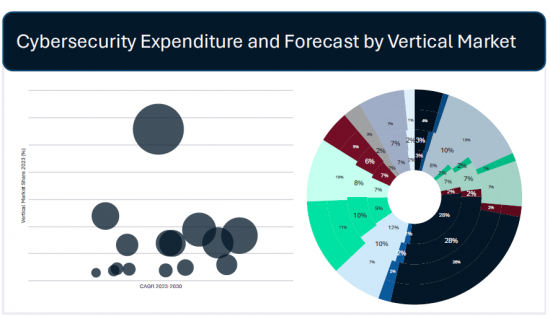

일부 산업은 다른 산업보다 앞서가고 있지만, IoT 사이버 보안의 성숙도는 상대적으로 낮은 수준으로, IoT 도입의 빠른 성장에 비해 IoT 사이버 보안의 성숙도가 뒤쳐져 있어 보안 대책의 필요성이 증가하고 있음을 보여줍니다. IoT 도입의 복잡성, 규모 및 범위가 확대되고 장치 수가 증가함에 따라 공격 대상이 증가함에 따라 보안은 점점 더 중요해질 것이며, 2023년 IoT 보안 지출은 73억 달러로 전 세계 사이버 보안 지출의 3.7% 이상에 도달할 것으로 예상됩니다. 2030년까지 IoT 보안 지출은 전 세계 사이버 보안 지출의 5%를 차지할 것으로 예상됩니다.

투자의 원동력은 규제, 취약한 디바이스 보안, 디바이스 급증, IoT 디바이스에 대한 경계감이 증가하고 있기 때문입니다. 특히 국가 중요 인프라(유틸리티, 교통, 금융 부문)와 생명과 관련된 영역(항공우주, 자동차 의료)에 대한 투자가 활발히 이루어지고 있습니다. 중요 인프라의 사이버 보안에 대한 관심 증가와 이들 분야에서의 IoT 디바이스의 빠른 도입은 규제가 까다로운 산업에서 큰 성장을 가속할 것으로 보입니다. 따라서 이 분야는 가장 큰 시장 부문으로 2030년까지 투자가 빠르게 증가할 것으로 예상됩니다.

5G 기술의 확산은 보다 빠르고 안정적인 연결성을 제공함으로써 보다 광범위한 '대규모' 및 '중요한' IoT 배포를 촉진하고 IoT의 급속한 성장을 가속하고 있습니다. 데이터의 본질적인 가치에 대한 인식이 높아짐에 따라, 의사결정과 업무 효율성 향상을 위해 실시간 정보를 활용하고자 하는 조직들의 IoT 도입이 더욱 가속화되고 있습니다. 데이터의 본질적 가치에 대한 인식이 높아짐에 따라 조직이 실시간 통찰력을 활용하여 의사결정과 업무 효율성을 개선하려는 시도가 IoT 도입을 더욱 촉진하고 있으며, IoT 도입이 증가함에 따라 연결되는 기기의 수가 늘어날 것으로 예상됩니다. 이를 효과적으로 처리하기 위해서는 종합적인 디바이스 자산 관리가 필요합니다. 따라서 보안 설계 및 임베디드 디바이스 보호에 대한 관심이 높아지고 있으며, 특히 IoT 제품의 보안 강화를 위한 법적 이니셔티브 및 국가 인증 제도에 의해 가속화되고 있습니다.

2030년까지 IoT 사이버 보안의 성숙도는 자동차 및 항공우주 산업에서 크게 향상되고, 운송 및 유틸리티 산업이 그 뒤를 이을 것으로 예상되며, IoT 디바이스가 비즈니스 및 인프라에 점점 더 중요해짐에 따라 많은 조직이 IoT 보안을 전체 사이버 보안 전략에 통합할 것으로 예상됩니다. 사이버 보안 전략 전체에 IoT 보안을 통합할 것으로 보입니다. 또한, 규제가 보안 설계(Secure by Design) 관행에 대한 투자를 촉진함에 따라 네이티브 디바이스의 보안이 더욱 강화될 것으로 예상되며, IoT 도입 규모와 범위, 사이버 보안의 성숙도는 산업과 지역에 따라 크게 다르지만, IoT 보안에 대한 인식과 도입이 증가하는 추세는 앞으로도 지속될 것으로 예상됩니다.

