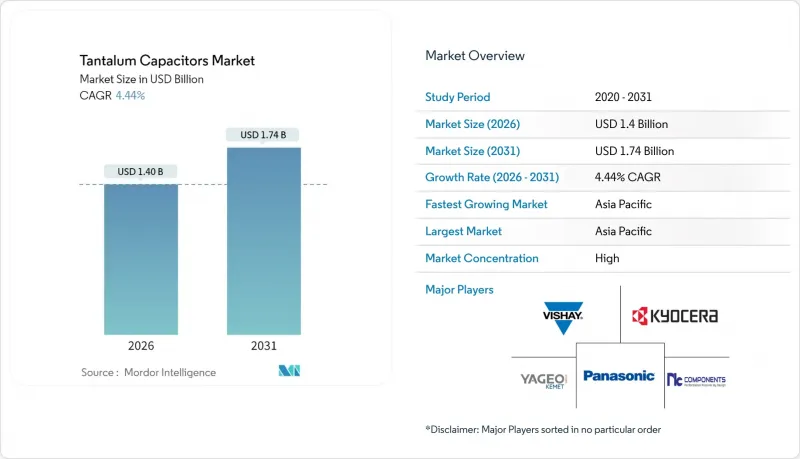

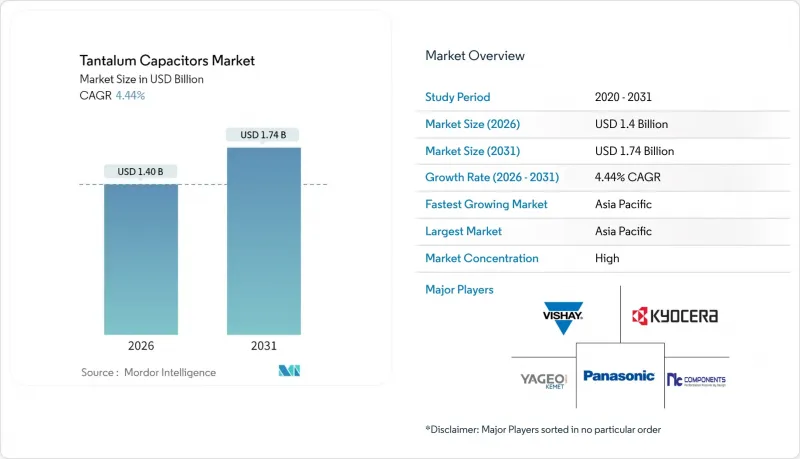

탄탈룸 커패시터 시장은 2025년 13억 4,000만 달러에서 2026년에는 14억 달러로 성장하며, 2026-2031년에 CAGR 4.44%로 추이하며, 2031년까지 17억 4,000만 달러에 달할 것으로 예측되고 있습니다.

높은 용량 밀도, 온도 안정성 및 장기 신뢰성에 대한 강한 수요로 인해 탄탈 커패시터 시장은 지속적인 비용 압박에도 불구하고 미션 크리티컬 전자기기 분야에서 확고한 입지를 유지하고 있습니다. 민생기기의 소형화, 자동차 전동화 가속화, 5G 인프라 확대, 다층세라믹커패시터(MLCC)공급망 혼란이 맞물려 꾸준한 성장을 지원하고 있습니다. 한편, 주요 광물에 대한 무역 제한과 원자재 가격 급등은 CAGR 전망을 억제하고 있으며, 바이어 측에 조달 전략의 다양화를 요구하고 있습니다.

기판의 소형화에 따라 평방센티미터당 방열량이 급격히 증가하고 있으며, 스마트폰, 웨어러블 기기, 임베디드 의료기기에 내장된 전원 관리 IC에서 탄탈럼의 열 안정성은 필수적입니다. 최신 플래그십 스마트폰에는 1,000개 이상의 커패시터가 내장되어 있으며, 탄탈럼 커패시터는 체적 효율과 높은 리플로우 저항이 요구되는 중요한 전원 라인 조정 역할을 담당하고 있습니다. 접이식 및 초박형 폼팩터를 지향하는 OEM의 로드맵은 정전 용량을 희생하지 않고 소형 케이스 크기에 대한 수요를 강화하여 탄탈럼 커패시터 시장의 모멘텀을 유지하고 있습니다.

