자발적 탄소배출권 시장 : 업계 동향과 세계 예측(-2035년) - 프로젝트별, 거래 유형별, 응용 분야별, 최종사용자별, 지역별

Voluntary Carbon Credit Market: Industry Trends and Global Forecasts, till 2035 - Distribution by Project, Transaction, Application Area, End User and Geography

상품코드:1869573

리서치사:Roots Analysis

발행일:2025년 10월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

한글목차

세계의 자발적 탄소배출권 시장 : 개요

Roots Analysis의 조사에 따르면, 세계 자발적 탄소배출권 시장 규모는 예측 기간 동안 CAGR 40%로 성장하여 현재 16억 달러에서 475억 달러에 달할 것으로 예측됩니다.

시장 규모 및 기회 분석은 다음 매개 변수를 기반으로 세분화됩니다.

프로젝트

재생에너지 프로젝트

에너지 효율화 프로젝트

임업 및 토지 이용 프로젝트

메탄 회수 및 처리 프로젝트

기타 프로젝트

거래 유형

탄소 제거

탄소 저감

복합거래

응용 분야

산업 부문

가정 부문

에너지 부문

농업 분야

기타

최종 사용자

정부기관-단체

비영리단체

비상장사

개인

지역

북미(미국 및 캐나다)

유럽(오스트리아, 벨기에, 에스토니아, 프랑스, 독일, 이탈리아, 네덜란드, 스페인, 스웨덴, 영국, 기타)

탄소배출권은 다양한 기후 변화 대응을 통해 달성한 대기 중 온실가스의 감축 또는 제거를 의미합니다. 이러한 크레딧은 규제 준수 의무를 충족하기 위해 획득하거나 자발적으로 구매합니다. 배출 감소 노력은 이해관계자들이 자발적으로 배출을 줄이거나 방지하여 환경에 미치는 영향을 줄이기 위해 시장에 이익을 가져다줍니다. 이 시장은 기후 변화와 관련된 전 지구적 과제를 해결하기 위한 중요한 수단이 되고 있습니다. 정부 규제나 배출권 거래제의 영향을 받는 규제 준수 시장과 달리, 자발적 탄소배출권 부문은 비강제적 원칙에 따라 기업, 개인, 조직이 자발적으로 탄소배출량을 상쇄할 수 있도록 하는 자율적 탄소배출권 부문이 있습니다. 2021년에는 자발적 탄소배출권 거래 수익이 20억 달러를 넘어섰고, 시장은 정점을 찍었습니다. 이러한 확대는 공공 및 민간 부문 모두에서 탄소 배출량을 줄이고 지속가능성으로의 전환을 위한 지속적인 노력에 의해 추진되고 있습니다. 프로젝트 개발자는 조림, 블루카본, 클린 쿠킹, 깨끗한 물, 산림보전, 재조림, 토지보전, 재생에너지 프로젝트 등 다양한 노력을 통해 다양한 유형의 탄소배출권을 제공합니다.

또한, 이 시장의 최종 사용자는 자발적인 탄소 상쇄 활동에 참여함으로써 온실가스 배출량 감축에 기여하고, 생물다양성 증진, 환경 복원력 강화, 지속 가능한 개발을 촉진하는 프로젝트에 재정적 지원을 제공합니다. 자발적 탄소배출권은 환경적 측면의 촉매제이자 경제적 측면의 촉진제 역할을 하며, 혁신을 촉진하고 새로운 비즈니스 기회를 창출하고 있습니다. 환경-사회-지배구조(ESG) 목표가 비즈니스 전략에 통합되는 움직임이 가속화되면서 탄소배출권에 대한 수요는 더욱 증가할 것으로 예측됩니다.

기업과 정부 기관 및 단체들이 야심찬 기후 목표를 추구하는 가운데, 자발적 탄소배출권 시장은 세계 저탄소 경제로의 전환을 가능하게 하는 데 중요한 역할을 할 것입니다. 또한, 기업의 순배출량 제로 목표에 대한 노력 강화는 향후 10년간 시장의 큰 성장을 견인할 것으로 예측됩니다.

세계의 자발적 탄소배출권 시장 : 주요 연구 결과

이 보고서는 자발적 탄소배출권 시장의 현황을 상세하게 분석하고, 업계의 잠재적인 성장 기회를 파악합니다. 주요 조사 결과는 다음과 같습니다.

1. 자발적 탄소배출권 제공업체는 다양한 프로젝트를 통해 생성된 탄소배출권을 제공함으로써 기후 변화 문제 해결에 기여하고 있습니다.

