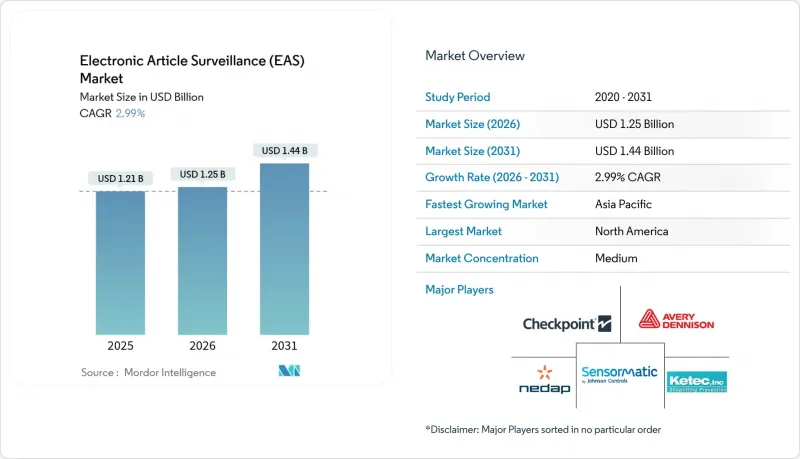

EAS(Electronic Article Surveillance) 시장은 2025년 12억 1,000만 달러에서 2026년에는 12억 5,000만 달러에 이르고, 2026-2031년 CAGR 2.99%로 성장을 지속하여 2031년까지 14억 4,000만 달러에 달할 것으로 예측됩니다.

이러한 측정된 확장은 기존의 받침대나 태그에서 융합형, 데이터 중심의 보안 생태계로의 전환을 반영하고 있습니다. 소매 업계는 2022년까지 전 세계적으로 1,121억 달러의 재고 감소 손실이 발생할 것으로 예상되며, 음향 자기식, 무선 주파수, RFID 기술을 융합한 손실 방지 기술에 대한 지속적인 자본 투입을 촉구하고 있습니다. 소비재 공장의 필수 소스 태깅 프로그램, 셀프 체크아웃 레인 도입, 전자기 형식에서 RF/RFID 하이브리드로의 전환이 결합되어 수요를 뒷받침하고 있습니다. 한편, 두 대기업이 연간 약 60억 개의 태그를 처리하는 독점 구조로 인해 일회용 태그의 가격은 0.05달러 전후로 안정되어 있습니다. 이는 신규 시장 진출기업에 대한 기술적, 유통적 장벽으로 작용하고 있습니다. 또한, 재활용 가능한 포장재와 탄소 저감 목표에 대한 규제 움직임은 제조 단계에서 배터리가 필요 없는 인쇄 가능한 라벨에 대한 투자를 촉진하고 있습니다.

많은 대형 체인점에서는 현재 매출의 평균 1.6%가 도난 손실로 발생하고 있으며, 경영진은 예방 예산의 50% 이상을 기업 분석 플랫폼에 데이터를 제공하는 기술에 투자할 수밖에 없는 상황입니다. 상품 단위의 RFID-EAS 태그는 게이트를 데이터 수집 장치로 전환하여 반복적으로 부정행위를 하는 사람을 식별하고 예측적 인사이트를 제공합니다. 월마트는 셀프 계산대에 AI가 탑재된 '스캔 누락' 감지 기능을 추가하여 전자물품감시 시장이 단순한 경보 시스템에서 손실의 격차를 줄이고 재고 정확도를 향상시키는 다중 센서 인텔리전스 계층으로 변모하고 있음을 보여주고 있습니다.

세계 FMCG 공급업체들은 공장 라인에서 직접 태그를 삽입하여 대량 생산 효율성과 위치의 일관성을 확보하여 오경보를 최소화하고 있습니다. 센서매틱 솔루션즈는 멕시코 마타모로스에 RFID 서비스 스테이션을 확장하여 북미 브랜드를 위한 국내 인코딩된 태그 생산 능력을 제공하게 되었습니다. 소매업체는 매장 내 인건비 절감과 감지율 향상이라는 이점을 얻을 수 있으며, 컨버터는 재활용 포장에 적합한 재생 가능 재료를 활용할 수 있습니다.

완전한 통합을 위해서는 고밀도 리더 그리드, 기업용 소프트웨어, 직원 재교육이 필요하며, 중형 체인점에서는 50만 달러가 넘을 수도 있습니다. 소매업체는 단계적 도입 기간 동안 기존 EM 장비와 병행하여 RF 게이트를 운영해야 하므로 실질적으로 운영 비용이 두 배로 증가하게 됩니다. 통합에는 18-24개월이 소요되며, GS1 데이터 모델과의 정합성이 요구됩니다. 예산 제약으로 인해 신흥국의 업그레이드가 지연되고 기술 비용이 점차 감소하고 있음에도 불구하고, 전자물품감시(EAS) 시장의 성장 전망은 둔화되고 있습니다.

