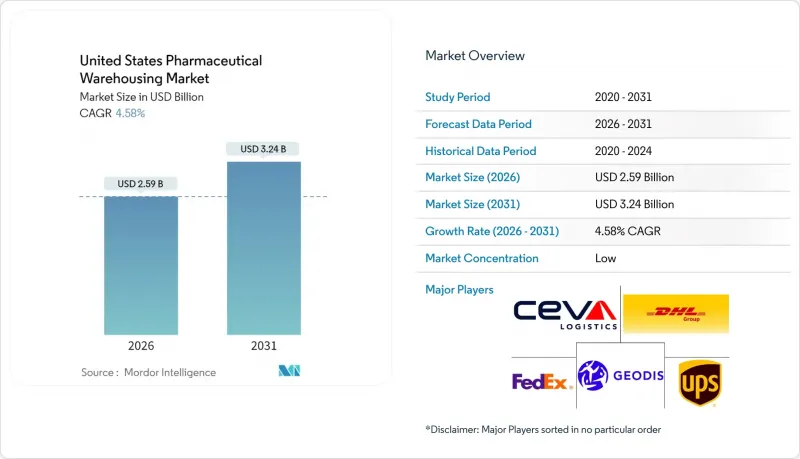

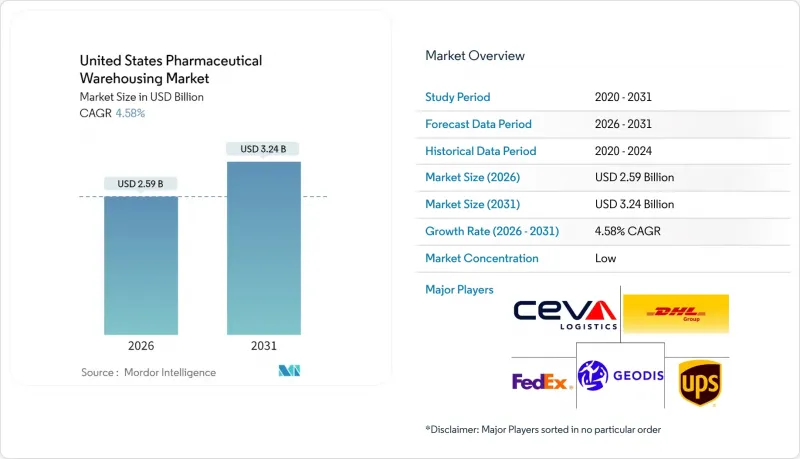

미국의 의약품 창고 시장은 2025년 24억 8,000만 달러에서 2026년에는 25억 9,000만 달러로 성장하고, 2026-2031년 CAGR 4.58%로 성장을 지속하여, 2031년까지 32억 4,000만 달러에 이를 것으로 예측됩니다.

바이오의약품 생산량 증가, DSCSA 직렬화 규정의 전면 시행, 급증하는 EC 풀필먼트 수요, 온도 관리형 인프라 및 자동화에 대한 새로운 자본 유입이 촉진되고 있습니다. 세포 및 유전자 치료제 파이프라인의 확장으로 초저온 요구사항이 추가되어 평방피트당 수익이 증가하고, 21 CFR 211.142에 따라 의무화된 안전한 추적 시스템이 창고의 IT 예산 구성을 변화시키고 있습니다. 에너지, 부동산, 전문 인력 등 비용 측면의 역풍은 여전히 두드러지지만, 로봇, IoT 센서, 친환경 콜드체인 설계에 대한 지속적인 투자로 영업 레버리지가 개선되고 있습니다. 3자물류(3PL) 업체 간 통합이 가속화되고 있는 배경에는 고수익 의료 관련 계약을 획득하고, 수직계열화를 추진하는 제조업체와 의료시스템 사업자에 대한 점유율 방어가 있습니다.

