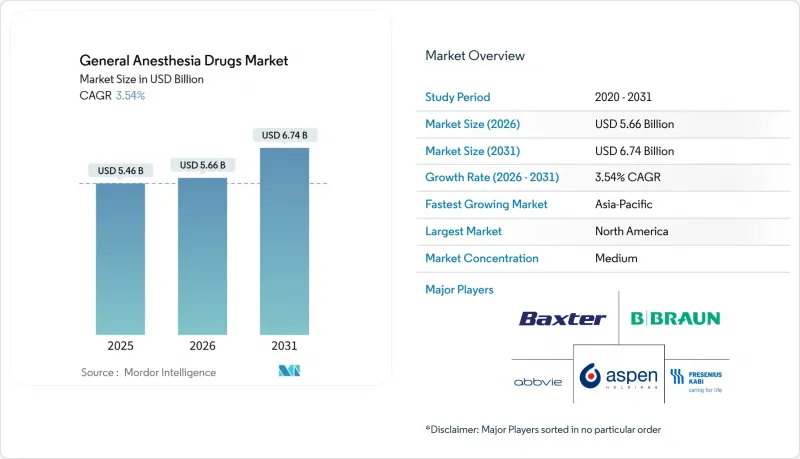

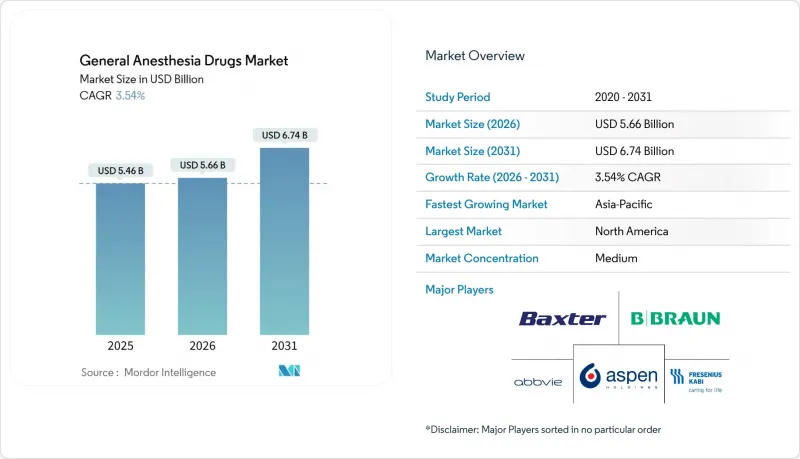

전신 마취제 시장은 2025년 54억 7,000만 달러에서 2026년에는 56억 6,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 3.54%를 기록하며 2031년까지 67억 4,000만 달러에 달할 것으로 예측됩니다.

이러한 꾸준한 확대는 전 세계 수술 건수의 증가, 인공지능을 탑재한 폐쇄 루프 투약 시스템의 보급 확대, 그리고 빠른 회복을 촉진하는 약물을 선호하는 외래 수술 센터의 단계적 확장에 의해 뒷받침되고 있습니다. 병원 관리자들은 환경 목표를 달성하고 환자 처리 능력을 향상시키기 위해 전신정맥마취(TIVA) 프로토콜로의 전환을 가속화하고 있습니다. 한편, 주요 휘발성 약품의 지속적인 부족은 조달 전략에 계속 혼란을 일으키고 있습니다. 시프로폴, 레미마졸람과 같은 새로운 분자가 규제 당국의 승인을 받아 기존 약물의 매출을 잠식하면서 경쟁 환경도 변화하고 있습니다. 이러한 요인들이 복합적으로 작용하여 전신 마취제 시장 전체에서 제제 포트폴리오, 상업적 제휴, 지역별 수요 패턴이 재편되고 있습니다.

시프로폴과 레미마졸람의 신속한 승인으로 마취과 의사의 치료 옵션이 확대되고, 주사 부위 통증 발생률이 77.1%에서 18.0%로 감소했으며, 고령 환자에서 우수한 심혈관계 안정성을 제공하게 되었습니다. 미국 식품의약국(FDA)의 2025년 JOURNAVX(수세트리딘) 승인은 전신마취 프로토콜을 보완하는 비오피오이드 계열의 수술 전후 진통제로의 광범위한 전환을 뒷받침합니다. 2024년 앤닐의 1회용 프로포폴 바이알 출시는 반복되는 공급 부족을 완화하기 위한 것으로, 연간 3억 1,400만 달러의 수익 창출이 예상됩니다. 이번 승인은 전체적으로 효과적인 정맥내 투여 옵션에 대한 선택의 폭을 넓히고, 경쟁을 강화하며, 전신 마취제 시장 전반의 혁신 수준을 높이는 계기가 될 것으로 기대됩니다.

