2025 Mini LED Backlight Display Trend and OLED Technology Competition Analysis

상품코드:1398376

리서치사:TrendForce

발행일:2024년 08월

페이지 정보:영문 194 Pages

라이선스 & 가격 (부가세 별도)

한글목차

인포그래픽

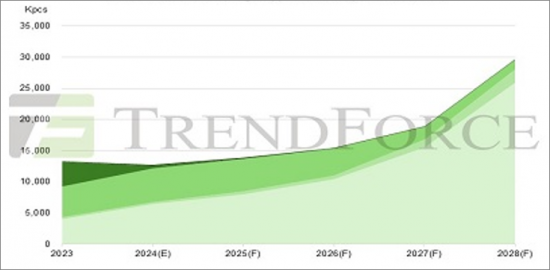

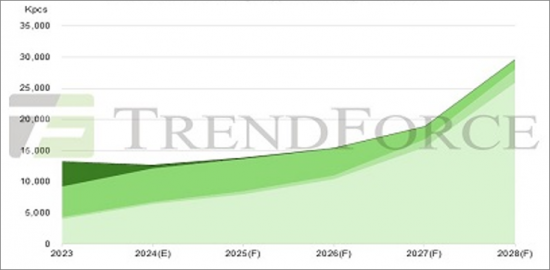

2024-2028년 미니 LED 백라이트 용도의 출하량 전망

제1장 산업 동향 : Mini LED와 OLED의 제로섬 게임, 대/중/소형 디스플레이의 치열한 경쟁

각 부문에서 미니 LED 백라이트가 탑재된 LCD 패널의 출하량이 증가하고 있으며, OLED와의 대결은 피할 수 없는 상황입니다. 대형, 중형 및 소형 패널의 다양한 응용 분야에서 미니 LED 백라이트의 이익은 OLED의 희생을 초래하고 그 반대는 제로섬 게임이되었습니다. 흥미롭게도 이것은 기술 개발의 역사에서 흔히 볼 수 있는 전형적인 일방통행식 대체 모드가 아닙니다. 오히려 두 기술은 각각 장단점이 있으며 서로 밀접하게 경쟁하고 있습니다.

미니 LED 백라이트 TV 시장은 2024년 큰 폭의 성장세를 보일 것으로 예상되지만, IT 시장에서 OLED 기술의 긍정적인 영향으로 미니 LED 백라이트 기술에 대한 각 브랜드의 투자 열의는 억제될 것으로 보입니다. 출하량은 1,270만 개로 2023년 대비 5% 감소할 것으로 전망하고 있습니다.

TV, 자동차 및 미래 MNT 시장에서 Mini LED는 OLED보다 우위를 점하고 있으며, Mini LED 백라이트 TV의 비용 절감 효과가 크지만 OLED 기술은 대형 TV 시장에서 제한적인 강점을 가지고 있습니다. 제품 차별화를 강화하고 브랜드 경쟁력을 강화하기 위해 미니 LED 백라이트 기술은 제품 사양을 업그레이드하는 데 적합한 솔루션입니다. 장기적으로 이러한 추세는 MNT 시장에도 긍정적인 영향을 미쳐 MNT의 보급률을 높이는 촉진제가 될 것입니다. 자동차 시장에서는 Mini LED 백라이트가 신뢰성 측면에서 우위를 점하고 있으며, OLED보다 높은 출하량 점유율을 차지하고 있습니다.

그러나 NB, 태블릿 및 VR 분야에서 Mini LED는 OLED만큼 경쟁력이 없으며, Apple이 NB 및 태블릿 제품에 OLED를 채택함에 따라 전체 시장 상황이 바뀌고 이 두 응용 분야에서는 Mini LED 백라이트 기술의 보급률이 지속적으로 감소할 것입니다.

