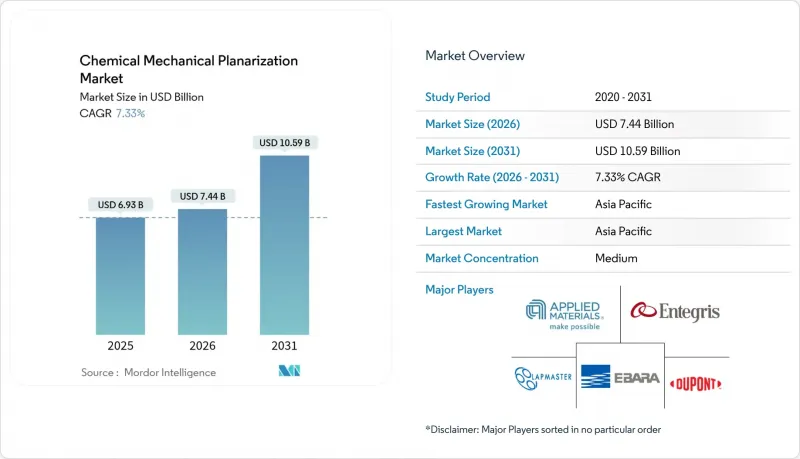

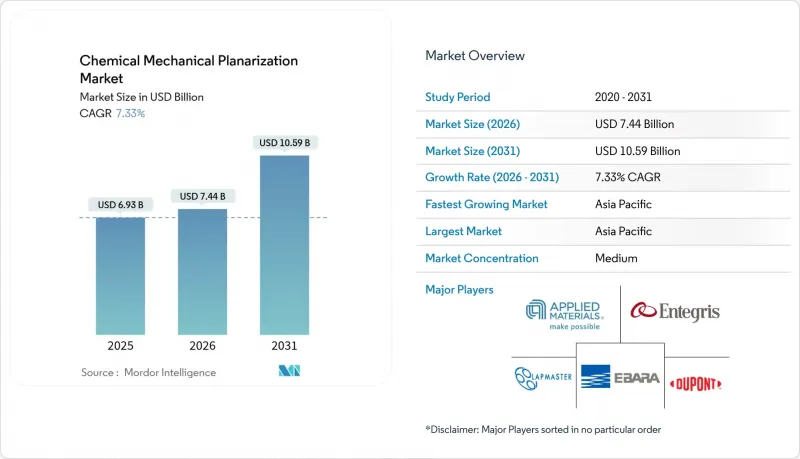

화학적 기계 연마(CMP) 시장 규모는 2025년 69억 3,000만 달러에서 2026년 74억 4,000만 달러로 성장이 전망됩니다.

2031년에는 105억 9,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 7.33%를 나타낼 전망입니다.

이러한 성장은 FinFET에서 GAA(Gate All Around) 트랜지스터로의 전환, 3D 집적화, 전력 소자에서 실리콘 카바이드(SiC)와 질화갈륨(GaN)의 사용 증가에 의해 주도되고 있습니다. 파운드리는 지속적으로 대규모 생산 능력 증설을 추진하고 있으며, 미국과 유럽연합(EU)의 정부 인센티브는 현지 CMP 공급망을 촉진하고 있습니다. 장비 공급 부족은 생산 확대를 제약하는 반면, 지속가능성에 대한 노력은 저연마제 및 무연마제 슬러리에 대한 수요를 가속화하고 있습니다. 지정학적 수출 규제가 장비의 흐름을 재구성하고, 유럽과 미국, 중국 벤더들 간의 병행적인 기술 혁신의 흐름을 촉진하고 있습니다.

GAA(Gate All Around) 트랜지스터는 높은 선택적 제거율과 엄격한 결함 임계값을 요구하는 새로운 금속 게이트 스택을 도입함으로써 CMP 화학물질의 특성을 변화시키고 있습니다. 주요 파운드리 업체들은 3nm 이하 GAA 노드 양산을 계획하고 있으며, 고도의 엔드포인트 제어가 가능한 300mm 단결정 연마기의 장비 갱신 주기를 추진하고 있습니다. 실리콘 관통 비아 등 보완적인 3D 집적 기술에서는 여러 웨이퍼 표면에 걸쳐 초평탄한 구리 층이 요구됩니다. 따라서 CMP 플랫폼은 폐쇄 루프 패드 조정과 실시간 슬러리 모니터링을 통합하여 더 엄격한 공차에서도 수율을 유지합니다.