자동차의 전동화는 구동용 인버터, 차량용 충전기, 첨단운전자보조시스템(ADAS), 인포테인먼트 모듈 등 다양한 분야에서 커패시터 수요를 확대하고 있습니다. 폴리머 탄탈 커패시터는 -40℃-+150℃의 작동 온도 범위에서 인증을 받았으며, 낮은 등가 직렬 저항(ESR)을 실현했습니다. 48V 및 새로운 800V 아키텍처에서 세라믹 커패시터를 능가하는 성능을 제공합니다. TDK는 자동차 수주 급증으로 차량 단가가 상승하고 있다는 점을 근거로 2025년도의 수동부품 성장을 예측했습니다. 이러한 추세로 인해 탄탈 커패시터 시장은 장기적인 전기화 추세와 잘 연동되고 있습니다.

콩고민주공화국의 분쟁 관련 생산 중단과 소규모 광부들의 강제노동 의혹으로 인해 원자재 공급라인이 타이트해져 커패시터 부품원가(BOM)에 가격 상승이 파급되고 있습니다. 2024년 9월 중국산 탄탈럼 수입품에 대한 25% 관세가 발효된 후, 미국의 탄탈럼 소비량은 급격히 감소했습니다. 이로 인해 OEM 업체들은 공급처를 다양화하고 설계를 재검토해야 하며, 이러한 혼란은 비용에 민감한 시장에서 탄탈럼 커패시터의 침투를 제한하고 있습니다.

고체 폴리머 탄탈럼 커패시터는 OEM(Original Equipment Manufacturer)들이 ESR 감소와 페일 세이프 성능을 우선시한 결과, 2025년 매출의 38.62%를 차지했습니다. 탄탈럼 커패시터 시장은 폴리머의 안전한 고장 모드(이산화망간(MnO2) 음극에 따른 산소 발생 위험 제거)의 이점을 누리고 있습니다. 니오브 산화물 커패시터는 여전히 틈새 시장이지만, 설계자들이 원자재 리스크를 회피하려는 움직임에 따라 2031년까지 연평균 복합 성장률(CAGR) 5.94%를 나타낼 것으로 예측됩니다. 고체 MnO2 소자는 비용 중심의 민생 기기용 양산 옵션으로, 습식 전해질 구조는 대량 저장 틈새 시장에서의 입지를 유지할 것입니다.

포장 기술 혁신은 재료 전환을 보완합니다. 폴리머 부품은 5G 전력 증폭기 및 EV 차량용 충전기의 리플 전류 요구에 대응하여 탄탈럼 커패시터 시장을 강화합니다. 의료용 임플란트 및 웨어러블 센서가 소형화를 추구하는 가운데, 1,000회 이상의 열 사이클을 견딜 수 있는 폴리머 기술의 안정성이 결정적인 요인으로 작용합니다.

표면 실장 패키지는 2025년 매출의 77.45%를 차지할 것으로 예상되며, 자동 조립 및 다층 PCB의 밀도 목표를 반영하여 CAGR 5.03%를 나타낼 것으로 예측됩니다. 표면 실장 형태와 관련된 탄탈 커패시터 시장 규모는 픽앤플레이스 정확도 향상에 따른 킵아웃 존의 축소로 인해 확대되고 있습니다. 스루홀 유형은 기계적 견고성과 현장 유지보수성이 형상보다 우선시되는 항공우주, 국방, 중공업용 기판에서 여전히 중요한 위치를 차지하고 있습니다.

