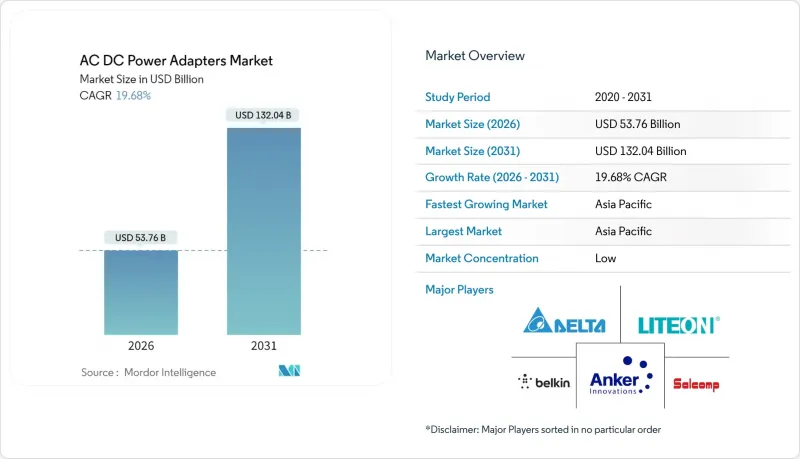

AC/DC 전원 어댑터 시장은 2025년에 449억 2,000만 달러로 평가되었으며, 2026년 537억 6,000만 달러에서 2031년까지 1,320억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 19.68%로 예상됩니다.

USB-C Power Delivery의 표준화, GaN 기술의 급속한 보급, 규제 효율화 요구가 맞물려 이러한 성장 궤도에 박차를 가하고 있습니다. 제조업체는 와트/그램 비율의 향상으로 컴팩트한 멀티 디바이스 충전 설계가 가능해짐에 따라 이점을 얻고 있습니다. 100W 이상의 고출력 부문에서는 기업용 하드웨어 및 EV 인프라가 확장 가능한 솔루션을 필요로 하기 때문에 수익 기반이 확대됩니다. 지속가능성 목표 달성으로 인해 모듈형 어댑터와 회수 프로그램이 가속화되고 있으며, AC-DC 전원 어댑터 시장의 주요 지역에서 컴플라이언스 비용이 브랜드 차별화의 수단으로 전환되고 있습니다.

USB-C PD 3.1은 최대 240W를 지원하여 고성능 노트북 및 산업용 장비의 단일 케이블 충전이 가능합니다. 2024년 12월부터 시행되는 EU의 USB-C 의무화 규정으로 인해 OEM 제조업체는 포트 통일을 해야 하며, 이는 독립형 충전기에 대한 애프터마켓 수요를 확대할 것입니다. IEC 62368-1과 같은 안전 규격도 병행하여 진화하고 있으며, 와트수가 증가해도 고장률을 낮게 유지하고 있습니다. 기업들은 케이블 통합을 통해 작업 공간을 깔끔하게 정리하고 재고 비용을 절감할 수 있는 이점을 얻을 수 있습니다. 이러한 추세는 산업용 제어 장비, POS 키오스크, 의료용 카트 등에도 적용되어 AC-DC 전원 어댑터 시장을 부문 간 전원 공급 생태계에 정착시키고 있습니다.

일반 가정에서는 10년 전만 해도 충전에 의존하는 기기가 3-4대였던 반면, 현재는 7-10대를 관리하고 있습니다. 하이브리드 업무 환경에서는 노트북에 100W 이상을 공급하면서 태블릿과 웨어러블 기기에도 전력을 공급할 수 있는 데스크톱 허브가 요구되고 있습니다. Apple이 iPhone 15 및 16 시리즈에서 USB-C로 전환함에 따라 AC/DC 전원 어댑터 시장의 모든 공급업체가 혜택을 받을 수 있는 액세서리 혁신 주기가 시작되었습니다. AI 지원 노트북은 정상 상태에서의 전력 소비를 증가시켜 140W 어댑터를 틈새 제품에서 주류 선택으로 바꾸어 놓았습니다. 제조업체는 이에 대응하여 열 부하와 휴대성의 균형을 추구한 GaN 충전기를 출시했습니다. 제품 수명 연장과 전자폐기물 문제 완화를 실현하고 있습니다.

