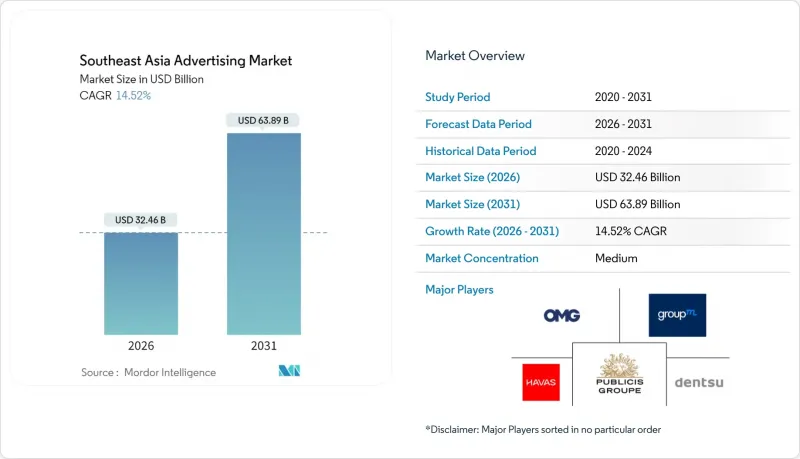

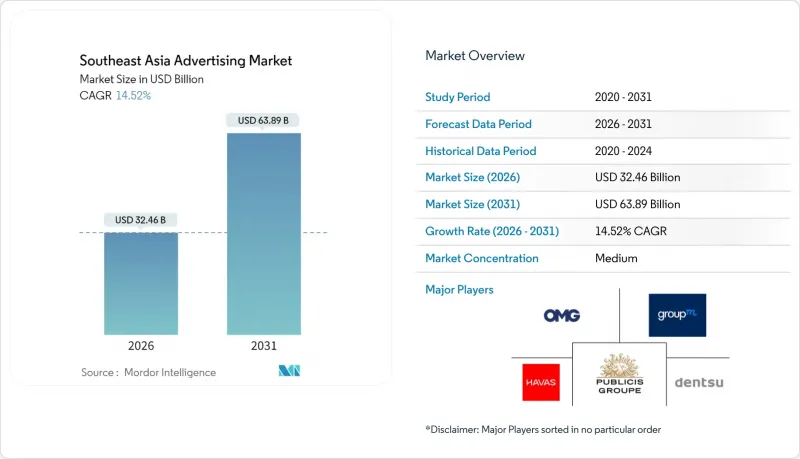

동남아시아의 광고 시장은 2025년에 283억 4,000만 달러로 평가되었으며, 2026년 324억 6,000만 달러에서 2031년까지 638억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 14.52%로 예상됩니다.

매출 성장은 모바일 퍼스트의 급속한 디지털 도입, AI를 활용한 캠페인 최적화, 중소기업의 온라인 광고를 지원하는 정부 보조금에 힘입어 성장세를 보이고 있습니다. 전통적인 채널에 대한 지출이 여전히 집중되어 있는 반면, 자동화되고 데이터가 풍부한 포맷으로의 전환은 분명하며, 특히 스마트폰 당 월별 모바일 데이터 사용량이 2023년 13GB에서 2030년까지 59GB로 증가할 것으로 예상됨에 따라, 이러한 추세는 두드러집니다. 슈퍼 앱 생태계, 확대되는 소매 미디어 네트워크, 디지털 옥외광고(DOOH) 측정 기준 강화로 채널 구성이 확대되고, 지역 전체 브랜드에 대한 광고 비용 효율성(ROAS)이 향상되고 있습니다.

모바일 연결성은 동남아시아 광고 시장에서 광고 도달 범위를 재정의하고 있습니다. GSMA의 예측에 따르면, 2030년까지 월간 데이터 사용량이 4배 이상 급증할 것으로 예상되어, 그동안 대역폭의 제약을 받았던 고비트레이트 동영상과 몰입형 포맷을 위한 여지가 생겨날 것으로 보입니다. 인도네시아의 고정 브로드밴드 보급률이 20% 미만인 상황에서 모바일이 기본 디지털 게이트웨이로 자리 잡으면서 광고주들은 위치 기반 타겟팅과 동영상 우선 크리에이티브를 채택하는 움직임이 가속화되고 있습니다. 통신 속도의 향상으로 인해 프로그래매틱 플랫폼이 사용할 수 있는 데이터도 풍부해졌고, 실시간 참여 지표를 재고 구매 및 최적화의 주요 메커니즘으로 바꾸고 있습니다.