표면 실장 기술의 우위는 기판 내장형 커패시터 로드맵에 의해 더욱 강화되고 있습니다. 이는 Z축 방향의 높이를 압축하여 전원 루프의 인덕턴스를 단축시킵니다. 삼성 전자 전기기계는 부품 라이브러리를 업데이트하여 RF 전력 모듈 시뮬레이션 워크플로우를 효율화했습니다. 이로 인해 표면 실장형 탄탈럼 커패시터로 설계 채택이 더욱 기울어지고 있습니다.

아시아태평양은 2025년 세계 매출의 44.10%를 차지할 것으로 예상되며, 2031년까지 연평균 5.63%의 성장률을 보일 것으로 예측됩니다. 중국에서는 첨단 패키징에 대한 보조금 지원을 배경으로 한 민생 전자기기 생산 촉진으로 수동 부품 수요가 증가하고, 한국과 대만에서는 고주파 디커플링 부품을 소비하는 메모리 제조 공장이 기반이 되고 있습니다.

북미에서는 중국산 탄탈럼 수입에 대한 25% 관세와 2027년 시행 예정인 미 국방부 조달 규제를 배경으로 공급망 재구축이 진행되고 있습니다. 국내 커패시터 제조업체들은 분쟁지역 위험으로부터 군사 프로그램을 격리하기 위해 호주와 브라질에서 윤리적으로 조달된 광석 인증을 서둘러 진행하고 있습니다. 이러한 정책 전환은 지역별로 수요량을 재편하는 한편, 추적 가능한 미국산 탄탈럼 부품에 대한 틈새 수요를 창출하고 있습니다.

유럽은 지속가능성에 대한 노력을 중시하며, 분쟁 없는 인증 탄탈럼의 조달을 추진하고 있습니다. 독일의 자동차 1등급 공급업체는 물류 루프를 단축하고 적기 생산 요구에 대응하기 위해 폴란드와 체코의 커패시터 공장과 협력하여 해상 운송의 장기적인 지연으로부터 탄탈럼 커패시터 시장을 보호하고 있습니다.

세계 기타 지역이 대체 원료 공급기지로 부상하고 있습니다. 대규모 경암 탄탈럼 광맥을 보유한 호주는 유럽과 미국의 ESG 기준에 부합하는 정제 능력을 확충하고 있습니다. 르완다는 농축물 정제 인프라를 구축하여 현지 부가가치 향상을 도모하고 있습니다. 브라질 미나스 제라이스 주 프로젝트는 광석 공급량 증가를 가져와 세계 공급 리스크 분산에 기여합니다.

The tantalum capacitors market is expected to grow from USD 1.34 billion in 2025 to USD 1.4 billion in 2026 and is forecast to reach USD 1.74 billion by 2031 at 4.44% CAGR over 2026-2031.

Strong demand for high-capacitance density, temperature stability, and long-term reliability keeps the tantalum capacitors market firmly rooted in mission-critical electronics, even as cost pressures persist. Miniaturization of consumer devices, accelerated electrification of vehicles, expanding 5G infrastructure, and supply-chain disturbances in multilayer ceramic capacitors (MLCCs) collectively underpin steady expansion. At the same time, trade restrictions on critical minerals and raw-material price spikes temper the CAGR outlook and force buyers to diversify sourcing strategies.

As circuit boards shrink, heat dissipation per square centimeter rises steeply, making tantalum's thermal stability indispensable for power-management ICs embedded within smartphones, wearables, and implantable medical devices. A modern flagship smartphone integrates more than 1,000 capacitors, and tantalum versions secure critical power-rail conditioning roles where volumetric efficiency and elevated reflow-temperature tolerance intersect . OEM roadmaps that target foldable, ultra-slim form factors reinforce demand for smaller case sizes without sacrificing capacitance, sustaining momentum in the tantalum capacitors market.

