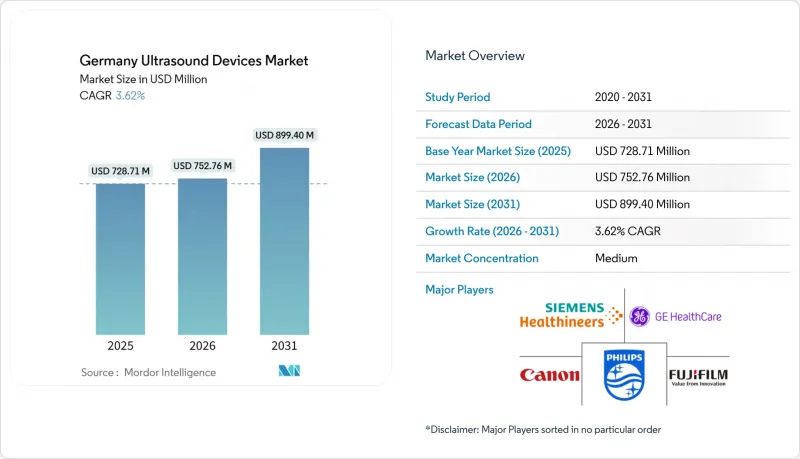

독일의 초음파 진단 기기 시장 규모는 2026년에 7억 5,173만 달러로 추정됩니다.

이는 2025년 7억 2,871만 달러에서 성장한 수치이며, 2031년에는 8억 7,688만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 3.16%로 확대될 것으로 예상됩니다.

이러한 점진적인 확대는 성숙한 병원 인프라, 고령화 인구 증가로 인한 영상 진단 수요 증가, 분산형 의료를 지원하는 휴대용 플랫폼으로의 꾸준한 전환에 기반하고 있습니다. 병원미래법(Hospital Future Act)에 따른 병원 기기 갱신 주기, 현장 초음파 검사에 대한 광범위한 보험 적용, AI를 활용한 자동화가 결합되어 신규 진입자의 가격 압력에 대한 영향을 상쇄하고 있습니다. 의료기기 규제(MDR)의 엄격한 일정은 인증 기간을 연장하는 한편, 신규 진입자의 가격 압력에 직면한 의료 서비스 제공업체들이 보다 새롭고 컴플라이언스가 쉬운 시스템을 우선시하도록 유도하여 수량 성장보다 가치 성장을 유지하도록 유도하고 있습니다. 그 결과, 독일 초음파 기기 시장은 기존의 물량 기반을 강화하는 동시에 종양학 및 심대사 질환의 요구를 충족시키는 첨단 3D/4D 콘솔 및 치료용 HIFU 기기로 축을 옮기고 있습니다.

독일의 65세 이상 인구 비율은 2025년 22%에 달해 심장학, 종양학, 예방적 혈관 검진에서 초음파 검사 건수를 증가시킬 것으로 예상됩니다. 65세 이상 남성을 대상으로 한 복부 대동맥류 검사의 새로운 법정 보험 적용은 이미 연간 혈관 검사 건수를 증가시키고 있으며, 본 대학병원의 임상연구에서 확인된 바와 같이 종양센터에서는 현재 미국 가이드 하 HIFU를 이용하여 수술이 불가능한 췌장 종양을 치료하고 있습니다. 가정의학과 전문의들은 WONCA Europe(유럽가정의학회)의 일차의료 영상 진단 가이드라인을 준수하기 위해 휴대용 프로브를 도입하고 있습니다. 이러한 분산형 스크리닝은 기기의 평균판매가격(ASP)이 하락하는 상황에서도 검사 건수 증가를 지속하고 있습니다. 따라서 이러한 인구 구성의 변화는 다년간의 검사 수요 기반을 뒷받침하고 수입 주도의 가격 하락으로부터 독일 초음파 기기 시장을 보호하는 쿠션 역할을 하고 있습니다.

