such as AMCA. Japan and South Korea are developing advanced engine testing infrastructure for both air and naval platforms, with a strong emphasis on stealth propulsion and export compliance. In the Middle East, nations like Saudi Arabia and the UAE are investing in establishing in-country test and evaluation hubs, often through partnerships with Western OEMs, as part of their localization strategies under Vision 2030 and similar initiatives. Globally, this regional diversity is fostering both cooperation and competition in the defense test rig ecosystem, ensuring steady innovation and growth in capabilities.

Boeing has been awarded the Engineering and Manufacturing Development (EMD) contract for the U.S. Air Force's Next-Generation Air Dominance (NGAD) fighter jet program. In a formal announcement from the Oval Office, President Donald Trump, Defense Secretary Pete Hegseth, and Air Force Chief General David Allvin revealed that the aircraft will be designated the F-47-marking the United States' first sixth-generation fighter jet. This contract marks a significant milestone for Boeing, representing its first "clean-sheet" fighter jet design selected since its 1997 merger with McDonnell Douglas. Unlike the F-15EX and other Boeing aircraft based on legacy McDonnell Douglas platforms, a clean-sheet design is developed entirely from scratch, tailored specifically to meet the customer's requirements.

Global Rigs for engine and engine component testing in defense- Table of Contents

Global Rigs for engine and engine component testing in defense Report Definition

Global Rigs for engine and engine component testing in defense Segmentation

By Type

By Platform

By Application

By Region

Global Rigs for engine and engine component testing in defense Analysis for next 10 Years

The 10-year Global Rigs for engine and engine component testing in defense analysis would give a detailed overview of Global Rigs for engine and engine component testing in defense growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Rigs for engine and engine component testing in defense Forecast

The 10-year Global Rigs for engine and engine component testing in defense forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global Rigs for engine and engine component testing in defense Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global Rigs for engine and engine component testing in defense

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Rigs for engine and engine component testing in defense

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Rigs for engine and engine component testing in defense

Hear from our experts their opinion of the possible analysis for this market.