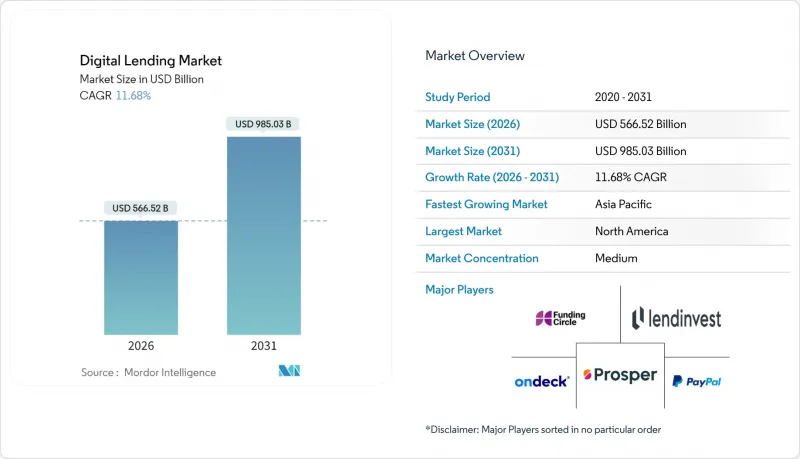

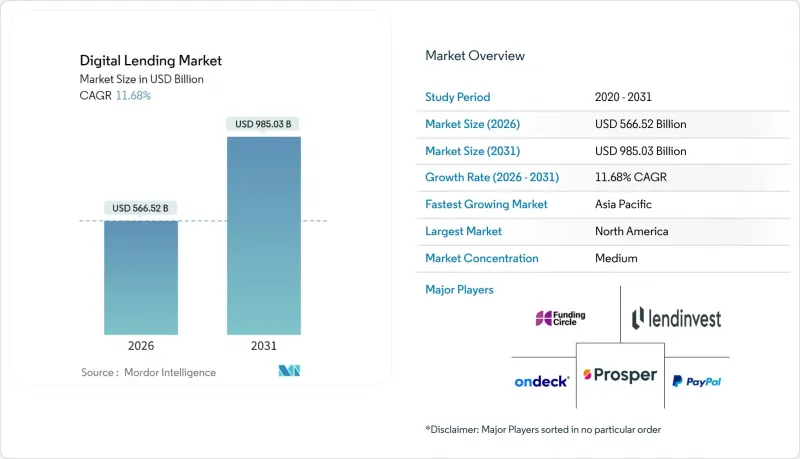

디지털 렌딩 시장은 2025년에 5,072억 7,000만 달러로 평가되었고, 2026년 5,665억 2,000만 달러에서 2031년까지 9,850억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 11.68%로 예상됩니다.

이러한 성장 추세는 기술을 통한 신용 업무의 꾸준한 발전, 임베디드 금융 거래량 증가, AI 심사에 대한 기관의 폭넓은 수용을 뒷받침합니다. 실시간 여신심사, 오픈뱅킹을 통한 데이터 전송, 후불결제(BNPL) 옵션은 대출자를 지점 채널에서 계속 멀어지게 하고 있습니다. 금융기관은 클라우드 네이티브 대출 시스템에 투자하여 처리 비용을 절감하고, 대출 실행 시간을 몇 주에서 몇 분으로 단축하고 있습니다. 얼터너티브 데이터를 활용한 신용 점수화 기술은 신용 기록이 부족한 고객층과 국경을 초월한 중소기업을 위한 자금 조달 등 새로운 수익 기회를 창출하고 있습니다. 주요 지역에서 핀테크 기업, 전통 은행, 빅테크 플랫폼이 동일한 고객층을 놓고 경쟁하는 가운데, 경쟁은 더욱 치열해지고 있습니다.

