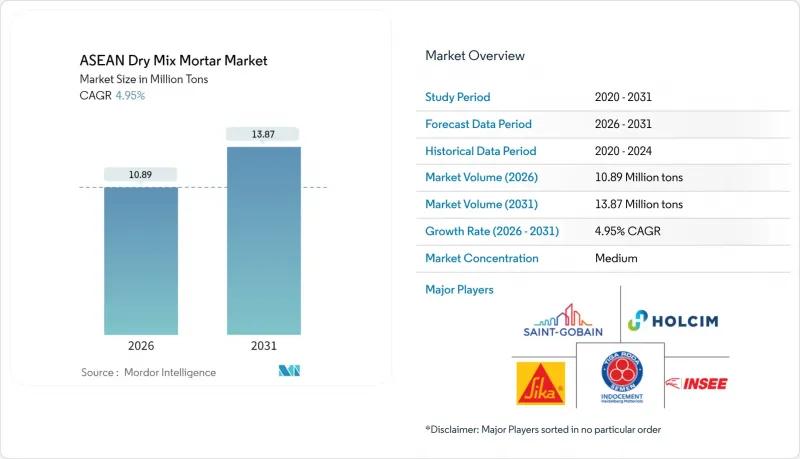

ASEAN 지역 드라이 믹스 모르타르 시장은 2025년 1,038만 톤에서 2026년에는 1,089만 톤으로 성장하여 2026년부터 2031년까지 CAGR 4.95%를 기록하며 2031년까지 1,387만 톤에 달할 것으로 예측됩니다.

이러한 확대는 대규모 공공 주택 프로그램, 민간 부동산 시장의 회복, 산업 생산능력의 증가를 반영하여 지역 전체에 대한 모르타르 수요를 증가시키고 있습니다. 아세안 드라이 믹스 모르타르 시장은 급속한 도시로의 인구 이동, 강화된 건축 기준, 그리고 프리믹스 솔루션에 유리한 인건비 상승의 혜택을 누리고 있습니다. 다국적 업체들이 현지 공장을 증설하고, 국내 시멘트 대기업들이 다운스트림공정으로 진출하여 부가가치가 높은 모르타르에 진출함에 따라 경쟁이 심화되고 있으며, 가치사슬 관리와 제품 차별화가 수익률을 좌우하는 상황이 발생하고 있습니다. 섬나라 시장의 물류 제약과 원자재 가격 변동은 여전히 구조적인 문제이지만, 운송비 비율을 낮추는 현지 공장과 프리미엄 특종 등급의 수요 기회도 창출하고 있습니다. 지속가능성에 대한 요구, 특히 저탄소 바인더 시스템의 채택은 새로운 환경 기준을 충족하는 배합에 대한 조달 선택을 촉진할 것으로 예상됩니다.

아세안 도시 지역에서는 2030년까지 8,400만 명의 인구가 증가할 것으로 예상되며, 도시화율은 56%에 달할 것으로 예측됩니다. 이를 통해 주택, 교통 회랑, 사회 인프라에 대한 지속적인 수요를 창출할 수 있습니다. 연간 인프라 수요는 600억 달러 규모에 달하며, 트랜스마트라 유료도로, 투아스 거대 항만 등의 프로젝트가 모르타르 소비를 뒷받침하고 있습니다. 인도네시아의 2024년 건설 전략은 가치사슬의 민첩성을 강조하고 있으며, 현지 생산자들이 파이프라인 일정에 대응할 수 있도록 생산능력을 확대할 것을 요구하고 있습니다. 수도권 이외의 지방 도시가 새로운 성장 거점이 되고 있으며, 모르타르 공급업체들의 유통 지도를 재구성하고 있습니다. 홍수 대책부터 해안 방호까지 기후변화에 적응하기 위해서는 가혹한 환경에 견딜 수 있는 특수 혼합재가 필요하며, 이는 고부가가치 제품 수요의 확대로 이어지고 있습니다.