제2장 기술 포커스: 비용절감을 위한 미니 LED와 성능 향상을 위한 OLED

2024년 미니 LED 백라이트의 가장 큰 변화는 솔루션이 점차 성숙해지면서 업스트림에서 하류까지 각 부문의 제조업체들이 비용 절감 방법에 대한 합의가 이루어졌습니다는 것입니다. 업계 전체의 합의는 제품 표준화를 가속화하고 공급업체의 과감한 확장을 촉진하여 비용 경쟁력을 더욱 향상시킬 수 있습니다. 그 결과 미니 LED 백라이트 개발의 가장 큰 장애물이 제거될 것으로 예상됩니다.

제3장 TV 시장: 시장 세분화의 성공으로 세계 미니 LED TV 판매량이 처음으로 OLED TV를 넘어설 것입니다.

2024년, 미니 LED 백라이트 TV의 예상 출하량은 642만 대에 달할 것으로 예상됩니다. 중국 브랜드 제조업체가 시장을 장악하고 있으며, 미니 LED 백라이트 공급망이 개선되고 각 기업이 점차적으로 비용 절감 전략을 시행함에 따라 전 세계 출하량은 2023년 대비 59% 증가하여 큰 폭의 성장을 보이고 있습니다.

OLED는 77인치, 83인치, 70-80인치 디스플레이 등의 제품을 보유하고 있지만, G8.5 생산의 원가 경쟁력이 낮고, 초대형 사이즈의 유연한 레이아웃으로 LCD를 따라잡을 수 없습니다. 상대적으로 집중된 공급, 유연하지 않은 패널 가격, 브랜드 전략의 변화, 경제적 인 절단 크기가 55인치와 65인치에 집중되어 있다는 점을 감안할 때 OLED는 다각적 인 커버 전략을 통해 미니 LED 백라이트 TV와 같은 바람직한 시장 세분화를 달성 할 수 없습니다. 할 수 없습니다. 따라서 2024년 총 출하량에서 미니 LED 백라이트 TV는 사상 처음으로 OLED TV를 앞지를 것으로 예상됩니다.

장기적인 관점에서 볼 때, 미니 LED 백라이트 TV의 가격은 OLED TV보다 낮게 유지될 것이며, 일부 제품은 하이엔드 LCD와 가격대가 겹치면서 미니 LED 제품의 보급률이 더욱 높아질 것으로 예상됩니다.

본 보고서에서는 Mini LED 백라이트 디스플레이 산업에 대해 조사 분석하여 출하량 및 보급률 예측, 기술 개발 동향, TV, IT, 자동차 등 3대 시장의 개발 동향 등을 제공합니다.

목차

제1장 Mini LED 백라이트/OLED 용도 출하대수와 보급률 예측

소비자 일렉트로닉스용 Mini LED 백라이트 출하대수(2024년-2028년)

Mini LED 백라이트 소비자 일렉트로닉스에의 보급(2024년-2028년)

Mini LED 백라이트/OLED TV 출하대수(2024년-2028년)

Mini LED 백라이트/OLED TV 보급률(2024년-2028년)

Mini LED 백라이트/OLED MNT 출하대수(2024년-2028년)

Mini LED 백라이트/OLED MNT 보급률(2024년-2028년)

Mini LED 백라이트/OLED NB 출하대수(2024년-2028년)

Mini LED 백라이트/OLED NB 보급률(2024년-2028년)

Mini LED 백라이트/OLED 태블릿 출하대수(2024년-2028년)

Mini LED 백라이트/OLED 태블릿 보급률(2024년-2028년)

Mini LED 백라이트 VR 출하대수와 보급률(2024년-2028년)

Mini LED 백라이트 TV 유형과 LED 수요(2024년-2028년)

Mini LED 백라이트 MNT 유형과 LED 수요(2024년-2028년)

Mini LED 백라이트 NB 유형과 LED 수요(2024년-2028년)

Mini LED 백라이트 태블릿 유형과 LED 수요(2024년-2028년)

Mini LED 백라이트 VR 유형과 LED 수요(2024년-2028년)

