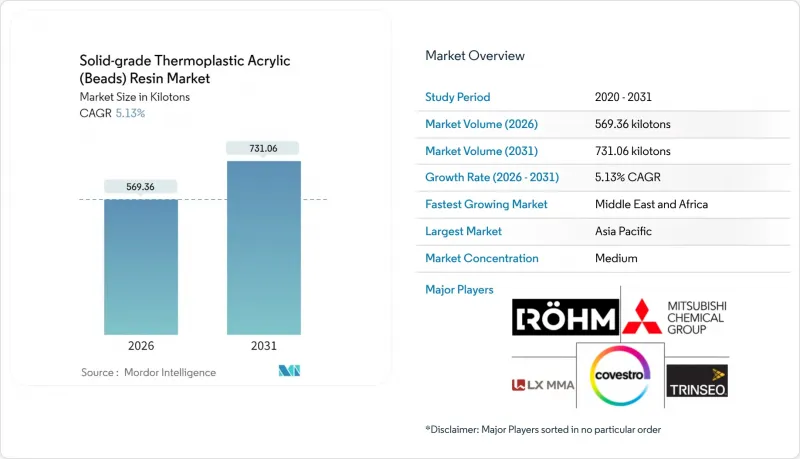

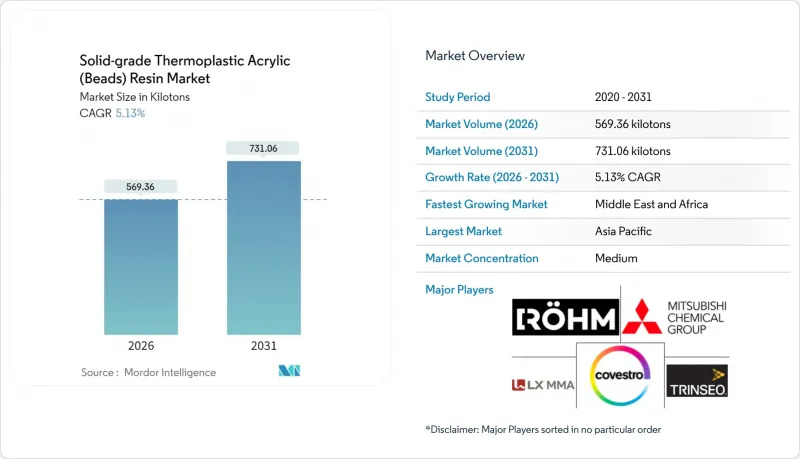

솔리드 등급 열가소성 아크릴(비드) 수지 시장 규모는 2026년에 569.36 킬로톤에 이를 것으로 예측되고 있습니다.

2025년 541.59kg톤에서 2031년에는 731.06kg톤에 달할 것으로 예상되며, 2026-2031년 연평균 5.13%의 연평균 복합 성장률(CAGR)로 확대될 것으로 전망됩니다.

이러한 꾸준한 성장은 자동차 산업의 경량화 요구, 분체 코팅으로의 전환 증가, 대기 오염 규제가 코팅, 복합재, 3D 프린팅의 밸류체인 전반에 걸쳐 조달 결정을 재구성하고 있음을 반영합니다. Tier 1 자동차 공급업체들은 광학 투명성을 유지하면서 차량 무게를 줄이는 투명 PMMA 조명 모듈에 대한 노력을 기울이고 있으며, 아시아태평양 및 북미에서의 인프라 투자는 신뢰할 수 있는 최종 용도의 기반이 되고 있습니다. MMA 원료 가격의 지속적인 변동이 생산자의 수익률을 시험하는 한편, 순환형 및 재생 등급에 대한 다운스트림 수요가 스미토모화학 등 기업의 탈중합 기술에 대한 투자를 가속화하고 있습니다. 용제 배출 규제와 마이크로비드 규제 강화를 배경으로 차별화된 아크릴 비드 화학기술이 평가받는 가운데, 유럽과 미국의 종합 제조업체들이 생산능력을 증강하고 일본의 기존 업체들이 철수하고 중국 업체들이 생산량을 늘리는 등 경쟁 환경이 변화하고 있습니다.

아시아태평양의 지속적인 인프라 투자로 인해 가혹한 기후 조건과 도시 오염에 견딜 수 있는 고성능 아크릴 도료에 대한 수요가 증가하고 있습니다. 중국의 급속한 도시화는 페인트에 대한 견고한 수요로 인해 공급 부족을 야기하고 있습니다. 북미에서는 미국 대기 정화법의 시행으로 인해 배합업체들이 점도 제어 및 광택 유지를 위해 비드 등급 아크릴에 의존하는 수성 또는 고형분 시스템으로 전환하고 있습니다. 이 두 대륙의 동시 수요 급증은 다년간의 갱신 주기를 지속하면서 고체 등급 열가소성 아크릴(비드) 수지 시장의 성장을 견인하고 있습니다. 실란트, 엘라스토머 페인트 등 건설용 화학제품은 아크릴 비드 수요의 2차적인 흐름을 형성하고 있지만, 생산능력 증설이 수요 증가를 따라잡지 못하고 있어 2025년과 2026년에도 공급측의 가격 유지 태세가 유지될 것으로 예측됩니다.

