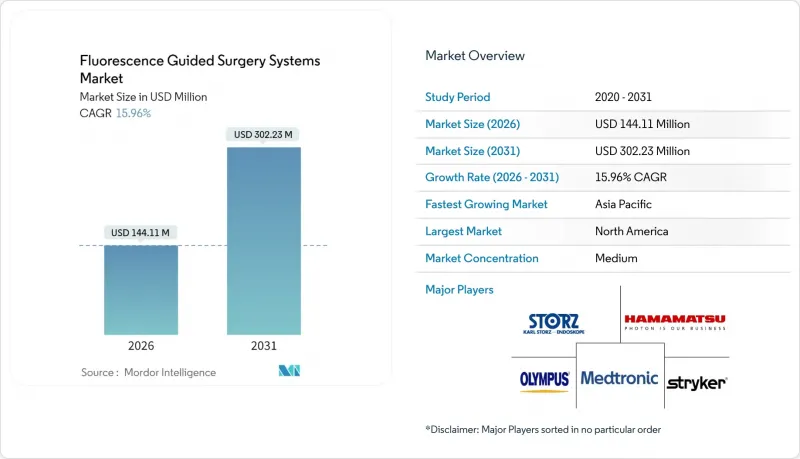

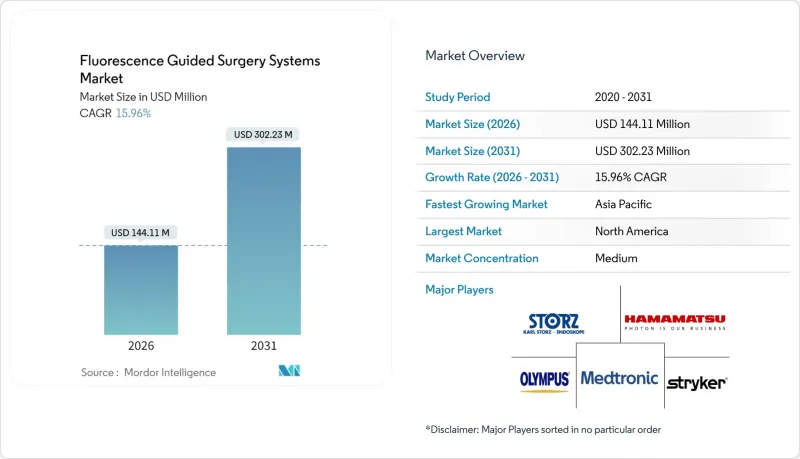

형광 유도 수술 시스템 시장 규모는 2025년 1억 2,427만 달러에서 2026년 1억 4,411만 달러에 달할 것으로 예측됩니다.

2031년까지 3억 2,230만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 15.96%의 연평균 복합 성장률(CAGR)로 확대될 것으로 전망됩니다.

종양학, 이식 및 혈관 수술에서 실시간 조직 식별에 대한 강력한 수요로 인해 첨단 광학 스택에 대한 자본 지출이 증가하고 있습니다. 여러 형광증백제를 동시에 표시하는 멀티 스펙트럼 플랫폼이 기술 혁신을 주도하는 한편, 로봇 시스템과의 통합으로 최소침습 수술실에서의 도입이 가속화되고 있습니다. 북미지역은 초기 FDA 승인과 병원 투자 사이클에 힘입어 현재 선두를 유지하고 있으며, 아시아태평양은 급증하는 수술 건수와 인프라 구축으로 인해 가장 빠른 성장세를 보이고 있습니다. 경쟁 우위는 현재 생태계의 깊이에 따라 좌우되고 있으며, 이미징 기술, AI 후처리, 시술 특화형 색소를 결합한 벤더가 시장에서 인지도를 얻고 있습니다. 데이터에 따르면 재수술률 감소와 수술 시간 단축이 나타났음에도 불구하고, 비용 장벽과 상환제도의 격차가 여전히 지역 의료기관에서의 도입을 저해하고 있습니다.

