오토인젝터 시장 : 사용법별, 투여 경로별, 전달 분자 유형별, 작용기전 유형별, 용기 용량별, 최종 사용자별, 표적 적응증별, 주요 지역별

Global Autoinjectors Market by Usability, Route of Administration, Type of Molecule Delivered, Type of Actuation Mechanism, Volume of Container, End-user, Target Indication and Key Geographical Regions

상품코드:1737048

리서치사:Roots Analysis

발행일:2025년 05월

페이지 정보:영문 593 Pages

라이선스 & 가격 (부가세 별도)

한글목차

세계의 오토인젝터 시장 규모는 2035년까지 예측 기간 동안 6.2%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상되며, 906억 달러에서 2035년까지 1,759억 달러로 성장할 것으로 예측됩니다.

시장 세분화 및 기회 분석은 다음 매개변수로 세분화됩니다.

사용법별

일회용

재사용형

투여 경로별

피하

정맥 내

근육 내

전달 분자 유형별

항체

펩티드

단백질

저분자

기타

작용기전 유형별

수동

자동

용기 용량별

1mL 미만

1-2 mL

2mL 이상

최종 사용자별

외래수술센터(ASC)

재택치료

병원 및 진료소

표적 적응증별

아나필락시

당뇨병

편두통

다발성 경화증

류마티스 관절

체중 감소

기타

주요 지역별

북미

유럽

아시아태평양

중동 및 북아프리카

라틴아메리카

세계의 오토인젝터 시장(5판) : 성장과 동향

당뇨병, 다발성 경화증, 류마티스 관절염, 심각한 알레르기와 같은 만성 질환의 세계적인 증가로 더욱 효율적이고 혁신적이고 사용자 친화적인 약물 전달 시스템이 시급해지고 있습니다. 이러한 만성 질환이 환자에게 미치는 영향은 상당한 것으로, 관련 비용과 합병증이 장기간에 걸쳐 극적으로 에스컬레이션될 수 있음은 주목할 만합니다. 그 결과 의료 산업은 오토인젝터를 포함한 새로운 약물 전달 장치를 개발하는 데 많은 노력을 기울였습니다.

오토인젝터는 피하 또는 근육 내 경로에서 약물전달에 사용되는 자동 주사기입니다. 이들은 주로 프리필드 주사기와 카트리지를 주 용기로 사용하는 스프링 구동 장치입니다. 약물전달 과정을 완전히 또는 부분적으로 자동화함으로써 이러한 장치는 투여 과정을 더욱 편리하게 만듭니다. 따라서 오토인젝터는 안전하고 신뢰할 수 있는 주사제를 전달할 수 있는 환자 중심의 차세대 장비로서 큰 잠재력을 보여줍니다. 또한, 새로운 생물 제제의 출현으로 점성이 높은 약물을 대량으로 주사하는 수요가 증가하고 있습니다. 그 결과, BD 메디컬이나 SHL 등 많은 기기 제조업체가 대용량의 오토인젝터를 도입하고 있습니다. 또한, 현재 개발중인 새로운 오토인젝터는 개별 환자의 특정 요구와 요구에 대응할 수 있습니다. 이들은 사용자의 요구에 따라 용량과 장비의 기능을 조정할 수 있도록 설계되었습니다. 사실, 주사기를 다양한 제품과 플랫폼에 디지털로 연결함으로써 환자의 복약 충고와 삶의 질을 향상시킬 것으로 기대됩니다. 오토인젝터의 이러한 진보를 바탕으로, 효과적인 약물 전달 시스템과 질병 관리에 대한 요구 증가에 미래에 효율적으로 대처할 수 있습니다.

세계 오토인젝터 시장 : 주요 인사이트력

이 보고서는 세계 오토인젝터 시장의 현재 상태를 파악하고 업계 내 잠재적 성장 기회를 확인합니다. 주요 조사 결과는 다음과 같습니다.

현재, 약 150개 오토인젝터가 세계 각종 진출기업에 의해 이용가능/제조되고 있습니다.

시판되는 대부분의 오토인젝터는 피하 투여에 적합합니다. 이 오토인젝터는 가청 및 시각 표시기와 통합되어 무수한 분자를 전달할 가능성이 있습니다.