Automotive electrification multiplies capacitor demand across traction inverters, on-board chargers, advanced driver assistance systems, and infotainment modules. Polymer tantalum capacitors remain qualified at -40 °C to +150 °C and exhibit low equivalent series resistance (ESR), outperforming ceramics in 48 V and emerging 800 V architectures. TDK projected growth in passive components for fiscal 2025 by citing surging automotive orders that elevate value per vehicle . These trends keep the tantalum capacitors market well aligned with the long-term electrification curve.

Conflict-related production interruptions in the Democratic Republic of Congo and forced-labor allegations among artisanal miners tighten raw-material supply lines, transmitting price spikes through to capacitor BOMs . U.S. consumption fell sharply after a 25% tariff on Chinese tantalum imports took effect in September 2024, compelling OEMs to dual-source or re-engineer designs . These disruptions limit cost-sensitive penetration of the tantalum capacitors market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solid polymer tantalum capacitors captured 38.62% revenue in 2025 as OEMs prioritized ESR reduction and fail-safe performance . The tantalum capacitors market benefits from polymers' benign failure mode, eliminating the oxygen generation risk that accompanies MnO2 cathodes. Niobium oxide capacitors, though still niche, chart a 5.94% CAGR through 2031 as designers hedge raw-material risk. Solid MnO2 devices remain the volume option for cost-sensitive consumer gear, while wet-electrolytic constructions hold ground in bulk-storage niches.

Packaging innovation complements material shifts. Polymer parts support ripple-current demands in 5G power amplifiers and EV onboard chargers, reinforcing the tantalum capacitors market. As medical implants and wearable sensors push for smaller case sizes, polymer technology's stability across 1,000+ thermal cycles becomes decisive .

Surface-mount packages commanded 77.45% revenue in 2025 and are forecast to grow 5.03% CAGR, reflecting automated assembly and multilayer PCB density targets. The tantalum capacitors market size linked to surface-mount formats gains from pick-and-place accuracy improvements that shrink keep-out zones. Through-hole variants stay relevant in aerospace, defense, and heavy industrial boards where mechanical robustness and field maintainability trump form factor.

Surface-mount leadership is reinforced by PCB-embedded capacitor roadmaps that compress z-axis height and shorten power-loop inductance. Samsung Electro-Mechanics updated its part libraries to streamline simulation workflows for RF power modules, further tilting design wins toward surface-mount tantalums.

The Tantalum Capacitors Market Report is Segmented by Product Type (Solid MnO2, Solid Polymer, Wet Electrolytic, Niobium Oxide), Mounting Type (Surface-Mount, Through-Hole), Capacitance Range (Up To 100 MF, Others), Application (Consumer Electronics, Automotive Electronics, Industrial Equipment, Medical Devices, Telecommunications Infrastructure, and ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific accounted for 44.10% of global revenue in 2025 and is poised to expand at a 5.63% CAGR through 2031. China's consumer-electronics production push, backed by subsidies for advanced packaging, reinforces passive-component pull, while Korea and Taiwan anchor memory fabs that consume high-frequency decoupling parts.

North America retools supply chains after a 25% tariff on Chinese tantalum imports and impending 2027 DoD sourcing restrictions. Domestic capacitor manufacturers expedite the qualification of ethically sourced ore from Australia and Brazil to insulate military programs from conflict-area risks . These policy shifts reshape regional volumes but also create niche demand for traceable, U.S.-made tantalum components.

Europe focuses on sustainability credentials and drives procurement toward certified conflict-free tantalum. German automotive Tier 1 suppliers collaborate with Polish and Czech capacitor plants to shorten logistics loops and meet just-in-time mandates, protecting the tantalum capacitors market against lengthy maritime delays.

Rest-of-World regions rise as alternative feedstock hubs. Australia, possessing large hard-rock tantalite reserves, adds refining capacity aligned with Western ESG standards, while Rwanda develops concentrate-upgrading infrastructure to capture more value locally. Brazil's Minas Gerais projects unlock incremental ore tonnage that diversifies global supply risk.