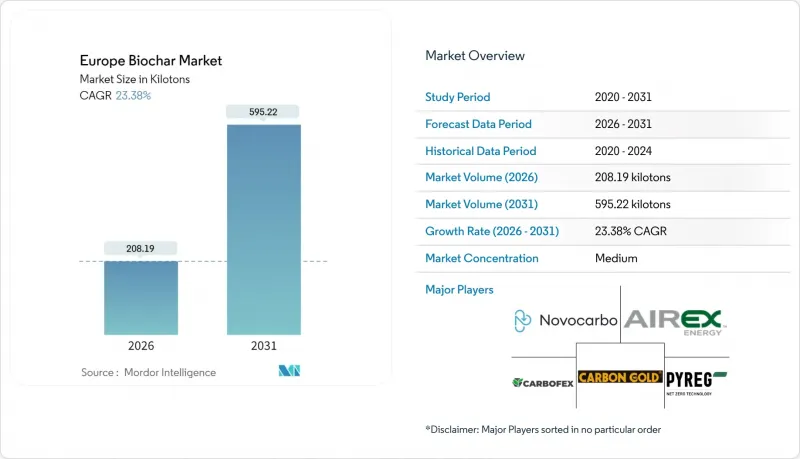

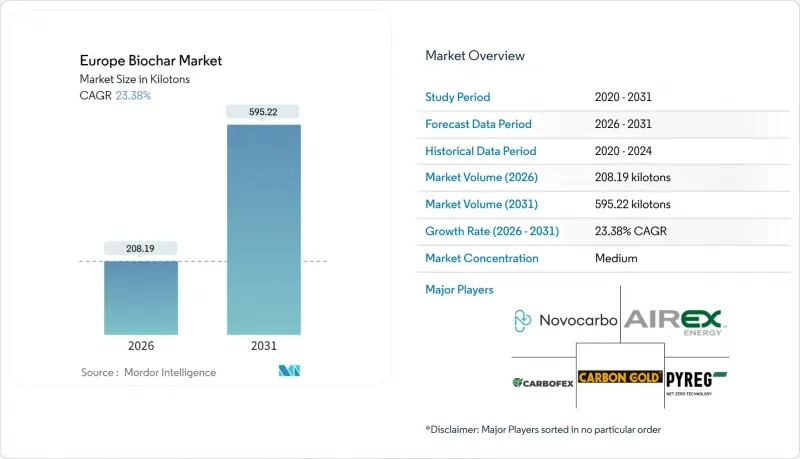

유럽의 바이오차 시장 규모는 2026년에 208.19킬로톤으로 추정되고 있습니다.

이는 2025년 168.77킬로톤에서 성장한 수치이며, 2031년에는 595.22킬로톤에 달할 것으로 예측됩니다. 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 23.38%를 나타낼 것으로 예측됩니다.

유럽연합(EU)이 탄소제거 인증 프레임워크(Carbon Removal Certification Framework)에서 바이오차을 공인된 탄소제거 경로로 규정하는 한편, 비료 제품 규정(Fertilising Products Regulation)의 CMC14 분류로 인해 으로 인해 품질의 모호성이 해소되고, 국경을 초월한 거래가 가능해지면서 수요가 증가하고 있습니다. 철강업체에서 지방 상수도 유틸리티자에 이르는 산업 바이어들은 신규 생산 능력을 보장하는 다년 계약을 체결하고 있으며, 투자자들은 지역난방용 열분해 플랜트를 열과 탄소배출권을 모두 수익화할 수 있는 이중 수익 자산으로 보고 있습니다. 독일은 60개 이상의 상업용 플랜트, 인증된 생산 프로토콜, 재생 가능 열 네트워크와의 긴밀한 협력으로 29.41%의 물량 점유율로 선두를 달리고 있습니다. 그러나 분산된 바이오매스 물류와 EU 전역의 농학적인 밭 적용률 가이드라인의 부재로 인해 비용 경쟁력과 농장 도입을 저해하고 있으며, 원료의 집적화와 농업 기준의 조화가 필요함을 강조하고 있습니다.

