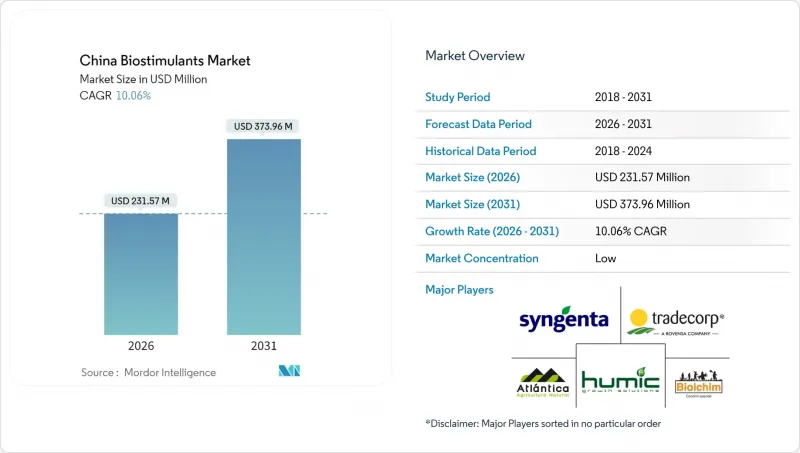

2026년 중국의 생물촉진제 시장 규모는 2억 3,157만 달러로 추정되며, 2025년 2억 1,040만 달러에서 성장이 전망됩니다.

2031년까지 3억 7,396만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 10.06%의 성장률을 보일 것으로 전망됩니다.

비료 이용 효율 향상을 위한 정책 지원 가속화, 견조한 보호 재배 면적, 전국적인 스마트 농업 추진이 수요 확대에 유리한 조건을 형성하고 있습니다. 해조류 추출물의 선도적 지위, 온실 재배에서의 아미노산 채용 증가, 토양 건강 악화에 대한 대책은 더욱 강화가 요구되고 있습니다. 경쟁 차별화는 품질 보증, 원자재 통합, 디지털 응용 지침에 초점을 맞추고 있습니다. 특허 출원 증가와 외국인 직접투자의 활성화는 중국의 식량안보 강화와 농업 투입물 배출 감소라는 두 가지 목표에 부합하는 혁신주도형 성장 경로를 보여주고 있습니다.

2024년에 시행된 새로운 생태보호 보상 규정에 따라 생태보호구역의 생물 자극제 비용의 30-50%를 상환하여 화학비료와의 가격차이가 줄어들었습니다. 등록 절차의 효율화로 인해 적합성 제제의 시장 진입이 12개월 이내에 완료될 수 있게 되었습니다. 국가의 탄소 중립 목표에 따라 요소 및 복합 비료의 저배출 대체제로서 생물학적 자극제의 중요성이 커지고 있습니다. 연간 총 150억 위안(21억 달러)에 달하는 성급 기금은 소매업체와 대규모 농장의 운영자금 부담을 줄이기 위해 우대 융자 및 세금 공제 혜택을 제공합니다. 병행되는 연구 보조금은 중국의 다양한 토양에 적응하는 제품 개발을 촉진하고, 국내 제조 경쟁력을 강화하고 있습니다.

식품 안전에 대한 우려로 도시 지역의 구매 패턴이 바뀌면서 2023년에는 유기농 농지가 18% 확대되어 240만 헥타르에 달했습니다. 상하이와 심천의 유기농 채소 소매가격이 200-300% 높아지면서 높은 투입비용이 정당화되었고, 생물 자극제는 인증기준에 부합하는 영양 보충 도구로 자리매김하고 있습니다. E-Commerce 플랫폼에서는 추적성을 중시하는 밀레니얼 세대와 Z세대 소비자를 중심으로 유기농 농산물의 매출이 전년 대비 40% 증가했다고 보고되고 있습니다. 국가 유기농 표준 GB/T 19630의 의무적 준수에 따라 생산자들은 합성 비료를 바이오 유래 재료로 대체할 수밖에 없었고, 신선 및 가공 부문 전반에 걸쳐 생물 자극제에 대한 수요가 지속되고 있습니다. 지속적인 도시화로 소비자 기반이 확대되고, 선호도가 구조적인 시장 수요로 전환되고 있습니다.

