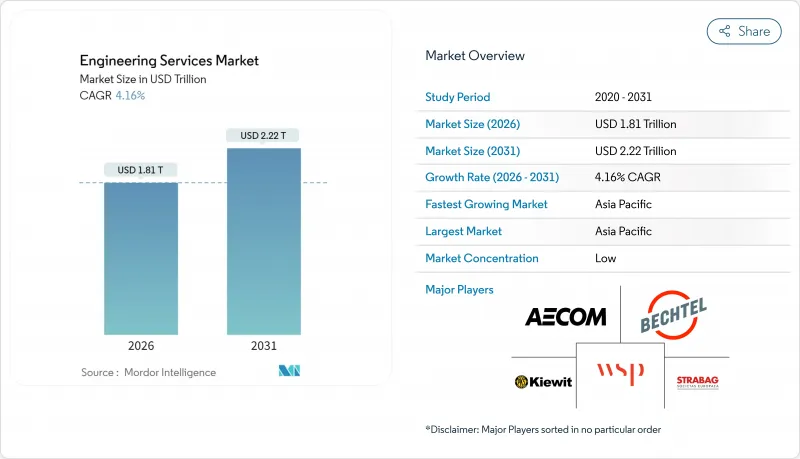

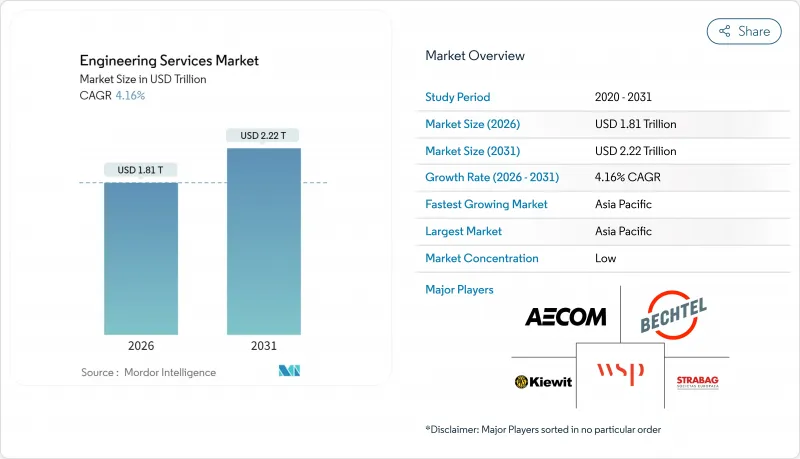

세계의 엔지니어링 서비스 시장 규모는 2026년 1조 8,100억 달러로 추정되며, 2025년 1조 7,400억 달러에서 성장해 2031년까지 2조 2,200억 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지의 연평균 성장률(CAGR)은 4.16%가 될 전망입니다.

공공 부문의 인프라 계획 증가, 에너지 전환 자산으로 민간 자본 유입, 디지털 트윈 도입 가속화가 이러한 확대를 지원하는 주요 요인입니다. 토목과 전기 분야가 공동으로 대부분의 계약을 지원하고 있으며, 하이브리드 온사이트 오프쇼어 제공을 통해 공급업체는 프로젝트의 복잡성과 비용 최적화의 균형을 맞추고 있습니다. 중견기업은 수소, 탄소회수, 소형 모듈로(SMR) 사업에 특화함으로써 점유율을 지속적으로 확대하고 있으며, 정부 인센티브가 수요 전망을 강화하고 있습니다. 아시아태평양은 가장 규모가 큰 지역 기회를 유지하고 있지만, 북미에서는 연방 정부의 청정 에너지 자금이 송전망 현대화와 방위 프로그램에 유입되고 있기 때문에 견조한 성장을 보이고 있습니다.