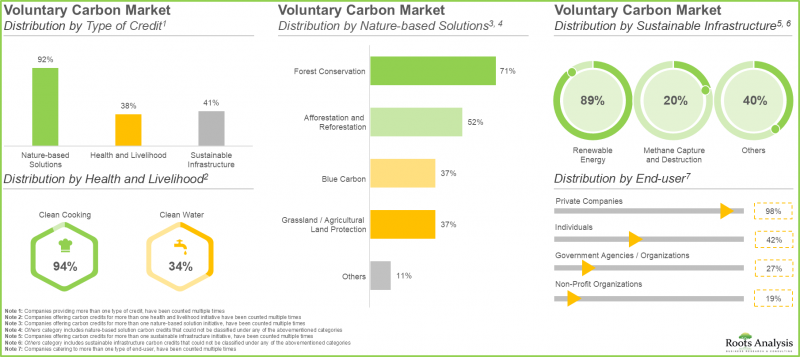

2. 90% 이상의 사업자가 자연기반형 솔루션(NBS) 이니셔티브를 통해 탄소배출권을 제공하고 있으며, 이 중 약 70%의 탄소배출권은 산림보전 프로젝트별로 생성되고 있습니다.

3. 지속 가능한 실천에 대한 관심 증가와 기후 변화에 대한 우려 증가가 자발적 탄소배출권 시장의 성장을 주도하고 있으며, 가까운 시일 내에 큰 폭의 성장이 예상됩니다.

4. 현재 세계 자발적 탄소배출권 시장 규모는 16억 달러로 추정되며, 향후 10년간 CAGR 40%를 보일 것으로 예측됩니다.

5. 상세한 시장 예측 분석은 과거 데이터(2020년 이후)와 올해 및 향후 10년간(2035년까지)의 전반적인 기회를 보여줍니다.

세계의 자발적 탄소배출권 시장 : 주요 부문별 시장 현황

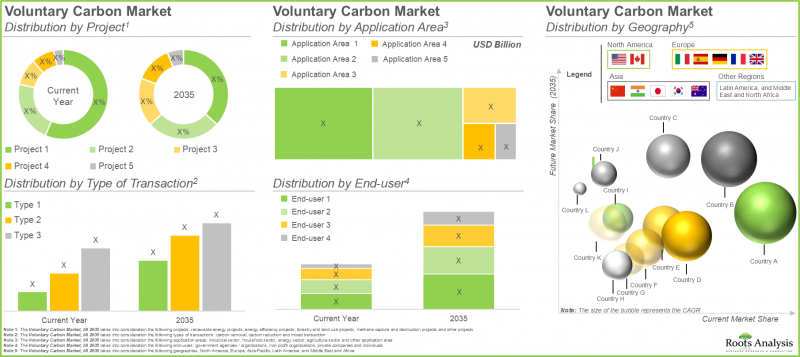

재생에너지 프로젝트가 상대적으로 높은 자발적 탄소배출권 시장 점유율을 차지하고 있습니다.

세계 자발적 탄소배출권 시장은 재생에너지 프로젝트, 에너지 효율화 프로젝트, 산림 및 토지이용 프로젝트, 메탄 회수 및 파괴 프로젝트, 기타 프로젝트 등 다양한 프로젝트로 분류됩니다. 현재 재생에너지 프로젝트가 상대적으로 높은 시장 점유율(30% 이상)을 차지하고 있지만, 가까운 시일 내에 이러한 상황이 바뀔 가능성이 높으며, 산림 및 토지 이용 프로젝트 부문은 예측 기간 동안 큰 폭의 성장이 예상됩니다.

이는 산림 관리가 산림 파괴와 산림 황폐화를 억제하여 배출량 흡수를 촉진하기 때문입니다. 또한, 임업 및 토지 관리 노력은 기후 변화의 영향과 생물 다양성 감소를 완화하는 데 도움이 됩니다.

탄소 제거 부문은 더 높은 CAGR로 성장할 것으로 예측됩니다.

세계 시장은 탄소 제거, 탄소 감축, 혼합 거래 등 다양한 거래 유형으로 구분됩니다. 현재 혼합 거래 부문이 자발적 탄소배출권 시장에서 가장 큰 점유율(45% 이상)을 차지하고 있으며, 이러한 추세는 향후 10년간 지속될 것으로 예측됩니다. 그러나 그린워싱에 대한 인식 증가와 규제 지침의 변화 등 여러 가지 이유로 탄소 제거 부문은 상대적으로 높은 성장률을 보일 것으로 예측됩니다.

산업 부문은 현재 자발적 탄소배출권 시장에서 가장 큰 점유율을 차지하고 있습니다.

이 부문에서는 산업 부문, 가정 부문, 에너지 부문, 농업 부문, 기타 응용 분야 등 다양한 응용 분야에 걸친 세계 시장 구분을 밝힙니다. 이러한 응용 분야 중 산업 부문은 현재 자발적 탄소배출권 시장에서 가장 큰 점유율을 차지하고 있으며, 예측 기간 동안에도 주도적인 위치를 유지할 것으로 예측됩니다. 이는 업계 관계자들의 순배출량 제로 이니셔티브에 대한 채택 확대와 연관되어 시장 성장을 가속하고 있습니다. 또한, 에너지 부문은 다른 부문에 비해 높은 CAGR로 성장할 것으로 예상된다는 점도 주목할 만합니다.

비상장 기업 부문이 시장 점유율의 대부분을 차지할 것으로 예측됩니다.