세계적으로 수술 건수는 지속적으로 증가하고 있으며, 종양 절제술과 혈관 재건술은 기술적으로 더 높은 수준의 요구사항을 수반하고 있습니다. 외과의사는 백색광만으로는 얻을 수 없는 절제된 가장자리와 중요한 혈관의 정밀한 경계 묘사가 필요합니다. 형광 유도 수술 시스템은 실시간 스펙트럼 대비를 제공하여 양성 절제율과 예기치 않은 개복 수술을 줄입니다. 2024년 유방 부분 절제술에서 페글리시아닌의 FDA 승인은 표준 절제술 후 7.6%의 환자에서 잔존 병변을 검출할 수 있는 것으로 나타나 이 치료법의 유효성을 입증했습니다. 병원들은 형광 기술을 재수술 비용 절감과 마취 시간 단축을 위한 품질 향상 수단으로 인식하고 도입에 박차를 가하고 있습니다.

2023년부터 2024년까지 발표된 동료평가 연구에 따르면, 림프종 환자에서 83.3%의 성공률로 인도시아닌그린을 이용한 림프절 생검을 시행한 결과, 심각한 합병증은 발견되지 않았습니다. 이식팀은 레이저 스펙클 콘트라스트 이미징이 초기 이식편 기능과 상관관계가 있음을 보여줌으로써 보다 광범위한 관류 분석의 길을 열었습니다. 형광 유도 수술 시스템 시장은 외과 학회를 통해 치료 결과 데이터가 유통되고, 가이드라인을 업데이트하고, 자본 예산이 영상 진단 장비 업그레이드에 투입되는 혜택을 누리고 있습니다.

고급 카메라 타워는 10만 달러를 초과 할 수 있으며, 케이스 당 색소 비용은 지속적인 지출이 될 수 있습니다. 소규모 시설에서는 더 저렴한 핸드헬드 장비가 등장할 때까지 구매를 미루고 있습니다. NICO의 2024년 핸드헬드 제품 출시는 이러한 구매층을 타겟으로 하고 있습니다. 벤더 파이낸싱과 종합적인 서비스 계약이 도움이 되고 있지만, 가격은 여전히 형광 유도 수술 시스템 시장의 장벽으로 작용하고 있습니다.

2025년 기준, 인도시아닌그린(ICG)의 보급으로 근적외선 방식은 형광 유도 수술 시스템 시장의 71.25%를 차지할 것으로 예측됩니다. 공급업체들이 고감도 센서를 추가함에 따라,이 부문은 여전히 업그레이드 수요가 발생하고 있습니다. 한편, 멀티 스펙트럼/하이브리드 솔루션은 19.05%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있으며, 전체 모달리티 중 가장 높은 성장률을 보이고 있습니다. 단일 프레임 내에서 하나의 색소로 종양을, 다른 색소로 신경을, 또 다른 색소로 혈류를 시각화할 수 있어 생존율을 좌우하는 절제 경계선 판단이 중요한 복잡한 절제 수술에서 외과의사의 관심을 끌고 있습니다. 이 하이브리드 분야의 형광 유도 수술 시스템 시장 규모는 승인된 염료 증가와 워크플로우의 성숙에 따라 2031년까지 두 배로 증가할 수 있습니다. 가시광 형광은 틈새 영역에서 유용성을 유지하고 있으며, 예를 들어 5-ALA 유도하 교모세포종 수술에서 외과 의사는 진홍색 형광을 악성 조직 식별 지표로 활용하고 있습니다.

액세서리 및 소모품은 염료 판매와 일회용 클립 마커를 통해 안정적인 수익을 창출합니다. 2024년 발표된 범암 색소는 향후 질환별 시약 파이프라인이 구축되어 설치되는 카메라마다 지속적인 수익원을 창출할 수 있는 가능성을 시사하고 있습니다.