정의

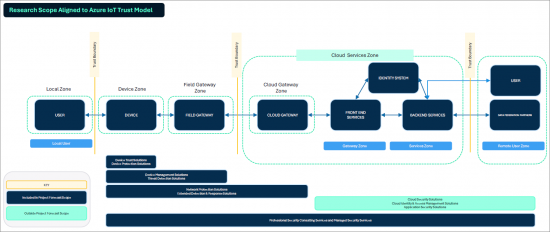

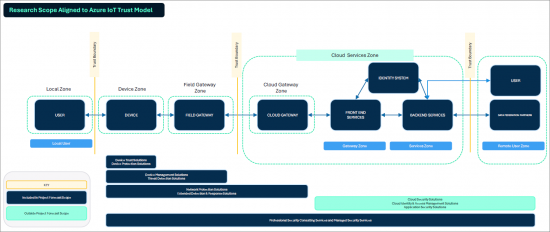

이 프로젝트에서는 디바이스, 엣지, 네트워크 각 레벨에서 신뢰와 보안을 구축하는 데 사용되는 사이버 보안 기술과 솔루션을 다룹니다. Azure IoT Trust Model을 사용하여 디바이스, 게이트웨이, 네트워크, 그리고 필드 게이트웨이와 클라우드 게이트웨이 간 데이터 전송 시 데이터 보호에 중점을 두고 있습니다. 데이터 보호에 중점을 두고 있습니다. 전문 및 관리형 보안 서비스 부문에는 클라우드 서비스를 포함한 IoT 디바이스 및 네트워크에 대한 자문, 구현 및 모니터링에 대한 서비스가 포함됩니다.

시장 세분화

조사 개요

목차

1. 정의와 세분화

주요 요약

1. 주요 요약

2. 전체적인 시장 규모 : 산업 부문별

3. 시장 예측 : 업계 부문별

4. 시장 점유율과 성장률 : 산업 부문별

5. 시장 규모 : 국가별

6. 시장 규모 : 지역별·산업별

7. 시장 지출·성장률 : 기술·서비스별

사이버 보안 투자 촉진요인

1. 투자 촉진요인 : 개요

2. 경제의 개요

3. 기술의 개요

4. 규제의 개요

5. 주요 규제 동향의 개요

6. 규제가 산업에 미치는 영향

7. 리스크의 개요

8. IoT의 위협·취약성의 개요

9. 위협의 동향

10. 취약성의 동향

11. 리스크의 동향

IoT 아키텍처

1. 고레벨 IoT 플랫폼·아키텍처

2. 고레벨 IoT 플랫폼·아키텍처와 프로젝트의 범위

3. IoT 시나리오

4. AWS 아키텍처

5. Azure 아키텍처

6. Rockwell Automation·PTC·Azure 아키텍처

7. IoT 접속 요건

8. IoT 접속 기술

9. 위협·보안 대책에 대응한 IoT 스택

기술의 수명주기와 이용 사례

1. IoT 디바이스 신뢰의 정의

2. IoT 디바이스 신뢰의 동향

3. 디바이스 신뢰 솔루션

4. IoT 디바이스 보안 관리의 정의

5. IoT 디바이스 보안 관리의 동향

6. IoT 디바이스 보안 관리 솔루션

7. IoT 위협 탐지의 정의

8. IoT 위협 탐지의 동향

9. IoT 위협 탐지 솔루션

10. 네트워크 보호의 정의

11. 네트워크 보호의 동향

12. 네트워크 보호 솔루션

13. IoT 엔드포인트 보호의 정의

14. IoT 엔드포인트 보호의 동향

15. IoT 엔드포인트 보호 솔루션

16. 전문 보안 서비스의 정의

17. 전문 보안 서비스의 동향

18. 매니지드 보안 서비스의 정의

19. 매니지드 보안 서비스의 동향

20. IoT 보안 기술·서비스의 예측(2023-2030년)

시장 지출과 전망

1. 요약

2. 시장 예측 : 산업 부문별(2023-2030년)