또한 대륙간 및 대륙 내 파트너십의 대부분은 유럽에 본사를 둔 진출기업에 의해 체결되었습니다.

2019년 이후, 오토인젝터와 관련된 1,100건 이상의 특허가 이 영역 내에서 생성된 지적재산을 보호하기 위해 다양한 이해관계자에 의해 출원되었으며, 다양한 이해관계자에게 부여되었습니다.

학술/의료/상업 조직에 속한 여러 과학자, 임상의, 업계의 베테랑이 오토인젝터와 관련된 연구의 선두에 서 있습니다.

또한 오토인젝터 배합제 개발기업의 약 60%가 초대형 기업입니다.

시판되는 오토인젝터 제형의 약 75%는 주사기와 호환되며, 특히 이러한 제형의 대부분은 성인의 가정용 의료용으로 사용하기 위한 것입니다.

다양한 적응증 치료를 목적으로 하는 70개 이상의 오토인젝터 제제가 현재 개발의 초기 단계와 후기 단계에서 평가되고 있습니다.

초기 및 후기 단계의 제형의 약 90%는 현재 다양한 임상 단계의 개발 단계에 있으며, 이들 대부분은 만성 질환(주로 류마티스 관절염)의 치료를 위해 개발되고 있습니다.

오토인젝터 시장은 안정적인 속도로 성장할 것으로 예측됩니다.

자동 작용기전을 가진 오토인젝터는 2035년까지 더 빠른 페이스(-7%)로 성장할 것으로 예측되고 있습니다.

재택치료에 적합한 오토인젝터는 예측 기간 동안 시장 대부분의 점유율을 획득할 것으로 보입니다.

세계의 오토인젝터 시장(5판) : 주요 부문

사용법별로는 시장은 일회용 오토인젝터와 재이용형 오토인젝터로 구분됩니다.

정맥 내 약물 전달용 오토인젝터는 예측 기간 동안 세계의 자동 주입 시장에서 가장 빠르게 성장하는 부문입니다.

투여 경로별로, 시장은 피하, 근육내, 정맥내로 구분됩니다. 현재, 피하 약물전달에 사용되는 오토인젝터가 세계의 오토인젝터 시장에서 가장 높은 비율을 차지하고 있습니다.

전달 분자 유형별로 시장은 항체, 펩티드, 단백질, 저분자 등으로 구분됩니다.

작용기전 유형별로는 시장은 수동작용기전과 자동작용기전 기반의 오토인젝터로 구분됩니다.

용기의 용량별로는 시장은 보존 용량이 1mL 미만, 1-2mL, 2mL 이상의 오토인젝터로 구분됩니다.

최종 사용자별로 보면 시장은 재택치료, 병원 및 진료소, 외래수술센터(ASC)로 구분됩니다.

표적 적응증별로는 시장은 아나필락시스, 당뇨병, 편두통, 다발성 경화증, 관절염 류마티스, 체중감소, 기타 적응증으로 구분됩니다.

주요 지역별로 볼 때 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동, 북아프리카로 구분됩니다.

오토 인젝터 세계 시장에서의 진출기업 예

Amgen

Antares Pharma

ChemProtect.SK

Elcam Medical

Eli Lilly and Company

Jiangsu Delfu Medical Device

Kindeva Drug Delivery

Merck

Novartis

Novo Nordisk

Oval Medical Technologies

Owen Mumford

PreciHealth

Recipharm

Sanofi

SHL Medical

Teva Pharmaceuticals

Union Medico

Ypsomed

본 보고서에서는 세계의 오토인젝터 시장에 대해 조사했으며, 시장 개요와 함께 사용법별, 투여경로별, 전달분자 유형별, 작용기전 유형별, 용기 용량별, 최종사용자별, 표적적응증별, 주요 지역별 동향 및 시장 진출기업 프로파일 등의 정보를 제공합니다.