최종 사용자별로 살펴보면, 세계 자발적 탄소배출권 시장은 정부기관 및 단체, 비영리단체, 민간기업, 개인 등 다양한 최종 사용자로 구분됩니다. 현재 민간 기업 부문이 시장 점유율의 대부분(약 45%)을 차지하고 있으며, 이러한 추세는 앞으로도 변함없이 유지될 것으로 보입니다. 또한, 비상장 기업 부문은 2035년까지 연간 약 40%의 성장률을 보일 것으로 예측됩니다. 이는 환경에 미치는 영향을 최소화하고 지속가능성 목표 달성에 집중하는 비상장기업들이 자발적 탄소배출권 사용을 확대하여 탄소배출량을 상쇄하려는 노력의 결과입니다.

북미가 주요 시장 점유율을 차지할 것으로 예측됩니다.

지역별로는 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 시장이 구분됩니다. 현재 북미가 시장 점유율의 대부분(30% 이상)을 차지하고 있지만, 향후 10년간은 유럽 시장이 점유율의 대부분을 차지할 것으로 예측됩니다. 주목할 만한 점은 2035년까지 예측 기간 동안 아시아태평양의 자발적 탄소배출권 시장 점유율이 다른 지역에 비해 상대적으로 빠른 속도(CAGR 42%)로 성장할 것으로 예상된다는 점입니다.

전 세계 자발적 탄소배출권 시장의 대표적인 진출 기업들

3Degrees

Climate Impact Partners

ClimateSeed

Cool Effect

Earthly

Ecologi Impact Funds

EKI Energy Services

First Climate

Green Wedge

Greenfleet

natureOffice

Solaxy Group

South Pole

The Carbon Collective Company

목차

섹션 I : 보고서 개요

제1장 배경

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

섹션 II : 정성적 인사이트

제5장 주요 요약

제6장 서론

탄소배출권 개요

탄소 배출권 발행자

탄소배출권 유형

자발적 탄소배출권 시장 소개

자발적 탄소 프로젝트 가격에 영향을 미치는 요인

자발적 탄소배출권의 자점

향후 전망

섹션 III : 시장 개요

제7장 경쟁 구도

조사 방법과 주요 파라미터

자발적 탄소배출권 제공 업자 : 전체적 상황

자발적 탄소배출권 시장 : 전체 상황

섹션 IV : 기업 개요

제8장 기업 개요

개요

자발적 탄소배출권 주요 제공 업자

EKI Energy Services

3Degrees

Climate Impact Partners

Cool Effect

Ecologi Impact Funds

natureOffice

Solaxy Group

기타 기업

ClimateSeed

Earthly

First Climate

Green Wedge

Greenfleet

South Pole

The Carbon Collective Company

섹션 V : 시장 동향

제9장 사례 연구 : 자주 배출 시장 대형 제약 기업의 영향

본 장의 개요

조사 방법과 주요 파라미터

자발적 탄소배출권 시장 대형 제약 기업의 영향

Johnson & Johnson

Roche

Pfizer

AbbVie

AstraZeneca

Novartis

Bristol Myers Squibb

GlaxoSmithKline

제10장 시장 영향 분석 : 성장 촉진요인 및 억제요인, 기회, 과제

본 장의 개요

시장 성장 촉진요인

시장 성장 억제요인

시장 기회

시장이 해결해야 할 과제

결론

섹션 VI : 시장 예측과 기회 분석

제11장 자발적 탄소배출권 시장

제12장 자발적 탄소배출권 시장(프로젝트별)

제13장 자발적 탄소배출권 시장(거래 유형별)

제14장 자발적 탄소배출권 시장(응용 분야별)

제15장 자발적 탄소배출권 시장(최종사용자별)

제16장 자발적 탄소배출권 시장(지역별)

섹션 VII : 지역 시장 기회 분석

제17장 시장 기회 분석 : 북미

제18장 시장 기회 분석 : 유럽

제19장 시장 기회 분석 : 아시아태평양

제20장 시장 기회 분석 : 라틴아메리카

제21장 시장 기회 분석 : 중동 및 아프리카

섹션 VIII : 기타 독점적 통찰

제22장 1차 조사에서의 인사이트

제23장 결론

제24장 커스터마이즈 기회

제25장 ROOT 구독 서비스

제26장 저자 상세

섹션 IX : 부록

제27장 표 형식 데이터

제28장 기업 및 단체 리스트

LSH

영문 목차

영문목차

GLOBAL VOLUNTARY CARBON CREDIT MARKET: OVERVIEW

As per Roots Analysis, the global voluntary carbon credit market is expected to grow from USD 1.6 billion in the current year to USD 47.5 billion, at a CAGR of 40% during the forecast period.

