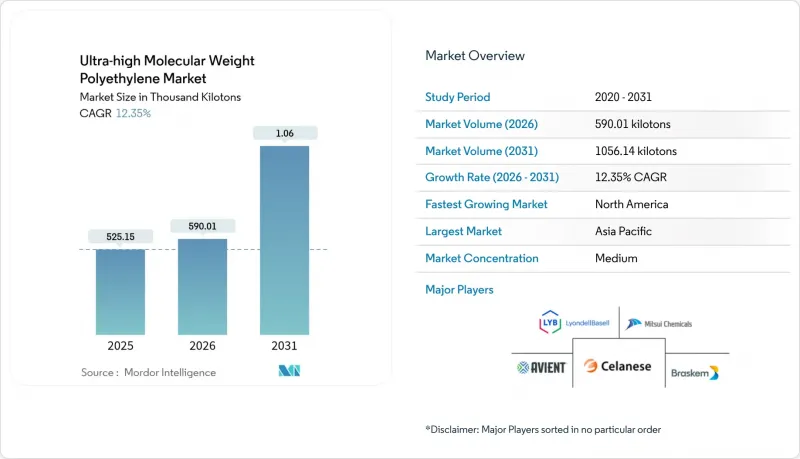

초고분자량 폴리에틸렌(UHMWPE) 시장은 2025년에 525.15킬로톤으로 평가되었고, 2026년 590.01 킬로톤에서 2031년까지 1056.14 킬로톤에 이를 것으로 예측되고 있습니다.

예측 기간(2026-2031년)의 CAGR은 12.35%로 추정됩니다.

이러한 성장 궤적은 배터리 분리막, 정형외과용 임플란트, 선박용 로프 등에 광범위하게 채택된 것을 반영하고 있으며, 이러한 응용 분야에서는 매우 긴 사슬 구조, 저마찰성, 생체적합성 등의 수지의 특성이 필수적입니다. 전기화 프로그램 확대, 관절 치환 수술 증가, 심해 인프라 구축이 수요를 촉진하고 있습니다. 생산업체들의 북미 공급 현지화 및 아시아태평양 확대 움직임은 리드 타임 단축, 물류 리스크 감소, 배터리 및 의료용 규격에 맞는 새로운 등급의 생산 능력 개발로 이어지고 있습니다. 지속가능성에 대한 요구로 인해 공급업체들은 에너지 소비를 줄이면서 초고분자량 특성을 유지하면서 바이오 에틸렌 생산 경로와 저온 가공 기술로 전환하고 있습니다.

전기차 배터리 제조업체들은 기존 폴리올레핀에서 초고분자량 폴리에틸렌(UHMWPE) 분리막으로 전환을 추진하고 있습니다. UHMWPE 세퍼레이터는 140℃ 이상에서도 치수 안정성을 유지하면서 더 얇은 필름화가 가능하여 에너지 밀도 향상에 기여하기 때문입니다. 미국 에너지부(DOE)가 지원하는 5,000만 달러 규모의 텍사스 프로젝트에서 브라스켐은 전용 배터리 등급 생산능력 2만 톤을 증설하고 250개의 숙련된 일자리를 창출할 예정입니다. 이는 초고분자량 폴리에틸렌(UHMWPE) 시장이 북미의 전기화 정책과 일치한다는 것을 보여줍니다. 해리쇄 기술을 채택한 분리막 라인은 전해액 흡수율을 15% 향상시키고 내부 저항을 감소시킵니다. 이는 장거리 주행 차량에 매우 중요한 특성입니다.

비타민 E 안정화 초고분자량 폴리에틸렌(UHMWPE) 수지는 산화 안정성이 뛰어나며, 1세대 가교 등급 대비 마모 파편 발생량을 42% 감소시킵니다. 이물질 감소는 임플란트 수명 연장으로 이어져 젊은 층의 고관절 및 슬관절 치환술에서 우선적으로 고려해야 할 사항입니다. 이러한 수지를 포함한 의료기기의 FDA 승인은 2024년 이후 꾸준히 증가하여 임상 현장의 신뢰성을 강화하고 초고분자량 폴리에틸렌(UHMWPE) 시장의 장기적인 성장을 확고히 하고 있습니다.