KHZG(의료 시스템 강화법)에 따른 연방 현대화 보조금이 노후화된 콘솔의 업데이트를 가속화하고 있습니다. 대학병원에서는 지멘스 헬시니어스의 Acuson Sequoia 3.5를 도입하여 복부 장기의 자동 라벨링과 검사 시간 단축을 실현하고 있습니다. 병원들은 경쟁적인 품질 감사에 직면하고 있으며(2024년 유방암 치료 시설의 40.1%가 종양학회 인증을 받지 못했음), 관리자들은 인증을 유지하기 위해 고해상도 3D/4D 플랫폼에 투자하고 있습니다. MDR(의료기기 규정)로 인해 레거시 시스템의 재인증 비용이 증가하여 신규 허가 모델로의 조달을 촉진하고 있습니다. 규제, 자금 조달 및 품질 기준이 결합되어 프리미엄 콘솔을 선호하는 스텝업 사이클을 지원하여 독일 초음파 기기 시장의 평균 판매 가격을 높이고 있습니다.

MDR 완전 적용 후, 인증기관 심사 대기기간이 갱신 시 24개월로 확대되었습니다. MedTech Europe의 조사에 따르면, 50%의 기업이 제품 라인 폐지를 고려하고 있으며, 독일 고유의 MPDG 규정에 따라 현지어 표시 및 추가 시험 모니터링이 의무화되어 있습니다. 이러한 추가 부담은 단가를 상승시켜 중소기업의 진입을 방해하고, 2028년까지 독일 초음파 기기 시장의 총 공급 모델 수를 억제할 수 있습니다.

2025년 기준, 독일 초음파 기기 시장에서 방사선과가 38.72%의 점유율을 차지할 것으로 예상되며, 병원 환경의 종합적인 영상 진단 제품군이 그 기반이 될 것으로 보입니다. 중환자 치료 분야는 현재 구조화된 응급 프로토콜과 초음파 분류와 최종 진단의 높은 상관관계로 인해 5.39%의 CAGR로 가장 빠르게 성장하고 있습니다. 뉘른베르크의 전임상 연구에서 79.5%의 일치율을 확인하여 자금 제공자의 모바일 스캔에 대한 상환을 촉진하고 있습니다. 부인과-산부인과 분야에서는 DEGUM(독일초음파학회)의 개정된 산전 선별검사로 인해 검사 건수가 견조한 증가세를 보이고 있습니다. 한편, 심장학 분야에서는 AI 자동 측정 기술을 통해 생산성이 향상되어 한 번의 초음파 검사로 5,600개의 데이터 포인트를 추가로 획득할 수 있게 되었습니다. 근골격계 및 혈관 영역은 연부조직 및 동맥류 검사의 급여 확대에 따라 외래 진료에서 지속적으로 성장하고 있습니다. 이러한 추세와 함께 수요처의 다변화가 진행되면서 독일 초음파 기기 시장은 단가 하락 압력에 대한 저항력을 유지하고 있습니다.

고령화와 조기 암 검진 정책으로 영상의학과가 주도적인 위치를 유지하는 한편, 응급실에서는 휴대용 스캐너의 도입이 보편화되고 있습니다. 중환자실 의사는 신속한 체액 평가를 위해 초음파를 중시하고, 지방의 중환자실에서는 인력 부족을 보완하기 위해 원격 판독에 의존하고 있습니다. 종양센터에서는 췌장, 전립선 병변에 대한 HIFU 검사를 실시하여 순수 진단을 넘어선 사용 사례를 강화하고 있습니다. 각 응용 분야는 화질, 휴대성, AI 오버레이에 대한 고유한 요구 사항을 요구하기 때문에 공급업체는 제품 라인을 확장하여 병원 및 외래 환경을 가로지르는 독일 초음파 기기 시장 규모의 성장으로 이어졌습니다.