Mini LED 백라이트 용도에 요구되는 LED(COB)

Mini LED 백라이트 용도에 요구되는 LED(POB)

Mini LED 백라이트 용도용 LED(COB) 매출

Mini LED 백라이트 용도용 LED(POB) 매출

Mini LED 백라이트 용도용 LED(COB/POB) 매출

제2장 Mini LED 백라이트 기술 개발 동향

COB 기술 비용 분석

PCB 비용 분석

LED 칩 비용 분석

Mini LED 백라이트 구동 아키텍처 분석

드라이버 IC 비용 분석

AM 드라이버 IC시장 분석

주류 8채널 AM 드라이버 IC 비교

프로세스와 재료 비용 분석

제8.x세대 OLED 패널 공장 투자 계획

Apple OLED 기술을 자사 제품에 통합할 계획

OLED 기술 로드맵

OLED 효율 향상 - CSOT 잉크젯 VS. UDC 드라이 프린트

OLED 효율 개선 - JDI eLEAP VS. Visionox ViP

제3장 Mini LED 백라이트/OLED TV 시장

Mini LED 백라이트/OLED TV 입수 가능한 수량 : 지역별

Mini LED 백라이트/OLED TV 가격차 : 지역별

초대형 TV 수요 - 75인치와 80인치(2022년-2024년)

초대형 TV 수요 - 98인치와 100인치(2023년-2024년)

Mini LED 백라이트 TV 가격 변화 : 지역별

중국 Mini LED 백라이트 TV 사양과 가격 변화

중국 저가격 Mini LED 백라이트 TV 사양과 가격 변화

로 존 TV 백라이트 비용 분석

밋드존 TV 백라이트 비용 분석

하이 존 TV 백라이트 비용 분석

브랜드 : Mini LED 백라이트 모델 개요(2023년·2024년)

Mini LED 백라이트 TV 출하대수 : 브랜드별(2023년-2024년)

Mini LED 백라이트 TV 공급망 분석

주류 Mini LED 백라이트 TV 판매 가격 비교

OLED TV 출하대수와 보급률(2023년-2024년)

TV패널 가격 비교 : 55인치 OLED vs. LCD 오픈 셀

제4장 Mini LED 백라이트/OLED IT 시장

1. MNT 시장

Mini LED 백라이트/OLED MNT 입수 가능한 수량 : 지역별

중국의 Mini LED 백라이트 MNT 수량 변화

Mini LED 백라이트/OLED MNT 가격차 : 지역별

Mini LED 백라이트 MNT 가격 변화 : 지역별

중국의 Mini LED 백라이트 MNT 사양과 가격 변화

미국의 Mini LED 백라이트 MNT 사양과 가격 변화

영국의 Mini LED 백라이트 MNT 사양과 가격 변화

중국의 유리 기반 Mini LED 백라이트 MNT 사양과 가격 변화

Mini LED 백라이트 MNT 출하대수 : 브랜드별(2023년-2024년)

주류 OLED MNT 판매 가격 비교(2024년)

OLED MNT 패널 공급 상황(2023년-2025년)

OLED MNT 점유율 : 브랜드별(2023년-2024년)

2. NB시장

Mini LED 백라이트/OLED NB 입수 가능한 수량 : 지역별

Mini LED 백라이트/OLED NB 가격차 : 지역별

Mini LED 백라이트 NB 가격 변화 : 지역별

NB LTPS LCD 패널 출하대수(2023년-2025년)

NB OLED 패널 출하대수 예측(2022년-2027년)

OLED NB세트 출하대수 예측(2022년-2027년)