EN61204-3 및 FCC 클래스 B 준수는 최대 30kW까지 철저한 방사 및 전도 방출 테스트를 요구하며, 중소기업의 개발 예산의 최대 25%를 흡수할 수 있습니다. 의료용 어댑터는 IEC/EN60601-1의 누설 전류 및 절연 조항을 충족해야 하며, 제품군당 5만 달러 이상의 추가 비용이 발생합니다. 공급 장애 시 빈번한 부품 교체는 전체 재시험 주기를 필요로 하며, 재고 리스크를 발생시킵니다. 대형 브랜드는 일정 단축을 위해 자체 실험실을 정비하고 있으며, AC-DC 전원 어댑터 시장에서 자원 격차가 확대되고 있습니다.

2025년에는 모바일 기기 및 태블릿 분야가 30.78%로 가장 큰 수익을 창출했습니다. 이는 스마트폰의 보급과 태블릿의 보급률 상승에 힘입은 것입니다. 그러나 EV 충전기 어댑터 분야는 2031년까지 22.50%의 CAGR을 기록했으며, 이는 전체 산업 중 가장 높은 수준입니다. 이러한 급격한 성장은 전 세계 충전기 설치 보조금과 자동차 제조업체 간의 상호 운용성 이니셔티브를 반영하고 있습니다. 차량 기지에서는 800V 아키텍처가 채택되어 SiC 정류기가 장착된 견고한 DC-DC 어댑터가 필요하기 때문에 AC-DC 전원 어댑터 시장 규모 내에서 프리미엄 가격대를 형성하고 있습니다. AI 지원 노트북으로의 업그레이드 수요도 수익에 기여하지만, 성장 요인은 유통되는 PC 대수의 증가보다는 대당 와트수 증가에 따른 성장 요인입니다.

자동차와 소비자 디자인의 상호 영향으로 차량용 인포테인먼트 콘솔에 USB-C PD의 도입이 가속화되고 있습니다. 주행거리에 대한 불안감이 줄어들면서 운전자들은 차량 내 장치, 노트북, VR 헤드셋, 냉장 장치 등을 동시에 충전할 수 있기를 기대하며 멀티포트에 대한 수요가 증가하고 있습니다. 산업 자동화 분야는 아직 규모가 작지만, 24시간 가동되는 로봇 기술이 고신뢰성 24V 어댑터의 A/S 수익을 안정적으로 창출하고 있습니다. 로드맵 검증 주기를 자동차 제조업체의 인증 일정과 일치시키는 벤더는 AC-DC 전원 어댑터 시장에서 지속적인 점유율을 확보할 수 있습니다.

16-45W급은 스마트폰과 태블릿 출하량에 힘입어 2025년 매출의 26.39%를 차지했습니다. 그러나 워크스테이션 노트북, 데스크톱 대체 충전기, 휴대용 게임기에 힘입어 101-240W급은 21.95%의 CAGR로 성장할 것으로 예상됩니다. GaN 스위칭 소자의 250% 전력 밀도 향상으로 설치 면적을 줄이면서 효과적인 방열을 실현하고, 공급업체는 크기 증가 없이 가격 프리미엄을 책정할 수 있습니다. 전력 예산이 확대됨에 따라 인덕터 설계 및 게이트 구동 최적화가 AC-DC 전원 어댑터 시장의 주요 차별화 포인트가 될 것입니다.

15W 미만 부문은 무선화 전환과 고효율 SoC의 보급으로 매출 성장이 둔화되고 있습니다. 46-100W 부문은 주류 노트북 생태계의 핵심으로 남아 있지만, 스마트폰, 태블릿, 노트북을 동시에 충전할 수 있는 고출력 어댑터의 시장 잠식에 직면해 있습니다. 기업 IT 구매 담당자들은 책상 위를 깔끔하게 정리하고 다년간의 업데이트 주기를 단축할 수 있는 통합형 240W 도크를 선호하는 경향이 있습니다. 이로써 광대역 갭 칩은 AC-DC 전원 어댑터 시장에서 최첨단 혁신 기술에서 기본 요구 사항으로 전환되고 있습니다.

아시아태평양은 2025년 44.80%의 매출 점유율을 차지했으며, 2031년까지 CAGR 22.35%를 기록할 것으로 전망됩니다. 중국의 수직 통합 공급망이 부품 비용을 낮추는 반면, 대만의 파운더리는 세계 혁신을 뒷받침하는 GaN 에피택셜 웨이퍼를 공급하고 있습니다. 한국의 스마트폰 OEM 업체와 일본의 정밀기기 제조업체가 AC-DC 전원 어댑터 시장의 주도적 지위를 뒷받침하는 견고한 가치사슬을 형성하고 있습니다.