디지털 사이니지에서는 현재 실시간 기상정보와 교통정보에 따라 변화하는 동적 광고를 제공하고 있습니다. 2024년 7월 Moving Walls와 GroupM이 체결한 계약에 따라 말레이시아 바이어들은 검증된 DOOH 재고를 확보할 수 있게 되어 기존의 가시성에 대한 우려를 줄일 수 있게 되었습니다. 인구 밀도가 높은 싱가포르나 방콕의 경우, 알고리즘에 의한 스케줄링을 통해 시간대, 혼잡 경로, 모바일 단말기에서 수집한 시장 내 행동에 따라 크리에이티브를 로테이션할 수 있습니다. Open Measurement in Out-of-Home Group과 같은 표준화 단체는 오픈 소스 노출 프레임워크를 공개하여 광고주가 온라인 채널에 요구하는 책임성을 실현하고 있습니다.

말레이시아에는 300개 이상의 간판 소유자가 존재하며, 바이어들은 단편적으로 캠페인을 구성해야만 합니다. CtrlShift의 AMP 마켓플레이스는 현재 7대 퍼블리셔의 인벤토리를 통합하고 있지만, 그 규모는 여전히 제한적입니다. 인도네시아나 필리핀의 소규모 디지털 퍼블리셔들은 공통의 애드테크 스택과 가격 책정의 투명성이 부족하여 문제를 더욱 복잡하게 만들고 있습니다. 이러한 파편화는 거래 비용을 높이고 신규 진입을 방해하며, 동남아시아 광고 시장에서 프로그래매틱 지출의 성장세를 둔화시키고 있습니다.

2025년 기준, 동남아시아 광고 시장에서 전통적 채널의 점유율은 60.12%를 유지했습니다. 이는 지방과 노년층의 TV 시청이 정착되어 있기 때문입니다. 그러나 이 부문의 완만한 성장은 디지털 미디어의 CAGR 15.05%와는 대조적으로, 스마트폰과 저가 데이터 요금제에 힘입은 소비 행태의 전환이 되돌릴 수 없는 것임을 보여줍니다. 이러한 빠른 성장은 TV나 인쇄매체에서는 실현 불가능한 프로그래매틱 구매의 효율성과 세밀한 타겟팅에 기인합니다. 태국에서는 2024년 디지털 광고 지출이 처음으로 TV 광고를 앞질렀고(45% 대 35%), 온라인 동영상과 소셜 피드로의 소비자 이동이 두드러졌습니다.

디지털 광고의 발전은 실시간 현지화가 필요한 크로스보더 EC 캠페인에 의해 더욱 가속화되고 있습니다. 이 기능을 제공할 수 있는 것은 알고리즘을 활용한 채널뿐입니다. 한편, 영화관이나 전통적인 옥외광고 포맷은 밀집된 대도시 지역에서는 여전히 유효합니다. 이러한 지역에서는 프리미엄 계층이 몰입감이 있고 브랜드 이미지를 훼손하지 않는 환경을 중요하게 여깁니다. 그러나 성과지표, 어트리뷰션, 오디언스 데이터의 차이로 인해 예산이 디지털 광고에 크게 기울어지고 있으며, 예측 기간 동안 동남아시아 광고 시장의 지출 구성을 재구성하는 피드백 루프를 강화하고 있습니다.

2025년 TV의 29.35% 점유율은 여전히 가장 수익성이 높은 단일 미디어로서의 지위를 반영하고 있으며, 이는 전통적인 관습과 대중 도달 효율을 모두 반영합니다. 그러나 디지털 옥외광고(DOOH)는 스크린 비용 감소, 5G 연결, 표준화된 노출 측정 프레임워크에 힘입어 15.72%의 CAGR로 가장 높은 성장세를 보이고 있습니다. 광고주들은 DOOH가 시간대별로 크리에이티브를 업데이트하고, 날씨나 교통 체증과 같은 지역 고유의 자극에 따라 광고를 트리거할 수 있는 DOOH의 능력을 높이 평가하고 있습니다.

전통적인 인쇄 매체와 라디오는 노인층을 대상으로 한 신문 지면 광고, 혼잡한 노선의 출퇴근 시간대 라디오 광고 등 특정 틈새 시장에서의 매력을 유지하고 있습니다. 그러나 측정 방법의 격차가 확대됨에 따라 그 점유율은 줄어드는 추세입니다. 영화관 광고는 대작 영화 개봉 시 프리미엄 광고?을 활용할 수 있지만, 상영관 수용인원이 성장의 한계로 작용하고 있습니다. 검색, 소셜, 디스플레이, OTT 동영상을 포함한 디지털 광고는 더 나은 어트리뷰션 모델과 AI 강화 크리에이티브 테스트를 통해 동남아시아 광고 시장에서 브랜드의 운영 성과를 최적화하고 방송 예산에서 자금을 계속 빨아들이고 있습니다.