기존의 지글러-나타 방식은 반응기 온도를 약 250℃로 유지하며 고압 압출을 필요로 하기 때문에 스코프1 배출량이 증가합니다. 브라스켐의 사탕수수에서 추출한 에틸렌 생산 루트는 탄소 발자국을 60% 감소시키지만, 원료 비용이 12% 상승합니다. EU 바이어들은 바이오 유래 원료를 점점 더 중요시하고 있지만, 바이오매스 공급량의 제약으로 인해 규모 확대가 어려운 상황입니다.

분말은 2025년 총량의 44.63%를 차지하며 초고분자량 폴리에틸렌(UHMWPE) 시장의 근간을 이루고 있습니다. 100µ&m-150µ&m의 미립자 크기 조정으로 슈트 라이너 및 방탄판에 사용되는 압축 성형 시트의 균일한 소결을 보장합니다. 분말은 2031년까지 12.62%의 연평균 복합 성장률(CAGR)로 성장하여 섬유 및 필름을 능가할 것입니다. 이는 EV 분리막 제조업체가 분자량 분포의 좁은 분포를 요구하기 때문이며, 현재로서는 분말 제법만이 이를 보장할 수 있기 때문입니다.

이 부문은 점도 상승 없이 분자량을 1,000만 g/mol까지 끌어올리는 촉매기술의 발전으로 식품 가공기계용 로드의 고속 램 압출 성형이 가능해졌습니다. 따라서 분말 생산 능력에 대한 투자는 보다 광범위한 초고분자량 폴리에틸렌(UHMWPE) 시장 확대의 토대를 마련하고 있습니다. 두 번째 형태인 섬유는 선박 및 방위 분야 수요를 확보하고 있습니다. 한편, 시트 필름은 박막 분리막 시장에 침투하고 있습니다. 로드 및 튜브는 틈새 시장이지만, 내마모성 수명이 50,000시간 이상인 케미컬 펌프 용도에서 매우 중요한 역할을 합니다.

초고분자량 폴리에틸렌(UHMWPE) 보고서는 형태별(분말, 섬유, 시트/필름, 로드/튜브, 기타), 최종사용자 산업별(자동차, 항공우주/방위산업, 의료, 화학, 전자, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카), 지역별(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 킬로톤 단위로 제공됩니다.

아시아태평양은 2025년 44.55%의 점유율로 초고분자량 폴리에틸렌(UHMWPE) 시장을 주도했습니다. 이는 하류의 섬유 및 필름 공장에 원료를 공급하는 통합 석유화학 허브를 활용하고 있기 때문입니다. 중국의 '일대일로' 프로젝트는 새로운 항구에서 경량 및 내식성 로프에 대한 수요를 증가시키고 있으며, 일본의 의료기기 공급업체는 장기적인 분말 계약을 확보했습니다. 중국 및 일본 연안의 지역적 해상 풍력 발전의 확대는 심해 계류 라인의 섬유 소비를 더욱 증가시키고 있습니다.

북미는 2031년까지 연평균 복합 성장률(CAGR) 12.97%로 확대되어 세계에서 가장 빠른 속도를 유지할 것으로 예측됩니다. 연방정부의 특혜 조치로 인해 공급 리스크 감소를 목적으로 한 자사 전용 초고분자량 폴리에틸렌(UHMWPE) 라인을 핵심으로 하는 분리막 플랜트 3기 신설이 촉진되고 있습니다. 미국 에너지부(DOE)의 5,000만 달러의 보조금 지원을 받은 브라스켐의 텍사스 확장 계획은 국내 복귀의 모멘텀을 보여주며, 초고분자량 폴리에틸렌(UHMWPE) 시장이 배터리 밸류체인에서 전략적 가치를 가지고 있다는 것을 입증합니다.

유럽은 지속가능성을 중시하는 PFAS 대체와 적극적인 순환경제 목표에 따라 중간 수준의 한 자릿수 성장을 유지하고 있습니다. 독일에서는 의료용 라이너의 폐쇄형 루프 재생이 시범사업을 통해 입증되었으며, 이 지역의 재활용 원칙에 부합하는 노력이 진행되고 있습니다. 남미와 중동 및 아프리카은 신흥 시장이지만 전략적으로 중요한 시장이며, 브라질의 프리솔트 유전 시추 장비와 사우디아라비아의 석유화학 다각화로 인해 지역 고유의 용도가 개척되어 초고분자량 폴리에틸렌(UHMWPE)의 지역 시장 침투율이 점차 높아질 것으로 예측됩니다.

The Ultra-high Molecular Weight Polyethylene Market was valued at 525.15 kilotons in 2025 and estimated to grow from 590.01 kilotons in 2026 to reach 1056.14 kilotons by 2031, at a CAGR of 12.35% during the forecast period (2026-2031).