일반적인 생물 자극제의 가격은 화학 비료의 2-5배에 달하며, 아미노산 제품은 복잡한 가수분해 공정과 수입 원료로 인해 높은 가격대를 형성하고 있습니다. 평균 0.6헥타르의 소규모 농가는 예산의 유연성이 제한되어 있고, 농가 소득이 해안 지역보다 40-50% 낮은 서부 지역에서는 보급이 둔화되고 있습니다. 위안화 약세는 수입 원자재 비용을 상승시켜 가격 변동성을 증폭시키는 동시에 유통업체들의 수익률을 압박하고 있습니다. 지방정부 차원의 보조금 제도는 부담을 일부 경감시켜 주지만, 적용 범위에 편차가 있어 시장 침투에 불균형을 초래하고 있습니다. 입증된 투자 수익률은 여전히 중요하며, 보급 지도의 부족은 인식의 변화를 지연시키고 가격 상승에 대한 우려를 상쇄할 수 있는 가능성을 가로막고 있습니다.

2025년 기준 해조류 추출물은 중국 생물촉진제 시장 점유율의 38.15%를 차지했습니다. 이는 산동성의 재배부터 추출까지 일관된 생산 클러스터가 물류비용 절감과 신선도 확보를 실현한 것이 그 기반이 되었습니다. 이 카테고리는 중국의 전통적인 다시마 소비 문화와 일치하는 해양 유래 재료에 대한 소비자 선호에 따른 혜택을 누리고 있습니다. 해조류 추출물의 중국 생물촉진제 시장 규모는 가공업체들이 효소 보조 추출 라인을 업그레이드하고, 사이토키닌 및 옥신 농도를 높임으로써 꾸준히 확대될 것으로 예상됩니다. 아미노산은 수익 기반이 작지만 정밀 시비 관리를 통한 수확량 반응이 두드러지는 온실 채소 분야를 견인하며 2031년까지 CAGR 13.09%로 성장할 것으로 예상됩니다. 휴믹산과 펄빅산은 흑룡강성 및 내몽골자치구의 토양개량 프로그램으로부터 안정적인 수요를 얻고 있습니다. 단백질 가수분해물은 품질 프리미엄을 추구하는 과수원과 베리 농장에서 틈새시장을 형성하고 있습니다. 신생 키토산 및 미생물 컨소시엄 제품은 향후 성장을 위한 규제 경로가 확립되기를 기다리면서 시험 단계의 파일럿 테스트를 진행 중입니다.

아미노산 제조업체는 발효기술에 대한 투자를 통해 생산의 현지화를 진행하여 수입 깃털 분말 기질의 의존도를 낮추고 있습니다. 청도씨윈바이오텍그룹은 다단계 효소 라인을 출시하여 처리 시간을 25% 단축하고 유리 아미노산 함량을 향상시켜 엽면 영양제 제품의 차별화를 꾀했습니다. 경쟁 심화에 따라 2선급 제조업체는 연안 가공업체와 OEM 제휴를 추진하여 원료 조달력과 전국적인 판매망을 상호 활용하고 있습니다. 디지털 플랫폼의 통합 확대로 정밀 시비가 가능해지면서 화학비료에 대한 부가가치 인식이 높아져 단계적 프리미엄 가격 유지를 뒷받침하고 있습니다.

중국 생물촉진제 시장 보고서는 형태별(아미노산, 풀빅산, 휴믹산, 단백질 가수분해물, 해조류 추출물 등) 및 작물 유형별(원예작물, 밭작물 등)로 분류됩니다. 시장 예측은 금액(달러) 및 미터톤으로 제공됩니다.

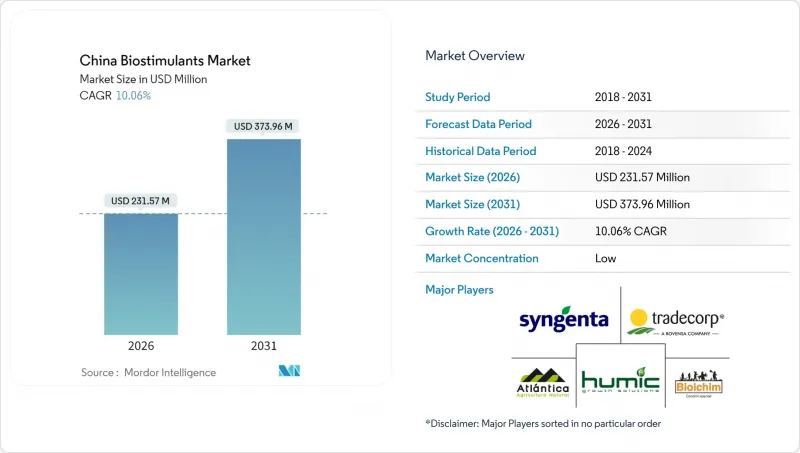

China biostimulants market size in 2026 is estimated at USD 231.57 million, growing from 2025 value of USD 210.4 million with 2031 projections showing USD 373.96 million, growing at 10.06% CAGR over 2026-2031.