The market sizing and opportunity analysis has been segmented across the following parameters:

Project

Renewable Energy Projects

Energy Efficiency Projects

Forestry and Land Use Projects

Methane Capture and Destruction Projects

Other Projects

Type of Transaction

Carbon Removal

Carbon Reduction

Mixed Transaction

Application Area

Industrial Sector

Household Sector

Energy Sector

Agriculture Sector

Other Application Area

End User

Government Agencies / Organizations

Non-Profit Organizations

Private Companies

Individuals

Geography

North America (US and Canada)

Europe (Austria, Belgium, Estonia, France, Germany, Italy, Netherlands, Spain, Sweden, UK and Rest of Europe)

Asia-Pacific (Australia, China, India, Japan, Malaysia, Singapore, Thailand and Rest of Asia-Pacific)

Latin America (Argentina, Brazil and Rest of Latin America)

Middle East and Africa (Israel, Kenya, Kuwait, Malawi, Oman, South Africa, Uganda, UAE, Zambia and Rest of MEA)

GLOBAL VOLUNTARY CARBON CREDIT MARKET: GROWTH AND TRENDS

Carbon credits signify a decrease or elimination of greenhouse gases in the atmosphere achieved through several climate initiatives. These credits are acquired either to meet compliance obligations or are purchased on a voluntary basis. The carbon reduction initiatives benefit the market by stakeholders either willingly eliminate or prevent emissions to lessen their environmental impact. This market has become an essential tool for tackling worldwide issues related to climate change. In contrast to compliance markets that are influenced by government regulations and cap-and-trade systems, the voluntary carbon credit sector functions on a non-mandatory principle, enabling companies, individuals, and organizations to voluntarily compensate for their carbon emissions. In 2021, the market reached a peak with more than USD 2 billion in revenue from trading voluntary carbon credits. This expansion is driven by continuous initiatives to decrease carbon emissions and transition towards sustainability in both public and private sectors. To offer different kinds of carbon credits, the project developers engage in a diverse range of efforts, such as afforestation, blue carbon, clean cooking, clean water, forest preservation, reforestation, land safeguarding, and renewable energy projects.

Additionally, by engaging in voluntary carbon offset initiatives, the end users in this market aid in lowering greenhouse gas emissions and provide financial backing for projects that enhance biodiversity, environmental resilience, and sustainable development. Voluntary carbon credits serve as both an environmental catalyst and an economic driver, fostering innovation and generating new business prospects. With the growing integration of environmental, social, and governance objectives into business strategies, it is expected that the need for carbon credits will rise.

As both businesses and government agencies / organizations pursue ambitious climate goals, the voluntary carbon credit market will play an essential role in enabling a global transition to a low-carbon economy. Moreover, the increasing corporate commitment to net zero emissions targets is anticipated to drive significant growth in the market, in the coming decade.

GLOBAL VOLUNTARY CARBON CREDIT MARKET: KEY INSIGHTS

The report delves into the current state of voluntary carbon credit market and identifies potential growth opportunities within industry. Some key findings from the report include:

1. Voluntary carbon credit providers are dedicated to addressing climate change issues by offering carbon credits generated through a variety of projects.

2. More than 90% of the players provide carbon credits through nature-based solution initiatives; of these, nearly 70% of the credits are generated via forest conservation projects.

3. The piqued interest towards sustainable practices and increasing concerns related to climate change drives the market for voluntary carbon credits, positioning it for significant growth in the foreseeable future.

4. Currently, the global voluntary carbon market size is estimated to be worth USD 1.6 billion and is anticipated to grow at a CAGR of 40% over the next ten years.

5. The detailed market forecast analysis reveals the historical data (since 2020) and the overall opportunity in the current year and the next 10 years (till 2035).

GLOBAL VOLUNTARY CARBON CREDIT MARKET: KEY SEGMENTS

Renewable Energy Projects Occupies a Relatively Higher Voluntary Carbon Credit Market Share

The global voluntary carbon credit market is categorized into different projects, such as renewable energy projects, energy efficiency projects, forestry and land use projects, methane capture and destruction projects and other projects. Currently, the renewable energy projects occupy a relatively higher market share (more than 30%); however, this scenario is likely to change in the upcoming future and the forestry and land use projects segment and is expected to witness substantial growth during the forecast period.

This is because forest management enhances the absorption of emissions by regulating deforestation and forest degradation. Moreover, forestry and land management initiatives help reduce the effects of climate change and the decline of biodiversity.

Carbon Removal Segment Is Expected to Grow at a Higher CAGR

The global market is segmented across various types of transactions, such as carbon removal, carbon reduction and mixed transactions. Presently, the mixed transactions segment occupies the highest voluntary carbon credit market share (more than 45%), and this trend is unlikely to change over the next decade. However, the carbon removal segment is expected to grow at a relatively higher pace due to several reasons, including heightened awareness concerning greenwashing and changes in regulatory guidelines.

Industrial Sector Currently Occupies the Highest Voluntary Carbon Credit Market Share

This segment highlights the segmentation of global market across various application areas, such as industrial sector, household sector, energy sector, agriculture sector and other application areas. Among these application areas, the industrial sector segment currently occupies the highest voluntary carbon credit market share and is likely to stay dominant during the forecast period. This can be linked to the growing adoption of net zero emission initiatives by industry participants, fostering a flourishing market. Further, it is worth mentioning that the energy sector segment is expected to grow at a higher CAGR compared to other segments.

