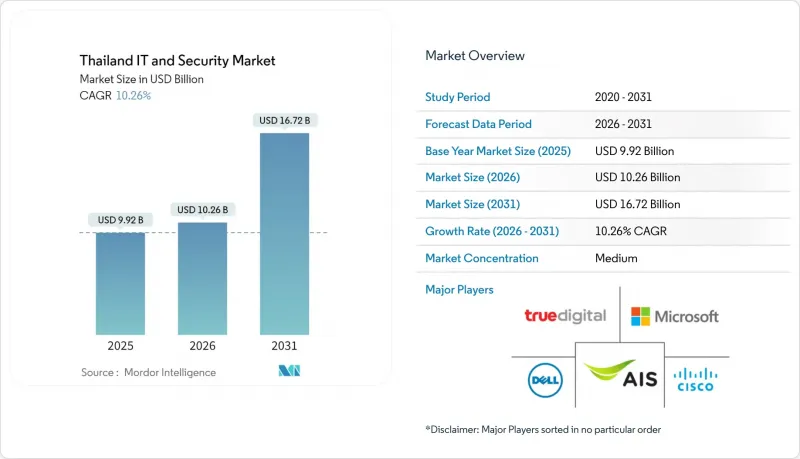

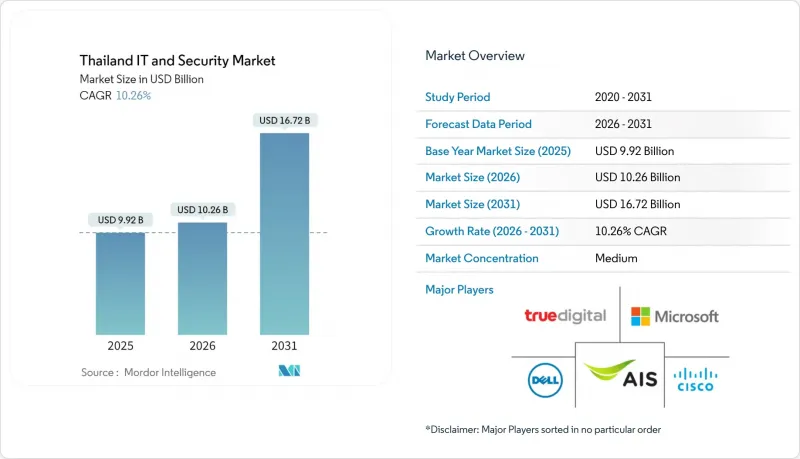

태국의 IT 및 보안 시장은 2025년에 89억 5,000만 달러로 평가되었고, 2026년 102억 7,000만 달러에서 2031년까지 204억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 14.78%로 예상됩니다.

이러한 급격한 성장은 태국이 아세안의 디지털 인프라 허브로 자리매김하고, 공공 부문의 클라우드 우선 정책 추진, 그리고 이미 85억 달러 이상의 하이퍼스케일 데이터센터가 지속적으로 유입되고 있음을 반영합니다. 인구의 95%를 커버하는 강력한 5G 네트워크, 15억 바트의 국가 AI 예산, 그리고 국경 간 전자상거래의 흐름은 엣지부터 클라우드까지 아키텍처 도입을 촉진하고 있습니다. 기업 구매자들은 점점 더 매니지드 서비스를 선호하는 경향이 있습니다. 그 배경에는 국내 3만 명의 사이버 보안 전문가가 부족하고, 새로운 데이터 보호 규정으로 인해 컴플라이언스 지출이 증가하고 있다는 점이 있습니다. DTAC의 경쟁 심화, True Corporation과의 합병으로 인한 네트워크 도달 범위 재편, 그리고 미국 클라우드 제공업체들의 가용성 영역 현지화 경쟁은 경쟁의 격화를 더욱 가속화시키고 있습니다. 이러한 요인들이 결합되어 태국의 IT 및 보안 시장은 향후 10년간 두 자릿수 성장을 유지할 것으로 예측됩니다.