2023-2027년 공동농업정책(CAP)에 근거한 유럽연합의 친환경 계획은 탄소 고정 관행에 대한 농가에 대한 보상을 실시하고 있으며, 바이오차도 그 대상에 포함되었습니다. 네덜란드의 온실 재배 농가는 정밀 시비 관리와 바이오차을 결합한 결과, 토마토 생산에서 최대 20%의 수확량 증가를 기록하여 고부가가치 원예 분야로의 보급을 촉진하고 있습니다. 독일의 유기농 농지(국내 농지의 10.20%)에서는 순 제로 목표 달성과 토양 비옥도 유지를 위해 인증된 바이오차을 사용하고 있습니다. 기존 보조금 제도와의 정책 연계를 통해 생산자 수익 안정화, 변동성이 큰 탄소배출권 가격에 대한 의존도 감소. 이를 통해 꾸준한 도입량 확대가 가속화되고 있습니다. 회원국들이 농촌 개발 예산을 탄소농업에 투자하는 가운데, 유럽의 바이오차 시장은 주류 농업 프로그램을 통해 예측 가능한 수요 창출 효과를 얻고 있습니다.

2024년 탄소배출권 인증 프레임워크가 가동된 이후, 바이오차 크레딧(CO2 제거 인증서로 발행)은 기업의 지속가능성 회계에서 표준화된 회계처리 방식을 획득했습니다. 북유럽 기업들은 다년간의 인증 제거량 계약을 체결하고 있으며, ECOERA와 같은 생산자에게는 공장 확장을 뒷받침할 수 있는 확실한 수익 전망을 제공합니다. 유기탄소 비율 0.3 미만을 검증하는 제3자 감사는 지속성 주장을 강화하여 농업용 숯의 2배에 달하는 프리미엄 가격 책정을 가능하게 합니다. 기업 수요의 급증은 신규 열분해 설비의 회수 기간을 단축시키고, 기관투자자의 자본을 유럽의 바이오차 시장에 끌어들여 인증된 공급량을 늘리고 있습니다.

바이오차 원료 네트워크는 통일된 상품 거래소가 아닌 분산된 지역 수집 거점으로 운영되기 때문에 운송 거리가 길어지고, 독일 플랜트용 바이오매스 납품 가격이 25-40% 상승합니다. 소규모 생산자는 장기 계약을 확보할 수 있는 협상 규모가 부족하고, 현물 조달에 의존하는 경우가 많아 영업 이익률에 가격 변동 위험을 초래합니다. 펠릿 부문과 달리 국경을 넘어 통용되는 통일된 등급 기준이나 수분 함량 기준이 존재하지 않아 회원국 간 원료 이동 시 품질 검사를 복잡하게 만들고 있습니다. 중앙집중식 집적 창고와 디지털 추적성 플랫폼에 대한 투자를 통해 물류 비용을 절감할 수 있지만, 이러한 인프라를 구축하기 위해서는 국경을 초월한 정책적 조정이 필요하며, 이러한 노력은 아직 시작에 불과합니다.

2025년 기준 열분해법은 유럽의 바이오차 시장의 74.32%를 차지하고 있으며, 연속 유동 반응기, 자동 온도 제어, 합성가스 회수 기술을 통한 비용 절감에 힘입어 2031년까지 연평균 23.88%의 성장률을 보일 것으로 예측됩니다. 이러한 장점은 CMC14 오염물질 기준을 충족하는 동시에 목재 잔재물, 농작물 짚, 하수 슬러지를 처리할 수 있는 기술의 범용성에 기인합니다. 가스화는 고수분 원료를 위한 소규모 틈새 시장을 차지하고, 열분해와 수열탄화는 활성탄 시장을 위한 특수탄을 공급하고 있습니다.

설비의 경제성은 점점 더 통합적인 에너지 이용에 의존하고 있습니다. 작센 주나 스코네 주와 같이 열분해와 지역난방이 결합된 플랜트에서는 운전 열비용이 마이너스가 되고, 그 절감분을 원료의 전처리에 사용함으로써 전체 탄소 수율을 향상시키고 있습니다. 자동 샘플링과 인라인 분광분석은 배치 간 변동을 감소시켜 산업용 바이어가 요구하는 좁은 기공 크기 분포를 실현하는 데 중요한 요소입니다. 이러한 공정상의 이점은 독일 장비 공급업체의 프리미엄 브랜드 가치를 강화하여 열분해가 유럽의 바이오차 시장 확대의 기반이 될 수 있는 기반을 확고히 하고 있습니다.

