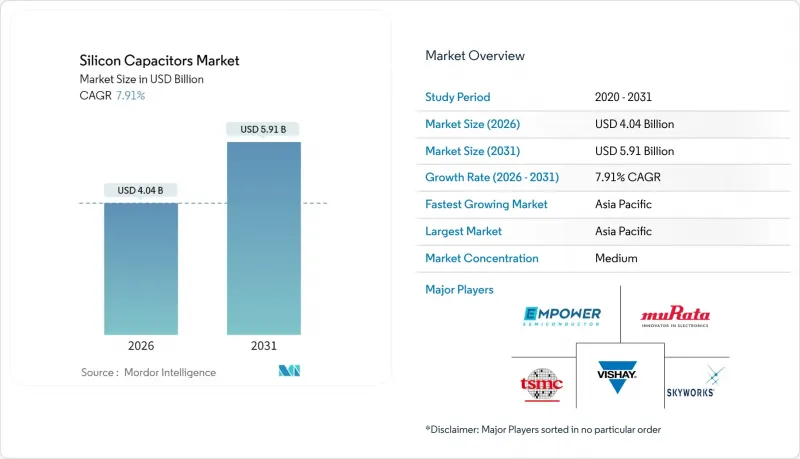

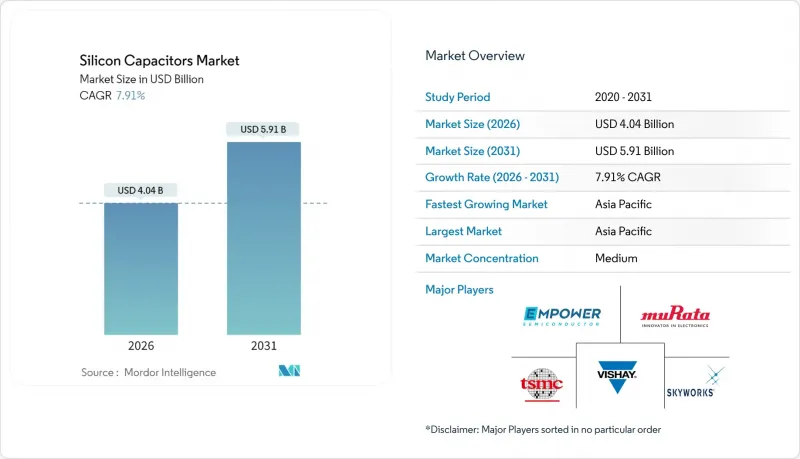

실리콘 커패시터 시장은 2025년 37억 4,000만 달러에서 2026년에는 40억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 7.91%로 추이하며, 2031년까지 59억 1,000만 달러에 달할 것으로 예측되고 있습니다.

이는 5G 및 차세대 6G 디바이스를 위한 고밀도 RF 프론트엔드 설계의 급속한 확산, 고온에 대응하는 차량용 LiDAR 모듈로의 전환, 딥 그루브 커패시터를 내장한 칩렛 기반 2.5D 인터포저에 대한 강력한 수요 증가를 반영합니다. 파운더리가 첨단 수동 부품에 대한 새로운 라인을 할당함으로써 탄소나노섬유 MIM 구조공급 안정성이 향상되고 이전의 비용 상승 추세가 완화되었습니다. 아시아태평양은 집적화된 웨이퍼 제조거점과 적극적인 무선 인프라 구축으로 생산 측면에서 뚜렷한 우위를 유지하고 있습니다. 한편, 북미는 100GHz 이상에서 작동하는 국방용 평판 어레이의 프리미엄 수요를 확보하고 있습니다. 기존 수동 부품 업체들이 임베디드 커패시터를 로직 다이와 번들로 묶은 파운드리 수준의 제품군에 맞서 점유율을 지키고 있는 가운데, 경쟁 환경은 더욱 치열해지고 있습니다. 이를 통해 대량생산 스마트폰용 제품의 매출은 감소하는 반면, 열악한 환경의 틈새 시장에서의 성장 여력은 유지되고 있습니다.