3. 지출액·성장률 : 산업 부문별

4. 북미 시장 예측 : 산업 부문별(2023-2030년)

5. 북미의 지출액과 CAGR : 산업 부문별(2023년)

6. 북미 시장 예측 : 국가별(2023-2030년)

7. 아시아태평양 시장 예측 : 산업 부문별(2023-2030년)

8. 아시아태평양의 지출액과 CAGR : 산업 부문별(2023년)

9. 아시아태평양 시장 예측 : 국가별(2023-2030년)

10. 유럽 시장 예측 : 산업 부문별(2023-2030년)

11. 유럽의 지출액과 CAGR : 산업 부문별(2023년)

12. 유럽 시장 예측 : 국가별(2023-2030년)

13. 아프리카 시장 예측 : 산업 부문별(2023-2030년)

14. 아프리카의 지출액과 CAGR : 산업 부문별(2023년)

15. 아프리카 시장 예측 : 국가별(2023-2030년)

16. 중동 시장 예측 : 산업 부문별(2023-2030년)

17. 중동의 지출액과 CAGR : 산업 부문별(2023년)

18. 중동 시장 예측 : 국가별(2023-2030년)

19. 라틴아메리카 시장 예측 : 산업 부문별(2023-2030년)

20. 라틴아메리카의 지출액과 CAGR : 산업 부문별(2023년)

21. 라틴아메리카 시장 예측 : 국가별(2023-2030년)

22. 중앙아시아 시장 예측 : 산업 부문별(2023-2030년)

23. 중앙아시아 지출액과 CAGR : 산업 부문별(2023년)

24. 중앙아시아 시장 예측 : 국가별(2023-2030년)

IoT 사이버 보안 에코시스템

1. 요약

2. 에코시스템

3. 벤더별 제품 맵

4. IoT 플랫폼과 보안 서비스

산업별 시장 예측

1. 항공우주의 동향

2. 항공우주 시장의 지출액(2023-2030년)과 지역별 동향

3. 농업의 동향

4. 농업 시장의 지출액(2023-2030년)과 지역별 동향

5. 자동차의 동향

6. 자동차 시장의 지출액(2023-2030년)과 지역별 동향

7. 교육의 동향

8. 교육 시장의 지출액(2023-2030년)과 지역별 동향

9. 의료의 동향

10. 의료 시장의 지출액(2023-2030년)과 지역별 동향

11. 접객(Hoapitality)·엔터테인먼트의 동향

12. 접객(Hoapitality)·엔터테인먼트 시장의 지출액(2023-2030년)과 지역별 동향

13. 산업의 동향

14. 산업 시장의 지출액(2023-2030년)과 지역별 동향

15. 물류의 동향

16. 물류 시장의 지출액(2023-2030년)과 지역별 동향

17. 운송의 동향

18. 운송 시장의 지출액(2023-2030년)과 지역별 동향

19. 유틸리티의 동향

20. 유틸리티 시장의 지출액(2023-2030년)과 지역별 동향

21. 소매의 동향

22. 소매 시장 지출액(2023-2030년)과 지역별 동향

23. 방위의 동향

24. 방위 시장의 지출액(2023-2030년)과 지역별 동향

25. 금융의 동향

26. 금융 시장 지출액(2023-2030년)과 지역별 동향

27. 공공안전의 동향

28. 공공안전 시장의 지출액(2023-2030년)과 지역별 동향

부록 : 조사 방법

KSA

영문 목차

영문목차

Overview

Across all industries, IoT cybersecurity maturity remains relatively low despite some industries being further along than others. The maturity of IoT cybersecurity lags behind the rapid growth in IoT deployments, highlighting the escalating necessity for security measures. As the complexity, scale and scope of IoT deployments evolve, and the growing number of devices expands attack surfaces, security will become increasingly critical. Westlands advisory estimates that expenditure on IoT security in 2023 was $7.3B or 3.7% of the global spend on cybersecurity. By 2030 IoT will make up 5% of expenditure.