전동화 목표에 따라 자동차 제조업체들은 안전성과 디자인을 해치지 않으면서 차량 중량을 줄여야 한다는 압박을 받고 있습니다. 스미토모화학의 화학적 재생 PMMA는 이미 LG디스플레이와 닛산자동차에 채택되어 폐쇄형 지속가능성 모델로의 전환을 상징하고 있습니다. 에보닉의 프로토타입 PMMA 전면 유리는 유리 대비 경량화를 실현하여 투명 PMMA 구조 부품의 광범위한 채택을 예고하고 있습니다. ADAS 센서 하우징, 고급 라이트 가이드, 발광 배지 등의 융합으로 인해 자동차용 고체 등급 열가소성 아크릴 수지(비드) 수요는 기본 예측치를 상회하는 성장을 지속하고 있습니다. 2024년 말 유럽의 일시적인 수요 감소로 MMA 가격은 완화되었지만, 경량화라는 근본적인 요구는 재료과학 예산을 아크릴 솔루션으로 끌어들이는 추세가 계속되고 있습니다.

프로파일렌 가격 변동과 예상치 못한 크래커 가동 중단은 MMA 가격 급등과 직결되어 수지 제조업체의 수익률을 압박합니다. 미국 현물 MMA 가격은 2024년 4월에 급등한 후 다운스트림 수요 둔화에 따라 조정 국면에 접어들었습니다. 한편, 중국의 수출량은 거의 두 배로 증가하여 아시아 계약 가격에 새로운 압력을 가하고 있습니다. 이에 따라 구조조정이 진행되었습니다. 스미토모화학은 싱가포르 MMA 공장을 중단하고, 미쓰비시화학은 루이지애나주의 신규 프로젝트를 동결했습니다. 이러한 움직임은 고체 등급 열가소성 아크릴(비드) 수지 시장에서 원료 가격의 불안정성이 확장 경제성에 미치는 취약성을 강조하고 있습니다.

페인트 및 코팅 분야는 2025년 고체 등급 열가소성 아크릴(비드) 수지 시장에서 52.74%를 차지했습니다. 이는 건축, 산업 및 보수 도장 분야에서 이 소재의 확고한 입지를 반영합니다. 비드 등급 아크릴은 고광택, 내스크래치성 필름을 실현하고, VOC 규제를 충족하는 분체 도장의 기반이 됩니다. 이 부문은 아시아태평양에서 동시에 진행되는 인프라 구축, 고성능 방수재에 대한 높은 수요, 그리고 분체 코팅의 세계적인 보급으로 인해 수혜를 받고 있습니다. 빠르게 도시화되는 경제권에서 에너지 절약형 건축용 코일 코팅에 대한 수요는 고체 등급 열가소성 아크릴(비드) 수지 시장 규모 확장을 꾸준히 견인하고 있습니다.

경량 구조 부품용 아크릴 복합수지는 2031년까지 연평균 복합 성장률(CAGR) 5.62%로 확대될 성장 동력입니다. 자동차 전조등 렌즈, 미등 하우징, 가전제품에는 투명성과 내충격성을 겸비한 PMMA 블렌드가 활용되고 있습니다. UV 경화형 코팅은 전자기기 및 자동차 내장재용 급속 경화 솔루션을 제공함으로써 기존의 부문 경계를 모호하게 만들고 있습니다. 접착제 및 실란트 분야는 내후성, 내화학성을 갖춘 비드 등급 수지를 활용하여 성장률은 완만하지만 안정적인 수익원을 형성하고 있습니다. VOC(휘발성 유기 화합물) 및 미세 플라스틱에 대한 규제가 강화됨에 따라, 배합 기술자들은 지속가능성을 유지하면서도 내구성을 확보하기 위해 혁신적인 고체 등급 열가소성 아크릴 수지(비드) 시장 솔루션에 의존하고 있습니다.