제조업체는 디지털 트윈을 확대하고 가동 중지 시간을 줄이고 자산 이용률을 최적화하고 있으며, 이로 인해 다분야에 걸친 엔지니어링 지원에 대한 프리미엄 수요가 발생하고 있습니다. 예측 보전이 운영을 안정화시키면 일반적으로 15-25%의 비용 절감이 약속됩니다. 기계적 강점에 분석 능력을 결합한 벤더는 보다 높은 청구 단가를 획득하지만, 이러한 하이브리드 스킬의 부족이 마진을 견조하게 유지하고 있습니다. 운영 기술 네트워크가 기업 IT와 연결됨에 따라 사이버 강화 설계는 필수 범위 요소가 되어 프로젝트의 가치와 복잡성을 더욱 확대하고 있습니다. 이 추세는 예기치 않은 정지에 대한 허용 오차가 최소한인 반도체 공장, 배터리 셀 공장 및 해양 생산 플랫폼에서 가장 두드러집니다. 중기적으로는 교차 도메인 전문 지식이 경쟁 우위를 결정하고 전문 기업이 일반 기업을 능가하는 여지가 탄생합니다.

세계 주요 도시에서는 혼잡 완화와 기후 변화 대책을 위해 2025년까지 연간 9조 달러의 투자가 필요합니다. 아시아에서는 도시 인구가 연률 2.3% 증가하고 있으며 대량 운송 노선, 홍수 대책 시스템, 스마트 유틸리티 그리드에 대한 기록적인 지출을 강요받고 있습니다. 엔지니어링 컨설턴트 기업은 지자체가 자금 조달 가능한 관민 연계(PPP) 안건을 구축하는 지원을 하고 있으며, 이 능력이 기관 투자가의 자본을 끌어들이고 있습니다. 미국에서는 연방 정부의 물 인프라 보조금만으로도 연간 60억 달러의 엔지니어링 수요를 창출하고 있습니다. 특히 폐수처리 및 재해 내성 프로젝트에 있어서 환경규제 준수의 의무화는 계획 수립 단계를 장기화시켜 경험이 풍부한 토목기업 수요를 높이고 있습니다. 그러므로 장기적인 성장은 도시 개발 수요와 엄격한 지속가능성 기준의 교차에 뿌리를 둔 상태가 지속될 것입니다.

정치적으로 불안정한 지역에서는 국경을 넘어선 프로젝트의 리스크 프리미엄이 확대되어 보험 비용 증가와 승인 프로세스의 장기화를 초래하고 있습니다. 동시에 수요가 최고치에 이르는 가운데 퇴직으로 인해 숙련된 기술자 공급이 감소하고 있습니다. 기업은 중요한 사이버 피지컬 분야의 직책에서 최대 40%의 결원률을 보고하고 있으며, 25-35%의 임금 프리미엄을 강요하고 있습니다. 하도급 업체에 대한 과도한 의존은 이익률을 낮추고 품질 모니터링을 초래하는 반면, 비자 및 자격증 병목 현상은 인원의 신속한 재배치를 제한합니다. 기업은 현재 사내 아카데미와 국제 로테이션 프로그램에 투자하여 인재 파이프라인의 안정화를 도모하고 있지만 단기적인 용량 제약이 시장 속도의 부족이 되고 있습니다.

토목 공사는 정부가 운송 회랑과 내성이 있는 수도 시스템의 우선도를 유지했기 때문에 2025년 수익의 37.86%를 차지했습니다. 한편 전기공사는 미국의 청정에너지 장려금 3,690억 달러와 병행하는 EU 그린딜 자금에 힘입어 분야 중 가장 빠른 CAGR 4.93%를 보일 것으로 예측됩니다. 기계설비 분야는 공장 자동화나 로봇화 개수에 의해 수요가 확대되는 한편, 구조물 및 배관 분야는 건설 사이클 전체에 연동한 추이를 나타내고 있습니다. 전기 기술자는 기존 설계 범위 외에도 소프트웨어 코딩, 사이버 보안, IEC-61850 그리드 프로토콜 전문 지식을 통합하는 경향이 강해졌으며, 이러한 융합으로 평균 판매 가격은 높은 수준을 유지하고 있습니다. 분산 에너지 자원의 보급에 따라 전력 회사는 변전소의 디지털화 및 축전 시스템 통합 조사를 다루는 다년 계약을 체결하고 있습니다. 이러한 추세로 인해 엔지니어링 서비스 시장은 전기 지향 성장 궤도를 유지하고 있습니다.