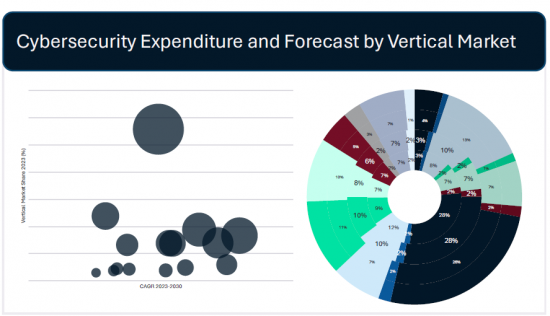

Investment is being driven by regulation, weak native device security, device proliferation and growing adversarial interest in IoT devices. Investment is particularly strong in critical national infrastructure (utilities, transportation, and financial sectors) and life critical applications (aerospace, automotive, and healthcare) . A growing focus on critical infrastructure cybersecurity and the rapid adoption of IoT devices in these fields will drive significant growth in highly regulated industries. Accordingly, these are the largest market segments and investment will continue to increase rapidly to 2030.

The rollout of 5G technology is catalysing rapid IoT growth by providing fast, more reliable connectivity thereby facilitating more widespread 'Massive' and 'Critical' IoT deployments. The increasing recognition of data's intrinsic value is further driving IoT adoption as organisations seek to leverage real time insights for improved decision making and operational efficiency. As IoT adoption increases, the number of connected devices is expected to grow, necessitating comprehensive Device Asset Management to effectively handle this expansion. Poor native device security has made these devices particularly weak links in the security of digital deployments. As such there is a growing focus on secure by design and embedded device protection, particularly accelerated by legislative initiatives and national certification schemes aimed at enhancing IoT product security.

By 2030 WA expects IoT cybersecurity maturity to have advanced significantly within the automotive and aerospace industries with transportation and utilities following closely behind. Many organisations will integrate IoT security into their overall cybersecurity strategy as these devices become increasingly integral to their operations and infrastructure. WA also expects far greater native device security as regulation drives investment in secure-by-design practices. Although the scale and scope of IoT adoption and cyber security maturity will vary greatly across industries and geographies, the trend towards greater IoT security awareness and implementation is expected to continue its upward trajectory.

Definition

The project focuses on cybersecurity technologies and solutions used to establish trust and security at the device, edge and network level. This does not include security of Virtual Private Clouds, the IoT data residing in the cloud, or IoT applications. Using the Azure IoT Trust Model, the focus of the work includes protection of devices, gateways, networks, and data in transit between the field gateway and the cloud gateway. The professional and managed security services segment includes services related to advising, implementing and monitoring IoT devices and networks which may include the cloud services.