타워형 카트는 고출력 조명과 GPU급 처리 능력을 겸비하고 기존 수술실 모니터에 연결할 수 있어 2025년 매출의 53.35%를 차지했습니다. 그러나 내시경 내 NIR 센서가 내장된 통합형 로봇팔은 17.95%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 외과 의사들은 콘솔의 조작을 중단하지 않고 풋 페달로 백색광과 형광을 원활하게 전환할 수 있다는 점을 높이 평가했습니다. 휴대형 스코프는 휴대성이 최우선인 위성 수술실이나 외상 치료실에 대응합니다. 2023년 기록된 형광 클립 네비게이션 장치는 저렴한 비용으로 도입을 실현합니다. 가격에 민감한 의료 기관이 도입 곡선에 합류함에 따라 휴대용 형광 유도 수술 시스템 시장 규모는 계속 확대될 것입니다.

북미는 2025년 매출의 37.60%를 차지했습니다. 루미사이트의 FDA 승인과 유연한 상환 시범사업이 선도적 지위를 유지하고 있습니다. 미국의 통합 의료 네트워크는 구매를 통합하고, 여러 시설에서 도입할 수 있도록 하고 있습니다. 캐나다와 멕시코는 증가하는 로봇 수술 시스템에 대응하기 위해 형광증백제 공급업체 도입을 추진하고 있습니다.

아시아태평양은 18.12%의 가장 빠른 CAGR을 기록했습니다. 중국의 정밀 수술 계획과 3차 병원 건설이 대량 주문의 기반이 되고 있습니다. 수술 중 형광 이미징에 관한 논문은 현재 간, 비뇨기, 소화기 코호트에 걸쳐 있습니다. 일본과 한국은 성숙한 로봇의 기준선을 가지고 있으며, 보다 하이엔드급 하이브리드 스코프를 채택하고 있습니다. 인도의 민간 병원 체인은 종양의 가장자리 진단을 위한 휴대용 기기를 평가했습니다.

유럽은 독일의 대학병원과 NHS가 당일 수술로의 전환을 추진하고 있는 것을 배경으로 견고한 점유율을 유지하고 있습니다. 프랑스와 이탈리아 그룹은 새로운 안료에 대한 다기관 시험을 주도하고 공급업체의 증거 자료를 뒷받침하고 있습니다. 중동의 걸프협력회의는 주요 센터에 프리미엄 스위트룸을 설치했지만, 아프리카의 일부 지역은 자본 부족으로 인해 지연되고 있습니다. 남미에서는 브라질이 암 센터를 위한 형광 모듈에 투자하고 있으며, 아르헨티나는 이식 관류 이미징을 위한 보조금을 확보하고 있습니다. 전반적으로 형광 유도 수술 시스템 시장 채택은 로봇의 보급률 및 염료의 가용성과 밀접한 관련이 있습니다.

Fluorescence guided surgery systems market size in 2026 is estimated at USD 144.11 million, growing from 2025 value of USD 124.27 million with 2031 projections showing USD 302.23 million, growing at 15.96% CAGR over 2026-2031.

Strong demand for real-time tissue discrimination in oncology, transplantation, and vascular procedures is lifting capital spending on advanced optical stacks. Multispectral platforms that show several fluorophores at once are pacing innovation, while integration with robotic systems is accelerating adoption in minimally invasive suites. North America holds the lead today, buoyed by early FDA clearances and hospital investment cycles, yet Asia-Pacific's fast-growing surgical volumes and infrastructure upgrades give it the steepest trajectory. Competitive positioning now hinges on ecosystem depth: vendors that pair imaging, AI post-processing, and procedure-specific dyes are capturing mindshare. Cost barriers and reimbursement gaps still curb uptake in community institutions even though data show lower re-operation rates and shorter theater time.

Worldwide procedure counts continue to climb, while tumor resections and vascular reconstructions are becoming more technically demanding. Surgeons need precise delineation of margins and critical vessels that white light alone cannot supply. Fluorescence guided surgery systems market systems deliver real-time spectral contrast, shrinking positive-margin rates and unplanned conversions. FDA clearance of pegulicianine for breast lumpectomy in 2024 validated the modality and showcased detection of residual disease in 7.6% of patients after standard excision. Hospitals now view fluorescence as a quality-improvement lever that can trim re-operation costs and shorten anesthesia time, reinforcing procurement momentum.