차세대 스마트폰은 4G 설계 대비 40-60% 더 많은 정전용량 소자를 통합하므로 OEM 업체들은 6-40GHz 대역의 기생 인덕턴스를 감소시키는 실리콘 유전체에서 세라믹 MLCC로 전환할 수밖에 없습니다. 무라타제작소가 2025년 3월에 발표한 디지털 엔벨로프 트래킹 플랫폼은 트래커 모듈에 실리콘 커패시터를 내장하여 광대역 5G 신호에서 25%의 전력 효율 향상을 실현했습니다. 이러한 접근 방식은 24개 스펙트럼 블록에 걸친 멀티밴드 동작을 통해 컴팩트하고 높은 Q값의 수동 부품의 가치를 높이는 3GPP 릴리즈 18의 6G 준비와 일치합니다. 파운드리 수준의 딥 그루브 집적화를 통해 RF-SIP 어셈블리 비용을 15-20% 절감하고, 주요 스마트폰 브랜드가 설정한 8mm 미만의 Z방향 높이 제한을 충족합니다. 이러한 추세에 따라 세계 최대 스마트폰 ODM 클러스터가 존재하는 아시아태평양이 가까운 미래에 수요의 중심지가 될 것으로 보입니다.

레벨 3 이상의 차량에서 카메라와 LiDAR의 융합으로 인해 센서 모듈이 후드 아래에 배치되어 수동 부품은 150℃ 이상의 환경에 노출될 수 있습니다. 실리콘 커패시터는 동일한 스트레스 하에서 최대 65%의 용량 손실이 발생하는 MLCC(다층 세라믹 커패시터)에 비해 훨씬 더 예측 가능한 용량 특성을 유지합니다. 2024년 9월 로옴이 DENSO와 제휴한 배경에는 고온 환경용 아날로그 프론트엔드(AFE) 수요 증가와 AEC-Q200 Grade 0 부품의 일반적인 장기 설계 채용 주기를 강화하기 위한 목적이 있습니다. 현재 프리미엄 전기자동차 플랫폼에는 8-12개의 LiDAR 유닛이 사양화되어 있으며, 각 유닛에는 바이어스, 평활화, EMI 억제를 위해 20-30개의 실리콘 커패시터가 내장되어 있습니다. 이를 통해 2027년까지 연간 1억 5,000만 달러 수요 증가가 예상됩니다. 유럽이 선행 도입 지역인 반면, 미국 제조업체들도 연방 NCAP 기준 강화로 LiDAR 탑재 안전시스템이 평가됨에 따라 조달에 박차를 가하고 있습니다.

바이어스 전압이 25V를 초과하면 이산화규소 적층 커패시터의 누설 전류가 급격히 증가합니다. 이는 마일드 하이브리드차량에 채택되고 있는 48V 아키텍처에 대한 적합성을 제한합니다. 일반적으로 34V 부근에서 파괴가 발생하여 세라믹 부품의 표준 내전압 50V보다 훨씬 낮습니다. 설계자들은 안전 작동 한계 내에 맞추기 위해 추가적인 레귤레이션 단계를 추가하는 경우, 8-12%의 비용 증가를 보고하고 있으며, 이는 산업용 드라이브 및 자동차 컨버터에 대한 채택을 제한하고 있습니다. 고온 환경에서는 문제가 더욱 심각해져 장기 유지 성능이 저하되므로 OEM(Original Equipment Manufacturer)는 부피와 압전 노이즈의 단점에도 불구하고 고전압 라인에 MLCC를 계속 사용해야 합니다.