전문 분야의 경계가 모호해지면서 인재 전략도 재구축되어 기업은 디지털 트윈 상품에 대응하기 위해 PE 자격 보유 기술자와 함께 데이터 사이언티스트를 채용하고 있습니다. IEEE나 ISO-55000 등의 인증 제도가 입찰 평가에 중시되기 때문에 확실한 컴플라이언스 실적을 가지는 기업이 우위가 됩니다. 그 결과 가격 감도가 높은 신흥 시장에서도 높은 단가 청구율이 유지되고 있습니다. 2031년까지 전기공사 계약의 수익 규모는 토목 분야에 육박할 것으로 예측되어 경쟁이 격화됩니다. 차별화를 도모하기 위해, Vehicle-to-Grid(V2G) 시스템이나 고압 직류 송전(HVDC) 접속 등의 틈새 분야로 특화가 진행될 것입니다.

규제 대상 프로젝트에서 대면 조정의 필요성으로 2025년 시점에서는 현지 작업이 66.83%의 점유율을 차지하고 있지만, 오프쇼어 실행은 CAGR 5.05%로 확대중입니다. 클라우드 네이티브 CAD/CAM 플랫폼에 의해 인도, 필리핀, 동유럽의 센터에 산출물을 위탁함으로써 24시간 설계 사이클을 실현하고 있습니다. 일상적인 제도 업무에 있어서는 현지 팀에 비해 40-60%의 비용 차이가 여전히 매력적이며, 이것에 의해 현지 스탭은 이해 관계자 관리나 현장 감독에 주력할 수 있습니다. 엔지니어링 서비스 시장에서는 인원수가 아닌 성과물을 명기하는 하이브리드형 업무 사양서가 주류가 되고 있어, 이것에 의해 기존의 원격 품질 관리에 관한 고객의 우려가 해소되고 있습니다.

벤더 선정 기준은 시간당 단가에서 사이버 보안 시스템 및 데이터 세분화 능력으로 전환하고 있습니다. ISO-27001 및 SOC-2 인증은 필수 요건이 되었습니다. 정부 관련 업무에 있어서는 수출관리 규제에 준거하기 위해 동맹국의 국민만으로 구성된 클린룸형 오프쇼어 부문을 설치하는 경우도 볼 수 있습니다. 문서화와 모델 검증의 자동화가 진행되고 있는 가운데, 시니어 아키텍트의 일당은 변화가 적지만 생산성 향상에 의한 이익률의 점진적 상승이 기대되고 있습니다. 이 추세는 오프쇼어가 단순한 비용 절감 수단에서 전략적 자원 증폭 장치로 진화하고 있음을 뒷받침합니다.

아시아태평양은 2025년 수익의 39.52%를 차지했으며 연간 1조 7,000억 달러의 인프라 지출이 기반을 두고 있습니다. 중국의 '일대일로' 구상과 인도의 대량고속운송시스템(MRT) 정비가 견조한 토목공사의 수주 잔여를 확보하는 한편, 아시아태평양에서의 제조업 회귀(리쇼어링)가 공장 자동화와 전력망 업그레이드 수주를 촉진하고 있습니다. 지역정부는 기후 변화 적응조성금을 연안 보호공사에 배분하여 연안 토목분야를 견인하고 있습니다. 그 결과 이 지역에서는 메가 프로젝트에 국부 기금 투입에 힘입어 엔지니어링 서비스 시장이 5.13%라는 지역 최고 CAGR을 기록하고 있습니다.

북미는 2위 점유율을 차지하고 있으며 미국의 청정에너지 장려책 3,690억 달러와 광범위한 인프라 현대화를 위한 1조 2,000억 달러가 지원되고 있습니다. 방위 지출과 소형 모듈로(SMR)의 시험 운용은 첨단 기술을 가진 엔지니어 인력에 대한 수요를 더욱 높이고 있습니다. 캐나다의 LNG 및 원자력 계획, 멕시코의 니어 쇼어링에 의한 공장 건설이 대륙 규모의 프로젝트 파이프라인을 확대했습니다. 벤더를 위한 기회는 송전망 상호접속 조사, 수소 허브 FEED 계약, 중요 광물 처리 플랜트에 이릅니다.