3D/4D 이미징은 고해상도 산부인과, 심장, 복부 검사로 인해 2025년 매출의 44.85%를 차지했습니다. 다음 물결은 비침습적 종양 소작술의 표준 프로토콜이 확립됨에 따라 2031년까지 CAGR 4.92%로 확대될 것으로 예상됩니다. 본 대학병원의 췌장 병변 데이터는 도입 촉진 및 급여 신청 서류의 근거 자료로 활용되고 있습니다. 혈관 매핑에는 도플러 및 조영제 모드가 지속적으로 채택되고 있으며, 지방간 모니터링을 하는 간 클리닉에서는 엘라스토그래피의 채택이 증가하고 있습니다. HIFU의 규제 신청 서류는 유럽에서 축적된 안전성 증거의 혜택을 받아 최초 신청에 비해 의료기기 규정(MDR)의 허들이 완화되었습니다.

치료용 플랫폼은 진단 기기에 비해 평균 판매 가격을 최대 4배까지 끌어올려 독일 초음파 기기 시장 규모에서 가치 성장을 촉진하고 있습니다. 그럼에도 불구하고 예산이 제한적이거나 절차가 표준화된 분야에서는 2D 시스템이 여전히 유용합니다. 벤더는 모듈식 설계를 통해 병원이 기존 콘솔에 HIFU 헤드를 추가할 수 있도록 지원하고 있습니다. 번들 전략은 자본 비용의 급등을 완화하고 업그레이드 경로를 유지함으로써 독일 초음파 기기 시장의 장기적인 수익 안정성을 뒷받침하고 있습니다.

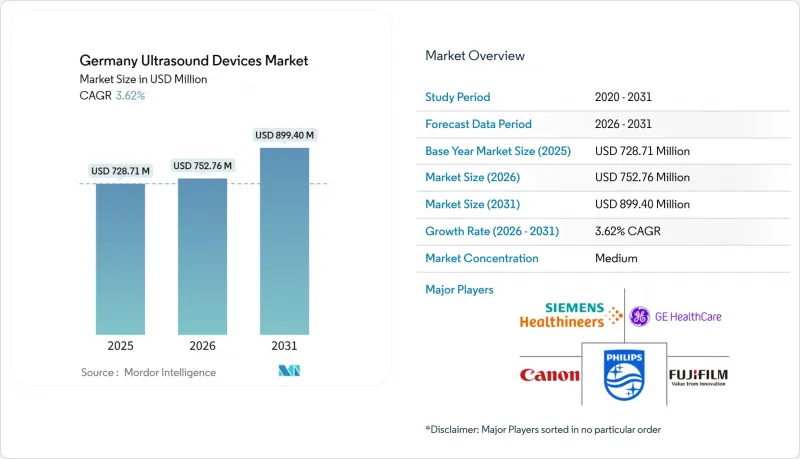

Germany Ultrasound Devices market size in 2026 is estimated at USD 751.73 million, growing from 2025 value of USD 728.71 million with 2031 projections showing USD 876.88 million, growing at 3.16% CAGR over 2026-2031.

This moderate expansion is rooted in the country's mature hospital infrastructure, an aging population that lifts imaging demand, and a steady shift toward portable platforms that support distributed care. Hospital replacement cycles funded through the Hospital Future Act, wider reimbursement for point-of-care ultrasound, and AI-enabled automation all work together to offset pricing pressure from new entrants. Tight Medical Device Regulation (MDR) timelines still lengthen certification but also push providers to favor newer, easier-to-comply systems, keeping value growth ahead of unit growth. As a result, the Germany ultrasound devices market builds on existing volume while pivoting toward advanced 3D/4D consoles and therapeutic HIFU equipment that answer oncology and cardiometabolic needs.

Germany's share of residents aged 65 and above climbed to 22% in 2025, pushing ultrasound volumes in cardiology, oncology, and preventive vascular screening. New statutory coverage for abdominal aortic aneurysm scans in 65-plus men has already lifted annual vascular studies, and oncology centers now employ US-guided HIFU to treat inoperable pancreatic tumors, as confirmed by clinical work at University Hospital Bonn. Family physicians are adding handheld probes to comply with WONCA Europe guidance on primary-care imaging, and these distributed screenings sustain procedure growth even while device ASPs fall. The demographic tilt therefore underwrites a multi-year baseline of examination demand that cushions the Germany ultrasound devices market against import-driven price cuts.