Accelerated policy support for fertilizer-use efficiency, a robust protected-horticulture footprint, and a nationwide push for smart agriculture create favorable demand conditions. Seaweed extract leadership, rising amino-acid adoption in greenhouses, and soil-health degradation mitigation need further reinforcement. Competitive differentiation centers on quality assurance, raw-material integration, and digital application guidance. Intensifying patent filings and foreign direct investment signal an innovation-driven growth path that aligns with China's dual goals of food-security resilience and ag-input emission reduction.

New ecological-protection compensation rules implemented in 2024 reimburse 30%-50% of biostimulant costs in eco-sensitive zones, closing price gaps with bulk fertilizers. Streamlined registration now completes within 12 months, accelerating market entry for compliant formulations. National carbon-neutrality commitments elevate biostimulants as low-emission substitutes for urea and compound fertilizers. Provincial pools totaling CNY 15 billion (USD 2.1 billion) per year provide concessional loans and tax credits that reduce working-capital stress for retailers and large farms. Parallel research grants foster domestic innovation that tailors products to China's diverse soils, reinforcing local manufacturing competitiveness.

Organic farmland expanded 18% in 2023 to 2.4 million hectares as food-safety concerns reshape urban purchasing patterns. Retail premiums of 200%-300% on organic vegetables in Shanghai and Shenzhen justify higher input costs, positioning biostimulants as certification-compliant nutrition tools. E-commerce platforms reported 40% year-over-year organic sales growth, led by millennial and Generation Z consumers who value traceability. Mandatory adherence to national organic standard GB/T 19630 forces growers to substitute synthetic fertilizers with bio-derived inputs, sustaining biostimulant demand across fresh and processed segments. Continuous urbanization widens the consumer base, converting preference into structural market demand.

Typical biostimulant prices exceed chemical fertilizers by two to five times, with amino-acid products at the upper band due to complex hydrolysis processes and imported substrates. Smallholder farmers averaging 0.6 hectares show limited budget flexibility, dampening uptake in western provinces where farm incomes trail coastal counterparts by 40%-50%. Yuan depreciation inflates costs for imported raw materials, amplifying volatility and compressing distributor margins. Province-level subsidy programs partially alleviate burdens but vary in coverage, creating uneven market penetration. Demonstrated return on investment remains critical, lack of extension training slows perception shifts that could offset sticker-shock concerns.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Seaweed extracts held 38.15% of the China biostimulants market share in 2025, anchored by Shandong's integrated cultivation-to-extraction clusters that lower logistics costs and assure freshness. The category benefits from consumer preference for marine-derived inputs aligned with China's traditional kelp consumption culture. The China biostimulants market size for seaweed extracts is forecast to expand steadily as processors upgrade enzyme-assisted extraction lines to boost cytokinin and auxin concentrations. Amino acids, while representing a smaller revenue base, post a 13.09% CAGR through 2031, fueled by greenhouse vegetables where precision fertigation magnifies yield responses. Humic and fulvic acids enjoy stable demand from soil-remediation programs in Heilongjiang and Inner Mongolia. Protein hydrolysates attract niche demand in fruit orchards and berry plantations that seek quality premiums. Emerging chitosan and microbial consortium products occupy pilot-stage trials, pending regulatory pathways that can unlock future growth.

Amino-acid manufacturers invest in fermentation technologies to localize production, trimming dependency on imported feather meal substrates. Qingdao Seawin Biotech Group unveiled a multi-phase enzymatic line that cuts processing time 25% and raises free-amino-acid content, differentiating its foliar nutrient range. Competitive intensity prompts tier-two players to pursue OEM partnerships with coastal processors, cross-leveraging raw-material access and nationwide distributor networks. Wider digital-platform integration enables precise dosing, enhancing perceived value relative to fertilizers and supporting gradual premium retention.

The China Biostimulants Market Report is Segmented by Form (Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts, and More) and Crop Type (Horticultural Crops, Row Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).