미국 외래 수술 센터(ASC)의 지출은 2022년 330만 명의 메디케어 종량제 서비스 수혜자 대비 61억 달러에 달할 것으로 예상되며, 이 부문의 수익 기반은 2021년 370억 달러에서 2028년까지 590억 달러로 확대될 것으로 예상됩니다. 미국 의료보험 및 의료서비스센터(CMS)가 지원하는 NOPAIN법에 따라 2025년 1월부터 EXPAREL과 같은 비오피오이드 진통제에 대한 독자적인 상환이 허용되어 외래 진료 환경에서 빠른 회복 마취 프로토콜의 경제적 합리성이 더욱 높아질 것으로 보입니다. 이러한 ASC의 확대에 따라 시프로폴과 같은 속효성 약물에 대한 수요가 증가하면서 전신 마취제 시장 전체에서 측정 가능한 판매량 증가를 견인하고 있습니다.

영국 국민보건서비스(NHS)의 데스플루란 단계적 폐지와 유럽위원회의 규제 검토로 지난 10년간 전 세계 흡입 마취제 배출량은 27% 감소했습니다. 동시에 불화수소 방출 위험을 이유로 한 게팅게의 세보플랑 증발기 등 장비 리콜이 잇따르면서 공급망에 대한 압박이 가중되고 있습니다. 이에 따라 병원에서는 재고 확보 및 TIVA(전신 마취제 시장 전체에서 휘발성 매출 성장 둔화)로의 전환이 진행되어 일반마취제 시장 전체에서 휘발성 매출 성장을 둔화시키고 있습니다.

2025년 기준 세보플루란은 전신 마취제 시장 점유율 36.78%를 유지한 반면, 프로포폴은 2031년까지 CAGR 4.65%로 확대될 것으로 예상되며, 이는 TIVA 프로토콜로의 결정적인 전환을 반영하고 있습니다. 프로포폴 제제의 시장 규모는 시프로포올이 비열등성을 보이면서 주사 부위 통증 발생률을 크게 낮추기 때문에 더욱 확대될 것으로 예상됩니다. 덱스플루란은 유럽 내 환경 규제에 따른 판매 금지가 임박함에 따라 여전히 마이너스 성장이 지속될 전망입니다. 반면 덱스메데토미딘과 레미펜타닐은 특정 치료에 특화된 틈새시장을 유지하고 있습니다. 2024년에 발생한 덱스메데토미딘의 규제 판매 중단은 일시적으로 공급을 압박했지만, 장기적인 수요에 큰 변화를 가져오지는 않았습니다. 중국에서 미다졸람에 대한 규제가 강화됨에 따라 유사한 규제 부담 없이 빠른 회복을 제공하는 레미마졸람으로의 전환이 가속화되고 있습니다. 케타민과 에토미데이트는 안정적인 소규모 부문을 유지하고 있으며, 에토미데이트는 정기적인 공급 부족이 있는 것으로, 혈역학적으로 불안정한 경우에 필수적입니다.

환경 규제 강화, 정맥주사제 관련 면역 조절 효과에 대한 관심 증가, AI 기반 수액 펌프의 운영 효율성 등이 촉진요인으로 작용하고 있습니다. 이러한 추세와 함께 정맥 투여로의 전환이 정착되면서 진화하는 전신 마취제 시장에서 프로포폴의 주도적인 역할이 강화되고 있습니다.

2025년 기준 흡입 마취제는 전신 마취제 시장의 58.41%를 차지했지만, 정맥 투여는 5.88%의 CAGR을 보이며 정밀하게 제어된 수액에 대한 선호가 가속화되고 있음을 시사합니다. 정맥내 제품의 전신 마취제 시장 규모는 뇌파(EEG)에 기반한 심도 지표에 따라 용량을 자동 조절하는 폐쇄 루프 시스템의 혜택을 받고 있으며, 이 기능은 휘발성 약물로는 재현할 수 없습니다. 배출량 감축 의무와 할로겐화 가스 공급 불안정으로 인해 병원은 TIVA를 임상적 사치품이 아닌 컴플라이언스 전략으로 포지셔닝해야 할 필요성이 있습니다.