2025년 연간 설비투자액은 1,600억 달러(2024년 대비 15% 증가)에 달할 것으로 예상되며, 투자금액 10억 달러당 230만 평방피트의 추가 창고 수요가 발생할 것으로 예측됩니다. 바이오의약품은 신규 건설의 44%를 차지하며, 연속적인 생산 일정에 대응할 수 있는 모듈형 레이아웃이 요구되고 있습니다. FDA의 첨단 제조 기술 지원으로 실시간 모니터링 도입이 가속화되고 있으며, 시설에 이중화 전원 및 데이터 시스템 구축이 추진되고 있습니다. 세포치료제의 분산형 생산으로 인해 치료센터 인근에 마이크로 창고가 생겨나면서 기존의 허브 앤 스포크형 네트워크가 축소되는 추세입니다. 이러한 변화로 인해 미국의 의약품 창고 시장 전체에서 안전하고 높은 처리 능력을 갖춘 보관 거점에 대한 수요가 증가하고 있습니다.

mRNA 백신(-80℃)에서 극저온 요법(-196℃)에 이르는 초저온 요구사항이 주류가 되고 있으며, 21 CFR 600.15에 따른 엄격한 온도 범위 관리로 인해 상온 운영 기준 대비 에너지 사용량이 20-30% 증가함. 이에 따라 IoT 대응을 위한 검증 및 경보 시스템의 이중화가 요구되고 있습니다. 지속가능성 목표는 화석연료 의존도를 60% 감소시키는 재사용 가능한 운송 용기를 장려하고 있습니다. 사업자들은 소비 억제를 위해 고효율 컴프레서 및 LED 조명으로 개보수를 진행하고 있지만, 자본집약성은 중소기업의 진입장벽으로 작용하고 있습니다. 그 결과, 미국의 의약품 창고 시장에서 콜드체인 용량은 가격 결정력을 획득하고 있습니다.

지속적인 온도 기록, 전자 추적, 격리 구역 설치로 인해 2025년까지 규정 준수 예산이 25% 증가합니다. DSCSA 직렬화 시스템은 시설당 50만-200만 달러의 비용이 소요되어 소규모 사업자를 압박하고 있습니다. 안정화 이후에도 26%는 여전히 미지원 상태입니다. 벌칙은 벌금부터 형사책임까지 다양하며, 업계 구조조정을 가속화하고 있습니다. 문서화 부담 증가로 인해 제3자 전문업체에 대한 수요가 증가하는 반면, 범용 스토리지의 수익률은 줄어들고 있습니다. 이러한 규제 부담은 미국의 의약품 창고 시장의 성장 곡선을 둔화시키고 있습니다.

유통 및 재고 관리는 2025년 매출의 45.32%를 차지할 것으로 예상되며, 미국의 의약품 창고 시장에서 현금 흐름 안정화에 기여하는 장기 계약의 중요성을 보여줍니다. 부가가치 서비스(시리얼라이제이션, 키트화, 규제 문서 작성)는 DSCSA 시행 강화에 따라 CAGR 5.72%로 확대되고 있습니다. 클라우드 기반 WMS 솔루션은 시설의 90%를 커버하며, 가시성과 감사 대응력을 강화하고 있습니다.

부가가치 서비스는 일반적으로 기본 요금에 25-40% 추가 요금이 부과되므로, 컴플라이언스 관련 비용을 상쇄할 수 있습니다. RaaS(Robotics as a Service) 모델은 중견 사업자의 진입장벽을 낮추고, 시장 세분화를 촉진하는 동시에 효율성을 높이고 있습니다. FDA 21 CFR 205.50은 안전한 보관 및 취급을 규정하고 있으며, 대규모 컴플라이언스 대응을 일괄적으로 제공할 수 있는 사업자가 유리합니다. 이러한 추세로 인해 보관 업무가 기반이 강화되는 동시에 미국의 의약품 창고 시장 전체에서 서비스 복잡성이 향상되고 있습니다.

비콜드체인 시설은 여전히 미국의 의약품 창고 시장 규모의 58.05%를 차지하지만, 콜드체인 용량은 2031년까지 연평균 복합 성장률(CAGR) 6.01%로 계속 확대될 것으로 예측됩니다. 냉장-냉동-초저온 구역은 상온 대체시설보다 150-200% 높은 요금을 책정하여 에너지 소비를 보전하고 있습니다.

사업자들은 유연성과 설비투자의 균형을 맞추기 위해 상온 구조물에 모듈형 냉각실을 후장하고 있습니다. IoT 센서는 온도 편차 위험을 60% 감소시켜 업계 전체에서 연간 350억 달러의 손실을 억제하고 있습니다. 온도 관리 요건은 높은 컴플라이언스 장벽을 만들어 기존 사업자를 보호하고 있습니다. 바이오 의약품 파이프라인이 확대됨에 따라 미국의 의약품 창고 시장에서 콜드체인의 점유율은 점차 상승할 것입니다.