디지털정부개발청은 부처 간 클라우드 도입을 의무화하여 부처별 조달을 해소하고, 보안, 통합, 분석 서비스에서 규모의 경제를 실현합니다. ISO/IEC 27001에 기반한 중앙 집중식 프레임워크는 신규 벤더의 진입장벽을 높이고, 국가사이버보안청과 구글 클라우드의 협력으로 정부 워크로드에 AI 기반 위협 감지 기능을 추가할 수 있게 됩니다. 로컬 클라우드 리전은 데이터 주권에 대한 우려에 대응하고, 각 기관이 하드웨어에서 관리형 플랫폼으로 예산을 전환하면서 태국의 IT 및 보안 시장을 강화하고 있습니다.

어드밴스드 인포 서비스의 95%의 인구 커버리지는 공장, 병원, 물류 거점에서의 저지연 용도를 지원합니다. 동부 경제 회랑의 제조 공장에서는 센서 데이터를 클라우드 AI 엔진으로 스트리밍하여 실시간 품질 관리를 실현하고 있습니다. 한편, 트루코퍼레이션의 '트루사이버세이프'는 모바일 사용자를 위해 하루 10만 건의 위험한 링크를 필터링하고 있습니다. 이를 통해 통신 사업자는 단순한 연결 제공업체에서 엣지 플랫폼 사업자로 진화하여 태국의 IT 및 보안 시장에서 입지를 더욱 강화할 수 있게 되었습니다.

은행은 현재 고급 애널리스트에게 180만 바트(5만 달러)를 지불하고 있지만, 수요는 여전히 공급을 3만 건 이상 초과하고 있습니다. 중소기업은 임금 인플레이션에 대응할 수 없어 프로젝트를 연기하거나 MSSP(Managed Security Service Provider)에 외주화할 수밖에 없습니다. 대학은 커리큘럼을 확대하기 위해 애쓰는 반면, 인재들은 싱가포르의 고임금 직종으로 유출되어 태국의 IT 및 보안 시장의 모멘텀을 떨어뜨리고 있습니다.

2025년 매출에서 서비스 부문이 차지하는 비중은 41.64%로, 기업들은 매니지드 SOC, 위협 헌팅, 통합 솔루션을 선택하고 있습니다. 인력 부족이 지속되는 가운데 태국의 IT 및 보안 서비스 시장 규모는 CAGR 10.55%를 나타낼 것으로 예측됩니다. True Corporation과 같은 통신사업자들은 보안과 연결 서비스를 묶어 고수익 서비스 업셀링을 시도하고 있습니다. 하드웨어 매출은 데이터센터와 5G 네트워크 설비투자로 인해 꾸준히 증가하고 있지만, 상품화가 성장을 억제하고 있습니다. 소프트웨어, 특히 AI 지원 분석은 구독 모델이 예산을 설비투자에서 운영비용으로 전환하기 때문에 가장 빠른 성장률을 기록하고 있습니다.

이러한 구성 비율의 변화는 태국 시장이 하드웨어 중심의 구축에서 소프트웨어 정의 및 서비스 지향 아키텍처로 진화하고 있음을 보여줍니다. 전문 통합업체가 레거시 시스템과 클라우드 API를 연동하는 한편, 벤더는 인력 부족을 보완할 수 있는 자동화 플레이북을 제공합니다. 이러한 전환은 임금 상승 압력에도 불구하고 태국의 IT 및 보안 시장의 효율성을 유지하고 있습니다.

2025년 기준 클라우드는 태국의 IT 및 보안 시장 점유율의 53.12%를 차지하며 16.43%의 연평균 복합 성장률(CAGR)을 유지하며 산업 전반에 걸쳐 도입이 심화되고 있습니다. 하이퍼스케일러는 태국 지역 출시를 통해 데이터 거주지에 대한 우려를 해소하고, 규제 대상 은행들이 핵심 워크로드를 이전할 수 있도록 자신감을 심어주고 있습니다. 국방 및 중요 인프라 분야에서는 On-Premise가 지속될 것이지만, 기업들이 로컬 제어와 탄력적 컴퓨팅을 결합함에 따라 하이브리드 모델이 인기를 끌고 있습니다.