딥트렌치 공정은 좁은 다이 면적에서 높은 용량을 구현하는 3차원 측벽 구조의 장점으로 인해 2025년 실리콘 커패시터 시장에서 35.70%의 점유율을 차지할 것으로 예측됩니다. MIM(금속 이온 결합법) 변형으로 인한 실리콘 커패시터 시장 규모가 가장 빠르게 성장하고 있으며, 탄소나노섬유 전극이 특수 재료를 사용하지 않고도 밀도를 200 nF/mm2까지 증가시켜 CAGR 9.03% 성장하고 있습니다. MOS와 MIS는 틈새 시장에 머물러 있으며, 선형성이 순수 밀도를 능가하는 전압 제어 발진기용으로 제공되고 있습니다. 전략적 로드맵은 현재 60 이상의 유전율을 목표로 하고 있으며, 2027년까지 트렌치 부품을 500 nF/mm2로 끌어올려 모바일 SoC용 소형 전원 공급 네트워크의 매력을 강화하는 것을 목표로 하고 있습니다.

설계 채택은 휴대폰용 PMIC(전원관리 IC)와 2.5D AI 가속기에 집중하고 있습니다. 이 경우, 이식형 트렌치 뱅크는 디커플링 레이어 수를 줄이고, 패키지 두께를 줄일 수 있습니다. 제조 규모는 파운드리 투자에 따라 달라지지만, 멀티 프로젝트 웨이퍼는 팹리스 스타트업의 시제품 제작에 대한 접근을 용이하게 해줍니다. 특수 IP 프로바이더와 주요 파운더리 간의 라이선스 계약은 진입장벽을 낮추고, 소비자 및 자동차 시장 전반에 걸쳐 기술 보급을 촉진하고 있습니다.

2025년에는 수직 배선과 정전용량 스토리지를 단일 성형 공정으로 통합하여 고 대역폭 메모리 스택을 효율화하는 3D 관통 실리콘 비아 구조가 매출의 38.05%를 차지할 것으로 예측됩니다. 한편, 최첨단 AI 패키지가 초박형 파워플레인에 채택하는 CNF-MIM 옵션은 CAGR 9.21%를 기록했습니다. 평면 설계는 성능보다 비용이 우선시되는 웨어러블 기기 분야에서 살아남고, 실리콘 관통형 딥 그루브 브리지는 평면 설계보다 높은 Q값을 제공하면서 TSV보다 복잡성을 줄여 중간 영역을 메우는 역할을 합니다.

차세대 CNF 층의 인증 주기가 빠르게 진행되고 있으며, Smoltek은 2025년 검증 테스트에서 200nF/mm2에서 34V의 항복 전압을 기록했습니다. 패키징 업체들이 TSV와 커패시터 툴을 공유함에 따라 공급업체들은 각 다이 영역에 최적화된 혼합 구조 솔루션을 제공할 수 있게 되었습니다. 이러한 모듈성은 다양한 공급 레일에 걸친 맞춤형 임피던스 제어를 요구하는 서버 및 항공우주 통합업체 간의 지속적인 거래를 촉진합니다.

아시아태평양은 2025년 실리콘 커패시터 시장의 45.95%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 8.84%를 유지할 것으로 예측됩니다. 중국은 적극적인 5G 매크로셀 구축과 세계 최대 규모의 전기자동차 기반이 물량을 지원하고, 일본과 한국은 Material-2 기술과 정밀 자동차 수요로 기여합니다. 대만의 파운드리 생태계는 딥트렌치 및 CNF-MIM 생산에 즉시 접근할 수 있으며, 팹리스 고객의 설계 주기를 단축할 수 있습니다. 인도의 생산 연동형 인센티브는 개별 수동 부품 조립을 유치하고 있지만, 지역 전체 생산량에 비하면 아직 초기 단계에 불과합니다. 역내 각국 정부의 지원으로 실리콘 커패시터 산업의 생산 능력을 직접적으로 강화하는 새로운 300mm 라인이 구축되고 있습니다.

북미는 국방, 우주, 고성능 컴퓨팅 수요를 통합하여 수량은 적지만 높은 단가를 실현하고 있습니다. 국방부의 안전공급 의무화로 국내 첨단 패키징이 우대받고, 실리콘 커패시터 시장 규모 확대. 애리조나, 텍사스, 오하이오 주에 미국 팹 계획에는 로직 웨이퍼 생산과 통합된 트렌치 커패시터 후공정 모듈이 포함되어 있으며, 해외 공급 의존도를 낮추기 위해 노력하고 있습니다. 미시간과 캘리포니아의 전기자동차 제조업체들은 48V 서브시스템에 고온용 실리콘 커패시터를 지정하고 있으며, 기존 항공우주 제조업체 위주였던 포트폴리오에 자동차 분야로의 다양화가 이루어지고 있습니다.