외국인 노동자 수용 한도 축소와 노동력 고령화로 인해 말레이시아와 싱가포르에서는 노동력 부족이 심화되고 있습니다. 이는 건설업체들이 현장에서의 기술 요구 사항을 최소화하는 기성품 모르타르를 채택하도록 장려하고 있습니다. 중소기업은 품질 일관성과 시공 속도를 보장하는 표준화된 배합을 점점 더 선호하고 있습니다. 디지털 커머스 솔루션을 통해 중소 건설업체는 기존 유통업체를 거치지 않고 온라인으로 포장 배합을 주문할 수 있어 리드타임을 단축할 수 있습니다. 고층 프로젝트에서는 균일한 배합으로 재작업과 재료 폐기물을 줄여 부가가치를 높입니다. 싱가포르 주택개발청(HDB)은 공공주택용 폴리머 개질 모르타르에 대한 공식적인 사양을 정하고 있으며, 고급 제품에 대한 지역 표준을 확립하고 있습니다.

인도네시아, 필리핀, 미얀마의 농촌 지역 주택 소유주들은 패키지 모르타르에 부가가치가 더해져 수작업으로 모래와 시멘트를 혼합하는 것을 선호합니다. 현금 거래가 주를 이루는 이 부문에서는 장기적인 성능 향상을 통해 초기 비용 회수를 정당화할 수 있는 융자 옵션이 제한적입니다. 소규모 프로젝트에서는 품질 기준이 지정되는 경우가 드물기 때문에 가장 저렴한 자재가 수주하는 경향이 있습니다. 인플레이션 충격은 가계 비용을 높이고, 프로젝트 연기를 유발하고, 가격에 민감한 계층의 박격포 수요를 직접적으로 감소시킵니다.

2025년 기준, 아세안 지역 드라이 믹스 모르타르 시장 점유율의 40.62%를 미장용 모르타르가 차지했습니다. 이는 습한 기후에서 보호 기능과 장식 기능의 이중 역할이 선호되기 때문입니다. 타일용 접착제는 고층 아파트 및 소매점 인테리어에서 고급 세라믹 바닥재에 대한 수요가 증가함에 따라 2031년까지 CAGR 6.31%로 성장할 것으로 예상됩니다. 타일용 접착제의 아세안 드라이믹스 모르타르 시장 규모는 2026년부터 2031년까지 도시지역 분양 아파트 건설 수요와 연동하여 확대될 것으로 예상됩니다. 그라우트는 인프라 접합부에서 안정적인 틈새시장을 유지하고 있으며, 방수 슬러리는 집중호우 대책이 필요한 해안도시에서 수요가 증가하고 있습니다. 콘크리트 보호 및 개보수 분야에서는 내구성이 뛰어난 오버레이 솔루션을 필요로 하는 노후화된 교량 및 항만이 수요를 뒷받침합니다. SNI 6880 : 2016과 같은 국가 표준은 구조용 콘크리트용 포장된 건조혼합재의 사용을 승인하여 특수 배합재에 대한 신뢰성을 높이고 있습니다.

공공주택에서는 유지보수 주기를 단축하는 내장형 발수제를 내장한 2세대 렌더링 소재가 사양 채택을 이끌어내고 있습니다. 타일 접착제 제조업체는 새롭게 등장한 대형 도자기 타일에 대응하기 위해 변형성 등급을 제공합니다. 디지털 커머스 플랫폼에서는 시공업체가 쉽게 도입할 수 있는 즉시 사용 가능한 제품 계산 도구가 주목받고 있습니다. 방수 슬러리에 대한 수요는 건축 외피의 건전성을 우선시하는 기후변화 적응 투자와 연동되어 있습니다. 저탄소 바인더와 재생골재 충전재의 혁신은 지속가능한 개보수를 지향하는 공급업체의 차별화 요소가 될 것입니다.

아세안 드라이믹스 모르타르 시장 보고서는 용도별(석고, 렌더링, 타일 접착제, 방수 슬러리, 콘크리트 보호 및 보수 등), 최종사용자 산업별(주거, 상업, 인프라, 산업 및 공공시설), 지역별(말레이시아, 인도네시아, 태국, 싱가포르, 필리핀, 베트남, 미얀마, 기타 아세안 국가)로 분류됩니다. 필리핀, 베트남, 미얀마, 기타 아세안 국가)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

The ASEAN Dry Mix Mortar Market is expected to grow from 10.38 million tons in 2025 to 10.89 million tons in 2026 and is forecast to reach 13.87 million tons by 2031 at 4.95% CAGR over 2026-2031.