3. 태블릿 시장

Mini LED 백라이트/OLED 태블릿 입수 가능한 수량 : 지역별

Mini LED 백라이트/OLED 태블릿 가격차 : 지역별

4. 기타 지역에서의 응용

인도의 Mini LED 백라이트/OLED 용도 이용 가능한 수량

인도의 Mini LED 백라이트/OLED 용도 가격차

브라질의 Mini LED 백라이트/OLED 용도 이용 가능한 수량

브라질의 Mini LED 백라이트/OLED 용도 가격차

제5장 Mini LED 자동차용 디스플레이 시장

스마트 콕핏 동향

자동차용 디스플레이 기술 개요

자동차용 디스플레이 패널 출하대수와 보급률(2024년-2028년)

자동차용 백라이트 LED 시장 매출 분석(2024년-2028년)

Mini LED/HDR 자동차용 디스플레이 동향 - 패널 사이즈(2022년-2023년)

Mini LED/HDR 자동차용 디스플레이 동향 - 디밍 존(2022년-2023년)

Mini LED/HDR 자동차용 디스플레이 - 사양 vs. 공급망(2022년)

Mini LED/HDR 자동차용 디스플레이 - 사양 vs. 공급망(2023년)

COB/COG/POG 기술 분석

Mini LED/HDR 자동차용 디스플레이 스케줄과 사양(2022년-2028년)

Cadillac LYRIQ Automotive Display - 사양과 분석

Roewe RX5 Automotive Display - 사양과 비용 분석

Cadillac LYRIQ Automotive Display - 사양과 분석

Buick Electra E5 Automotive Display - 사양과 분석

Lincoln Nautilus Automotive Display - 사양과 분석

Cadillac Celestiq Automotive Display - 사양과 분석

LCD (Edge / Direct-Type) vs. OLED Automotive Display Specification

자동차용 디스플레이 비용 분석 - 엣지/직접 유형(2024년)

자동차용 백라이트 LED 제품 사양과 가격 분석(2024년)

Mini LED 자동차용 디스플레이 - 드라이버 IC 사양 분석

Mini LED 자동차용 디스플레이 - 직접/스캔 드라이버 IC 장단점 분석

OLED 자동차용 디스플레이 스케줄과 사양(2022년-2024년)

자동차용 백라이트 디스플레이 시장 구도 분석

HUD 시장 출하대수 - 제품과 지역 시장 분석(2024년-2028년)

HUD 제품 사양 분석(2024년)

AR-HUD 기술 분석

HUD 제품 가격 분석(2023년-2024년)

파노라마 헤드업 디스플레이(P-HUD)와 투명 디스플레이

AR-HUD OEM 공급망과 제품 사양 분석

HUD 시장 구도 분석

제6장 Mini LED 백라이트 산업 역학, Mini LED 백라이트 시장 공급망

LED 칩 제조업체 : HC Semitek

LED 칩 제조업체 : Aucksun

드라이버 IC 제조업체 : HYASiC

드라이버 IC 제조업체 : X-Signal Integrated

장비 기업 : Kulicke & Soffa

장비 프로바이더 : HOSON

LED 패키지 프로바이더 : Everlight

LED 패키지 프로바이더 : Lextar

LED 패키지 프로바이더 : Jufei

LED 패키지 프로바이더 : APT Electronics

LED 패키지 프로바이더 : Hongli Display

LED 패키지 프로바이더 : Nationstar

LED 모듈 제조업체 : Core Photoelectric Technology

LED 패키지 프로바이더 : HGC

LED 패키지 프로바이더 : ESPACE

LED 패키지 프로바이더 : COREACH

LED 유리기재 제조업체 : WG Tech

용도 기업 : BOE

용도 기업 : Tianma

용도 기업 : TCL

용도 기업 : Hisense

용도 기업 : Xiaomi

LSH

영문 목차

영문목차

INFOGRAPHICS

2024-2028 Mini LED Backlight Applications Shipments Forecast

Chapter 1 Industry Trends: Mini LED and OLED in Zero-sum Game, with Fierce Competition between Large-, Mid-, and Small-size Displays

With expanded shipments of LCD panels engineered with Mini LED backlight for various segments, the confrontation with OLED is inevitable. In various application across large, medium, and small panels, it has become a zero-sum game: gains for Mini LED backlight come at the expense of OLED, and vice versa. Interestingly, this is not the typical one-way replacement mode usually seen in the history of technological development. Instead, both technologies have their own strengths and weaknesses, competing closely with each other.