목차

제1장 서문

제2장 조사 방법

제3장 경제적 및 기타 프로젝트 특유의 고려 사항

제4장 주요 요약

제5장 소개

장의 개요

약물전달 시스템의 유형

종래의 비경구 투여 시스템의 단점

자기 관리의 새로운 조류

자기 투여 장치의 유형

오토인젝터의 개요

규제 고려 사항

장래의 전망

제6장 오토인젝터에 사용되는 주요 약제 용기

장의 개요

포장의 유형

주요 의약품 용기

1차 의약품 용기의 역할

카트리지

주사기

바이알

다양한 제조 재료의 비교

제7장 오토인젝터 : 시장 개요

장의 개요

오토인젝터: 시장 상황

오토인젝터 제조업체 : 시장 상황

제8장 제품 경쟁력 분석

장의 개요

전제 및 주요 파라미터

조사 방법

오토인젝터 : 제품 경쟁력 분석

일회용 오토인젝터

재사용형 오토인젝터

제9장 브랜드 포지셔닝 분석

장의 개요

전제 및 주요 파라미터

조사 방법

오토인젝터 제조업체 : 브랜드 포지셔닝 프레임워크

브랜드 포지셔닝 프레임워크: Owen Mumford

브랜드 포지셔닝 프레임워크: Ypsomed

브랜드 포지셔닝 프레임워크: Elcam Medical

브랜드 포지셔닝 프레임워크: SHL Medical

브랜드 포지셔닝 프레임워크: Union Medico

브랜드 포지셔닝 프레임워크: Antares Pharma

브랜드 포지셔닝 프레임워크: PreciHealth

브랜드 포지셔닝 프레임워크: Jiangsu Delfu Medical Device

브랜드 포지셔닝 프레임워크: Oval Medical Technologies

브랜드 포지셔닝 프레임워크: Recipharm

제10장 오토인젝터 제조업체 : 상세한 기업 프로파일

장의 개요

Antares Pharma

Elcam Medical

Jiangsu Delfu Medical Device

Oval Medical Technologies

Owen Mumford

PreciHealth

Recipharm

SHL Medical

Union Medico

Ypsomed

제11장 파트너십 및 협업

장의 개요

파트너십 모델

오토인젝터 : 파트너십과 콜라보레이션

제12장 특허 분석

장의 개요

범위와 조사 방법

오토인젝터 : 특허 분석

특허 벤치마킹 분석

특허평가

인용수 상위의 특허

제13장 약제 및 디바이스 조합 : 상시가 끝난 오토인젝터

장의 개요

약제 및 디바이스의 조합 : 상시가 끝난 오토 인젝터

약제 및 장치의 조합 : 상시가 끝난 오토인젝터 개발자

제14장 약물과 장치의 조합 : 초기 및 후기 단계의 오토인젝터

장의 개요

약물 및 장치 조합: 초기 및 후기 단계의 오토인젝터

의약품 장치 조합: 초기 및 후기 단계의 오토인젝터 개발자의 상황

제15장 기업 프로파일 : 오토인젝터 복합제품 개발 기업

장의 개요

Amgen

ChemProtect.SK

Eli Lilly and Company

Kindeva Drug Delivery

Merck

Novartis

Novo Nordisk

Sanofi

Teva Pharmaceutical Industries

제16장 KOL 분석

제17장 사례 연구: 주요 치료 적응

장의 개요

아나필락시

다발성 경화증

편두통

류마티스 관절

제18장 사례 연구: 의료기기 계약 서비스 제공업체

장의 개요

의료기기 제조에 따른 과제

의료기기 제조에 있어서의 CMO의 역할

의료기기 CMO가 제공하는 서비스

의료기기 CMO가 제공하는 이점

CMO에 아웃소싱에 따른 위험

약물전달 디바이스 서비스 제공업체

결론

제19장 사례 연구: 프리필드 주사기

장 개요

프리필드 주사기: 시장 상황

프리필드 주사기 제조업체 : 시장 상황

장래의 전망

제20장 SWOT 분석

제21장 세계의 오토인젝터 시장

장의 개요

주요 전제와 조사 방법

세계의 오토인젝터 시장, 과거 동향(2018년 이후) 및 예측(2035년까지)

