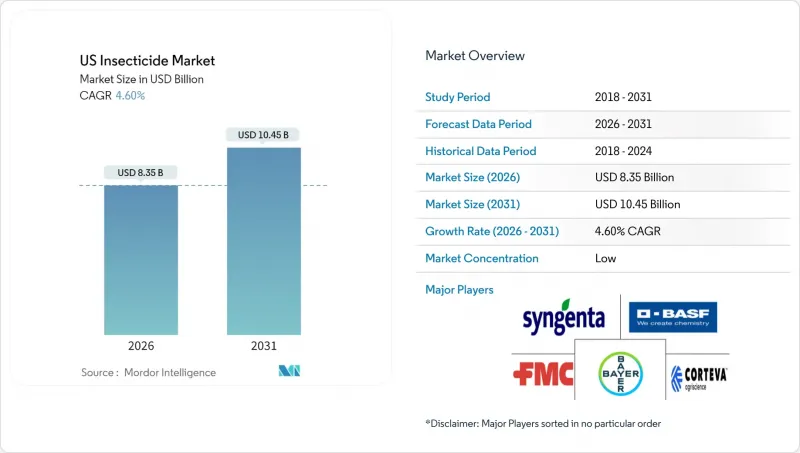

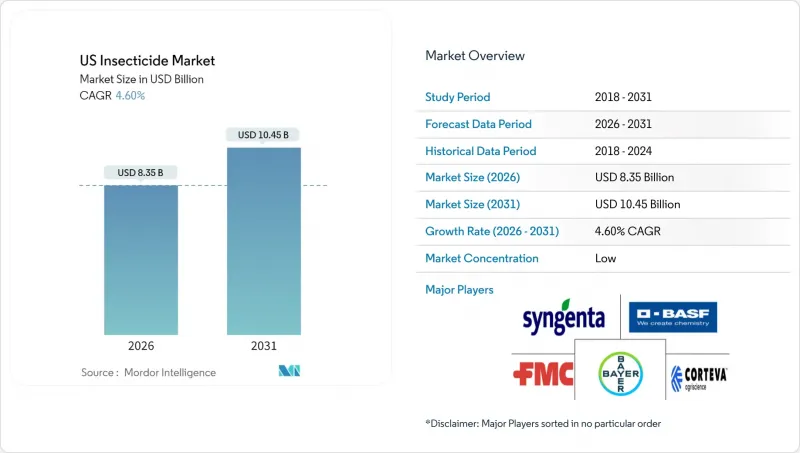

미국의 살충제 시장은 2025년에 79억 8,000만 달러로 평가되었고, 2026년 83억 5,000만 달러에서 2031년까지 104억 5,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.60%로 예상됩니다.

규제 감시가 강화되는 가운데 특수작물 재배면적 확대, 정밀농업의 보급 확대, 지속적인 저항성 문제가 수요를 뒷받침하고 있습니다. 성장 요인으로는 종자 처리를 통한 초기 단계 보호 노력, 환경 부하를 줄이는 저용량 유효 성분에 대한 프리미엄 평가, 자동화 또는 원패스 살포 방식을 촉진하는 인건비 상승 등을 꼽을 수 있습니다. 미국의 살충제 시장은 여전히 엽면살포가 주류를 이루고 있지만, 작업자의 노출을 줄이고 투자 수익률을 높이는 기술 중심의 접근 방식으로 꾸준히 전환하고 있습니다. 현재 경쟁 전략은 제품 포트폴리오의 다양성, 규제 적응성, 가변 비율 분산 판단을 지원하는 데이터 플랫폼과의 통합에 초점을 맞추었습니다.

아몬드, 감귤류, 와인용 포도의 에이커당 수익성은 2020년부터 2024년까지 눈에 띄게 증가하여 수출 잔류 기준을 충족하는 고품질 농약에 대한 투자 확대를 촉진하고 있습니다. 캘리포니아 주에서는 같은 기간 동안 아몬드 재배 면적이 12% 증가했으며, 플로리다 주에서는 감귤류 회복을 위해 아시아 감귤류 잎파리 방제를 위한 살충제 프로그램을 확대했습니다. 특수작물은 곡물에 비해 3-5배 높은 조수익을 창출하는 경우가 많기 때문에 생산자들은 수율과 품질을 모두 보호하는 고가격 저위험 제제를 적극적으로 채택하고 있습니다. 동시에 기후 변화로 인해 태평양 연안 북서부 지역에 새로운 생산지역이 개척되어 대상 재배 면적이 확대되고 있습니다. 그 결과, 미국의 살충제 시장은 가격 상승을 흡수하면서도 수요의 급격한 감소를 초래하지 않는 프리미엄 카테고리에서 안정적인 판매량을 확보하고 있습니다.