2024년 전 세계 스마트폰 사용자 수는 68억 명에 달할 것이며, 대출기관은 모바일 앱을 통해 대출자에게 직접 접근할 수 있는 환경이 조성될 것입니다. 아시아태평양에서만 디지털 월렛 결제가 9조 8,000억 달러에 달하며, 앱 내 신용 제공에 대한 고객의 준비 태세를 강화하고 있습니다. 현재 대출 기관들은 위치 정보, 기기 메타데이터, 행동 패턴을 활용하여 몇 초 만에 위험을 평가함으로써 수백만 명의 첫 대출자에게 신용 한도를 열어주고 있습니다. 인도 데이터 보호위원회, EU의 AI법 등 규제 당국은 데이터 활용을 표준화하고 있으며, 이를 통해 대출 기관은 컴플라이언스를 준수하는 모바일 퍼스트 모델을 확장할 수 있습니다.

디지털 대출 신청의 90% 이상이 자동 심사 엔진을 통해 이루어지고 있으며, Upstart는 서류 업로드 없이 80%의 즉각적인 승인을 실현하고 있습니다. 머신러닝 모델이 수백 개의 대출자 속성을 실시간으로 분석하여 심사 비용 절감과 고객 만족도 향상을 도모하고 있습니다. 5분 미만의 승인 시간을 실현할 수 없는 은행들은 시장 점유율 유지를 위해 핀테크 업체와의 화이트 라벨 제휴를 선택하는 경우가 증가하고 있습니다.

금융기관 IT 예산 중 보안에 할당되는 비중은 13%에 불과한 반면, API의 영향력은 점점 확대되고 있습니다. 2024년 조사 대상 대출 기관의 62%가 사기 사건 증가를 보고했으며, 규제 당국은 GDPR(EU 개인정보보호규정)과 CCPA 제도에 따라 제로 트러스트 아키텍처를 요구하고 있습니다. 사이버 보험의 보험료 상승과 정보 유출 통지 의무화로 인해, 특히 크로스보더 플랫폼의 컴플라이언스 비용이 급증하고 있습니다.

2025년 소비자 대출은 개인금융과 BNPL 수요에 힘입어 디지털 대출 시장의 60.78%를 차지할 것으로 예측됩니다. 한편, 중소기업 대출은 2031년까지 연평균 복합 성장률(CAGR) 16.08%로 확대될 것으로 예상되며, 이는 운전자금 부족과 실시간 현금 흐름 가시성을 평가하는 얼터너티브 데이터 모델 채택이 그 배경이 될 것으로 보입니다. 중소기업용 디지털 대출 시장 규모는 2031년까지 2,460억 9,000만 달러에 달할 것으로 예측됩니다. 대출기관은 회계 소프트웨어와 API를 연동하여 인보이스, 급여, 세금 데이터를 수집함으로써 신용 심사 주기를 몇 주에서 48시간으로 단축하고 있습니다. 지역밀착형 플랫폼이 소비자 포트폴리오와 동등한 수준의 신용손실률을 달성하는 가운데, 전 세계 은행들은 수익배분형 파트너십을 통해 유통망 확보에 나서고 있습니다.

소비자 분야에서는 EC 결제 프로세스에 내장된 신용 제공이 저소득층에 대한 보급을 지속적으로 확대하고 있습니다. 밀레니얼 세대의 경우, 월급쟁이 밀레니얼 세대의 경우, 급여 주기 데이터를 활용한 급여 선지급 서비스 이용률이 증가하고 있습니다. 고도의 설명 가능한 AI 모델이 편향성을 줄이고, 대규모 동세대 그룹 전체에서 대손율 하락 추세를 시사하고 있습니다. 이러한 요인들이 결합되어 소비자 대출 규모의 견고한 기반을 유지하면서 급성장하는 중소기업 시장을 개척하고 있습니다.

2025년 기준 디지털 대출 시장 규모에서 개인 대출은 즉시 심사 모델과 저비용을 바탕으로 35.44%를 차지했습니다. 자동차 대출은 판매점에서 60초 이내로 절차 시간을 단축하는 판매시점정보관리(POS) 연계를 활용하고, 이에 이어(UPSTART.COM)이 이어집니다. 주택담보대출, 주택담보대출, 학자금대출 분야는 복잡한 담보 심사 및 보조금 규정으로 인해 디지털 전환이 늦어지고 있습니다.