북미 시장에서는 100W 이상의 데스크톱 충전기에 대한 기업 수요 증가와 캘리포니아 및 북동부 지역의 적극적인 EV 인프라 구축이 호재로 작용하고 있습니다. 미국 에너지부(DoE)의 레벨 VI 규제는 에너지 효율이 높은 토폴로지의 조기 채택을 촉진하고 있으며, 포춘지 선정 500대 기업의 조달 정책에도 영향을 미치고 있습니다. 따라서 이 지역은 AC-DC 전원 어댑터 시장에서 고부가가치, 고수익률 설계의 실증장 역할을 하고 있습니다.

유럽에서는 규제의 엄격함과 지속가능성 지향이 결합되어 있습니다. 공통 충전기 지침으로 인해 USB-C의 역내 보급이 가속화되어 PD 호환 충전기에 대한 애프터마켓 수요를 불러일으켰습니다. Tier 2 CoC 효율 규제는 광대역 갭으로의 전환을 촉진하고, 순환 경제법은 모듈형 어댑터와 회수 체계를 장려하고 있습니다. 동유럽의 수탁 제조업체들은 아시아산 제품에 대한 비용 경쟁력 있는 대안으로 시장 점유율을 확대하고 있으며, 이를 통해 세계 AC-DC 전원 어댑터 시장에서 위험을 분산시키고 있습니다.

중동 및 아프리카, 남미 신흥 경제국은 절대적인 수익은 작지만 두 자릿수 성장률을 달성하고 있습니다. 브라질과 아르헨티나는 산업용 어댑터에 의존하는 재생에너지의 통합과 소비자 전자제품 수입을 통해 남미의 확장을 뒷받침하고 있습니다. 걸프협력회의(GCC)의 인프라 구축과 아프리카의 모바일 퍼스트 기술 생태계는 전력망의 불안정성을 견딜 수 있는 견고한 충전기를 필요로 합니다. 현지 전압 표준 및 가격 민감도에 따라 제품을 맞춤화하는 벤더들은 AC-DC 전원 어댑터 시장에 새로운 수요를 창출하고 있습니다.

The AC DC power adapters market was valued at USD 44.92 billion in 2025 and estimated to grow from USD 53.76 billion in 2026 to reach USD 132.04 billion by 2031, at a CAGR of 19.68% during the forecast period (2026-2031).

Standardization around USB-C Power Delivery, rapid GaN adoption, and regulatory efficiency mandates collectively drive this trajectory. Manufacturers benefit from higher watt-per-gram ratios that allow compact, multi-device charging designs. High-power segments above 100 W widen profit pools as enterprise hardware and EV infrastructure demand scalable solutions. Sustainability targets accelerate modular adapters and take-back programs, turning compliance costs into brand differentiation levers across every major region of the AC-DC power adapters market.

USB-C PD 3.1 now supports up to 240 W, enabling single-cable charging for high-performance laptops and industrial equipment. Mandatory USB-C rules in the EU, effective since December 2024, compel OEMs to unify ports, which widens aftermarket demand for standalone chargers. Safety frameworks, such as IEC 62368-1, evolve in parallel, keeping failure rates low even as wattage increases. Enterprises benefit from cable consolidation that reduces workspace clutter and lowers inventory costs. The trend permeates industrial controls, point-of-sale kiosks, and medical carts, entrenching the AC DC power adapters market in cross-sector power-delivery ecosystems.

Households now manage 7-10 charge-dependent devices, up from 3-4 a decade ago. Hybrid work environments require desktop hubs that allocate 100 W or more to laptops while sustaining tablets and wearables. Apple's transition to USB-C across the iPhone 15 and 16 families unlocked accessory refresh cycles that benefit every vendor in the AC DC power adapters market. AI-capable laptops increase steady-state power draw, making 140 W bricks a mainstream option instead of a niche one. Manufacturers respond by releasing GaN chargers that balance thermal load and portability, thereby extending product life and alleviating electronic waste concerns.