규제 당국은 현재 옥수수 뿌리혹선충, 목화 꽃매미 등 해충 방제를 위해 작용 기작의 순환을 의무화하고 있습니다. 대학 확장 서비스 데이터에 따르면, 옥수수 생산자의 67%가 2024 년에 공식적인 저항성 관리 프로그램을 실시하여 2020 년의 23%에서 크게 증가한 것으로 나타났습니다. 이러한 변화는 새로운 활성 성분 수요 피크를 예측 가능하게 하는 동시에 구식 화합물의 노후화를 가속화할 것입니다. 따라서 제품 포트폴리오의 두께는 수익에 대한 헤지가 되고, 공급업체는 전체 시즌 계획을 충족시킬 수 있으며, 더 높은 점유율을 확보할 수 있습니다. 체계적인 로테이션은 여러 유효성분을 배합한 제제 개발도 촉진합니다. 이를 통해 살충제와 살균제의 보호 효과를 한 번의 처리로 제공함으로써 규제 준수와 노동력 절감을 동시에 달성할 수 있습니다.

기존 살충제 유효성분의 규제에 따른 퇴출은 시장 혼란을 야기하고 대체 화학물질의 빠른 채택을 강요하고 있습니다. 많은 경우, 에이커당 비용이 높아져 생산자의 경제성을 압박하는 반면, 강력한 대체 제품 포트폴리오를 보유한 기업에게는 이익을 가져다주는 경우가 많습니다. EPA가 2024년에 결정한 꽃가루 매개 곤충을 유인하는 작물에 대한 네오니코티노이드계 농약 사용 제한은 연간 약 3억 4,000만 달러 시장 가치를 소멸시켰으며, 공급 제한으로 인해 높은 가격을 요구하는 대체 화학물질에 대한 즉각적인 수요를 창출했습니다. 이러한 규제 조치는 화학물질 선택의 폭이 좁아지는 가운데 중소기업들이 지속가능한 제품 포트폴리오를 유지하기 위해 고군분투하고 있는 가운데 산업 구조조정을 가속화하고 있습니다.

2025년 기준 미국의 살충제 시장 점유율의 55.87%를 차지한 것은 엽면살충제였으나, 종자처리제는 작물 체계에 관계없이 범용성이 높아 2031년까지 연평균 복합 성장률(CAGR) 4.78%로 가장 높은 성장률을 나타낼 것으로 예측됩니다. 현재의 보급률이 지속된다면, 미국의 살충제 시장에서 종자처리제의 규모는 2031년까지 엽면살포제를 능가할 것으로 예측됩니다. 이 제품의 채택을 촉진하는 것은 단일 코팅으로 4-6주 동안 방제 효과를 얻을 수 있고, 동일한 엽면 살포 프로그램 대비 총 비용을 최대 40%까지 절감할 수 있다는 입증된 데이터입니다. 처리된 종자는 한 번의 작업으로 토양에 투입되기 때문에 추가 작업과정이 불필요하여 노동력 절감 효과가 뛰어납니다. 또한, 살포 작업자의 노출을 줄여주는 밀폐형 종자 코팅 장비는 규제 압력으로부터도 지지를 받고 있습니다.

관개 인프라가 잘 갖춰진 지역, 특히 수자원이 한정된 지역에서는 해충 방제와 수분 관리를 동시에 하기 위해 케미게이션(화학적 관개)과 점적관개에 대한 수요가 증가하고 있습니다. 훈증 처리는 딸기 재배상이나 묘목 재배에서 틈새 수요를 유지하고 있지만, 그 성장은 제한적입니다. 뿌리 영역 보호가 중요한 다년생 과수원에서는 토양 처리가 여전히 중요합니다. 현재 제품 개발은 뿌리 성장기 동안 지속적으로 방출되는 계통 활성 성분을 보완하는 캡슐화 된 마이크로 과립 및 생물학적 접종제에 초점을 맞추었습니다. 이러한 추세는 미국의 살충제 시장이 진화하는 농학 및 노동 현실에 대응하는 다양한 경로를 보여주고 있습니다.