Private Companies' Segment Is Expected to Hold the Majority Market Share

In terms of end-users, the global voluntary carbon credit market is segmented across different types of end users, such as government agencies / organizations, non-profit organizations, private companies and individuals. Currently, private companies' segment is expected to hold the majority (nearly 45%) of the market share, and this trend is unlikely to change in the future as well. Further, private companies' segment is anticipated to grow at an annualized rate of ~40%, till 2035. This is a result of the growing use of voluntary carbon credit by private companies to counterbalance their carbon emissions, focusing on minimizing environmental impact and achieving their sustainability objectives.

North America is Likely to Capture the Major Market Share

In terms of geography, the global market is segmented across North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa. Currently North America is likely to capture the majority (over 30%) of the market share; however, in the upcoming decade the market for Europe is likely to capture majority of the market share. It is worth highlighting that during the forecast period till 2035, the voluntary carbon credit market share in Asia-Pacific is expected to grow at a relatively faster pace (CAGR of 42%) in comparison to other regions.

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders in this domain. The market report features detailed transcripts of interviews held with the following individuals:

Founder, Small Company, UAE

Managing Director, Small Company, Poland

Global Senior Director of Nature Based Solutions, Very Large Company, Switzerland

Team Lead Sales International, Mid-sized Company, Germany

Enterprise Innovation Lead, Small Company, UK

International Business Development and Strategic Business Partnerships, Small Company, France

Partnerships Coordinator, Small Company, Australia

Example Players in the Global Voluntary Carbon Credit Market

3Degrees

Climate Impact Partners

ClimateSeed

Cool Effect

Earthly

Ecologi Impact Funds

EKI Energy Services

First Climate

Green Wedge

Greenfleet

natureOffice

Solaxy Group

South Pole

The Carbon Collective Company

GLOBAL VOLUNTARY CARBON CREDIT MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global voluntary carbon credit market, focusing on key market segments, including [A] project, [B] type of transaction [C] application area, [D] end user and [H] geography.

Market Landscape: A comprehensive evaluation of voluntary carbon credit project developers, considering various parameters, such as [A] type of credit, [B] nature-based solution credits, [C] health and livelihood credits, [D] sustainable infrastructure credits, and [E] end user and [F] year of their establishment, [B] company size, and [C] location of headquarters.

Company Profiles: In-depth profiles of companies that are engaged in this domain, focusing on [A] company overview, [B] financial information (if available), [C] carbon credit portfolio, and [E] recent developments and an informed future outlook.

Case Study: A detailed case study on voluntary carbon offset initiatives by pharma companies in this domain, highlighting the impact of these practices within the pharmaceutical industry.

Market Impact Analysis: An in-depth analysis of the factors that can impact on the growth of the market. It also features identification and market analysis of [A] key drivers, [B] potential restraints, [C] emerging opportunities, and [D] existing challenges.

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What factors are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary Excel Data Packs for all Analytical Modules in the Report

15% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. BACKGROUND

1.1. Context

1.2. Project Objectives

2. RESEARCH METHODOLOGY

2.1. Chapter Overview

2.2. Research Assumptions

2.2.1. Market Landscape and Market Trends

2.2.2. Market Forecast and Opportunity Analysis

2.2.3. Comparative Analysis

2.3. Database Building

2.3.1. Data Collection

2.3.2. Data Validation

2.3.3. Data Analysis

2.4. Project Methodology

2.4.1. Secondary Research

2.4.1.1. Annual Reports

2.4.1.2. Academic Research Papers

2.4.1.3. Company Websites

2.4.1.4. Investor Presentations

2.4.1.5. Regulatory Filings

2.4.1.6. White Papers

2.4.1.7. Industry Publications

2.4.1.8. Conferences and Seminars

2.4.1.9. Government Portals

2.4.1.10. Media and Press Releases

2.4.1.11. Newsletters

2.4.1.12. Industry Databases

2.4.1.13. Roots Proprietary Databases

2.4.1.14. Paid Databases and Sources

2.4.1.15. Social Media Portals

2.4.1.16. Other Secondary Sources

2.4.2. Primary Research

2.4.2.1. Types of Primary Research

2.4.2.1.1. Qualitative Research

2.4.2.1.2. Quantitative Research

2.4.2.1.3. Hybrid Approach

2.4.2.2. Advantages of Primary Research

2.4.2.3. Techniques for Primary Research

2.4.2.3.1. Interviews

2.4.2.3.2. Surveys

2.4.2.3.3. Focus Groups

2.4.2.3.4. Observational Research

2.4.2.3.5. Social Media Interactions

2.4.2.4. Key Opinion Leaders Considered in Primary Research

2.4.2.4.1. Company Executives (CXOs)

2.4.2.4.2. Board of Directors

2.4.2.4.3. Company Presidents and Vice Presidents

2.4.2.4.4. Research and Development Heads

2.4.2.4.5. Technical Experts

2.4.2.4.6. Subject Matter Experts

2.4.2.4.7. Scientists

2.4.2.4.8. Doctors and Other Healthcare Providers

2.4.2.5. Ethics and Integrity

2.4.2.5.1. Research Ethics

2.4.2.5.2. Data Integrity

2.4.3. Analytical Tools and Databases

2.5. Robust Quality Control

3. MARKET DYNAMICS

3.1. Chapter Overview

3.2. Forecast Methodology

3.2.1. Top-down Approach

3.2.2. Bottom-up Approach

3.2.3. Hybrid Approach

3.3. Market Assessment Framework

3.3.1. Total Addressable Market (TAM)

3.3.2. Serviceable Addressable Market (SAM)

3.3.3. Serviceable Obtainable Market (SOM)

3.3.4. Currently Acquired Market (CAM)

3.4. Forecasting Tools and Techniques

3.4.1. Qualitative Forecasting

3.4.2. Correlation

3.4.3. Regression

3.4.4. Extrapolation

3.4.5. Convergence

3.4.6. Sensitivity Analysis

3.4.7. Scenario Planning

3.4.8. Data Visualization

3.4.9. Time Series Analysis

3.4.10. Forecast Error Analysis

3.5. Key Considerations

3.5.1. Demographics

3.5.2. Government Regulations

3.5.3. Reimbursement Scenarios

3.5.4. Market Access

3.5.5. Supply Chain

3.5.6. Industry Consolidation

3.5.7. Pandemic / Unforeseen Disruptions Impact

3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

4.1. Chapter Overview

4.2. Market Dynamics

4.2.1. Time Period

4.2.1.1. Historical Trends

4.2.1.2. Current and Forecasted Estimates

4.2.2. Currency Coverage

4.2.2.1. Major Currencies Affecting the Market

4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

4.2.2.3. Impact of Currency Fluctuations on the Industry

4.2.3. Foreign Currency Exchange Rate

4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

4.2.4. Recession

4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

4.2.5. Inflation

4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

4.2.5.2. Potential Impact of Inflation on the Market Evolution

4.2.6. Interest Rates

4.2.6.1. Interest Rates and Their Impact on the Market

4.2.6.2. Strategies for Managing Interest Rate Risk

4.2.7. Commodity Flow Analysis

4.2.7.1. Type of Commodity

4.2.7.2. Origins and Destinations

4.2.7.3. Values and Weights

4.2.7.4. Modes of Transportation

4.2.8. Global Trade Dynamics

4.2.8.1. Import Scenario

4.2.8.2. Export Scenario

4.2.8.3. Trade Policies

4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

4.2.8.5. Impact of Trade Barriers on the Market

4.2.9. War Impact Analysis

4.2.9.1. Russian-Ukraine War

4.2.9.2. Israel-Hamas War

4.2.10. COVID Impact / Related Factors

4.2.10.1. Global Economic Impact

4.2.10.2. Industry-specific Impact

4.2.10.3. Government Response and Stimulus Measures

4.2.10.4. Future Outlook and Adaptation Strategies

4.2.11. Other Indicators

4.2.11.1. Fiscal Policy

4.2.11.2. Consumer Spending

4.2.11.3. Gross Domestic Product

4.2.11.4. Employment

4.2.11.5. Taxes

4.2.11.6. Stock Market Performance

4.2.11.7. Cross Border Dynamics

4.3. Conclusion

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

6.1. Overview of Carbon Credits

6.2. Carbon Credits Issuers

6.3. Types of Carbon Credits

6.4. Introduction to Voluntary Carbon Market

6.5. Factors Impacting the Pricing of Voluntary Carbon Projects

12.2. Voluntary Carbon Market: Distribution by Project

12.2.1. Voluntary Carbon Market for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

12.2.2. Voluntary Carbon Market for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

12.2.3. Voluntary Carbon Market for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

12.2.4. Voluntary Carbon Market for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

12.2.5. Voluntary Carbon Market for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

12.3. Data Triangulation and Validation

12.3.1. Secondary Sources

12.3.2. Primary Sources

13. Voluntary Carbon MARKET, BY TYPE OF TRANSACTION

13.1. Key Assumptions and Methodology

13.2. Voluntary Carbon Market: Distribution by Type of Transaction

13.2.1. Voluntary Carbon Market for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

13.2.2. Voluntary Carbon Market for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

13.2.3. Voluntary Carbon Market for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

13.3. Data Triangulation and Validation

13.3.1. Secondary Sources

13.3.2. Primary Sources

14. Voluntary Carbon MARKET, BY APPLICATION AREA

14.1. Key Assumptions and Methodology

14.2. Voluntary Carbon Market: Distribution by Application Area

14.2.1. Voluntary Carbon Market for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

14.2.2. Voluntary Carbon Market for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

14.2.3. Voluntary Carbon Market for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

14.2.4. Voluntary Carbon Market for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

14.2.5. Voluntary Carbon Market for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

14.3. Data Triangulation and Validation

14.3.1. Secondary Sources

14.3.2. Primary Sources

15. VOLUNTARY CARBON MARKET, BY END-USER

15.1. Key Assumptions and Methodology

15.2. Voluntary Carbon Market: Distribution by End-user

15.2.1. Voluntary Carbon Market for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

15.2.2. Voluntary Carbon Market for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

15.2.3. Voluntary Carbon Market for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

15.2.4. Voluntary Carbon Market for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

15.3. Data Triangulation and Validation

15.3.1. Secondary Sources

15.3.2. Primary Sources

16. VOLUNTARY CARBON MARKET, BY GEOGRAPHICAL REGION

16.1. Key Assumptions and Methodology

16.2. Voluntary Carbon Market: Distribution by Geographical Regions