휘발성 가스 회수 기술의 유효 효율은 25-73%에 불과해 본격적인 대책으로서의 실용성에 한계가 있어 간접적으로 정맥투여의 수요 확대를 뒷받침하고 있습니다. 또한, 새로운 임상 연구에 따르면 정맥 마취는 수술 후 메스꺼움(수술 후 구역질) 감소, 인지 기능 회복 촉진, 염증 지표 감소와 관련이 있는 것으로 나타났습니다. 이러한 의료 및 규제적 측면의 호재로 인해 전체 전신 마취제 시장에서 정맥 투여는 흡입 경로를 능가하는 성장세를 이어갈 것으로 예상됩니다.

북미는 2025년 전신 마취제 시장 매출의 37.84%를 차지했으며, 이는 첨단 수술 인프라, AI 기반 투약 시스템의 조기 도입, 지원적인 상환 정책을 반영하고 있습니다. FTC의 미국 마취 파트너스에 대한 소송으로 상징되는 연방정부의 통합 감시가 향후 통합 전략을 억제할 가능성은 있지만, 물량 성장을 저해할 가능성은 낮다고 판단됩니다. 2022년 미국 병원의 78%가 인력 부족을 보고하는 등 인력난이 심각해지면서 의료진의 부담을 안전하게 줄여줄 수 있는 자동화 솔루션에 대한 투자가 가속화되고 있습니다.

아시아태평양은 2031년까지 CAGR 5.19%로 가장 빠르게 성장하는 지역입니다. 수술 건수 증가, 수술실 업그레이드를 장려하는 정부 인센티브, 휘발성 마취제 배출을 줄이기 위한 국가 정책이 성장을 주도하고 있습니다. 중국에서는 미다졸람이 1급 마약으로 지정됨에 따라 임상의들은 이미 레미마졸람으로 전환하고 있으며, 인도에서는 단계적 GMP 준수 프로그램을 통해 공급에 지장을 주지 않으면서 제조 품질을 향상시키고 있습니다. 유럽에서는 지속가능성 정책으로 인한 데스플레인 단계적 폐지가 기회와 제약을 동시에 가져오고 있습니다. 영국 국민보건서비스(NHS)는 2024년 완전 폐지를 완료하고, 유럽연합(EU) 전체는 2026년까지 지역 전체 금지를 검토하고 있습니다. 독일과 스칸디나비아 병원들은 휘발성 가스 회수 시스템 시험 운영을 주도하고 있으며, 회수 효율이 100% 미만인 경우 전신마취(TIVA)가 여전히 주요 컴플라이언스 수단임을 인정하고 있습니다. 프레제니우스(Fresenius)와 같은 유럽 공급업체들은 엄격한 규제 상황에도 불구하고 2025년 1분기 7%의 매출 성장을 달성한 것에서 알 수 있듯이, 주사제 라인 확장을 통해 대응하고 있습니다.

The General Anesthesia Drugs Market is expected to grow from USD 5.47 billion in 2025 to USD 5.66 billion in 2026 and is forecast to reach USD 6.74 billion by 2031 at 3.54% CAGR over 2026-2031.

This steady expansion is underpinned by rising global surgical volumes, widening uptake of artificial-intelligence-enabled closed-loop delivery systems, and the progressive rollout of ambulatory surgical centers that favor rapid-recovery agents. Hospital administrators are increasingly shifting toward total intravenous anesthesia (TIVA) protocols to meet environmental targets and improve patient throughput, while sustained shortages in key volatile agents continue to disrupt purchasing strategies. Competitive dynamics are also changing as novel molecules such as ciprofol and remimazolam win regulatory approval and erode incumbent drug revenues. Together, these forces are re-shaping formulation portfolios, commercial alliances, and regional demand patterns across the general anesthesia drugs market.

Accelerated clearance of ciprofol and remimazolam has widened the therapeutic toolkit for anesthesiologists, lowering injection-site pain incidence from 77.1% to 18.0% and offering superior cardiovascular stability in elderly patients. The United States Food and Drug Administration's 2025 nod for JOURNAVX (suzetrigine) underscores a wider pivot toward non-opioid peri-operative analgesia that complements general anesthesia protocols. Amneal's 2024 launch of single-dose propofol vials aimed at easing recurrent shortages is projected to generate USD 314 million in annual revenue. Collectively, these approvals expand the number of viable intravenous options, intensify competition, and raise the innovation bar throughout the general anesthesia drugs market.