중소기업 운전자금 대출은 10.52%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 매출연동형 대출은 상환을 일일 카드매출액에 연동하여 수요 변동 시 사업자에게 유연성을 제공합니다. 기업 자원 계획(ERP) 대시보드에 내장된 인보이스 팩토링 플랫폼은 인보이스 발행 후 24시간 이내에 유동성을 확보할 수 있습니다. 이 임베디드 금융 루트는 기존 신용 한도에 대한 담보가 부족했던 전 세계 물류, 농업, 프리랜서 생태계를 끌어들이고 있습니다.

2025년 아시아태평양은 디지털 대출 시장의 39.35%를 차지했습니다. 이는 235개 이상의 인가된 디지털 은행과 인도의 UPI(월평균 거래 건수 120억 건)와 같은 정부 지원 결제 인프라가 뒷받침하고 있습니다. 중국의 슈퍼앱은 지갑, 라이드 셰어링, 음식 배달 서비스 위에 대출 기능을 얹어 강력한 데이터 루프를 형성하고 있습니다. 싱가포르와 호주 정부는 제품 테스트 주기를 6개월로 단축하는 규제 샌드박스를 운영하여 신규 진입 금융기관 시장 진입을 가속화하고 있습니다.

아프리카는 21.85%의 가장 빠른 CAGR을 기록하며 2028년까지 470억 달러의 매출 규모에 도달할 것으로 예측됩니다. 케냐와 가나에서 선구적으로 도입된 모바일 머니 기반은 통화시간 구매와 개인 간 송금을 분석하여 위험 점수를 산출하는 소액 대출의 기반을 형성하고 있습니다. 나이지리아와 이집트의 스타트업 기업들은 국제적인 벤처 자금을 유치하여 아프리카 이민자들을 위한 국경 간 급여 선지급 솔루션을 개발하고 있습니다.

북미와 유럽은 높은 보급률을 보이는 반면, 표면적인 성장률은 둔화되고 있습니다. 미국의 BNPL(후불제) 관련 법규는 유동적이지만, PayPal의 누적 대출액은 300억 달러를 돌파하며 성숙한 기업의 규모를 보여주고 있습니다. 유럽에서는 PSD3 개정과 EU AI 법이 통일된 규칙을 제공하고, 국경을 넘는 여권 제도를 강화하고 있습니다. 다만, 여러 소비자 신용 지침의 금리 상한선이 고수익 부문을 억제하고 있습니다. 라틴아메리카에서는 브라질의 PIX와 같은 실시간 결제 기반의 임베디드 금융 거래가 증가하고 있으며, 거시경제의 변동성에도 불구하고 두 자릿수 대출 성장의 토대를 마련하고 있습니다.

The digital lending market was valued at USD 507.27 billion in 2025 and estimated to grow from USD 566.52 billion in 2026 to reach USD 985.03 billion by 2031, at a CAGR of 11.68% during the forecast period (2026-2031).

This growth profile underscores steady gains in technology-mediated credit origination, rising embedded-finance volumes, and wider institutional acceptance of AI underwriting. Real-time credit decisioning, open-banking data transfers, and buy-now-pay-later (BNPL) options continue to draw borrowers away from branch channels. Institutions are investing in cloud-native loan-origination systems that trim processing costs and shrink disbursement times from weeks to minutes. New revenue opportunities have emerged around thin-file customers and cross-border small-business funding, aided by alternative-data credit scoring. Competitive intensity is strengthening as fintechs, traditional banks, and BigTech platforms converge on identical customer segments in every major region.

Global smartphone users totaled 6.8 billion in 2024, giving lenders a direct path to borrowers through mobile apps. In Asia-Pacific alone, digital-wallet payments hit USD 9.8 trillion, reinforcing customer readiness for in-app credit offers. Lenders now harness geolocation, device metadata, and behavioural signals to evaluate risk in seconds, opening credit lines to millions of first-time borrowers. Regulators such as India's Data Protection Board and the EU's AI Act are standardizing data use, which helps lenders scale compliant mobile-first models.