유럽에서는 자동차의 신뢰성과 산업 자동화에 대한 중요성이 강조되고 있습니다. 독일의 Tier 1 공급업체는 라이더 바이어스 및 SiC 인버터 평활화에 사용되는 0등급 커패시터에 대한 다년 계약을 체결하여 자동차 생산량 변동에도 불구하고 2031년까지 지역 수요를 유지할 수 있도록 하고 있습니다. 프랑스와 이탈리아의 항공우주 클러스터는 소형 위성 버스용 내방사선 수동 부품이 필요하며, 100GHz 이상의 프리미엄 부문을 강화하고 있습니다. REACH 및 RoHS의 PFAS 프리 재료로의 확장을 포함한 EU 환경 규제는 세라믹이 적합성 심사에 직면한 분야에서 실리콘 유전체의 채택을 촉진하고 있습니다.

The silicon capacitors market is expected to grow from USD 3.74 billion in 2025 to USD 4.04 billion in 2026 and is forecast to reach USD 5.91 billion by 2031 at 7.91% CAGR over 2026-2031.

This expansion tracks the rapid proliferation of high-density RF front-end designs for 5G and nascent 6G devices, the shift toward high-temperature automotive LiDAR modules, and the strong push for chiplet-based 2.5D interposers that embed deep-trench capacitors. Supply stability for carbon-nanofiber MIM structures is improving as foundries allocate new lines to advanced passive components, tempering earlier cost inflation. Asia-Pacific retains clear production leadership because of its concentrated wafer fabrication base and aggressive wireless-infrastructure roll-outs, while North America captures premium demand from defense-grade flat-panel arrays operating above 100 GHz. Competitive intensity is rising as traditional passive-component vendors defend share against foundry-level offerings that bundle embedded capacitors with logic dies, narrowing gross-margin spreads on high-volume phones yet preserving upside in extreme-environment niches.

Next-generation smartphones integrate 40-60% more capacitive elements than 4G designs, forcing OEMs to migrate from ceramic MLCCs to silicon dielectrics that mitigate parasitic inductance at 6-40 GHz. Murata's March 2025 Digital Envelope Tracking platform demonstrates a 25% power-efficiency gain in broadband 5G signals by embedding silicon capacitors within the tracker module. The approach aligns with 3GPP Release 18 preparations for 6G, where multi-band operation across 24 spectrum blocks elevates the value of compact, high-Q passives. Foundry-level deep-trench integration further eliminates 15-20% of RF-SIP assembly cost while meeting sub-8 mm z-height limits set by tier-one handset brands. These dynamics position Asia-Pacific, home to the largest smartphone ODM cluster, as the near-term demand epicenter.

Camera-lidar fusion in Level 3+ vehicles is pushing sensor modules under the hood, exposing passives to >=150 °C. Silicon capacitors retain capacitance far more predictably than MLCCs, which lose up to 65% under identical stress. ROHM's September 2024 tie-up with DENSO targets high-temperature analog front-ends, reinforcing the long-cycle design wins typical of AEC-Q200 Grade 0 parts. Premium electric-vehicle platforms now specify 8-12 lidar units, each embedding 20-30 Si-Caps for bias, smoothing, and EMI suppression, translating to a USD 150 million annual uplift by 2027. Europe remains the early adopter, yet U.S. makers are accelerating procurement as federal NCAP upgrades reward lidar-backed safety stacks.