16.2.1. Voluntary Carbon Market in North America, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.1.1. Voluntary Carbon Market in the US, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.1.2. Voluntary Carbon Market in Canada, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2. Voluntary Carbon Market in Europe, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.1. Voluntary Carbon Market in Germany, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.2. Voluntary Carbon Market in France, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.3. Voluntary Carbon Market in Italy, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.4. Voluntary Carbon Market in Belgium, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.5. Voluntary Carbon Market in Austria, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.6. Voluntary Carbon Market in Spain, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.7. Voluntary Carbon Market in Netherlands, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.8. Voluntary Carbon Market in the UK, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.2.9. Voluntary Carbon Market in Rest of the Europe, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3. Voluntary Carbon Market in Asia-Pacific, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.1. Voluntary Carbon Market in China, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.2. Voluntary Carbon Market in India, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.3. Voluntary Carbon Market in Japan, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.4. Voluntary Carbon Market in Indonesia, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.5. Voluntary Carbon Market in South Korea, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.6. Voluntary Carbon Market in Australia, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.3.7. Voluntary Carbon Market in Rest of the Asia-Pacific, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.4. Voluntary Carbon Market in Latin America, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.4.1. Voluntary Carbon Market in Argentina, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.4.2. Voluntary Carbon Market in Brazil, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.4.3. Voluntary Carbon Market in Mexico, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.4.4. Voluntary Carbon Market in Rest of Latin America, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5. Voluntary Carbon Market in Middle East and Africa, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.1. Voluntary Carbon Market in Iran, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.2. Voluntary Carbon Market in Saudi Arabia, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.3. Voluntary Carbon Market in UAE, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.4. Voluntary Carbon Market in Israel, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.5. Voluntary Carbon Market in South Africa, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.6. Voluntary Carbon Market in Kuwait, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.7. Voluntary Carbon Market in Oman, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.2.5.8. Voluntary Carbon Market in Rest of the Middle East and Africa, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

16.3 Voluntary Carbon Market, By Geographical Regions: Market Dynamics Assessment

16.3.1. Penetration-Growth (P-G) Matrix

16.3.2. Market Movement Analysis

16.4. Data Triangulation and Validation

16.4.1. Secondary Sources

16.4.2. Primary Sources

SECTION VII: MARKET OPPORTUNITY ANALYSIS WITHIN GEOGRAPHICAL REGIONS**

17. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

17.1. Voluntary Carbon Market in North America: Distribution by Project

17.1.1. Voluntary Carbon Market in North America for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.1.2. Voluntary Carbon Market in North America for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.1.3. Voluntary Carbon Market in North America for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.1.4. Voluntary Carbon Market in North America for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.1.5. Voluntary Carbon Market in North America for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.2. Voluntary Carbon Market in North America: Distribution by Type of Transaction

17.2.1. Voluntary Carbon Market in North America for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.2.2. Voluntary Carbon Market in North America for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.2.3. Voluntary Carbon Market in North America for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.3. Voluntary Carbon Market in North America: Distribution by Application Area

17.3.1. Voluntary Carbon Market in North America for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.3.2. Voluntary Carbon Market in North America for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.3.3. Voluntary Carbon Market in North America for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.3.4. Voluntary Carbon Market in North America for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.3.5. Voluntary Carbon Market in North America for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.4. Voluntary Carbon Market in North America: Distribution by End-user

17.4.1. Voluntary Carbon Market in North America for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.4.2. Voluntary Carbon Market in North America for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.4.3. Voluntary Carbon Market in North America for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

17.4.4. Voluntary Carbon Market in North America for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18. MARKET OPPORTUNITY ANALYSIS: EUROPE

18.1. Voluntary Carbon Market in Europe: Distribution by Project

18.1.1. Voluntary Carbon Market in Europe for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.1.2. Voluntary Carbon Market in Europe for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.1.3. Voluntary Carbon Market in Europe for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.1.4. Voluntary Carbon Market in Europe for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.1.5. Voluntary Carbon Market in Europe for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.2. Voluntary Carbon Market in Europe: Distribution by Type of Transaction

18.2.1. Voluntary Carbon Market in Europe for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.2.2. Voluntary Carbon Market in Europe for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.2.3. Voluntary Carbon Market in Europe for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.3. Voluntary Carbon Market in Europe: Distribution by Application Area

18.3.1. Voluntary Carbon Market in Europe for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.3.2. Voluntary Carbon Market in Europe for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.3.3. Voluntary Carbon Market in Europe for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.3.4. Voluntary Carbon Market in Europe for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.3.5. Voluntary Carbon Market in Europe for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.4. Voluntary Carbon Market in Europe: Distribution by End-user

18.4.1. Voluntary Carbon Market in Europe for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.4.2. Voluntary Carbon Market in Europe for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.4.3. Voluntary Carbon Market in Europe for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