Although the Mini LED backlight TV market makes a significant increase in 2024, the positive impact of OLED technology in the IT market has also suppressed the enthusiasm of brands in investing in Mini LED backlight technology. TrendForce estimates that the total shipment of each application will be 12.7Mpcs in 2024, a decrease of 5% compared to 2023.

In the TV, automotive, and future MNT markets, Mini LED holds more advantages over OLED. The cost reduction effect of Mini LED backlight TV is significant, while OLED technology shows limited strength in the large-sized TV market. To enhance product differentiation and increase brand competitiveness, Mini LED backlight technology is the preferred solution for upgrading product specifications. In the long term, this trend will also have a positive impact on the MNT market, driving an increase in its penetration rate. In the automotive market, Mini LED backlight have won the reliability advantage, resulting in a higher share of shipments than OLED.

However, in the NB , Tablet, and VR sectors, Mini LED is not as competitive as OLED.Apple's embrace of OLED for NB and Tablet products will change the entire market landscape, leading to a continuous reduction in the penetration rate of Mini LED backlight technology in these two application areas.

Chapter 2 Technical Focus: Mini LED Strives for Cost Down, while OLED Aims at Better Performance

The biggest change in Mini LED backlight in 2024 is that the solutions are gradually becoming more mature, and manufacturers throughout the upstream and downstream segments have reached a consensus on ways to reduce costs. This chapter explores the cost reduction strategies that the industry is focusing on, including various strategies related to PCB, LED chips, driver IC, and process materials. The industry-wide consensus helps accelerate the standardization of products, which encourages suppliers to boldly scale up and further enhance cost competitiveness. As a result, the biggest obstacle to the development of Mini LED backlight is expected to be removed. According to TrendForce's analysis, cost reduction strategies for Mini LED that have achieved high consensus are as follows:

1. PCB Cost Down Analysis

The form of PCB has transitioned from FR4 to single-sided aluminum substrates, comb boards, and light bars, which are applied to products with high, medium, and low dimming zone count, respectively.

The harpoon board design enhances PCB material utilization, reducing the cost by more than 30%.

Reduced material usage, increased single-board utilization, and decreased precision requirements have lowered PCB manufacturing costs but introduced reliability challenges.

The key opportunity for cost reduction lies in whether the size of individual light boards can be standardized.

2. LED Chip Cost Down Analysis

Increasing the pitch or optimizing the light emission angle through optical design to reduce the number of LEDs can achieve cost reduction.

Using high-voltage chips(18V/24V/36V) not only reduces the number of LED per zone but also offers higher luminous efficiency, lower driving current, and simpler routing overall.

3. Driver IC Cost Down Analysis

Among the two driving modes, Passive Matrix (PM) and Active Matrix (AM), the AM scheme is widely adopted due to its simple wiring and the ability to drive each zone separately.

The AM driver IC is paired with a single-layer aluminum substrate and high-voltage LED chips to reduce the number of LED series connections, maximize driving efficiency, and lower PCB wiring complexity.

As the number of dimming zones increases, more driver IC are needed.

The material costs of using an AM driver IC are significantly reduced by over 70% compared to a PM driver IC, and increasing the number of channels further expands the cost reduction advantage.

4. Process and Materials Cost Down Analysis

Currently, mainstream COB products are engineered with dispensing technology, which reduces material and manufacturing process costs while improving light uniformity.

some manufacturers have replaced QD diffusion films with QD diffusion plates, reducing the cost by 20% in a single-channel process. However, high-temperature reliability challenges may still be encountered.