This expansion reflects large public-sector housing programs, private real-estate recovery, and industrial capacity additions, pushing mortar volumes across the region. The ASEAN dry mix mortar market benefits from rapid urban migration, stronger building codes, and rising labor costs that favor pre-mixed solutions. Competitive intensity is growing as multinational producers add local plants and domestic cement majors move downstream into value-added mortars, creating a landscape where supply-chain control and product differentiation determine margin performance. Logistics constraints in archipelagic markets and raw-material price swings remain structural challenges, yet they also open opportunities for localized plants and premium specialty grades that reduce transport cost ratios. Sustainability mandates, particularly adopting low-carbon binder systems, are expected to tilt procurement choices toward formulations that meet new green codes.

ASEAN cities are forecast to absorb 84 million additional residents by 2030, lifting urbanization to 56% and driving sustained demand for housing, transport corridors, and social infrastructure. Annual infrastructure needs run to USD 60 billion, with projects such as the Trans-Sumatra toll road and Tuas mega-port underpinning mortar consumption. Indonesia's 2024 construction strategy highlights supply-chain agility, ensuring local producers scale capacity to meet pipeline timelines. Secondary cities outside national capitals now represent growth nodes, reshaping distribution maps for mortar suppliers. From flood mitigation to coastal defenses, climate adaptation requires specialty mixes that withstand aggressive environments, amplifying value-added volume opportunities.

Tighter foreign-worker quotas and an aging workforce have sharpened labor shortages in Malaysia and Singapore, encouraging contractors to adopt ready-mixed mortars that minimize on-site skill requirements. Small and medium enterprises increasingly favor standardized mixes that guarantee consistent quality and faster application. Digital commerce solutions let SME builders order pre-bagged formulations online, bypassing traditional distributors and shortening lead times. High-rise projects gain added value because uniform mixes reduce rework and material waste. Singapore's Housing and Development Board has formal specifications for polymer-modified mortars in public housing, setting a regional benchmark for advanced products.

Self-build homeowners in rural Indonesia, the Philippines, and Myanmar favor manual sand-cement mixes because packaged mortars carry price premiums they are unwilling to absorb. Cash transactions dominate these segments, limiting financing options that could justify higher upfront outlays through long-term performance gains. Smaller projects rarely specify quality benchmarks, so cheapest materials often win orders. Inflation shocks raise household costs and trigger project deferrals, directly trimming mortar demand in price-sensitive tiers.the

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Render accounted for 40.62% of the ASEAN dry mix mortar market share in 2025, supported by its dual protective and decorative roles in humid climates. Tile adhesives are expected to post a 6.31% CAGR through 2031 as rising income levels drive demand for premium ceramic flooring in high-rise apartments and retail interiors. The ASEAN dry mix mortar market size for tile adhesives is forecast to expand by 2026-2031 alongside urban condominium pipelines. Grout maintains a steady niche in infrastructure joints, while waterproofing slurries grow in coastal cities coping with heavy rainfall. Concrete protection and renovation receive support from aging bridges and ports requiring durable overlay solutions. National standards such as SNI 6880:2016 authorize packaged dry combined materials for structural concrete, reinforcing confidence in specialty formulations.

Second-generation renders with integral water repellents are winning specifications in public housing because they cut maintenance cycles. Tile adhesive producers offer deformability classes to fit new large-format porcelain tiles. Digital commerce platforms spotlight ready-to-use product calculators, easing contractor adoption. Waterproofing slurry demand dovetails with climate adaptation investments that prioritize building-envelope integrity. Innovation in low-carbon binders and recycled aggregate infill is set to differentiate suppliers targeting sustainable renovation.

The ASEAN Dry Mix Mortar Market Report is Segmented by Application (Plaster, Render, Tile Adhesive, Water Proofing Slurry, Concrete Protection and Renovation, and More), End-User Industry (Residential, Commercial, Infrastructure, and Industrial and Institutional), and Geography (Malaysia, Indonesia, Thailand, Singapore, Philippines, Vietnam, Myanmar, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Volume (Tons).