시나리오 분석

주요 시장 세분화

제22장 관절 류마티스용 오토인젝터 시장

제23장 다발성 경화증용 오토인젝터 시장

제24장 당뇨병용 오토인젝터 시장

제25장 체중 감량용 오토인젝터 시장

제26장 아나필락시스용 오토인젝터 시장

제27장 편두통 치료용 오토인젝터 시장

제28장 기타 적응증용 오토인젝터 시장

제29장 오토인젝터 시장, 사용법별

제30장 오토인젝터 시장, 투여 경로별

제31장 오토인젝터 시장, 전달 분자 유형별

제32장 오토인젝터 시장, 작용기전 유형별

제33장 오토인젝터 시장, 용기의 용량별

제34장 오토인젝터 시장, 최종 사용자별

제35장 오토인젝터 시장, 표적 적응증별

제36장 오토인젝터 시장, 주요 지역별

제37장 결론

제38장 주요 인사이트

제39장 부록 1:표 형식 데이터

제40장 부록 2: 기업 및 조직 목록

SHW

영문 목차

영문목차

GLOBAL AUTOINJECTORS MARKET (5TH EDITION): OVERVIEW

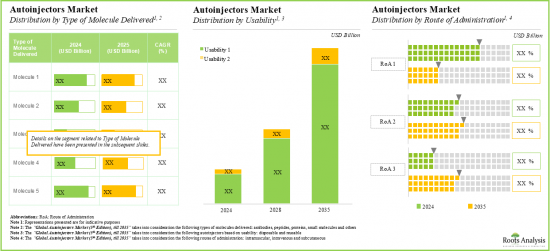

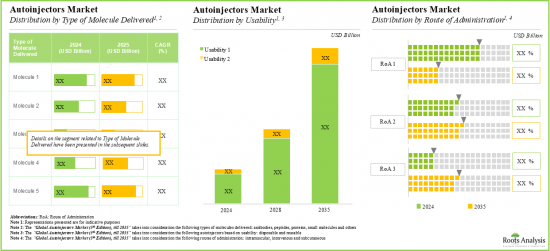

As per Roots Analysis, the global autoinjectors market is estimated to grow from USD 90.6 billion in the current year to USD 175.9 billion by 2035, at a CAGR of 6.2% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Usability

Disposable

Reusable

Route of Administration

Subcutaneous

Intravenous

Intramuscular

Type of Molecule Delivered

Antibodies

Peptides

Proteins

Small Molecules

Others

Type of Actuation Mechanism

Manual

Automatic

Volume of Container

Less than 1 mL

1-2 mL

More than 2 mL

End-user

Ambulatory Surgical Centers

Home Care

Hospitals and Clinics

Target Indication

Anaphylaxis

Diabetes

Migraine

Multiple Sclerosis

Rheumatoid Arthritis

Weight Loss

Others

Key Geographical Regions

North America

Europe

Asia-Pacific

Middle East and North Africa

Latin America

GLOBAL AUTOINJECTORS MARKET (5TH EDITION): GROWTH AND TRENDS

The global rise in chronic diseases, such as diabetes, multiple sclerosis, rheumatoid arthritis and severe allergies, has driven a pressing requirement for a more efficient, innovative and user-friendly drug delivery systems. It is worth highlighting that the impact of these chronic conditions on patients is substantial, as the associated costs and complications can escalate dramatically over a period. As a result, the medical industry has made significant efforts in developing novel drug delivery devices, including autoinjectors.

Autoinjectors are automatic injection devices that are used for the delivery of drugs through the subcutaneous or intramuscular routes. These are primarily spring-driven devices that use prefilled syringes or cartridges as primary containers. By complete or partial automation of the drug delivery process, these devices make the dosing process more convenient. Owing to which, autoinjectors have demonstrated significant potential as the next generation of patient-centric devices, capable of safe and reliable delivery of injectables. Further, the advent of novel biologics is driving the demand for injection of higher viscosities of drugs in larger volumes. Consequently, many device manufacturers, such as BD Medical and SHL, have introduced large volume autoinjectors. Additionally, the new autoinjector devices, which are currently under development, are capable of addressing the specific needs and wants of individual patients. These are designed to enable adjustments in the dosage or features of the device based upon the requirements of the user. In fact, connecting the injectors digitally to various products and platforms is expected to improve adherence and quality of life for the patients. Given these advancements in autoinjectors, the growing need for effective drug delivery systems and disease management can be efficiently addressed in the future.