미국의 살충제 시장 보고서는 적용 방법(화학 관개, 엽면 살포, 훈증, 종자 처리 등) 및 작물 유형(상업용 작물, 과일 및 채소, 곡물 및 시리얼, 콩류 및 유지 종자 등)별로 세분화되어 있습니다. 시장 예측은 금액(USD) 및 수량(미터톤)으로 제공됩니다.

The US insecticide market was valued at USD 7.98 billion in 2025 and estimated to grow from USD 8.35 billion in 2026 to reach USD 10.45 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

Rising specialty-crop acreage, wider precision-agriculture deployment, and persistent resistance issues are sustaining demand even as regulatory scrutiny tightens. Growth also reflects the drive for earlier-stage protection through seed treatment, the premium assigned to low-rate active ingredients that lighten environmental loading, and escalating labor costs that favor automated or one-pass application tactics. While foliar sprays still dominate, the US insecticide market is steadily tilting toward technology-enabled approaches that reduce operator exposure and improve return on investment. Competitive strategies now center on portfolio breadth, regulatory adaptability, and integration with data platforms that support variable-rate decisions.

Revenue potential per acre for almonds, citrus, and wine grapes grew markedly between 2020 and 2024, encouraging heavier investment in premium chemistry that meets export residue rules. In California, almond plantings rose 12% over the period, while Florida citrus recovery efforts enlarged insecticide programs aimed at Asian citrus psyllid suppression. Specialty crops often deliver three-to-five-fold higher gross returns relative to grains, so growers willingly adopt high-priced, reduced-risk formulations that protect both yield and quality. Climate shifts are simultaneously opening new production zones in the Pacific Northwest, widening the addressable acreage. As a result, the US insecticide market gains reliable volume from premium categories that absorb price increases without material demand destruction.

Regulatory mandates now codify rotation of modes of action for pests such as corn rootworm and cotton bollworm. University extension data show 67% of corn growers implemented formal resistance programs in 2024 versus 23% in 2020, a shift that creates predictable peaks for newer actives while hastening obsolescence of aging compounds. Portfolio depth, therefore, becomes a revenue hedge, with suppliers able to fill entire seasonal plans, enjoying greater share security. Structured rotation also stimulates development of formulations that blend multiple actives, bundling insecticidal and fungicidal protection in single passes to ensure compliance and labor savings.

Regulatory withdrawals of established insecticide active ingredients are creating market disruptions that force rapid adoption of alternative chemistries, often at higher per-acre costs that strain grower economics while benefiting companies with robust replacement product portfolios. The EPA's 2024 decision to restrict neonicotinoid applications on pollinator-attractive crops eliminated approximately USD 340 million in annual market value, creating immediate demand for alternative chemistries that command premium pricing due to limited supply. These regulatory actions are accelerating industry consolidation as smaller companies struggle to maintain viable product portfolios amid shrinking chemistry options.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Foliar sprays led with 55.87% of the US insecticide market share in 2025, whereas seed treatment posted the fastest growth at a 4.78% CAGR through 2031, anchored by their versatility across crop systems. The US insecticide market size for seed treatment is poised to eclipse by 2031 if current penetration continues. Adoption is supported by evidence that a single coating delivers four-to-six-week protection at up to 40% lower total cost than comparable foliar-only programs. Labor savings are significant because treated seed enters the soil in one operation, eliminating additional passes. Regulatory pressure also favors closed-system seed coaters that reduce applicator exposure.

Demand for chemigation and drip injection rises where irrigation infrastructure permits, especially in water-limited regions aiming for simultaneous pest and moisture management. Fumigation retains a niche in strawberry beds and nursery stock but exhibits minimal growth. Soil treatments remain important in perennial orchards where root-zone protection is critical. Product development now focuses on encapsulated microgranules and biological inoculants that complement systemic actives, offering sustained release throughout root flushes. Together, these trends illustrate the diversified pathway through which the US insecticide market accommodates evolving agronomic and labor realities.

The US Insecticide Market Report is Segmented by Application Mode (Chemigation, Foliar, Fumigation, Seed Treatment, and More), and Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).