유럽에서는 EU 그린딜에 의한 자금으로, 넷 제로 개수와 해상 풍력 확대가 축이 됩니다. 독일의 5,000억 유로(5,500억 달러) 규모 인프라 기금과 영국의 Sizewell C 원자력 프로젝트가 대형 안건의 예시입니다. 엄격한 분류 규칙은 자금을 인증된 지속 가능한 프로젝트로 유도하고 ESG 보고에 뛰어난 기업을 평가합니다. 한편 중동 및 아프리카에서는 걸프 지역의 그린 암모니아 수출 거점과 북아프리카의 유틸리티 규모 태양광 발전 등 에너지 다양화에 주력하고 있습니다. 그러나 정치적 안정성 문제와 노동력 부족으로 인해 특정 중동 및 아프리카 시장에서는 성장 속도가 둔화되고 있습니다.

The engineering services market size in 2026 is estimated at USD 1.81 trillion, growing from 2025 value of USD 1.74 trillion with 2031 projections showing USD 2.22 trillion, growing at 4.16% CAGR over 2026-2031.

Rising public-sector infrastructure programs, private capital pouring into energy-transition assets, and accelerating digital-twin adoption are the primary vectors supporting that expansion. Civil and electrical disciplines jointly underpin most contracts, while hybrid onsite, offshore delivery helps vendors balance project complexity with cost optimization. Mid-sized firms continue to gain share by specializing in hydrogen, carbon-capture, and small modular reactor (SMR) work, where government incentives strengthen demand visibility. Asia Pacific sustains the largest regional opportunity set, yet North America posts resilient growth as federal clean-energy funds flow into grid-modernization and defense programs.

Manufacturers are scaling digital twins to cut downtime and fine-tune asset utilization, triggering premium demand for multidisciplinary engineering support. Engagements commonly promise 15-25% cost reductions once predictive maintenance stabilizes operations. Vendors that couple mechanical strength with analytics talent win higher bill rates, yet the scarcity of such hybrid skills keeps margins firm. As operational-technology networks connect to enterprise IT, cyber-hardening design has become a mandatory scope element, further widening project value and complexity. The trend is most visible in semiconductor fabs, battery-cell plants, and offshore production platforms, where tolerance for unplanned outages is minimal. Over the medium term, cross-domain expertise will define competitive advantage, giving specialist firms room to outpace generalists.

Global cities require USD 9 trillion annually through 2025 to relieve congestion and climate stress. Asia's 2.3% yearly urban-population increment forces record spending on mass-transit corridors, flood-control systems, and smart-utility grids. Engineering consultancies help municipalities structure bankable public-private partnership (PPP) deals, a capability that attracts institutional capital. In the United States, federal water infrastructure grants alone create a USD 6 billion annual engineering opportunity. Environmental-compliance mandates, particularly for wastewater and storm-resilience projects, lengthen scoping phases and raise demand for experienced civil firms. Long-term growth, therefore, remains anchored in the intersection of urban build-out needs and stricter sustainability codes.

Cross-border project risk premiums widen in politically volatile regions, inflating insurance costs and elongating approval cycles. Concurrently, retirements reduce the available experienced-engineer pool just as demand peaks. Firms report up to 40% vacancy rates for critical cyber-physical roles, forcing salary premiums of 25-35%. Over-reliance on subcontractors erodes margin and invites quality scrutiny, while visa and certification bottlenecks limit rapid redeployment of personnel. Companies now invest in internal academies and international rotation programs to stabilize workforce pipelines, but near-term capacity constraints remain a drag on market velocity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Civil engineering retained 37.86% of 2025 revenue as governments continued to prioritize transportation corridors and resilient water systems. Electrical work, however, is forecast to grow at a 4.93% CAGR, the fastest among disciplines, propelled by USD 369 billion in U.S. clean-energy incentives and parallel EU Green Deal funding. Mechanical services gain traction through factory automation and robotics retrofits, while structural and piping segments trace the broader construction cycle. Electrical practitioners increasingly bundle software coding, cybersecurity, and IEC-61850 grid-protocol expertise with traditional design scopes, a convergence that maintains high average selling prices. As distributed energy resources proliferate, utilities award multi-year frameworks covering substation digitalization and storage-integration studies. These developments keep the engineering services market on an electrification-tilted growth arc.