The United States Pharmaceutical Warehousing Market is expected to grow from USD 2.48 billion in 2025 to USD 2.59 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 4.58% CAGR over 2026-2031.

Rising biologics output, full enforcement of the DSCSA serialization rule, and surging e-commerce fulfillment volumes are channeling new capital into temperature-controlled infrastructure and automation. Cell and gene therapy pipelines are adding ultra-low temperature requirements that lift revenue per square foot, while secure track-and-trace systems mandated by 21 CFR 211.142 are reshaping warehouse IT budgets. Cost headwinds energy, real estate and specialized labor remain pronounced, yet continuous investment in robotics, IoT sensors and green cold-chain designs is improving operating leverage. Intensifying consolidation among third-party logistics (3PL) leaders aims to capture higher-margin healthcare contracts and defend share against vertically integrating manufacturers and health-system operators.

Annual capital spending of USD 160 billion in 2025 up 15% from 2024 couples every USD 1 billion invested with 2.3 million sq ft of extra warehouse need. Biologics represent 44% of new builds, prompting modular layouts that can flex with continuous-manufacturing schedules. FDA support for Advanced Manufacturing Technologies is accelerating real-time monitoring adoption, pushing facilities to embed redundant power and data systems. Decentralized production of cell therapies is spawning micro-warehouses near treatment centers, eroding the legacy hub-and-spoke network. These shifts collectively lift demand for secure, high-throughput storage nodes across the United States pharmaceutical warehousing market.

Ultra-low requirements from mRNA vaccines (-80 °C) to cryogenic therapies (-196 °C) are now mainstream, raising energy use 20-30% above ambient operations rules under 21 CFR 600.15 mandate precise ranges, prompting IoT-enabled validations and alarm redundancies. Sustainability targets are spurring reusable shippers that cut fossil-fuel reliance 60%. Operators retrofit high-efficiency compressors and LED lighting to curb consumption, yet capital intensity remains a barrier for smaller entrants. Consequently, cold-chain capacity garners pricing power within the United States pharmaceutical warehousing market.

Continuous temperature logging, electronic tracing and quarantine zones add 25% to 2025 compliance budgets. DSCSA serialization systems cost USD 0.5-2 million per facility, stretching small operators; 26% remain non-compliant post-stabilization. Penalties range from fines to criminal liability, accelerating consolidation. Documentation load drives demand for third-party specialists, yet shrinks margins for commodity storage. This regulatory burden dampens the growth curve of the United States pharmaceutical warehousing market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Distribution and Inventory Management generated 45.32% of 2025 revenue, a testament to long-term contracts that stabilize cash flows within the United States pharmaceutical warehousing market. Value-added offerings-serialization, kitting and regulatory documentation-are scaling at a 5.72% CAGR as DSCSA enforcement tightens. Cloud-based WMS solutions now cover 90% of facilities, enhancing visibility and audit readiness.

Value-added services typically bill 25-40% above baseline rates, offsetting compliance overhead. Robotics-as-a-Service models lower entry barriers for mid-tier operators, supporting market fragmentation while bolstering efficiency. FDA 21 CFR 205.50 stipulates secure storage and handling, favoring providers that can turnkey compliance at scale. These dynamics reinforce storage as the anchor while upgrading service complexity across the United States pharmaceutical warehousing market.

Non-cold-chain sites still constitute 58.05% of the United States pharmaceutical warehousing market size, but cold-chain capacity is outpacing at a 6.01% CAGR through 2031. Chilled, frozen and ultra-low zones command rates 150-200% higher than ambient alternatives, compensating for energy drain.

Operators retrofit ambient structures with modular cool chambers to balance flexibility and capex. IoT sensors cut temperature excursion risk 60%, curbing USD 35 billion annual losses industry-wide temperature mandates create high compliance hurdles, shielding incumbents. As biologics pipelines swell, cold-chain share will progressively rise within the United States pharmaceutical warehousing market.

The United States Pharmaceutical Warehousing Market Report is Segmented by Service Type (Storage, Distribution and Inventory Management, and More), Warehouse Type (Cold-Chain Warehouse, Non-Cold-Chain Warehouse), Product Type (Prescription Drugs, and More), End User (Pharmaceutical Manufacturers, Healthcare Providers, Retail & Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).