Federal modernization grants under KHZG accelerate replacement of aging consoles. University hospitals deploy Siemens Healthineers' Acuson Sequoia 3.5 units that auto-label abdominal organs and shorten scan times. Hospitals also face competitive quality audits-40.1% of breast-care facilities lacked oncology society certification in 2024-so administrators invest in high-resolution 3D/4D platforms to safeguard accreditation. The MDR makes recertifying legacy systems costly, nudging procurement toward newly cleared models. Together, regulation, funding, and quality benchmarks support a step-up cycle that favors premium consoles and increases the average selling price within the Germany ultrasound devices market.

After full MDR application, notified-body queues grew to 24 months for renewals. A MedTech Europe survey found 50% of companies planning to drop product lines, and German-specific MPDG rules add native-language labeling and extra trial oversight. These overheads raise per-unit costs, discourage SME entrants, and could suppress the total available models on the Germany ultrasound devices market until 2028.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Radiology owned 38.72% of the Germany ultrasound devices market in 2025, anchored by comprehensive imaging suites in hospital settings. Critical care now advances fastest at 5.39% CAGR, fueled by structured emergency protocols and a high correlation between ultrasound triage and final diagnosis. Pre-hospital studies in Nuremberg registered a 79.5% match rate, convincing funders to reimburse mobile scans. Gynecology and obstetrics keep volumes brisk under updated DEGUM prenatal screening, while cardiology gains productivity from AI auto-measurements that add 5,600 datapoints during a single echo session. Musculoskeletal and vascular niches continue to grow in outpatient clinics, riding reimbursement expansion for soft-tissue and aneurysm screening. Collectively, these trends diversify demand sources and help the Germany ultrasound devices market remain resilient to unit price compression.

Aging demographics and early cancer detection policies keep radiology dominant, yet every emergency department now budgets for handheld scanners. Critical care physicians value ultrasound for rapid fluid assessment, and rural ICUs depend on remote read-outs to compensate workforce gaps. Oncology centers test HIFU on pancreatic and prostate lesions, reinforcing therapeutic use cases that extend beyond pure diagnostics. Each application cluster lays unique requirements on image quality, portability, and AI overlay, encouraging vendors to broaden their line-ups and thereby grow the Germany ultrasound devices market size across hospital and ambulatory environments.

3D & 4D imaging delivered 44.85% of 2025 revenue thanks to high-resolution obstetric, cardiac, and abdominal studies. The next wave belongs to HIFU, projected to expand 4.92% CAGR through 2031 as consensus protocols emerge for non-invasive tumor ablation. University Hospital Bonn's data on pancreatic lesions lead adoption and support reimbursement dossiers. Doppler and contrast-enhanced modes persist for vascular mapping, while elastography gains traction in liver clinics monitoring steatosis. Regulatory dossiers for HIFU benefit from accumulated European safety evidence, easing MDR hurdles relative to first-time submissions.

Therapeutic platforms raise average selling prices up to fourfold versus diagnostic units, enhancing value growth within the Germany ultrasound devices market size. Even so, 2D systems stay relevant where budgets are tight or procedures standardized. Vendors answer by modular designs that let hospitals add HIFU heads to existing consoles. Bundle strategies soften capital cost spikes and keep upgrade paths open, supporting long-run revenue stability within the Germany ultrasound devices market.

The Germany Ultrasound Devices Market Report is Segmented by Application (Anesthesiology, Cardiology, Gynecology/Obstetrics, Musculoskeletal, Radiology, and More), Technology (2D Ultrasound Imaging, 3D & 4D Ultrasound Imaging, and More), Portability (Stationary Systems, and More), and End User (Hospitals, Diagnostic Centers, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).