GLOBAL AUTOINJECTORS MARKET: KEY INSIGHTS

The report delves into the current state of the global autoinjectors market and identifies potential growth opportunities within the industry. Some key findings from the report include:

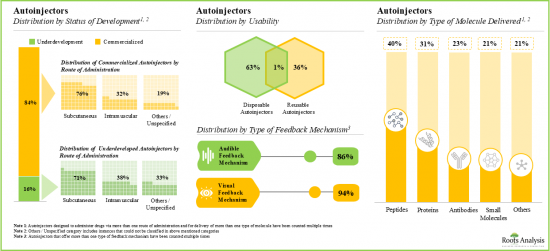

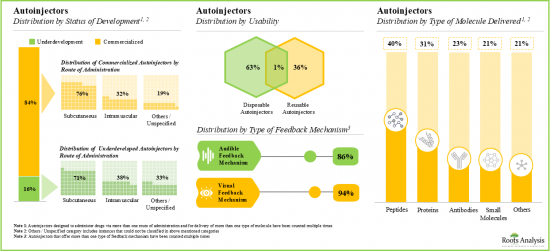

1. Presently, close to 150 autoinjectors are available / being manufactured by various players, globally; the majority of the autoinjector manufacturers are headquartered in North America.

2. Most of the commercially available autoinjectors are suitable for subcutaneous administration; these autoinjectors are integrated with audible and visual indicators and can deliver a myriad of molecules.

3. More than 50% of the deals in the autoinjectors domain were inked in the last three years; further, most of the intercontinental as well as intracontinental partnerships have been signed by players based in Europe.

4. Since 2019, more than 1,100 patents related to autoinjectors have been filed by / granted to various stakeholders to protect the intellectual property generated within this domain.

5. Several scientists, clinicians and industry veterans, affiliated to academic / medical / commercial organizations, are spearheading research related to autoinjectors.

6. Nearly 160 autoinjector combination products (with different drugs) have been approved by regulatory authorities, across the world; further, close to 60% of autoinjector combination product developers are very large players.

7. Around 75% of the commercialized autoinjector combination products are compatible with syringes; notably, majority of these combination products are intended to be used in homecare settings by adults.

8. More than 70 autoinjector combination products intended for the treatment of various indications are currently being evaluated in early and late stages of development; further, most of the developers for these products are publicly listed companies.

9. Around 90% of the early and late-stage combination products are currently in different clinical phases of development; majority of these are being developed for the treatment of chronic conditions (primarily rheumatoid arthritis).

10. The autoinjectors market is anticipated to grow at a steady rate; notably, disposable autoinjectors are likely to capture over 88% market share in 2024 as they eliminate the need for manual loading of medication and have lower risk of contamination.

11. Autoinjectors with automatic actuation mechanism are anticipated to grow at faster pace (~7%) till 2035; further, the autoinjectors intended for delivering drugs targeting rheumatoid arthritis are likely to dominate the current market.

12. The autoinjectors suitable for home care are likely to capture majority share in the market during the forecasted period; Asia-Pacific is anticipated to grow at higher rate in this domain, till 2035.

GLOBAL AUTOINJECTORS MARKET (5TH EDITION): KEY SEGMENTS

Disposable Autoinjectors Occupies the Largest Share of the Global Autoinjectors Market

Based on the usability, the market is segmented into disposable autoinjectors and reusable autoinjectors. At present, disposable autoinjectors segment hold the maximum share of the global autoinjectors market. This trend is likely to remain the same in the forthcoming years.

Autoinjectors for Intravenous Drug Delivery is the Fastest Growing Segment of the Global Autoinjectors Market During the Forecast Period

Based on the route of administration, the market is segmented into subcutaneous, intramuscular and intravenous routes. Currently, autoinjectors used for subcutaneous drug delivery capture the highest proportion of the global autoinjectors market. It is worth highlighting that the global autoinjector market for intravenous autoinjector segment is likely to grow at a relatively higher CAGR.

Proteins Segment Occupy the Largest Share of the Global Autoinjectors Market by Type of Molecule Delivered

Based on the type of molecule delivered, the market is segmented into antibodies, peptides, proteins, small molecules and others. At present, autoinjectors designed for the delivery of proteins hold the maximum share of the global autoinjectors market. This trend is likely to change in the foreseeable future.