고체 등급 열가소성 아크릴(비드) 수지 시장 보고서는 용도별(아크릴 복합수지, 페인트/코팅, 기타 용도), 최종 이용 산업별(건축/건설, 자동차/운송, 기타), 배합별(솔벤트 기반, 수성, 고형분, UV 경화형), 지역별(아시아태평양, 기타)로 세분화되어 있습니다. 세분화되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

2025년 아시아태평양은 세계 총량의 44.90%를 차지했습니다. 이는 중국의 인프라 붐, 일본의 전자산업, 한국의 자동차 수출에 힘입은 것입니다. 국내 MMA 가격은 공급 부족 속에서도 상승하며 물류 혼란 속에서도 시장의 회복력을 입증했습니다. 여러 중국 제조업체들이 2027년까지 공급 병목현상 해소를 위한 MMA/PMMA 신규 생산능력 증설 계획을 발표했지만, 실제 생산량은 세계 수요 동향에 따라 달라질 수 있습니다. 인도에서는 진행 중인 고속도로 건설과 저가 주택 정책이 비드 등급 아크릴 도료의 새로운 수요 창출의 원천이 되고, 아세안 국가에서는 공장 이전 흐름이 건설 및 가전제품 소비를 촉진하는 혜택을 누리고 있습니다.

북미 시장은 주택 건설의 회복과 자동차 제조업체의 전동화 전환으로 인해 계속해서 매력적인 시장입니다. 캘리포니아주의 엄격한 VOC 규제가 고형분 UV 경화형 아크릴 시스템의 조기 도입을 촉진하고, 다른 주에서도 유사한 규제를 도입하면서 대응 가능한 수요 기반이 확대되고 있습니다. 로옴의 텍사스주 베이시티 공장 증설은 공급선 단축과 원자재 리스크 헤지를 위한 전략적 미국 생산 거점 배치의 좋은 예입니다. 캐나다의 페인트 수요는 에너지 절약형 개보수 인센티브와 연동되어 있으며, 멕시코의 니어쇼어링 물결은 가전 및 자동차 부품 공장들이 마감재 및 투명렌즈에 아크릴 수지를 지정하는 것을 촉진하고 있습니다.

유럽의 전망은 복잡합니다. 독일 자동차 산업의 침체로 인해 2024년 수요량이 억제되는 반면, 선진적인 환경 규제로 인해 재활용 바이오 아크릴로의 전환이 가속화되고 있습니다. EU 규정 2023/2055는 화장품 및 산업용 사용자에게 생분해성 비드 대체품 채택을 의무화하여 특수 제품 공급업체에 틈새 성장 기회를 제공합니다. 북유럽 국가들의 지속가능한 건축자재 공공조달로 인해 수성 아크릴 도료의 보급이 진행되고 있습니다. 한편, EU 결속기금의 지원을 받은 동유럽의 인프라 프로젝트가 기준 수요를 뒷받침하고 있습니다. 중동 및 아프리카은 5.42%의 가장 빠른 지역 CAGR을 보이고 있으며, GCC 국가들의 건설 다각화와 아프리카의 도시화가 원동력이 되고 있습니다. 이를 통해 솔리드 그레이드 열가소성 아크릴(비드) 수지 시장에서 아직 초기 단계이지만 점유율을 높여가고 있습니다.

Solid-grade Thermoplastic Acrylic (Beads) Resin Market size in 2026 is estimated at 569.36 kilotons, growing from 2025 value of 541.59 kilotons with 2031 projections showing 731.06 kilotons, growing at 5.13% CAGR over 2026-2031.

This steady growth reflects how lightweighting mandates in the automotive industry, rising powder-coating conversions, and clean-air regulations are reshaping procurement decisions across coatings, composites, and 3D printing value chains. Tier-one automotive suppliers are committing to transparent PMMA lighting modules that cut vehicle weight while maintaining optical clarity, and infrastructure spending across Asia-Pacific and North America remains a dependable end-use anchor. Persistent MMA feedstock volatility tests producer margins, yet downstream demand for circular, recycled grades is accelerating investment in depolymerization technologies by firms such as Sumitomo Chemical. Competitive dynamics are shifting as Western integrated majors add capacity, Japanese incumbents exit, and Chinese firms increase volume, all against a backdrop of tighter solvent-emission and micro-bead limits that reward differentiated acrylic bead chemistries.

Continued infrastructure investment across the Asia-Pacific region elevates demand for high-performance acrylic coatings that can endure extreme weather and urban pollution. China's fast-paced urbanization highlights supply tightness amid robust demand for coatings. In North America, U.S. Clean Air Act enforcement is steering formulators toward waterborne or high-solids systems that rely on bead-grade acrylics for viscosity control and gloss retention. This parallel surge across two continents sustains a multi-year replacement cycle, favoring the expansion of the Solid-grade Thermoplastic Acrylic (Beads) Resin market. Construction chemicals, such as sealants and elastomeric coatings, form a secondary stream of acrylic bead demand, while capacity additions lag behind demand trajectories, preserving price discipline for suppliers in 2025 and 2026.