클라우드 보안 기능이 기존 방화벽을 능가하는 경우가 증가하고 있으며, 위험 회피 지향적인 구매 담당자들이 리프트 앤 시프트 계획을 앞당기고 있습니다. 통합의 복잡성이 MSSP 수요를 불러일으키는 한편, SD-WAN이 MPLS를 대체하여 회선 비용을 절감하고 있습니다. 통신 사업자들이 공장이나 병원에 엣지 노드를 구축함에 따라 하이브리드 도입에 따른 태국의 IT 및 보안 시장 규모는 확대될 것으로 예측됩니다.

The Thailand IT and Security market was valued at USD 8.95 billion in 2025 and estimated to grow from USD 10.27 billion in 2026 to reach USD 20.44 billion by 2031, at a CAGR of 14.78% during the forecast period (2026-2031).

This surge reflects Thailand's positioning as ASEAN's digital-infrastructure hub, the public-sector cloud-first mandate, and sustained hyperscale data-center inflows that already top USD 8.5 billion. Robust 5G coverage of 95% of the population, a THB 1.5 billion national AI budget, and cross-border e-commerce flows energize adoption of edge-to-cloud architectures. Enterprise buyers increasingly favor managed services because the country lacks 30,000 cybersecurity professionals, while new data-protection rules elevate compliance spending. The DTAC heightens competitive intensity-True Corporation merger that reshapes network reach, and by U.S. cloud providers racing to localize availability zones. These forces converge to keep the Thailand IT and Security market on a double-digit growth path through the decade.

The Digital Government Development Agency mandates cloud adoption across ministries, dissolving siloed procurement and creating scale for security, integration, and analytics services. Centralized frameworks anchored on ISO/IEC 27001 raise entry barriers for new vendors, while the National Cyber Security Agency's alliance with Google Cloud layers AI-driven threat detection onto government workloads. Local cloud regions address data-sovereignty concerns, bolstering the Thailand IT and Security market as agencies shift budget from hardware to managed platforms.

Advanced Info Service's 95% population coverage underpins low-latency applications in factories, hospitals, and logistics hubs. Manufacturing plants in the Eastern Economic Corridor now stream sensor data to cloud AI engines for real-time quality control, while True Corporation's "True CyberSafe" filters 100,000 risky links per day for mobile users. Telcos thus graduate from connectivity providers to edge-platform operators, deepening their stake in the Thailand IT and Security market.

Banks now pay senior analysts THB 1.8 million (USD 50,000) to secure scarce experts, yet demand still exceeds supply by 30,000 roles. SMEs cannot match wage inflation and therefore defer projects or outsource to MSSPs. Universities scramble to scale curricula, while talent migrates to higher-paying Singapore roles, subtracting momentum from the Thailand IT and Security market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

YServices contributed 41.64% of 2025 revenue as enterprises chose managed SOC, threat-hunting, and integration offerings. The Thailand IT and Security market size for services is projected to climb at a 10.55% CAGR as talent scarcity persists. Telecom operators such as True Corporation bundle security with connectivity to upsell higher-margin offerings. Hardware revenues rise steadily on data-center and 5G network capex, but commoditization caps growth. Software, especially AI-assisted analytics, records the fastest run-rate because subscription models shift budgets from capex to opex.

The mix signals Thailand's evolution from hardware-centric builds to software-defined, service-oriented architectures. Specialized integrators tie legacy systems to cloud APIs, while vendors deliver automated playbooks that offset human shortfalls. This pivot keeps the Thailand IT and Security market efficient even as wage pressure mounts.

Cloud controlled 53.12% of the Thailand IT and Security market share in 2025, and sustained a 16.43% CAGR, indicating deepening adoption across verticals. Hyperscalers neutralize data-residency concerns by launching Thai regions, giving regulated banks confidence to migrate core workloads. On-premises persists in defense and critical infrastructure, but hybrid models gain favor as enterprises pair local control with elastic compute.

Cloud security capabilities now often surpass legacy firewalls, prompting risk-averse buyers to accelerate lift-and-shift roadmaps. Integration complexity fuels MSSP demand, while SD-WAN replaces MPLS to cut circuit costs. The Thailand IT and Security market size attached to hybrid deployments will widen as telcos push edge nodes to factories and hospitals.

The Thailand IT and Security Market Report is Segmented by Component (Hardware and Devices, Software, Services), Deployment Mode (On-Premises, Cloud, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Government and Defense, Manufacturing, Healthcare, Retail and E-Commerce, Energy and Utilities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).