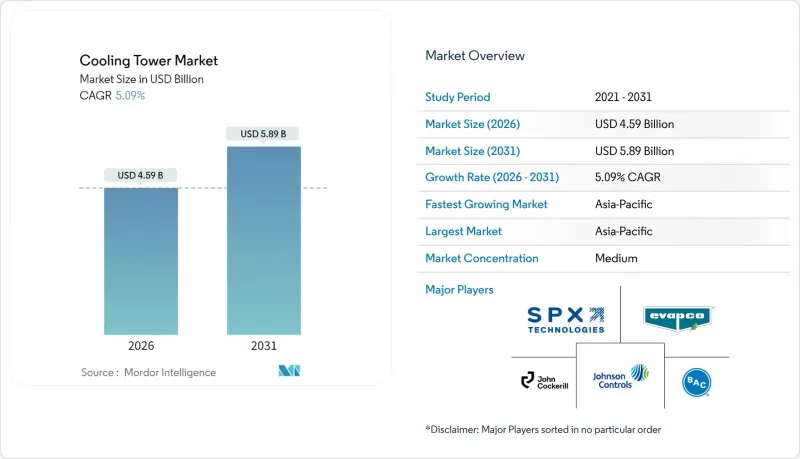

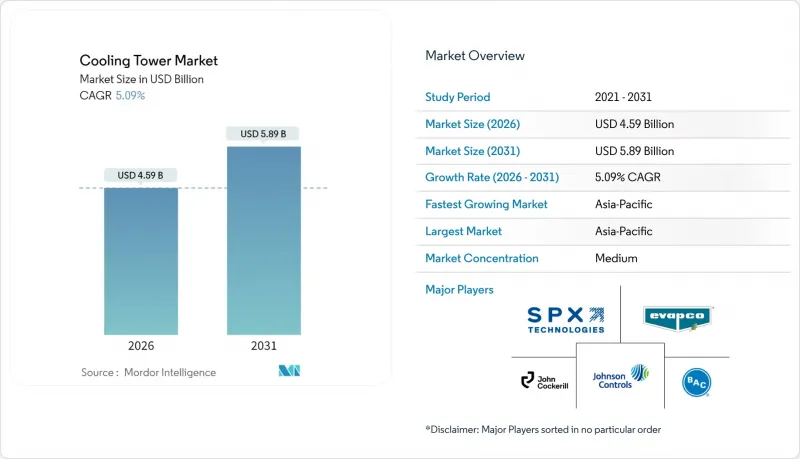

냉각탑 시장 규모는 2026년에는 45억 9,000만 달러로 추정되며, 2025년 43억 7,000만 달러에서 계속 성장하고 있습니다.

2031년에는 58억 9,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 5.09%로 성장할 것으로 전망됩니다.

발전 분야의 지속적인 설비 투자와 하이퍼스케일 데이터센터 시설의 확장으로 고용량 증발 냉각 시스템에 대한 수요는 지속적으로 증가하고 있습니다. 한편, 물 사용 규제 및 에너지 효율 규제 강화에 대응하기 위해 사업자들의 하이브리드형(습식-건식 병용) 설계 도입이 가속화되고 있습니다. 역류형 구성의 채택 가속화, 20MW 이상의 설치 증가, PFAS가 없는 충전재로의 전환은 냉각탑 시장의 성장 궤도를 더욱 강화시키고 있습니다. 디지털 트윈 분석, 예지보전, 대체 급수 체계를 통합할 수 있는 공급업체는 지속가능성에 대한 요구가 높아지는 가운데 실행 측면에서 우위를 점할 수 있습니다.