By Type of Actuation Mechanism, Autoinjectors with Automatic Actuation Mechanism is the Fastest Growing Segment of the Global Autoinjectors Market During the Forecast Period

Based on the type of actuation mechanism, the market is segmented into manual and automatic actuation mechanism based autoinjectors. At present, autoinjectors equipped with automatic actuation mechanisms capture the highest proportion of the global autoinjectors market. Further, it is worth highlighting that the global autoinjector market for automatic actuation mechanism based autoinjectors is likely to grow at a relatively higher CAGR.

Autoinjectors with Volume Containers of 1-2 mL Account for the Largest Share of the Global Autoinjectors Market

Based on the volume of containers, the market is segmented into autoinjectors with less than 1 ml, 1-2 ml and more than 2 ml storing volumes. Currently, autoinjectors with a drug storing capacity of 1-2 ml of a drug hold the maximum share of the global autoinjectors market. This trend is likely to remain the same in the coming decade.

By End-user, Home Care Segment is Likely to Dominate the Global Autoinjectors Market

Based on the end-user, the market is segmented into home care, hospitals and clinics and ambulatory surgical centers. At present autoinjectors used in the home care segment hold the maximum share of the global autoinjectors market. Additionally, this segment is likely to grow at a faster pace, compared to the other segments.

Autoinjectors Designed for the Treatment of Rheumatoid Arthritis Occupy the Largest Share of the Global Autoinjectors Market

Based on the target indication, the market is segmented into anaphylaxis, diabetes, migraine, multiple sclerosis, rheumatoid arthritis, weight loss and other indications. Whilst rheumatoid arthritis target indication segment is expected to be the primary driver of the overall market, it is worth highlighting that the global autoinjectors market for weight loss segment is likely to grow at a relatively higher CAGR.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East and North Africa. The majority share is expected to be captured by players based in North America and Europe.

Example Players in the Global Autoinjectors Market

Amgen

Antares Pharma

ChemProtect.SK

Elcam Medical

Eli Lilly and Company

Jiangsu Delfu Medical Device

Kindeva Drug Delivery

Merck

Novartis

Novo Nordisk

Oval Medical Technologies

Owen Mumford

PreciHealth

Recipharm

Sanofi

SHL Medical

Teva Pharmaceuticals

Union Medico

Ypsomed

GLOBAL AUTOINJECTORS MARKET: RESEARCH COVERAGE

Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global autoinjectors market, focusing on key market segments, including [A] usability, [B] route of administration, [C] type of molecule delivered, [D] type of actuation mechanism, [E] volume of container, [F] end-user, [G] target indication and [H] key geographical regions.

Autoinjectors Market Landscape: A comprehensive evaluation of autoinjectors, considering various parameters, such as [A] status of development, [B] usability, [C] type of primary drug container, [D] requirement of needle, [E] volume of container, [F] type of dose delivered, [G] route of administration, [H] type of actuation mechanism, [I] type of feedback mechanism, [J] availability of connectivity feature, [K] target indication, [L] type of molecule delivered and [M] end-user. Additionally, a comprehensive evaluation of the companies engaged in manufacturing autoinjectors, based on several relevant parameters, such as [N] year of establishment, [O] company size (in terms of employee count), [P] location of headquarters, [Q] type of company and [R] most active players (in terms of number of autoinjectors manufactured).

Product Competitiveness Analysis: A comprehensive competitive analysis of autoinjectors, examining factors, such as [A] manufacturer strength and [B] product strength.

Brand Positioning Analysis: A comprehensive brand positioning assessment framework of the autoinjector manufacturers focusing on the current perceptions of their proprietary brands across various device types. This analysis evaluates autoinjector manufacturers by various parameters, including [A] strength and diversity of product portfolio, [B] routes of administration, [C] type of actuation mechanism, [D] type of feedback mechanism, [E] geographical presence / reach and [F] supplier strength of each player.

Company Profiles of Autoinjectors Manufacturers: In-depth profiles of key autoinjector manufacturers, focusing on [A] company overviews, [B] financial information (if available), [C] autoinjectors portfolio, [D] manufacturing capabilities and facilities, [E] recent developments and [F] an informed future outlook.