More than 90% of digital loan applications are now routed through automated underwriting engines, and Upstart reports 80% instant approvals without document uploads. Machine-learning models digest hundreds of borrower attributes in real time, cutting origination costs and elevating customer satisfaction. Banks unable to match sub-five-minute approval windows increasingly choose white-label partnerships with fintech vendors to preserve market share.

Financial institutions allocate just 13% of IT budgets to security even as API footprints widen. In 2024, 62% of surveyed lenders registered rising fraud incidents, and regulators now demand zero-trust architectures under GDPR and CCPA regimes. Higher cyber-insurance premiums and mandatory breach notifications inflate compliance costs, particularly for cross-border platforms.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumer loans retained 60.78% of the digital lending market in 2025, propelled by personal finance and BNPL demand. At the same time, SME facilities are forecast to grow at a 16.08% CAGR to 2031, reflecting working-capital shortages and adoption of alternative-data models that reward real-time cash-flow visibility. The digital lending market size for SME products is projected to reach USD 246.09 billion by 2031. Lenders integrate APIs with accounting software to harvest invoices, payroll, and tax data, reducing underwriting cycles from weeks to 48 hours. As localized platforms achieve credit-loss rates on par with consumer portfolios, global banks are entering revenue-sharing partnerships to secure distribution.

In the consumer arena, embedded credit offers inside e-commerce checkouts continue to extend reach into lower-income cohorts. A growing share of salaried millennials now use pay-period data to unlock salary-advance options. Advanced explainable-AI models mitigate bias, pointing to downward pressure on charge-offs across large peer cohorts. Together, these forces preserve a solid base for consumer-loan volumes while opening an even faster-growing SME lane.

Personal loans represented 35.44% of the digital lending market size in 2025, fueled by instant-decision models and low acquisition costs. Auto loans follow, leveraging point-of-sale integrations that cut dealership desk time to under 60 seconds [UPSTART.COM]. Mortgage, home-equity, and student-loan categories are undergoing slower digital migration due to complex collateral checks and subsidy rules.

Working-capital loans to small businesses are projected to register a 10.52% CAGR. Revenue-based financing aligns repayments with daily card receipts, offering merchants flexibility during demand fluctuations. Invoice-factoring platforms that anchor inside enterprise-resource-planning dashboards unlock liquidity within 24 hours of invoice issuance. This embedded-finance route attracts global logistics, agriculture, and freelancer ecosystems that historically lacked collateral for traditional lines of credit.

The Digital Lending Market Report is Segmented by Type (Consumer, Enterprise/SME), Loan Type (Personal Loans, Auto Loans, and More), Deployment Mode (Cloud-Based, Hybrid and More), Business Model (Peer-To-Peer Marketplace Lending, Balance-Sheet Direct Lending, and More), Technology (AI/ML-driven Underwriting, API and Open-Banking Platforms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 39.35% of the digital lending market in 2025, supported by more than 235 licensed digital banks and government-backed payment infrastructures such as India's UPI, which averaged 12 billion monthly transactions in 2025. China's super-apps layer credit on top of wallets, ride-hailing, and food-delivery services, creating powerful data loops. Governments in Singapore and Australia operate regulatory sandboxes that shorten product-testing cycles to six months, accelerating market entry for challenger lenders.

Africa recorded the fastest 21.85% CAGR and is forecast to reach USD 47 billion in revenues by 2028. Mobile-money rails pioneered in Kenya and Ghana form the backbone of microlending engines that evaluate airtime purchases and peer-to-peer transfers to score risk. Start-ups in Nigeria and Egypt attract international venture funds and develop cross-border payroll-advance solutions for the African diaspora.

North America and Europe exhibit high penetration but slower headline growth. U.S. BNPL legislation remains fluid, yet PayPal surpassed USD 30 billion in cumulative originations, demonstrating scale for mature players. In Europe, PSD3 upgrades and the EU AI Act provide unified rules that enhance cross-border passporting, though interest-rate caps in several consumer-credit directives restrain high-yield segments. Latin America sees growing embedded-finance deals anchored on real-time payments such as Brazil's PIX, creating a runway for double-digit lending growth despite macro volatility.