복합용도 시설과 고사양 데이터센터의 급속한 상용화로 인해 개발업체들은 대용량, 디지털 모니터링이 가능한 증발 냉각식 및 하이브리드 시스템을 지향하고 있습니다. 존슨콘트롤즈는 빌딩 자동화 서버와 연동되는 수요 반응 제어장치를 갖춘 냉각탑을 지정하는 스마트 빌딩 소유주로부터 수주 잔액이 131억 달러에 달한다고 보고했습니다. IoT 센서의 통합은 예지보전 루틴을 실현하고 다운타임을 줄일 수 있습니다. 수자원에 제약이 있는 지역에서는 부하 추종 능력을 손상시키지 않으면서 규제 기준을 충족하기 위해 하이브리드식 습식/건식 복합 유닛의 채택이 증가하고 있습니다. CTI 인증 성능 테스트를 통해 실제 에너지 절감 효과를 입증할 수 있는 공급업체는 부동산 투자자들이 지속가능성 지표를 감사할 때 조달 측면에서 우위를 점할 수 있습니다.

중국, 인도, 걸프 국가의 전력회사들은 변동하는 증기 부하를 관리하기 위해 대용량 역류식 냉각탑이 필요한 원자력, 가스화력, 재생에너지 하이브리드 발전소의 규모 확대를 추진하고 있습니다. 중국의 허시 산업 증기 연계 시스템(허시-1)은 연간 480만 톤의 공정 증기를 공급하고 있으며, 냉각탑을 산업 열회수 루프에 통합하는 것이 상업적 이점이 있음을 입증하고 있습니다. GCC(걸프협력회의) 회원국의 전력회사들은 해안지역 복합화력 발전소에 해수냉각식 냉각탑을 도입하여 담수 취수량을 줄이고, 극한의 외부 온도에서도 40% 이상의 가동률을 달성하고 있습니다. 중동 지역의 태양열 발전 강화 움직임은 향후 탄소 가격제도에 적합한 하이브리드 시스템의 우위를 더욱 높여주고 있습니다.

건조지역에서는 화학약품 처리비용과 폐수처리비용이 전력비용을 초과하기 때문에 총 소유비용이 증가하는 추세입니다. 태평양 북서부 국립 연구소의 사례 연구에 따르면, 군사 시설에서는 에어컨 응축수 및 빗물 회수를 통해 보충수 수요를 줄이고 있지만, 저장 시설 통합에 따른 자본 지출로 인해 투자 회수 기간이 5년을 초과하는 것으로 나타났습니다. 호주, 중동 등 물값이 1,000갤런당 5달러가 넘는 지역에서는 효율성 저하를 감수하고서라도 건식냉각이나 하이브리드 설계를 채택하는 시설이 증가하고 있습니다. 성능 보증과 물 절약 개보수를 결합한 서비스를 제공하는 공급업체는 신규 건설 침체기에 수익 변동을 완화하는 장기 서비스 계약을 체결하고 있습니다.

역류식 냉각탑은 2025년 매출의 43.10%를 차지했으며, 데이터센터 및 제약 고객사들이 높은 L/G 비율과 작은 설치 면적을 선호하는 추세로 인해 CAGR 7.69%로 성장하고 있습니다. 역류 냉각탑과 공정용 냉각기를 결합한 산업용 히트 펌프 프로젝트는 연간 15% 이상의 에너지 절감을 실현하여 식음료 공장의 운영 비용 민감도를 직접적으로 개선할 수 있습니다. 교차 흐름식 냉각탑은 설치 기반의 우위를 유지하고 있으며, 특히 석탄 및 가스 터빈 발전소에서는 낮은 정압 손실이 보조 부하를 줄입니다. 그러나 수도요금의 단계적 인상으로 온도관리가 더욱 엄격해지는 추세에 따라 그 점유율은 감소할 것으로 예상됩니다. 디지털 트윈 시뮬레이션을 통해 예측형 저수관리와 통합할 경우 역류식 설계가 운영비용을 5% 절감할 수 있는 것으로 확인되어 점유율 확대를 더욱 촉진할 것으로 예상됩니다.