This chapter also discusses how, under the significant cost reduction pressure from Mini LED players, OLED manufacturers are advancing their technology to make their solutions increasingly refined, thereby defending against the threat posed by Mini LED.

Chapter 3 TV Market: Successful Market Segmentation Allows Mini LED TVs to Surpass OLED TVs in Global Sales for the First Time

From this chapter to Chapter 5, we will analyze the development trends of Mini LED backlight in the three major markets: TV, IT, and automotive.

In 2024, the estimated shipment of Mini LED backlight TV is 6,420K units. Chinese brand manufacturers have gained dominance in the market. With the improvement of the Mini LED backlight supply chain and the gradual implementation of cost reduction strategies by various companies, there has been significant growth, with global shipments increasing by 59% compared to 2023.

Although OLED has products such as 77-inch and 83-inch displays for the 70-80 inch range, its cost competitiveness in G8.5 production is poor, leading to OLED's inability to keep up with LCD in flexible layouts for extra-large sizes.Given the relatively concentrated supply, inflexible panel prices, changes in branding strategy, and the concentration of economic cutting size at 55 and 65 inches, OLED cannot achieve desirable market segmentation like Mini LED backlight TV through a diversified coverage strategy. Therefore, for the first time in history, Mini LED backlight TV will surpass OLED TV in total shipments for 2024.

From a long-term perspective, the pricing of Mini LED backlight TVs is expected to remain lower than that of OLED TVs, with some products even overlapping in pricing with high-end LCD, further increasing the penetration rate of Mini LED products.

Chapter 4 IT Market: As OLED Solidifies Its High-End Status, Mini LED is Likely to Become a "Wall Breaker"

Shipment of Mini LED backlight MNT in 2024 is estimated to be 347K units, which is only a 48% growth rate compared to 2023, lower than initially expected. This is mainly because of the positive response to OLED technology in the high-end market, leading brands to invest more actively in OLED product lines, resulting in Samsung's market share shrinking to 46%. However, Chinese brands continue to enter the mid-to-low-end market, but due their limited recognition and promotion efforts, benefits are limited.

Chinese brands such as Taidu and Titan Army continue to advance the specifications of

OLED MNT are currently in high demand and are almost a standard configuration product for all brands targeting the high-end market.In 2024, the supply capacity of OLED MNT will double compared to 2023. SDC's QD OLED, accounting for 75%, remains mainstream, while LGD's WOLED supply scale is also gradually increasing.Due to the strong demand, the supply of OLED MNT panels is expected to climb to 2.4 million pieces in 2025, with CSOT also joining the supply ranks.With the increasing availability of OLED MNT panels, the willingness of brands to adopt Mini LED backlight will also be correspondingly weakened.Brands almost universally allocate their high-end MNT resources to the promotion of OLED, causing a significant crowding-out effect on similarly positioned Mini LED backlight products.

In the long run, we still have faith in the development of Mini LED applications in the IT sector. As the shipments of Mini LED backlight TV increase, the cost reduction benefits are expected to extend to MNT applications, once again demonstrating the strategic advantage of diversified coverage for Mini LED products. Mini LED could overcome the current situation where high-end MNT products are primarily confined to the gaming market.

The rest of this chapter includes analyses of the price differences between Mini LED backlight and OLED products in the NB market, as well as shipment analysis. In addition to analyzing product specifications in the major markets, namely the US, Europe, and China, this report also offers insights into India and Brazil by analyzing the models available and the local price trends of new Mini LED backlight and OLED displays.