2025년에도 태그는 53.92%의 점유율을 유지하며 모든 형태의 기본 감지 요소로서의 역할을 강조하고 있습니다. 소스 태깅은 현재 생산 공정에서 하드 태그나 인레이를 삽입하여 입고 시 처리 효율을 향상시키는 방식이 수량 기준으로 80% 이상을 차지하고 있습니다. 라벨 및 세이퍼는 규모는 작지만 인쇄 가능한 RFID-EAS 인레이가 지속가능성과 보안을 동시에 만족시키면서 4.52%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 에칭 처리된 알루미늄 회로에 비해 70-90% 낮은 CO2 배출량은 소매업체의 탄소 저감 목표의 핵심으로 자리 잡고 있습니다. 따라서 전자물품감시(EAS) 시장에서 라벨 시장 규모는 구성 요소 중 가장 빠르게 성장할 것으로 예측됩니다. 안테나의 업그레이드는 매장 리뉴얼 및 하이브리드 방식 전환에 따른 것이며, 셀프 계산대와 연동된 자동 탈착기 및 디액티베이터가 관련 수요를 견인할 것으로 보입니다.

2세대 분리기는 듀얼 테크놀로지를 지원하여 마찰 없는 반품 처리와 옴니채널 주문 수령을 실현합니다. 통합기는 안테나와 데이터 분석 대시보드가 표준으로 번들로 제공되며, 알람 이벤트와 트래픽 카운터를 시각화합니다. 이를 통해 제공 가치가 하드웨어에서 SaaS(Software as a Service)로 승화됩니다. 이러한 부가가치 계층과 공장 내장형 인레이가 결합되어 태그 공급망의 2대 기업 체제를 강화하는 동시에 소매업체의 총 소유비용을 예측 가능한 범위로 유지합니다.

북미는 2025년 매출의 33.72%를 차지하며 1위를 유지했습니다. 이는 EAS 도입의 선구자 역할을 한 체인점들과 의약품의 품목단위 추적관리를 의무화한 연방정부의 가이드라인이 주도한 결과입니다. 게이트 업그레이드에서는 영상 분석과 트래픽 카운터를 통합하여 기업 대시보드에 정보를 제공합니다. 이로써 EAS의 유용성은 경보 발생 기능을 넘어선 영역으로 확장되고 있습니다. 멕시코가 태그 변환 거점으로 부상하고 있는 것은 지역 통합의 진전을 보여주는 것으로, 센서매틱의 마타모로스 지사가 미국 의류 라인에 인코딩된 RFID 인레이를 공급하고 있습니다. 한편, 캐나다 식료품 업계에서는 셀프 계산대 도입에 따른 상품 감소를 억제하기 위해 하이브리드 RFID 도입을 확대하고 있습니다.

아시아태평양은 3.84%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 중국은 국내 안테나 및 태그 공장이 아세안 소매업체에 수출함으로써 지역 전체 물량을 뒷받침하고 있습니다. RFID 초기 도입 국가인 일본과 한국에서는 EAS 이벤트와 상품 판매 분석을 연계하는 클라우드 네이티브 분석을 도입하여 하드웨어 설치와 연동된 소프트웨어 수익원을 가속화하고 있습니다. 인도에서는 의류 프랜차이즈와 대형 식료품점을 포함한 조직화된 소매업의 확장이 새로운 시장 기회를 창출하고 있으며, 지역 전체에서 전자물품감시 시장 규모를 확대하고 있습니다.

유럽에서는 재활용 가능한 인레이 형태를 장려하는 지속가능성 규제로 인해 안정적인 성장세를 보이고 있습니다. 소매업체는 EU의 순환 경제 지침을 준수하기 위해 종이 기반 안테나로 제조된 라벨을 채택하고 있습니다. 독일과 프랑스는 조직적 소매 범죄에 대응하기 위한 국가 행동 계획을 추진하고 있으며, AI 대응형 페데스탈에 대한 투자를 촉진하고 있습니다. 네덜란드, 벨기에, 프랑스에서는 HEMA사의 740개 매장에 RFID 도입이 진행되어 대륙별 확산과 개별 게이트에서 통합 재고 시각화 시스템으로의 전환이 이루어지고 있습니다. 남유럽의 패션 체인들은 EAS(전자물품감시) 업그레이드를 옴니채널 대응 전략과 연동하여 이러한 움직임을 따르고 있습니다.

The Electronic Article Surveillance market is expected to grow from USD 1.21 billion in 2025 to USD 1.25 billion in 2026 and is forecast to reach USD 1.44 billion by 2031 at 2.99% CAGR over 2026-2031.