The blurring of disciplinary boundaries also reshapes talent strategies; firms now recruit data scientists alongside PE-licensed engineers to satisfy digital-twin deliverables. Certification regimes such as IEEE and ISO-55000 factor heavily into bid evaluations, elevating firms with proven compliance track records. Consequently, premium billing rates remain sticky even in price-sensitive emerging markets. By 2031, electrical contracts are expected to approach civil's revenue scale, tightening competition and prompting niche specialization, such as vehicle-to-grid systems and high-voltage direct-current interconnects, to preserve differentiation.

On-site work held a 66.83% share in 2025 due to the need for face-to-face coordination on regulated projects, yet offshore execution is expanding at a 5.05% CAGR. Cloud-native CAD/CAM platforms enable 24-hour design cycles by handing deliverables to centers in India, the Philippines, and Eastern Europe. Cost arbitrage of 40-60% versus local teams remains compelling for routine drafting, freeing onsite staff for stakeholder management and field supervision. The engineering services market increasingly coalesces around hybrid statements of work that specify deliverables, not headcount, thereby defusing earlier client concerns about remote quality control.

Vendor selection now pivots on cybersecurity posture and data-segmentation capabilities rather than solely on hourly rates. ISO-27001 and SOC-2 attestations have become table stakes. For government-sensitive scopes, clients sometimes carve out clean-room offshore pods staffed exclusively by citizens of allied nations to comply with export-control regulations. With automation in documentation and model-checking advancing, firms expect incremental margin lift from productivity gains, even as daily rates for senior architects remain flat. The trend confirms offshore's evolution from tactical cost lever to strategic resource multiplier.

The Engineering Services Market Report is Segmented by Engineering Disciplines (Civil, Mechanical, and More), Delivery Model (Offshore, and Onsite), Services (Product Engineering, Process Engineering, and More), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific retained 39.52% of 2025 revenue, anchored by USD 1.7 trillion in annual infrastructure spending. China's Belt and Road initiatives and India's mass rapid-transit build-outs secure a robust civil-work backlog, while Asia-Pacific manufacturing-reshoring funnels orders into factory-automation and utility-grid upgrades. Regional governments allocate climate-adaptation grants toward coastal-protection engineering, propelling coastal-civil sub-disciplines. As a result, the engineering services market registers its fastest 5.13% regional CAGR here, sustained by sovereign wealth deployment into mega-projects.

North America holds the second-largest share, buoyed by USD 369 billion in U.S. clean-energy incentives and USD 1.2 trillion for broader infrastructure modernization. Defense spending and SMR pilots further sharpen demand for high-clearance engineering talent. Canada's LNG and nuclear programs, along with Mexico's near-shoring-induced factory builds, enlarge the continental project funnel. Vendor opportunities span grid-interconnect studies, hydrogen-hub FEED contracts, and critical-mineral processing plants.

Europe pivots on net-zero retrofits and offshore-wind expansion financed by the EU Green Deal.Germany's EUR 500 billion (USD 550 billion) infrastructure fund and the U.K.'s Sizewell C nuclear project typify large pipeline items. Strict taxonomy rules steer capital toward certified sustainable projects, rewarding firms adept at ESG reporting. Meanwhile, the Middle East and Africa focus on energy diversification, such as green-ammonia export hubs in the Gulf and utility-scale solar in North Africa. Political stability issues and labor shortages, however, temper growth velocity in selected Middle East and Africa markets.