Leakage current rises sharply in silicon dioxide stacks when bias surpasses 25 V, limiting suitability for the 48 V architectures emerging in mild-hybrid vehicles. Breakdown typically occurs near 34 V, well below the 50 V routine for ceramic parts. Designers adding extra regulation stages to stay within safe-operating limits report 8-12% cost penalties, constraining adoption in industrial drives and automotive converters. Elevated temperatures compound the issue, degrading long-term retention and forcing OEMs to retain MLCCs for high-voltage rails despite the volume and piezo-electric noise drawbacks.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Deep-Trench processes secured 35.70% silicon capacitors market share in 2025, benefiting from three-dimensional sidewalls that achieve high capacitance within tight die footprints. The silicon capacitors market size attributed to MIM variants is rising quickest, expanding at 9.03% CAGR as carbon-nanofiber electrodes lift density to 200 nF/mm2 without exotic materials. MOS and MIS remain niche, servicing voltage-controlled oscillators where linearity outweighs raw density. Strategic roadmaps now target dielectric constants above 60 to push trench parts toward 500 nF/mm2 by 2027, reinforcing their appeal for compact power-delivery networks in mobile System-on-Chips.

Design wins concentrate on handset PMICs and 2.5D AI accelerators, where embedded trench banks reduce decoupling layer count and shrink package thickness. Manufacturing scale hinges on foundry investment, yet multi-project wafers are easing prototype access for fab-less start-ups. License agreements between specialty IP providers and leading fabs lower entry barriers, supporting broader technology penetration across consumer and automotive tiers.

3D through-silicon-via structures held 38.05% revenue in 2025 by combining vertical interconnect and capacitive storage within one formation step, streamlining high-bandwidth-memory stacks. Meanwhile, CNF-MIM options post a 9.21% CAGR as bleeding-edge AI packages adopt them for ultra-thin power planes. Planar designs survive in wearables where cost trumps performance, and through-silicon deep-trench bridges the middle ground by offering higher Q than planar yet lower complexity than TSV.

Qualification cycles for next-generation CNF layers progress swiftly; Smoltek recorded 34 V breakdown at 200 nF/mm2 in 2025 validation runs. As packaging houses co-locate TSV and capacitor tooling, suppliers can deliver mixed-structure solutions optimized for each die region. This modularity fosters stickiness among server and aerospace integrators that demand tailored impedance control across a range of supply rails.

The Silicon Capacitors Market Report is Segmented by Technology (MOS, MIS, Deep-Trench, and MIM), Capacitor Structure (Planar, 3D TSV, and More), End-User Application (Automotive and Mobility, Consumer Electronics, and More), Frequency Band (Less Than 6 GHz, 6-40 GHz, and More), Integration Level (Discrete SMD, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific retained 45.95% of the silicon capacitors market in 2025 and is projected to log an 8.84% CAGR through 2031. China anchors volume with aggressive 5G macro-cell roll-outs and the world's largest electric-vehicle base, while Japan and South Korea contribute Material-2 technology and precision automotive demand. Taiwan's foundry ecosystem enables immediate access to deep-trench and CNF-MIM production, shortening design cycles for fab-less customers. India's production-linked incentives are luring discrete-passive assembly but remain nascent relative to overall regional output. Government sponsorship across the bloc underpins new 300 mm lines that directly enhance the silicon capacitors industry capacity.

North America combines defense, space, and high-performance-compute needs, delivering high ASPs despite smaller unit counts. The region's silicon capacitors market size is bolstered by DoD secure-supply mandates favoring on-shore advanced packaging. U.S. fab announcements in Arizona, Texas, and Ohio include trench-cap back-end modules integrated with logic wafer starts, improving independence from overseas supply. Electric-vehicle OEMs in Michigan and California specify high-temperature Si-Caps for 48 V subsystems, adding automotive diversification to a portfolio historically dominated by aerospace primes.

Europe emphasizes automotive reliability and industrial automation. German Tier-1 suppliers lock multi-year commitments for Grade 0 capacitors used in lidar bias and SiC inverter smoothing, maintaining regional demand through 2031 despite vehicle-production volatility. French and Italian aerospace clusters require radiation-hardened passives for small-satellite buses, reinforcing premium segments above 100 GHz. EU environmental regulations, including REACH and RoHS extensions for PFAS-free materials, drive silicon-dielectric adoption where ceramics face compliance scrutiny.