The measured expansion reflects the shift from traditional pedestals and tags to convergent, data-centric security ecosystems. Retailers are confronting USD 112.1 billion in global shrink losses reported for 2022, prompting sustained capital allocation toward loss-prevention technologies that fuse acousto-magnetic, radio-frequency and RFID capabilities. Mandatory source-tagging programs at consumer-goods plants, the roll-out of self-checkout lanes and the phasing-out of electromagnetic formats in favor of RF/RFID hybrids collectively underpin demand. At the same time, a duopoly structure-two players process about 6 billion tags each year-keeps pricing for disposable tags near USD 0.05 while erecting technical and distribution barriers for new entrants. Regulatory pushes for recyclable packaging and carbon-reduction targets further steer investment toward battery-free printable labels embedded at the point of manufacture.

Shrink now averages 1.6% of sales for many large chains, forcing executives to devote more than 50% of prevention budgets to technology that feeds data into enterprise analytics platforms. Item-level RFID-EAS tags convert gates into data collectors that flag repeat offenders and generate predictive insights. Walmart added AI-enabled "missed-scan" detection at self-checkout bays, demonstrating how the Electronic Article Surveillance market is morphing from a simple alarm system into a multi-sensor intelligence layer that closes loss gaps while improving inventory accuracy.

Global FMCG suppliers embed tags directly on the factory line, driving volume efficiencies and consistent placement that minimizes false alarms. Sensormatic Solutions expanded its RFID service bureau in Matamoros, Mexico, giving North American brands on-shore capacity for encoded tag production. Retailers benefit through labor-savings at the store and improved detection rates, whereas converters leverage recyclable substrates that comply with circular-packaging commitments.

Complete convergence demands dense reader grids, enterprise software and staff re-training that can exceed USD 500,000 for mid-sized chains. Retailers must often run RF gates in parallel with legacy EM equipment during phased roll-outs, effectively doubling operating costs. Integration timelines stretch 18-24 months and require GS1 data-model alignment. Budget constraints delay upgrades across emerging economies, tempering the Electronic Article Surveillance market growth outlook even as technology costs gradually decline.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Tags retained 53.92% share in 2025, underlining their role as the fundamental detection element across all formats. Source-tagging now covers more than 80% of volume, embedding hard tags or inlays during production and lifting throughput at receiving docks. Labels and Safers, though smaller, are on track for a 4.52% CAGR as printable RFID-EAS inlays marry sustainability and security; 70-90% lower CO2 output compared with etched-aluminium circuits places them at the center of retailer carbon pledges. The Electronic Article Surveillance market size for Labels is therefore projected to widen most rapidly within the component mix. Antenna upgrades follow store refurbishments and hybrid conversions, while automated detachers and deactivators tied to self-checkout kiosks lift ancillary demand.

Second-generation detachers now accommodate dual-technology tags, enabling frictionless returns processing and omnichannel order pick-ups. Integrators routinely bundle antennas with data-analytics dashboards that visualise alarm events alongside traffic counters, elevating the offer from hardware to software-as-a-service. These value-add layers, together with factory-embedded inlays, reinforce the duopolistic tag supply chain yet keep total cost of ownership predictable for retailers.

Electronic Article Surveillance Market Report is Segmented by Component (Tags, Antennas, Deactivators/Detachers, and More), Technology (Acousto-Magnetic AM, Electromagnetic EM, and More), End-User (Apparel and Fashion Accessories, Cosmetics and Pharmacies, Supermarkets/Hypermarkets/Mass-Merchandisers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led with 33.72% of 2025 revenue, propelled by chains that pioneered EAS adoption and by federal guidelines requiring item-level track-and-trace for pharmaceuticals. Gate upgrades integrate video analytics and traffic counters that feed enterprise dashboards, extending EAS usefulness beyond alarm generation. Mexico's emergence as a tag conversion hub underlines regional integration as Sensormatic's Matamoros bureau supplies encoded RFID inlays to United States garment lines. Canada's grocery sector, meanwhile, scales hybrid RFID roll-outs to curb shrink tied to self-checkout adoption.

Asia-Pacific is the fastest-growing territory at 3.84% CAGR. China anchors regional volume with domestic antenna and tag plants that export to ASEAN retailers. Japan and South Korea, early RFID adopters, deploy cloud-native analytics that tie EAS events to merchandising insights, accelerating software revenue streams linked to hardware installations. India's organised retail expansion, including apparel franchises and large-format grocery, adds greenfield opportunities that lift the Electronic Article Surveillance market size across the region.

Europe steadies growth through sustainability regulations that reward recyclable inlay formats. Retailers adopt labels fabricated from paper-based antennas to comply with the EU's circular-economy directives. Germany and France pursue national action plans against organised retail crime, spurring investments in AI-ready pedestal replacements. The Netherlands, Belgium and France host a 740-store RFID roll-out at HEMA, illustrating continental scale and the pivot from stand-alone gates to integrated inventory visibility. Southern Europe catches up through fashion chains that align EAS upgrades with omnichannel fulfilment strategies.