기존 크로스 플로우 유닛은 충전재에 쉽게 접근할 수 있고, 넓은 표면적이 먼지를 흡수해도 즉각적인 성능 저하를 일으키지 않기 때문에 리노베이션 용도로 여전히 매력적입니다. 단계적 규제 대응 전략을 추구하는 사업자는 자본적 갱신을 미루기 위해 저 드리프트 제거 장치를 갖춘 크로스 플로우 셀의 개보수를 자주 수행합니다. 그럼에도 불구하고 동남아시아의 신규 산업단지에서는 설계 습구 하강온도 10℃ 이상의 역류식 냉각탑이 표준화되고 있으며, 이러한 구조적 전환은 향후 10년간 제조업체의 제품 포트폴리오를 재구성할 조짐을 보이고 있습니다.

하이브리드(습식/건식 겸용) 모델은 CAGR 8.34%로 확대되고 있으며, 2025년 66.40%의 점유율을 유지할 것으로 예상되는 증발식 냉각탑을 능가하는 성장세를 보이고 있습니다. 물 스트레스 지역의 유틸리티 사업자들은 가뭄 조절 시 건식 모드로 전환되는 하이브리드 설계를 높이 평가하고 있으며, 열적 컴플라이언스를 유지하면서 계절별 취수량을 50%까지 줄일 수 있습니다. 천공식 이슬점 간접증발 모듈의 실지시험을 통해 급기비 0.5 미만에서 최적의 열효율 향상을 달성할 수 있음을 확인하여, 배연처리 개보수 대안으로 하이브리드의 유효성을 확인하였습니다.

증발 냉각탑은 대용량 응용 분야에서 주류입니다. 습식 운전은 습구 온도에서 3℃ 이내의 근접 온도를 달성할 수 있으며, 이는 증기 사이클 효율에 매우 중요합니다. 공급업체는 시장 리스크를 헤지하기 위해 기존 증발식 냉각 탱크에 모듈식 하이브리드 라인을 도입하여 레거시 자산을 효과적으로 전환하고 있습니다. 친수성 멤브레인 충진재 등 재료기술의 발전으로 하이브리드 배출구 온도가 습식 운전 기준치에 근접할 것으로 예상되며, 배연 대책이 필수적인 도심 병원이나 반도체 공장 등에서의 경쟁이 치열해지고 있습니다.

냉각탑 시장 보고서는 유량 유형(횡류식 및 역류식), 탑 유형(증발식, 건식, 하이브리드식), 용량 범위(5MW 미만, 5-20MW, 20MW 이상), 용도별(석유/가스, 화학/석유화학, 발전, HVACR, 데이터센터, 펄프/제지, 식음료, 기타), 지역별(북미, 아시아, 유럽, 아시아태평양, 남미, 중동, 아프리카, 유럽, 일본, 중국, 일본, 한국, 인도, 중국, 일본, 대만, 태국, 베트남, 태국, 필리핀, 인도네시아, 태국, 말레이시아, 필리핀, 인도네시아, 베트남, 태국, 필리핀, 태국, 인도네시아, 필리핀, 베트남, 태국, 필리핀, 인도네시아, 필리핀, 태국, 베트남, 필리핀, 태국, 필리핀, 필리핀, 베트남, 태국, 필리핀, 태국, 필리핀, 베트남, 필리핀, 태국, 필리핀, 필리핀, 필리핀, 태국, 베트남, 필리핀, 태국, 필리핀 북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류됩니다.

아시아태평양은 냉각탑 시장의 43.70%를 차지하고 있으며, 중국과 인도의 전력, 석유화학, 데이터센터 인프라에 대한 동시 다발적인 투자를 배경으로 6.78%의 CAGR로 성장할 것으로 예상됩니다. 중국의 원자력 증기열병합발전 모델은 산업 탈탄소화 목표와 공정열 최적화를 결합한 이 지역의 통합적 접근방식을 구현하고 있습니다. 인도에서는 취수 강도를 제한하는 국가 물 기준안을 준수하기 위해 화력발전소 개보수 시 하이브리드 냉각탑의 채택이 증가하고 있습니다.