Chapter 5 Automotive Market: Smart Cockpit Transitions from Concept to Mass Production, Allowing Mini LED to Benefit from Increased Display Number and Size

With the trend towards digitalization in smart cockpit, automotive displays have become a crucial interface for connecting vehicles and driver interaction. Automotive displays include instrument clusters, central displays, rear view mirrors, HUD, rear-seat entertainment applications, and more. With an increasing number of vehicles incorporating a variety of automotive display products, larger sizes, wider aspect ratios, more displays, and freer placement methods are becoming the development direction for in-car displays. Additionally, the continuous improvement of performance parameters such as High Dynamic Range (HDR), Local Dimming, Wide Color Gamut, etc., coupled with the increasing demand for automotive displays, indicates a sustained rapid growth trend in the automotive display market.According to TrendForce analysis, the shipment of automotive display panels is expected to reach 257 million units in 2028. Mini LED displays will reap the benefits, with a penetration rate of 5.9%, surpassing OLED's 4.1%.

Chapter 6 Industry Dynamics: From a Competitive Landscape of Numerous Businesses to Major Manufacturers, Elite Mini LED Players Have Emerged

As Mini LED backlight products gradually enter the mass production stage, there have been significant changes in the list of highly active manufacturers. Different players have bet on various technologies and product solutions. By 2024, mainstream technologies and solutions become clear throughout the market. Manufacturers who have made the right bets are now enjoying the winners' dividends and returns, while those who missed out are gearing up for another round of intense investments.

This chapter outlines the main supply chain for the Mini LED backlight market, focusing on the dynamics of leading manufacturers in chips, driver IC, transfer equipment, packaging and modules, and applications regarding their products, technologies, revenues, and supply chain activities in the Mini LED sector.

Compared to the conventional backlight, Mini LED backlight represents a major technological innovation, bringing significant changes to the industry landscape. Conventional backlight supply chain companies have strong first-mover advantages and incumbent benefits. However, new players are also fully benefiting from these changes, breaking the previous monopoly and rising to prominence. By 2024, powerful players have begun to take center stage in the industry arena.

In this report, we have added the analyses of niche businesses benefiting from Mini LED backlight, such as Aucksun, HYASiC, X-Signal Integrated, APT Electronics, Core Photoelectric Technology, HGC, COREACH, and ESPACE. We have also added an analysis focusing on the current development of WG Tech, a company with a comprehensive presence in LED glass substrates manufacturing.

Table of Contents

Chapter I. Mini LED Backlight/OLED Application Shipment and Penetration Rates Forecast