United States ASC expenditure reached USD 6.1 billion for 3.3 million Medicare fee-for-service beneficiaries in 2022, and the segment's revenue base is poised to advance from USD 37 billion in 2021 to USD 59 billion by 2028. The CMS-backed NOPAIN Act will grant distinct reimbursement for non-opioid analgesics such as EXPAREL from January 2025, sharpening the economic case for fast-recovery anesthesia protocols in outpatient settings. Growing ASC footprints are therefore heightening demand for rapid-onset drugs like ciprofol, driving measurable incremental volumes across the general anesthesia drugs market.

The National Health Service's phase-out of desflurane and the European Commission's pending restrictions have reduced global inhalational agent emissions by 27% over the last decade. Concurrent equipment recalls, including Getinge's sevoflurane vaporizers owing to hydrogen-fluoride release risk, exacerbate pressure on supply chains. Hospitals are therefore stockpiling or transitioning to TIVA, muting growth in volatile revenues across the general anesthesia drugs market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sevoflurane retained 36.78% of general anesthesia drugs market share in 2025, but propofol is projected to post a 4.65% CAGR through 2031, reflecting a decisive shift toward TIVA protocols. The general anesthesia drugs market size for propofol-based formulations is set to expand further as ciprofol demonstrates non-inferiority while slashing injection-site pain rates. Desflurane's trajectory remains negative because of impending European environmental bans, whereas dexmedetomidine and remifentanil maintain specialized, procedure-specific niches. Regulatory withdrawals affecting dexmedetomidine in 2024 temporarily tightened supply but did not materially alter long-term demand. Midazolam's stricter scheduling in China is pushing providers toward remimazolam, which offers rapid recovery without the same regulatory burden. Ketamine and etomidate continue to occupy stable, smaller segments, with etomidate indispensable for hemodynamically unstable cases despite periodic shortages.

Underlying drivers include tighter environmental rules, heightened interest in immunomodulatory advantages linked to intravenous agents, and the operational efficiency of AI-driven infusion pumps. Collectively, these trends cement the intravenous pivot and reinforce propofol's leadership role within the evolving general anesthesia drugs market.

Inhalational techniques held 58.41% of the general anesthesia drugs market in 2025, yet intravenous delivery displayed a 5.88% CAGR that signals accelerating preference for precision-controlled infusions. The general anesthesia drugs market size for intravenous products is benefitting from closed-loop systems that automatically titrate dosing in response to EEG-derived depth metrics, a feature that volatile agents cannot replicate. Emission-reduction mandates and inconsistent supply of halogenated gases are compelling hospitals to treat TIVA as a compliance strategy rather than a clinical luxury.

Volatile capture technology delivers only 25-73% real-world efficiency, limiting its viability as a full-scale mitigation approach and indirectly supporting the intravenous surge. Emerging clinical literature additionally links intravenous anesthesia to lower postoperative nausea, faster cognitive recovery, and reduced inflammatory markers. These medical and regulatory tailwinds position intravenous administration to continue outgrowing inhalational routes across the general anesthesia drugs market.

The General Anesthesia Drugs Market Report is Segmented by Drug Type (Propofol, Sevoflurane, Desflurane, Dexmedetomidine, Remifentanil, and More), Route of Administration (Inhalation, Intravenous), Application (General Surgery, Cancer Surgery, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 37.84% of general anesthesia drugs market revenue in 2025, reflecting advanced surgical infrastructure, early adoption of AI-driven delivery systems, and supportive reimbursement policies. Federal scrutiny of consolidation illustrated by the FTC's case against U.S. Anesthesia Partners-may temper future roll-up strategies but is unlikely to derail volume growth. Workforce shortages, with 78% of U.S. facilities reporting staffing gaps in 2022, are prompting accelerated investment in automated solutions that can safely extend clinician bandwidth.

Asia-Pacific is the fastest-growing geography at 5.19% CAGR through 2031, fueled by rising surgical volumes, government incentives to upgrade operating theatres, and national policies aimed at lowering volatile-agent emissions. China's Category I scheduling of midazolam is already steering clinicians toward remimazolam, while India's phased GMP compliance program seeks to raise manufacturing quality without choking supply. Europe faces both opportunity and constraint as sustainability agendas phase out desflurane; the United Kingdom's National Health Service completed full withdrawal in 2024 and the wider European Union weighs region-wide bans by 2026. German and Scandinavian hospitals lead trials of volatile capture systems but admit that sub-100% efficiencies will leave TIVA as the primary compliance pathway. European suppliers such as Fresenius are responding with expanded injectable lines, evidenced by Q1 2025 revenue growth of 7% despite stringent regulatory landscapes.