This trajectory reflects broad adoption in battery separators, orthopedic implants, and marine ropes, where the resin's distinct combination of very long chains, low friction, and biocompatibility is indispensable. Widening electrification programs, accelerated joint-replacement procedures, and deep-water infrastructure all reinforce demand. Producers' moves to localize supply in North America and expand in Asia-Pacific shorten lead-times, mitigate logistics risk, and unlock new capacity for grades tailored to battery and medical specifications. Sustainability mandates are pushing suppliers toward bio-based ethylene routes and lower-temperature processing technologies that cut energy intensity while preserving ultra-high molecular weight attributes.

Electric-vehicle cell makers are switching from conventional polyolefins to UHMWPE separators because the latter remain dimensionally stable above 140 °C while allowing thinner films that raise energy density. Braskem's USD 50 million DOE-backed project in Texas will add 20 kilo tons of dedicated battery-grade capacity and create 250 skilled jobs, underscoring the Ultra-high Molecular Weight Polyethylene market's alignment with North American electrification policy. Separator lines adopting disentangled-chain technology improve electrolyte uptake by 15% and cut internal resistance, attributes critical for longer-range vehicles.

Vitamin E-stabilized UHMWPE resins exhibit superior oxidative stability, reducing wear debris generation by 42% versus first-generation cross-linked grades. Lower debris translates into longer implant lifespans, a priority as younger patients undergo hip and knee replacements. FDA approvals for devices containing these resins have risen steadily since 2024, reinforcing clinical confidence and locking in long-term growth for the Ultra-high Molecular Weight Polyethylene market.

Traditional Ziegler-Natta pathways demand reactor temperatures near 250 °C and high-pressure extrusion, inflating Scope-1 emissions. Braskem's sugarcane-derived ethylene route offers a 60% lower carbon footprint but raises feedstock costs by 12%. EU buyers increasingly favor bio-attributed volumes, yet limited biomass availability restrains scale.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Powder accounted for 44.63% of the 2025 volume, making it the backbone of the Ultra-high Molecular Weight Polyethylene market. Tailored particle sizes between 100 µm and 150 µm ensure uniform sintering in compression-molded sheets used for chute liners and ballistic plates. Powder's 12.62% CAGR to 2031 outpaces fiber and film because EV separator producers prefer a tight molecular weight distribution that only powder routes currently guarantee.

The segment also benefits from catalyst advances that push molecular weight to 10 million g/mol without raising viscosity, enabling higher-speed ram-extrusion of rods for food-processing machinery. Investments in powder capacity, therefore, underpin broader Ultra-high Molecular Weight Polyethylene market expansion. Fibers, the second-largest form, secure marine and defense demand, while sheets and films penetrate thin-wall separators. Rods and tubes remain niche but critical for chemical pumps where wear life eclipses 50,000 hours.

The Ultra-High Molecular Weight Polyethylene Report is Segmented by Form (Powder, Fibers, Sheets and Films, Rods and Tubes, and Others), End-User Industry (Automotive, Aerospace and Defense, Medical, Chemical, Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilo Tons).

Asia-Pacific dominated the Ultra-high Molecular Weight Polyethylene market with a 44.55% share in 2025, leveraging integrated petrochemical hubs that feed downstream fiber and film plants. China's Belt and Road projects intensify demand for lightweight, corrosion-proof ropes in new ports, while Japan's medical-device suppliers secure long-term powder contracts. Regional offshore wind build-out along Chinese and Japanese coasts further multiplies fiber consumption for deep-water mooring lines.

North America is on track for a 12.97% CAGR up to 2031, the fastest globally. Federal incentives are catalyzing three new separator-film plants, each structured around captive UHMWPE lines to de-risk supply. Braskem's Texas expansion, supported by a USD 50 million DOE grant, illustrates domestic re-shoring momentum and underscores the Ultra-high Molecular Weight Polyethylene market's strategic value in battery supply chains.

Europe maintains mid-single-digit growth through sustainability-driven substitution of PFAS and aggressive circular-economy goals. Pilots in Germany demonstrate closed-loop reclaim of medical liners, aligning with the continent's recycling ethos. South America and MEA remain emerging but strategically significant, with Brazil's pre-salt rigs and Saudi petrochemical diversification opening localized applications that will gradually raise regional Ultra-high Molecular Weight Polyethylene market penetration.