2024-2028 Mini LED Backlight Shipment for Consumer Electronics Applications

2024-2028 Mini LED Backlight Penetration for Consumer Electronics Applications

2024-2028 Mini LED Backlight/OLED TV Shipment

2024-2028 Mini LED Backlight/OLED TV Penetration Rate

2024-2028 Mini LED Backlight/OLED MNT Shipment

2024-2028 Mini LED Backlight /OLED MNT Penetration Rate

2024-2028 Mini LED Backlight/OLED NB Shipment

2024-2028 Mini LED Backlight /OLED NB Penetration Rate

2024-2028 Mini LED Backlight/OLED Tablet Shipment

2024-2028 Mini LED Backlight /OLED Tablet Penetration Rate

2024-2028 Mini LED Backlight VR Shipment and Penetration Rate

2024-2028 Mini LED Backlight TV Types and LED Demand

2024-2028 Mini LED Backlight MNT Types and LED Demand

2024-2028 Mini LED Backlight NB Types and LED Demand

2024-2028 Mini LED Backlight Tablet Types and LED Demand

2024-2028 Mini LED Backlight VR Types and LED Demand

LED (COB) Demanded for Mini LED Backlight Applications

LED (POB) Demanded for Mini LED Backlight Applications

LED (COB) Revenue for Mini LED Backlight Applications

LED (POB) Revenue for Mini LED Backlight Applications

LED (COB/POB) Revenue for Mini LED Backlight Applications

Chapter II. Mini LED Backlight Technology Development Trend

COB Technology Cost Down Analysis

PCB Cost Down Analysis

LED Chip Cost Down Analysis

Mini LED Backlight Driving Architecture Analysis

Driver IC Cost Down Analysis

AM Driver IC Market Analysis

Mainstream 8-Channel AM Driver IC Comparison

Process and Materials Cost Down Analysis

8.x Generation OLED Panel Factory Investment Plan

Apple's Plan for Integrating OLED Technology into Its Products

OLED Technology Roadmap

OLED Efficacy Improvement - CSOT Ink-jet VS. UDC Dry Printed

OLED Efficacy Improvement - JDI eLEAP VS. Visionox ViP

Chapter III. Mini LED Backlight/OLED TV Market

Quantity of Available Mini LED Backlight/OLED TV in Different Regions

Mini LED Backlight/OLED TV Price Differences in Different Regions

2022-2024(E) Demand for Super-Large Sized TV - 75" and 80"

2023-2024(E) Demand for Ultra-Large Sizes TV - 98" and 100"

Mini LED Backlight TV Price Changes in Different Regions

Mini LED Backlight TV Specifications and Price Changes in China

Low-Priced Mini LED Backlight TV Specifications and Price Changes in China

Low-Zones TV Backlight Cost Analysis

Mid-Zones TV Backlight Cost Analysis

High-Zones TV Backlight Cost Analysis

Brands: 2023 and 2024 Mini LED Backlight Models Overview

2023-2024 Mini LED Backlight TV Shipments by Brand

Mini LED Backlight TV Supply Chain Analysis

Mainstream Mini LED Backlight TV Selling Price Comparison

2023-2024(E) OLED TV Shipment and Penetration Rate

TV Panel Price Comparison: 55" OLED vs. LCD Open Cell

Chapter IV. Mini LED Backlight/OLED IT Market

4.1. MNT Market

Quantity of Available Mini LED Backlight/OLED MNT in Different Regions

Quantity Changes of Mini LED Backlight MNT in China

Mini LED Backlight/OLED MNT Price Differences in Different Regions

Mini LED Backlight MNT Price Changes in Different Regions

Mini LED Backlight MNT Specifications and Price Changes in China

Mini LED Backlight MNT Specifications and Price Changes in the US

Mini LED Backlight MNT Specifications and Price Changes in the UK

Glass-based Mini LED Backlight MNT Specifications and Price Changes in China

2023-2024 Mini LED Backlight MNT Shipments by Brand

1H24 Mainstream OLED MNT Selling Price Comparison

2023-2025(F) OLED MNT Panel Supply Status

2023-2024(E) OLED MNT Share by Brands

4.2. NB Market

Quantity of Available Mini LED Backlight/OLED NB in Different Regions

Mini LED Backlight/OLED NB Price Differences in Different Regions

Mini LED Backlight NB Price Changes in Different Regions

2023-2025(F) NB LTPS LCD Panel Shipment

2022-2027(F) NB OLED Panel Shipment Forecast

2022-2027(F) OLED NB Set Shipment Forecast

4.3. Tablet Market

Quantity of Available Mini LED Backlight/OLED Tablet in Different Regions

Mini LED Backlight/OLED Tablet Price Differences in Different Regions

4.4. Applications in Other Regions

Quantity of Available Mini LED Backlight/OLED Applications in India

Mini LED Backlight/OLED Applications Price Differences in India

Quantity of Available Mini LED Backlight/OLED Applications in Brazil

Mini LED Backlight/OLED Applications Price Differences in Brazil

Chapter V. Mini LED Automotive Display Market

Smart Cockpit Trend

Automotive Display Technology Overview

2024-2028 Automotive Display Panel Shipment and Penetration Rate

2024-2028 Automotive Backlight LED Market Value Analysis

2022-2023 Mini LED / HDR Automotive Display Trend- Panel Size

2022-2023 Mini LED / HDR Automotive Display Trend- Dimming Zones

2022 Mini LED / HDR Automotive Display- Specification vs. Supply Chain

2023 Mini LED / HDR Automotive Display- Specification vs. Supply Chain

COB / COG / POG Technology Analysis

2022-2028 Mini LED / HDR Automotive Display Schedule and Specification