북미에서는 버지니아, 텍사스, 태평양 연안 북서부를 중심으로 집적된 데이터센터 확장 수요가 주를 이루며, 정유소 개보수를 통한 PFAS계 충진재 제거가 진행되고 있습니다. ASHRAE와 EPA의 엄격한 가이드라인으로 인해 CTI 인증을 받은 저 드리프트 셀을 조달하는 경향이 더욱 강화되고 있습니다. 유럽에서는 독일과 스칸디나비아의 지역 에너지 계획에서 수자원 관리와 계절적 부하변동의 균형을 맞추기 위해 하이브리드식 습식-건식 복합 냉각탑이 채택되어 완만한 성장세를 유지하고 있습니다. 아프리카 지역에서는 담수 부족이 제로 폐수 사이클에 대한 수요를 견인하는 가운데, 태양열 발전 및 해수담수화 복합시설에 부수되는 해수냉각식 및 건식 냉각탑의 도입이 증가하고 있습니다. 남미의 성장은 브라질 광산지역과 아르헨티나 대두 가공기지에 집중되어 있으며, 모두 높은 분진 및 변동부하에 대응하기 위해 20MW 이상의 역류식 냉각탑을 채택하고 있습니다. 이러한 지역별 동향은 서로 다른 기후와 규제 환경에도 불구하고 냉각탑 시장의 회복력을 뒷받침하고 있습니다.

Cooling Tower Market size in 2026 is estimated at USD 4.59 billion, growing from 2025 value of USD 4.37 billion with 2031 projections showing USD 5.89 billion, growing at 5.09% CAGR over 2026-2031.

Continued capital formation in power generation and the build-out of hyperscale data-center campuses keep high-capacity evaporative systems in demand, while hybrid wet-dry designs scale faster as operators react to tightening water-use and energy-efficiency regulations. The accelerated adoption of counter-flow configurations, growth in installations exceeding 20 MW, and the shift to PFAS-free fill materials further reinforce the cooling tower market's growth trajectory. Suppliers capable of integrating digital twin analytics, predictive maintenance, and alternative make-up-water schemes hold an execution edge as sustainability mandates intensify.

The rapid commercialization of mixed-use complexes and high-specification data centers is driving developers toward higher-capacity, digitally monitored evaporative and hybrid systems. Johnson Controls reported a USD 13.1 billion order backlog as smart-building owners specify cooling towers equipped with demand-responsive controls that synchronize with building automation servers. The integration of IoT sensors enables predictive maintenance routines that reduce downtime. Projects in water-stressed localities are increasingly selecting hybrid wet-dry units to meet compliance thresholds without compromising load-following capability. Suppliers that can validate real-world energy savings through CTI-certified performance testing gain a procurement advantage when property investors audit sustainability metrics.

Utilities in China, India, and the Gulf states are scaling nuclear, gas-fired, and renewable-hybrid plants that require high-capacity counter-flow towers to manage variable steam loads. China's Heqi-1 industrial steam linkage delivers 4.8 million tonnes of process steam annually, underscoring the commercial benefits of integrating cooling towers into industrial heat-recovery loops. GCC utilities adopt seawater-cooled towers at coastal Combined Cycle Gas Turbine sites, reducing freshwater withdrawal and enabling capacity factors above 40% in extreme ambient temperatures. The Middle East's move toward solar-thermal augmentation further positions hybrid systems as compliance-ready for future carbon pricing schemes.