유럽의 바이오차 시장 보고서는 기술별(열분해, 가스화 시스템, 기타 기술), 용도별(농업, 축산, 산업용, 기타 용도), 지역별(독일, 영국, 프랑스, 이탈리아, 스페인, 북유럽, 튀르키예, 러시아, 기타 유럽)로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

Europe Biochar Market size in 2026 is estimated at 208.19 kilotons, growing from 2025 value of 168.77 kilotons with 2031 projections showing 595.22 kilotons, growing at 23.38% CAGR over 2026-2031.

Demand rises as the European Union positions biochar as an accredited carbon-removal pathway under the Carbon Removal Certification Framework, while the CMC14 classification inside the Fertilising Products Regulation removes quality ambiguity and opens cross-border trade. Industrial buyers-from steel producers to municipal water utilities-are entering multi-year offtake contracts that underwrite new capacity, and investors view district-heating pyrolysis plants as dual-revenue assets that monetize heat and carbon credits. Germany leads with a 29.41% volume share thanks to more than 60 commercial plants, certified production protocols and close integration with renewable-heat networks. However, fragmented biomass logistics and the absence of pan-EU agronomic field-rate guidelines weigh on cost competitiveness and farm adoption, underscoring the need for tighter feedstock aggregation and harmonized agricultural standards.

European Union eco-schemes inside the 2023-2027 Common Agricultural Policy reimburse farmers for carbon-sequestration practices, and biochar now qualifies for these payments. Dutch greenhouse growers recorded yield gains of up to 20% in tomato production after integrating biochar with precision fertigation, prompting wider adoption across high-value horticulture. Germany's organic acreage-10.20% of national farmland-has embraced certified biochar to maintain soil fertility while meeting net-zero targets. The policy linkage to existing subsidy channels harmonizes revenue for growers and lessens exposure to volatile carbon-credit pricing, accelerating steady volume uptake. As member states earmark rural-development budgets for carbon farming, the Europe biochar market receives predictable pull-through from mainstream agricultural programs.

Since the Carbon Removal Certification Framework became operational in 2024, biochar credits-issued as CO2 Removal Certificates-have gained standardized accounting across corporate sustainability ledgers. Nordic corporates are contracting multiyear tranches of certified removals, giving producers like ECOERA firm revenue visibility that supports plant expansions. Third-party audits that verify H/C_org ratios below 0.3 reinforce permanence claims and enable premium pricing often double that of agricultural-grade char. The surge in corporate demand accelerates payback periods on new pyrolysis assets, drawing institutional capital into the Europe biochar market and lifting credentialed volumes.

Biochar feedstock networks operate through decentralized, regional collection hubs instead of unified commodity exchanges, resulting in transport distances that lift delivered biomass prices by 25-40% for German plants. Smaller producers lack the bargaining scale to secure long-term contracts and often rely on spot sourcing, injecting price volatility into operating margins. Unlike the pellet sector, there is no uniform grading or moisture-content standard recognized across borders, complicating quality checks when material moves between member states. Investment in centralized aggregation depots and digital traceability platforms could compress logistics costs, but such infrastructure requires cross-border policy coordination that remains nascent.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pyrolysis accounted for 74.32% of the Europe biochar market share in 2025, and the pathway is on track for a 23.88% CAGR through 2031 as continuous-flow reactors, automated temperature control, and syngas recovery underpin cost reductions. This dominance stems from the technology's versatility to process wood residuals, crop straw, and sewage sludge while still meeting CMC14 contaminant thresholds. Gasification claims a smaller niche for high-moisture feedstocks, whereas torrefaction and hydrothermal carbonization supply specialty chars for activated-carbon markets.

Unit economics increasingly hinge on integrated energy use. Plants that couple pyrolysis with district-heating, such as facilities in Saxony and Skane, achieve negative operating heat costs and channel savings into feedstock pre-processing, improving overall carbon yields. Automated sampling and inline spectrometry reduce batch-to-batch variability, an essential factor as industrial buyers specify narrow pore-size distributions. These process gains reinforce the premium branding of German equipment suppliers and cement pyrolysis as the backbone of Europe biochar market expansion.

The Europe Biochar Market Report is Segmented by Technology (Pyrolysis, Gasification Systems, Other Technologies), Application (Agriculture, Animal Farming, Industrial Uses, Other Applications), and Geography (Germany, United Kingdom, France, Italy, Spain, Nordic Countries, Turkey, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).