EN61204-3 and FCC Class B compliance demand exhaustive radiated and conducted emission tests up to 30 kW, absorbing as much as 25% of engineering budgets for smaller firms. Medical adapters must also satisfy IEC/EN60601-1 leakage and isolation clauses, adding USD 50,000 or more per product family. Component substitutions common during supply disruptions trigger full retest cycles, creating inventory risk. Larger brands internalize labs to shorten schedules, widening the resource gap in the AC-DC power adapters market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The mobile devices and tablets segment generated the largest revenue in 2025, at 30.78%, driven by the ubiquity of smartphones and rising tablet penetration. Still, the EV charging-adapter category is forecast to register a 22.50% CAGR to 2031, the highest among all industries. This leap mirrors global charger-installation subsidies and automaker interoperability initiatives. Fleet depots adopt 800 V architectures that require robust DC-to-DC adapters with SiC rectifiers, creating premium price tiers within the AC DC power adapters market size. Consumers upgrading to AI-ready laptops also add revenue, yet growth stems more from higher wattage per unit than from additional PCs entering circulation.

Cross-pollination between automotive and consumer designs accelerates the deployment of USB-C PD in in-vehicle infotainment consoles. As range anxiety diminishes, drivers expect cabin devices, laptops, VR headsets, and refrigeration units to charge concurrently, elevating multi-port demand. Industrial automation remains a smaller slice, but round-the-clock robotics creates sticky after-sales revenue for high-reliability 24 V adapters. Vendors that align road-map validation cycles with automaker qualification timelines gain a durable share in the AC-DC power adapters market.

The 16-45 W class held 26.39% of 2025 revenue, supported by smartphone and tablet shipments. However, the 101-240 W bracket is projected to clock a 21.95% CAGR, propelled by workstation laptops, desktop replacement chargers, and portable gaming consoles. The 250% power-density gain from GaN switching elements compresses the footprint while dissipating heat effectively, allowing vendors to charge price premiums without incurring size penalties. As power budgets increase, inductor design and gate-drive optimization become key differentiation points in the AC-DC power adapter market.

Below 15 W, wireless substitution and power-efficient SoCs slow revenue expansion. The 46-100 W segment remains core to mainstream laptop ecosystems but faces cannibalization from high-power bricks that simultaneously support phones, tablets, and laptops. Enterprise IT buyers tend to gravitate toward unified 240 W docks, which reduce desk clutter and spark multi-year refresh cycles. Wide-bandgap chips thus transition from a flagship novelty to a baseline requirement in the AC-DC power adapter market.

The AC DC Power Adapters Market Report is Segmented by End-User Industry (Consumer Personal Computers, Laptops, Mobile Devices, and More), Output Power Rating (<=15W, 16-45W, 46-100W, and More), Port Type (Single-Port, and More), Form Factor (Wall Plug Fixed-Pin, Detachable Plug Interchangeable, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held a 44.80% revenue share in 2025 and is forecast to post a 22.35% CAGR through 2031. China's vertically integrated supply chain keeps component costs low, while Taiwan's foundries supply GaN epi-wafers that underpin global innovation. South Korea's smartphone OEMs and Japan's precision engineering firms round out a robust value chain that anchors leadership in the AC-DC power adapter market.

North America follows with strong enterprise uptake of 100 W-plus desktop chargers and aggressive EV infrastructure rollouts in California and northeastern states. DoE Level VI rules push early adoption of energy-efficient topologies that ripple through the procurement policies of Fortune 500 firms. The region thus serves as a proving ground for premium, high-margin designs inside the AC-DC power adapters market.

Europe combines regulatory heft with sustainability orientation. The common-charger directive accelerated the ubiquity of USB-C across the bloc and catalyzed aftermarket demand for PD-compliant chargers. Tier 2 CoC efficiency regulations stimulate wide-bandgap migration, while circular-economy legislation rewards modular adapters and take-back schemes. Eastern European contract manufacturers are gaining market share as cost-competitive alternatives to Asian sources, thereby diversifying risk across the global AC-DC power adapters market.

Emerging economies in the Middle East, Africa, and South America contribute smaller absolute revenue but deliver double-digit growth. Brazil and Argentina anchor South American expansion through consumer electronics imports and renewable energy integrations that rely on industrial-grade adapters. Gulf Cooperation Council infrastructure upgrades and Africa's mobile-first tech ecosystems require ruggedized chargers that withstand grid instability. Vendors tailoring products to local voltage norms and price sensitivities add incremental volume to the AC-DC power adapters market.