Partnerships and Collaborations: An insightful analysis of the deals inked by stakeholders in the global autoinjectors market, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D] most active players (in terms of the number of partnerships signed) and [E] geographical distribution of partnership activity.

Patent Analysis: An in-depth analysis of patents filed / granted till date in the autoinjectors domain, based on various relevant parameters, such as [A] type of patent, [B] patent publication year, [C] patent application year, [D] patent jurisdiction, [E] CPC symbols, [F] type of applicant, [G] most active players, [H] patent benchmarking and [I] patent valuation analysis.

Commercialized Autoinjector Combination Product Market Landscape: A comprehensive evaluation of commercialized autoinjector combination products, considering various parameters, such as [A] approval year, [B] usability, [C] type of primary drug container, [D] requirement of needle, [E] volume of container, [F] injection time, [G] type of dose delivered, [H] route of administration, [I] type of actuation mechanism, [J] type of feedback mechanism, [K] availability of connectivity feature, [L] target indication, [M] severity of indication, [N] type of molecule delivered, [O] end-user and [P] target population. Additionally, a comprehensive evaluation of the companies engaged in manufacturing commercialized autoinjector combination product, based on several relevant parameters, such as [Q] year of establishment, [R] company size (in terms of employee count), [S] location of headquarters, [T] type of company and [U] most active players (in terms of number of commercialized autoinjector combination products developed).

Early and Late Stage Autoinjectors Combination Product Market Landscape: A comprehensive evaluation of early and late stage autoinjector combination products, considering various parameters, such as [A] stage of development, [B] route of administration, [C] dose strength, [D] target indication, [E] severity of indication, [F] type of molecule delivered, [G] end-user, [H] target population and [I] gender of target population. Additionally, a comprehensive evaluation of the companies engaged in manufacturing early and late stage autoinjector combination products, based on several relevant parameters, such as [J] year of establishment, [K] company size (in terms of employee count), [L] location of headquarters and [M] type of company.

Short Company Profiles of Autoinjector Combination Product Manufacturers: Short profiles of key autoinjector combination product manufacturers, focusing on [A] company overviews and [B] autoinjector product portfolio.

Key Opinion Leaders (KOLs]: An in-depth analysis that emphasizes the key opinion leaders in this domain, considering various parameters, such as [A] role of KOL, [B] type of sponsor organization, [C] affiliated organization, [D] target indication, [E] location of clinical trials and [F] most prominent KOLs.

Case Study 1: A general discussion on most commonly targeted indications, providing information on approved autoinjector combination products.

Case Study 2: A general discussion on the role of medical device CMOs in the manufacturing and assembly of drug-delivery devices, including autoinjectors, based on several relevant parameters, such as [A] scale of operation and [B] types of services provided for production of devices.

Case Study 3: A detailed assessment of prefilled syringes that are either commercialized or under development based on several relevant parameters, such as [A] type of barrel fabrication material, [B] number of barrel chambers, [C] type of needle system. In addition, the chapter provides a detailed analysis of prefilled syringe manufacturers, based on various parameters, such as [D] year of establishment, [E] company size (in terms of employee count) and [F] location of headquarters.

SWOT Analysis: An analysis of industry affiliated trends, opportunities and challenges, which are likely to impact the evolution of autoinjectors market; it includes a Harvey ball analysis, assessing the relative impact of each SWOT parameter on industry dynamics.

KEY QUESTIONS ANSWERED IN THIS REPORT

How many companies are currently engaged in this market?

Which are the leading companies in this market?

What factors are likely to influence the evolution of this market?

What is the current and future market size?

What is the CAGR of this market?