Peer-reviewed studies in 2023-2024 found indocyanine-green lymph node biopsy success in 83.3% of lymphoma cases without major complications. Transplant teams showed laser speckle contrast imaging correlates with initial graft function, paving a path for broader perfusion analytics. The fluorescence guided surgery systems market benefits when outcome data circulate through surgical societies, prompting guideline updates that pull capital budgets toward imaging upgrades.

Advanced camera towers can top USD 100,000 and per-case dye costs add recurrent expense. Smaller centers delay purchases until cheaper handheld units appear; NICO's 2024 handheld launch targets these buyers. Vendor financing and bundled service contracts are helping, yet price remains a gating factor for the fluorescence guided surgery systems market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Near-infrared modalities held 71.25% of fluorescence guided surgery systems market share in 2025 thanks to indocyanine-green ubiquity. The segment still garners upgrades as vendors add higher sensitivity sensors. Multispectral/Hybrid solutions, however, are sprinting at 19.05% CAGR, the swiftest among all modalities. They can reveal tumors with one dye, nerves with another, and perfusion with a third in a single frame. This captures surgeon mindshare in complex resections where decisive margins dictate survival odds. Fluorescence guided surgery systems market size for this hybrid slice could double by 2031 as more dyes win approval and workflows mature. Visible fluorescence retains niche relevance, for example 5-ALA-guided glioma surgery, where surgeons rely on crimson cues to distinguish malignant tissue.

Accessories & consumables generate predictable revenue through dye sales and disposable clip markers. A pan-cancer dye published in 2024 hints at a future pipeline of disease-specific reagents that will attach annuity streams to every installed camera.

Tower-based carts secured 53.35% of 2025 revenues because they combine high-power illumination and GPU-grade processing while plugging into legacy OR monitors. Yet integrated robotic arms embedding NIR sensors inside endoscopes are climbing at 17.95% CAGR. Surgeons appreciate seamless foot-pedal switching between white light and fluorescence without breaking console focus. Handheld scopes address satellite theaters and trauma bays where portability is king; fluorescent clip navigation devices documented in 2023 provide low-overhead entry. The fluorescence guided surgery systems market size tied to handhelds will keep rising as price-sensitive centers join the adoption curve.

The Fluorescence Guided Surgery Systems Market Report is Segmented by Type (Near-Infrared (NIR) FGS Systems, Visible Fluorescence FGS Systems and More), Platform (Tower-Based (Cart), and More), Surgery Type (Open Surgery, and More), Application (Cardiovascular & Peripheral Vascular and More), End User (Community Hospitals and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 37.60% of 2025 revenue; FDA approvals of Lumisight and flexible reimbursement pilots sustain leadership. U.S. integrated delivery networks consolidate purchasing, enabling multi-site roll-outs. Canada and Mexico are onboarding dye suppliers to match rising robotic fleets.

Asia-Pacific posts the fastest 18.12% CAGR. China's precision-surgery agenda and tertiary-hospital build-out underpin bulk orders; intraoperative fluorescence imaging papers now span hepatic, urologic, and GI cohorts. Japan and South Korea possess mature robotic baselines and adopt higher-end hybrid scopes. India's private hospital chains are evaluating handhelds for oncologic margins.

Europe maintains solid share on the back of Germany's university hospitals and the NHS push toward day-case pathways. French and Italian groups spearhead multicenter trials on new dyes, anchoring vendor evidence dossiers. The Middle East's Gulf Cooperation Council installs premium suites in flagship centers, whereas parts of Africa lag due to capital scarcity. In South America, Brazil invests in fluorescence modules for cancer centers while Argentina secures grants for transplant perfusion imaging. Overall, fluorescence guided surgery systems market adoption correlates tightly with robotic penetration and dye availability.