The total cost of ownership is rising because chemical conditioning and discharge fees now exceed electricity costs in many arid markets. Pacific Northwest National Laboratory case studies show that military installations are lowering makeup water demand by recovering HVAC condensate and rainwater; however, capital outlays for integrated storage push payback periods beyond five years. Facilities in Australia and the Middle East, where water charges exceed USD 5 per 1,000 gallons, are increasingly justifying dry cooling or hybrid designs despite efficiency penalties. Suppliers that bundle performance guarantees with water-saving retrofits secure longer-term service contracts that smooth revenue volatility during new-build lulls.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Counter-flow installations captured 43.10% of the revenue in 2025 and are growing at a 7.69% CAGR, as data-center and pharmaceutical clients prioritize high L/G ratios and smaller footprints. Industrial heat-pump projects that couple counter-flow towers with process chillers deliver annual energy savings of over 15%, directly improving OPEX sensitivity in food & beverage plants. Cross-flow towers retain an installed-base advantage, particularly at coal and gas turbines, where low static-pressure drops ease auxiliary load. However, their share is expected to erode as water tariff escalators favor a more stringent approach to temperature control. Digital twin simulations confirm that counter-flow designs can cut operating cost by 5% when integrated with predictive reservoir management, further propelling share gains.

Legacy cross-flow units remain attractive for retrofit because fill packs are more accessible, and large surface areas accommodate fouling without immediate performance loss. Owners pursuing phased compliance strategies often refurbish cross-flow cells with low-drift eliminators to postpone capital replacement. Even so, new industrial complexes in Southeast Asia are standardizing counter-flow towers sized for a design wet-bulb depression of more than 10 °C, signaling a structural pivot that will reshape manufacturer product portfolios over the decade.

Hybrid wet-dry models are advancing at an 8.34% CAGR, outpacing evaporative towers, which are expected to hold a 66.40% share in 2025. Utilities in water-stressed areas appreciate hybrid designs that switch to dry mode during drought restrictions, maintaining thermal compliance while cutting seasonal water draw by 50%. Field trials of perforated dew-point indirect evaporative modules confirm that supply-air ratios below 0.5 achieve optimal thermal efficiency gains, positioning hybrids as viable replacements for plume-abatement retrofits.

Evaporative towers dominate high-capacity applications because wet operation achieves approach temperatures within 3 °C of the wet-bulb temperature, which is crucial for steam-cycle efficiency. Suppliers hedge market risk by launching modular hybrid lines that retrofit onto evaporative basins, effectively transforming legacy assets. Material advances such as hydrophilic membrane fill promise to push hybrid outlet temperatures closer to wet operation benchmarks, intensifying competition for urban hospitals and semiconductor fabs where plume mitigation is non-negotiable.

The Cooling Tower Market Report is Segmented by Flow Type (Cross-Flow and Counter-Flow), Tower Type (Evaporative, Dry, and Hybrid), Capacity Range (Below 5 MW, 5 To 20 MW, and Above 20 MW), Application (Oil and Gas, Chemical and Petrochemical, Power Generation, HVACR, Data Centers, Pulp and Paper, Food and Beverage, and Others), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa).

The Asia-Pacific region commands 43.70% of the cooling tower market and is expected to grow at a 6.78% CAGR, driven by synchronized investments in power, petrochemical, and data center infrastructure across China and India. China's nuclear-steam cogeneration model exemplifies the region's integrated approach, combining industrial decarbonization targets with process heat optimization. India's thermal power refurbishments increasingly specify hybrid towers to conform with draft national water norms that cap withdrawal intensity.

North America registers demand primarily from data-center expansions clustered in Virginia, Texas, and the Pacific Northwest, paired with refinery retrofits to remove PFAS-based fill. Stringent ASHRAE and EPA guidelines further shape procurement toward CTI-certified, low-drift cells. Europe sustains moderate growth as district energy schemes in Germany and Scandinavia adopt hybrid wet-dry towers to balance water stewardship and seasonal load variation. The Middle East and Africa are witnessing a rising uptake of seawater and dry towers attached to solar-thermal and desalination complexes, where freshwater scarcity commands a premium on zero-discharge cycles. South American momentum concentrates in Brazil's mining corridors and Argentina's soy-crushing hubs, both leaning on >20 MW counter-flow towers to handle high dust and variable loading. Collectively, these regional dynamics validate the cooling tower market's resilience across climatic and regulatory mosaics.