Electrification goals pressure OEMs to trim vehicle mass without compromising safety or styling. Chemically recycled PMMA from Sumitomo Chemical, already specified by LG Display and Nissan, highlights the pivot toward closed-loop sustainability models. Evonik's prototype PMMA windshield demonstrates savings over glass, foreshadowing the broader adoption of transparent PMMA structural parts. The convergence of ADAS sensor housings, premium light guides, and illuminated badges continues to drive the automotive demand for Solid-grade Thermoplastic Acrylic (Beads) Resin above base-case projections. Temporary demand dips in Europe during late 2024 eased MMA prices; yet, the fundamental lightweighting imperative continues to pull material science budgets toward acrylic solutions.

Propylene cost swings and unplanned cracker outages translate rapidly into MMA price spikes, eroding resin producer margins. U.S. spot MMA surged during April 2024, then corrected as downstream demand cooled, while Chinese export volumes nearly doubled, exerting fresh pressure on Asian contract prices. Structural adjustments followed: Sumitomo Chemical idled Singapore MMA, and Mitsubishi Chemical shelved its Louisiana greenfield project. These moves underscore the vulnerability of expansion economics to feedstock instability in the Solid-grade Thermoplastic Acrylic (Beads) Resin market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Paints and coatings contributed 52.74% to the Solid-grade Thermoplastic Acrylic (Beads) Resin market in 2025, reflecting the material's entrenched position in architectural, industrial, and refinish applications. Bead-grade acrylic enables high-gloss, mar-resistant films and underpins powder coatings that meet VOC regulations. The segment benefits from simultaneous infrastructure buildouts in the Asia-Pacific region, high demand for waterproofing with high performance, and global adoption of powder coating. Coil-coating demand for energy-efficient buildings in rapidly urbanizing economies continues to drive the Solid-grade Thermoplastic Acrylic (Beads) Resin market size expansion at a stable rate.

Acrylic composite resins within lightweight structural parts represent the growth engine for applications, advancing at a 5.62% CAGR through 2031. Automotive headlamp lenses, tail light housings, and appliances exploit PMMA blends that offer clarity and impact resistance. UV-curable coatings blur traditional segment boundaries by providing rapid-cure solutions for electronics and automotive interiors. Adhesives and sealants add a predictable, though slower-growing, revenue stream by leveraging bead-grade resin for weatherability and chemical resistance. As regulatory focus intensifies on VOCs and microplastics, formulators rely on innovative Solid-grade Thermoplastic Acrylic (Beads) Resin market solutions to achieve durability without sacrificing sustainability credentials.

The Solid-Grade Thermoplastic Acrylic (Beads) Resin Market Report is Segmented by Application (Acrylic Composite Resins, Paints and Coatings, and Other Applications), End-Use Industry (Building and Construction, Automotive and Transportation, and More), Formulation (Solvent-Based, Water-Based, High-Solids, and UV-Curable), and Geography (Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific controlled 44.90% of global volume in 2025, powered by China's infrastructure boom, Japan's electronics sector, and South Korea's automotive exports. Domestic MMA prices climbed amid tight supply, validating market resilience even during logistic snarls. Multiple Chinese producers have announced plans to add new MMA/PMMA capacity, aiming to debottleneck the supply by 2027; however, actual output will depend on global demand. India's ongoing highway and affordable housing drives offer fresh outlets for bead-grade acrylic coatings, while ASEAN countries benefit from factory relocation trends that boost construction and appliance consumption.

North America stays attractive as residential construction rebounds and automakers shift to electric drivetrains. California's stringent VOC rules have catalyzed the early adoption of high-solid and UV-curable acrylic systems, and other states have referenced these limits, thereby expanding the establishment of addressable demand. Rohm's Bay City plant lift in Texas exemplifies strategic U.S. capacity placements that shorten supply lines and hedge feedstock risk. Canadian coatings demand tracks energy-efficiency retrofit incentives, whereas Mexico's near-shoring wave spurs appliance and auto-part factories that specify acrylic resins for finishes and transparent lenses.

Europe faces mixed prospects: German automotive weakness has tempered 2024 volumes, yet the continent's advanced environmental regulations are accelerating the pivot to recycled and bio-based acrylics. EU Regulation 2023/2055 requires cosmetic and industrial users to adopt biodegradable bead alternatives, creating niche growth opportunities for specialty suppliers. Nordic public procurement of sustainable building materials boosts the penetration of waterborne acrylic coatings, while Eastern European infrastructure projects supported by EU cohesion funds sustain baseline demand. The Middle East and Africa exhibit the fastest regional CAGR of 5.42%, driven by GCC construction diversification and African urbanization, which is fueling a nascent but rising share of the Solid-grade Thermoplastic Acrylic (Beads) Resin market.