The South East Asia Advertising market was valued at USD 28.34 billion in 2025 and estimated to grow from USD 32.46 billion in 2026 to reach USD 63.89 billion by 2031, at a CAGR of 14.52% during the forecast period (2026-2031).

Revenue growth rides on rapid mobile-first digital adoption, AI-enabled campaign optimization, and government grants that help small businesses advertise online. While traditional channels still concentrate spending, the shift toward automated, data-rich formats is unmistakable, especially as monthly mobile data usage per smartphone is set to climb from 13 GB in 2023 to 59 GB by 2030. Super-app ecosystems, expanding retail media networks, and stronger measurement standards for Digital Out-of-Home (DOOH) are widening the channel mix and enhancing return on ad spend for brands across the region.

Mobile connectivity is redefining ad reach across the Southeast Asia Advertising market. GSMA projects that monthly data usage will surge more than fourfold by 2030, opening space for high-bit-rate video and immersive formats that were previously bandwidth-constrained. With Indonesia's fixed broadband penetration below 20%, mobile is the default digital gateway, prompting advertisers to adopt location-based targeting and video-first creative. Faster speeds also enrich the data available to programmatic platforms, turning real-time engagement metrics into the primary mechanism for buying and optimizing inventory.

Digital billboards now stream dynamic ads shaped by live weather or traffic feeds. A July 2024 deal between Moving Walls and GroupM gave Malaysian buyers verified DOOH inventory, mitigating historical viewability doubts. In dense Singapore and Bangkok, algorithmic scheduling lets brands rotate creative by daypart, congested routes, or in-market behaviors pulled from mobile devices. Standard-setting bodies such as the Open Measurement in Out-of-Home Group released open-source impression frameworks, bringing the accountability that advertisers expect from online channels.

Malaysia counts more than 300 billboard owners, forcing buyers to stitch together campaigns piecemeal. CtrlShift's AMP marketplace now aggregates inventory from seven major publishers, but scale remains limited. Smaller digital publishers across Indonesia and the Philippines compound the problem, lacking common ad-tech stacks or transparency in pricing. Fragmentation raises transaction costs, deters new entrants, and slows the growth trajectory of programmatic spend within the Southeast Asia Advertising market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Traditional channels retained a 60.12% share of the South East Asia Advertising market in 2025, buoyed by entrenched TV viewership among rural and older audiences. Yet the segment's modest growth contrasts with digital media's 15.05% CAGR, signaling an irreversible consumption pivot fueled by smartphones and cheaper data plans. Rapid gains stem from programmatic buying efficiencies and granular targeting that television or print cannot match. Thailand marked a pivotal moment in 2024 when digital ad spend surpassed TV, taking 45% versus 35%, underlining consumer migration to online video and social feeds.

Digital's advance is accelerated further by cross-border e-commerce campaigns demanding real-time localization, a capability only algorithmic channels can deliver. Meanwhile, cinema and classic outdoor formats remain relevant in dense metros, where premium audiences value immersive, brand-safe settings. Still, the differential in performance metrics, attribution, and audience data tilts budgets heavily toward digital, reinforcing a feedback loop that reshapes the spending mix of the Southeast Asia Advertising market over the forecast period.

Television's 29.35% stake in 2025 still positions it as the most lucrative single medium, reflecting both legacy habit and mass-reach efficiency. However, Digital Out-of-Home exhibits the highest trajectory at 15.72% CAGR, aided by falling screen costs, 5G connectivity, and standardized impression counting frameworks. Advertisers appreciate DOOH's ability to refresh creative by daypart or trigger ads based on localized stimuli such as weather or traffic congestion.

Traditional print and radio keep niche appeal, newspaper inserts among older readers, and commuter-time radio ads on high-congestion routes, but their share contracts as measurement gaps widen. Cinema capitalizes on blockbuster releases for premium placements, yet venue capacity caps growth. Digital advertising covering search, social, display, and OTT video continues to siphon dollars from broadcast budgets, riding on better attribution models and AI-enhanced creative testing that optimize in-flight performance for brands across the Southeast Asia Advertising market.

The South East Asia Advertising Market Report is Segmented by Channel Type (Traditional Media and Digital Media), Advertising Medium (Television, Digital Advertising, Print, and More), Transaction Type (Programmatic and Non-Programmatic), End-User Industry (FMCG, Retail and E-Commerce, Automotive, BFSI, Telecom and IT, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).