18.4.4. Voluntary Carbon Market in Europe for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19. MARKET OPPORTUNITY ANALYSIS: ASIA-PACIFIC

19.1. Voluntary Carbon Market in Asia-Pacific: Distribution by Project

19.1.1. Voluntary Carbon Market in Asia-Pacific for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.1.2. Voluntary Carbon Market in Asia-Pacific for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.1.3. Voluntary Carbon Market in Asia-Pacific for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.1.4. Voluntary Carbon Market in Asia-Pacific for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.1.5. Voluntary Carbon Market in Asia-Pacific for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.2. Voluntary Carbon Market in Asia-Pacific: Distribution by Type of Transaction

19.2.1. Voluntary Carbon Market in Asia-Pacific for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.2.2. Voluntary Carbon Market in Asia-Pacific for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.2.3. Voluntary Carbon Market in Asia-Pacific for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.3. Voluntary Carbon Market in Asia-Pacific: Distribution by Application Area

19.3.1. Voluntary Carbon Market in Asia-Pacific for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.3.2. Voluntary Carbon Market in Asia-Pacific for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.3.3. Voluntary Carbon Market in Asia-Pacific for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.3.4. Voluntary Carbon Market in Asia-Pacific for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.3.5. Voluntary Carbon Market in Asia-Pacific for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.4. Voluntary Carbon Market in Asia-Pacific: Distribution by End-user

19.4.1. Voluntary Carbon Market in Asia-Pacific for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.4.2. Voluntary Carbon Market in Asia-Pacific for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.4.3. Voluntary Carbon Market in Asia-Pacific for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

19.4.4. Voluntary Carbon Market in Asia-Pacific for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20. MARKET OPPORTUNITY ANALYSIS: LATIN AMERICA

20.1. Voluntary Carbon Market in Latin America: Distribution by Project

20.1.1. Voluntary Carbon Market in Latin America for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.1.2. Voluntary Carbon Market in Latin America for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.1.3. Voluntary Carbon Market in Latin America for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.1.4. Voluntary Carbon Market in Latin America for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.1.5. Voluntary Carbon Market in Latin America for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.2. Voluntary Carbon Market in Latin America: Distribution by Type of Transaction

20.2.1. Voluntary Carbon Market in Latin America for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.2.2. Voluntary Carbon Market in Latin America for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.2.3. Voluntary Carbon Market in Latin America for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.3. Voluntary Carbon Market in Latin America: Distribution by Application Area

20.3.1. Voluntary Carbon Market in Latin America for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.3.2. Voluntary Carbon Market in Latin America for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.3.3. Voluntary Carbon Market in Latin America for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.3.4. Voluntary Carbon Market in Latin America for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.3.5. Voluntary Carbon Market in Latin America for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.4. Voluntary Carbon Market in Latin America: Distribution by End-user

20.4.1. Voluntary Carbon Market in Latin America for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.4.2. Voluntary Carbon Market in Latin America for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.4.3. Voluntary Carbon Market in Latin America for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

20.4.4. Voluntary Carbon Market in Latin America for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21. MARKET OPPORTUNITY ANALYSIS: MIDDLE EAST AND AFRICA

21.1. Voluntary Carbon Market in Middle East and Africa: Distribution by Project

21.1.1. Voluntary Carbon Market in Middle East and Africa for Renewable Energy Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.1.2. Voluntary Carbon Market in Middle East and Africa for Energy Efficiency Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.1.3. Voluntary Carbon Market in Middle East and Africa for Forestry and Land Use Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.1.4. Voluntary Carbon Market in Middle East and Africa for Methane Capture and Destruction Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.1.5. Voluntary Carbon Market in Middle East and Africa for Other Projects, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.2. Voluntary Carbon Market in Middle East and Africa: Distribution by Type of Transaction

21.2.1. Voluntary Carbon Market in Middle East and Africa for Carbon Removal, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.2.2. Voluntary Carbon Market in Middle East and Africa for Carbon Reduction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.2.3. Voluntary Carbon Market in Middle East and Africa for Mixed Transaction, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.3. Voluntary Carbon Market in Middle East and Africa: Distribution by Application Area

21.3.1. Voluntary Carbon Market in Middle East and Africa for Industrial Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.3.2. Voluntary Carbon Market in Middle East and Africa for Household Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.3.3. Voluntary Carbon Market in Middle East and Africa for Energy Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.3.4. Voluntary Carbon Market in Middle East and Africa for Agriculture Sector, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.3.5. Voluntary Carbon Market in Middle East and Africa for Other Application Area, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.4. Voluntary Carbon Market in Middle East and Africa: Distribution by End-user

21.4.1. Voluntary Carbon Market in Middle East and Africa for Government Agencies / Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.4.2. Voluntary Carbon Market in Middle East and Africa for Non-Profit Organizations, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.4.3. Voluntary Carbon Market in Middle East and Africa for Private Companies, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

21.4.4. Voluntary Carbon Market in Middle East and Africa for Individuals, Historical Trends (Since 2020) and Forecasted Estimates (Till 2035)

*Detailed information on Section VII is available in the Excel Data Packs shared along with the report