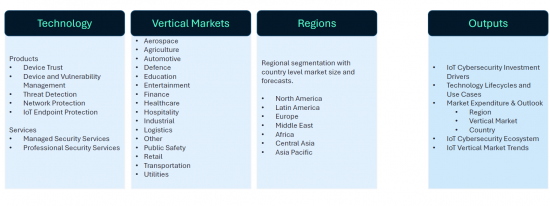

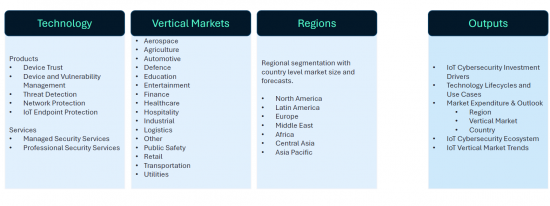

Segmentation

Deliverables

Table of Contents

1. Definitions & Segmentation

Executive Summary

1. Executive Summary

2. Total Available Market by Industry Segment

3. Market Forecast by Industry Segment

4. Market Share and Growth Rates by Industry Segment

5. Market Size by Country

6. Market Size by Region and Industry Segment

7. Market Expenditure and Growth Rate by Technology and Service

Cybersecurity Investment Drivers

1. Summary of Investment Drivers

2. Economics Summary

3. Technology Summary

4. Regulatory Summary

5. Summary of Major Regulatory Developments

6. Regulatory Impact on Industries

7. Risk Summary

8. Summary of IoT Threats and Vulnerabilities

9. Threat Trends

10. Vulnerability Trends

11. Risk Trends

IoT Architectures

1. High Level IoT Platform Architecture

2. High Level IoT Platform Architecture and Project Scope

3. IoT Scenarios

4. AWS Architecture

5. Azure Architecture

6. Rockwell Automation, PTC & Azure Architecture

7. IoT Connectivity Requirements

8. IoT Connectivity Technologies

9. IoT Stack Mapped to Threats and Security Measures

Technology Lifecycle & Use Cases

1. IoT Device Trust Definition

2. IoT Device Trust Trends

3. Device Trust Solutions

4. IoT Device Security Management Definition

5. IoT Device Security Management Trends

6. IoT Device Security Management Solutions

7. IoT Threat Detection Definition

8. IoT Threat Detection Trends

9. IoT Threat Detection Solutions

10. Network Protection Definition

11. Network Protection Trends

12. Network Protection Solutions

13. IoT Endpoint Protection Definition

14. IoT Endpoint Protection Trends

15. IoT Endpoint Protection Solutions

16. Professional Security Services Definition

17. Professional Security Services Trends

18. Managed Security Services Definition

19. Managed Security Services Trends

20. IoT Security Technology and Services Forecast 2023-2030

Market Expenditure & Outlook

1. Summary

2. Market Forecast by Industry Segment 2023-2030

3. Industry Segment by Expenditure & Growth Rate

4. North America Market Forecast by Industry Segment 2023-2030

5. North America Expenditure 2030 and CAGR by Industry Segment

6. North America Market Forecast by Country 2023-2030

7. Asia-Pacific Market Forecast by Industry Segment 2023-2030

8. Asia-Pacific Expenditure 2030 and CAGR by Industry Segment

9. Asia-Pacific Market Forecast by Country 2023-2030

10. Europe Market Forecast by Industry Segment 2023-2030

11. Europe Expenditure 2030 and CAGR by Industry Segment

12. Europe Market Forecast by Country 2023-2030

13. Africa Market Forecast by Industry Segment 2023-2030

14. Africa Expenditure 2030 and CAGR by Industry Segment

15. Africa Market Forecast by Country 2023-2030

16. Middle East Market Forecast by Industry Segment 2023-2030

17. Middle East Expenditure 2030 and CAGR by Industry Segment

18. Middle East Market Forecast by Country 2023-2030

19. Latin America Market Forecast by Industry Segment 2023-2030

20. Latin America Expenditure 2030 and CAGR by Industry Segment

21. Latin America Market Forecast by Country 2023-2030

22. Central Asia Market Forecast by Industry Segment 2023-2030

23. Central Asia Expenditure 2030 and CAGR by Industry Segment

24. Central Asia Market Forecast by Country 2023-2030

IoT Cybersecurity Ecosystem

1. Summary

2. Ecosystem

3. Product Map by Vendor

4. IoT Platforms and Security Services

Vertical Market Forecast

1. Aerospace Trends

2. Aerospace Market Expenditure 2023-2030 and by Region

3. Agriculture Trends

4. Agriculture Market Expenditure 2023-2030 and by Region

5. Automotive Trends

6. Automotive Market Expenditure 2023-2030 and by Region

7. Education Trends

8. Education Market Expenditure 2023-2030 and by Region

9. Healthcare Trends

10. Healthcare Market Expenditure 2023-2030 and by Region

11. Hospitality and Entertainment Trends

12. Hospitality and Entertainment Market Expenditure 2023-2030 and by Region

13. Industrial Trends

14. Industrial Market Expenditure 2023-2030 and by Region

15. Logistics Trends

16. Logistics Market Expenditure 2023-2030 and by Region

17. Transportation Trends

18. Transportation Market Expenditure 2023-2030 and by Region

19. Utilities Trends

20. Utilities Market Expenditure 2023-2030 and by Region

21. Retail Trends

22. Retail Market Expenditure 2023-2030 and by Region

23. Defence Trends

24. Defence Market Expenditure 2023-2030 and by Region

25. Finance Trends

26. Finance Market Expenditure 2023-2030 and by Region

27. Public Safety Trends

28. Public Safety Market Expenditure 2023-2030 and by Region