How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

Complimentary PPT Insights Packs

Complimentary Excel Data Packs for all Analytical Modules in the Report

10% Free Content Customization

Detailed Report Walkthrough Session with Research Team

Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

1.1. Introduction

1.2. Market Share Insights

1.3. Key Marget Insights

1.4. Report Coverage

1.5. Key Questions Answered

1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

2.1. Chapter Overview

2.2. Research Assumptions

2.3. Project Methodology

2.4. Forecast Methodology

2.5. Robust Quality Control

2.6. Key Market Segmentation

2.7. Key Considerations

2.7.1. Demographics

2.7.2. Economic Factors

2.7.3. Government Regulations

2.7.4. Supply Chain

2.7.5. COVID Impact

2.7.6. Market Access

2.7.7. Healthcare Policies

2.7.8. Industry Consolidation

3.ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

3.1. Chapter Overview

3.2. Market Dynamics

3.2.1. Time Period

3.2.1.1. Historical Trends

3.2.1.2. Current and Future Estimates

3.2.2. Currency Coverage and Foreign Exchange Rate

3.2.2.1. Major Currencies Affecting the Market

3.2.2.2. Factors Affecting Currency Fluctuations and Foreign Exchange Rates

3.2.2.3. Impact of Foreign Exchange Rate Volatility on the Market

3.2.2.4. Strategies for Mitigating Foreign Exchange Risk

3.2.3. Trade Policies

3.2.3.1. Impact of Trade Barriers on the Market

3.2.3.2. Strategies for Mitigating the Risks Associated with Trade Barriers

3.2.4. Recession

3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

3.2.5. Inflation

3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

3.2.5.2. Potential Impact of Inflation on the Market Evolution

4. EXECUTIVE SUMMARY

5. INTRODUCTION

5.1. Chapter Overview

5.2. Types of Drug Delivery Systems

5.3. Drawbacks of Conventional Parenteral Delivery Systems

5.4. Emerging Trend of Self-Administration

5.4.1. Rising Burden of Chronic Diseases

5.4.2. Healthcare Cost Savings

5.4.3. Need for Immediate Treatment in Emergency Situations

5.4.4. Growth of Injectable Biologics Market

5.4.5. Addressing Key User Safety Requirements

5.5. Types of Self-Administration Devices

5.5.1. Prefilled Syringes

5.5.2. Pen-Injectors

5.5.3. Needle-Free Injectors

5.5.4. Large Volume Wearable Injectors

5.5.5. Autoinjectors

5.6. Overview of Autoinjectors

5.6.1. Components of Autoinjectors

5.6.2. Classification of Autoinjectors

5.6.2.1. Classification Based on Mechanism of Action

5.6.2.2. Classification Based on Usability

5.6.2.3. Classification Based on Type of Dose Delivered

5.6.3. Manufacturing / Packaging of Autoinjectors

5.6.4. Benefits of Autoinjectors

5.7. Regulatory Considerations

5.7.1. Medical Devices

5.7.2. Drug Device Combination Products

5.8. Future Perspectives

6. PRIMARY DRUG CONTAINERS USED IN AUTOINJECTORS

6.1. Chapter Overview

6.2. Types of Packaging

6.3. Primary Drug Containers

6.3.1. Role of Primary Drug Containers

6.3.2. Cartridges

6.3.2.1. Components of Cartridges

6.3.2.2. Types of Cartridges

6.3.2.2.1. Single Chamber Cartridge

6.3.2.2.2. Dual Chamber Cartridge

6.3.2.3. Commercially Available Cartridges

6.3.3. Syringes

6.3.3.1. Components of Syringes

6.3.3.2. Classification of Syringes

6.3.3.2.1. Classification Based on Barrel Fabrication Material

6.3.3.2.2. Classification Based on Number of Chambers in the Barrel

6.3.3.2.3. Classification Based on Type of Needle

6.3.4. Vials

6.3.4.1. Components of Vials

6.3.4.2. Commercially Available Vials

6.4. Comparison of Different Fabrication Materials

7. AUTOINJECTORS: MARKET OVERVIEW

7.1. Chapter Overview

7.2. Autoinjectors: Overall Market Landscape

7.2.1. Analysis by Stage of Development

7.2.2. Analysis by Usability

7.2.3. Analysis by Type of Primary Drug Container

7.2.4. Analysis by Requirement of Needle

7.2.5. Analysis by Volume of Container

7.2.6. Analysis by Type of Dose Delivered

7.2.7. Analysis by Route of Administration

7.2.8. Analysis by Type of Actuation Mechanism

7.2.9. Analysis by Type of Feedback Mechanism

7.2.10. Analysis by Availability of Connectivity Feature