탄화규소 및 질화갈륨 웨이퍼는 경도와 화학적 불활성 특성으로 인해 연마 시간과 소모품 비용이 크게 증가합니다. 알칼리성 화학물질과 설계된 연마제를 사용한 전용 슬러리를 사용하여 표면 거칠기를 0.05nm 이하로 유지하면서 1µ&m/h에 가까운 제거율을 달성하고 있습니다. 자동차의 전동화로 인해 이러한 재료에 대한 수요가 가속화됨에 따라 공구 제조업체는 SiC 라인과 기존 실리콘 라인 사이의 연마 마모 및 교차 오염 방지를 위한 패드 설계를 출시하고 있습니다.

산화세륨, 과산화수소 등 고순도 원료는 희토류 공급이 부족하거나 화학공장이 유지보수에 들어가면 가격이 급등합니다. 미국 지질조사국에 따르면 중국은 여전히 희토류 수입의 주요 공급원이며, 세계 슬러리 공급업체는 무역 마찰의 영향을 받기 쉬운 상황에 처해 있습니다. 벤더는 연마제 부하를 줄인 슬러리를 재배합하거나 여과 루프를 통해 사용한 용액을 재활용하는 방식으로 대응하고 있습니다.

2025년 화학적 기계 연마(CMP) 시장 규모의 62.78%를 장비가 차지했습니다. 지출은 웨이퍼 내 불균일성을 1nm 이하로 억제하고 패드 표면 상태 관리를 위한 폐쇄 루프 조정 기능을 통합한 단일 웨이퍼 장비에 집중되어 있습니다. 이 부문은 GAA 공정과 와이드밴드갭 기판을 지원하는 새로운 플랫폼 팹의 도입으로 2031년까지 연평균 복합 성장률(CAGR) 7.54%를 나타낼 것으로 예측됩니다. 동시에 7nm 이하 공정 노드에서 나노 스케일 결함 제거를 위해 세정 모듈의 업그레이드도 진행되고 있습니다.

소모품은 매출의 37.22%를 차지하며, 정기적인 수요가 안정적인 수요를 보장하는 슬러리가 주도하고 있습니다. 실리카계 유전체 슬러리가 주류인 반면, 틈새 시장인 세리아 배합은 유리와 사파이어 연마에 대응합니다. 패드 공급업체는 홈이 있는 폴리머 블렌드를 출시하여 수명 연장에 따른 제거율의 안정적 유지와 결함 발생을 최소화하고 있습니다. 지속가능성 목표의 진전은 저마모성 화학물질로의 전환을 가속화할 것이며, 소모품 공급업체는 성능과 환경 지표를 모두 충족할 때 프리미엄 가격을 책정할 수 있습니다.

아시아태평양은 2025년 매출의 64.12%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 8.41%를 나타낼 것으로 예측됩니다. 중국 본토의 현지화 추진으로 적극적인 웨이퍼 공장 건설이 진행되는 반면, 대만은 최첨단 로직 및 첨단 패키징 분야에서 주도권을 유지하고 있습니다. 한국은 고층수 3D NAND 및 DRAM에 대한 투자를 확대하고 있으며, 유전체 및 금속 평탄화 능력에 대한 수요를 높이고 있습니다. 일본 공급업체들은 초순수 화학물질과 정밀 패드 분야에서 수십년동안 쌓아온 전문성을 바탕으로 이 지역의 수직 통합형 생태계를 강화하고 있습니다.

북미는 매출 규모에서 2위를 차지하고 있습니다. 연방정부의 우대 조치로 새로운 팹 건설이 실현되고, 고객이 안전한 공급망을 우선시하는 가운데 국내 장비 제조업체들이 중요한 수주를 따내고 있습니다. 애리조나 주와 뉴욕주의 선진적인 패키징 노력은 현지 조달 규칙을 준수하는 CMP 소모품에 대한 지역 수요를 자극하고 있습니다. 수출 규제로 인한 중국향 하이엔드 패드 출하 제한으로 시장이 양분되어 북미 CMP 벤더의 전략적 가치가 높아지고 있습니다.

유럽은 2030년까지 세계 반도체 생산량의 20%를 목표로 하고 있으며, 제조의 지속가능성을 중시하고 있습니다. 지역 소재 제조업체는 전자 등급 과산화수소 및 특수 슬러리 생산 능력을 확장하고, 독일과 네덜란드 장비 제조업체는 CMP 제품을 EU 환경 지침에 맞게 조정하고 있습니다. 정부 자금의 헤테로 통합 파일럿 라인 지원은 연구 거점 및 특수 파운드리에서 CMP 장비의 단계적 도입을 촉진하고 있습니다.

Chemical mechanical planarization market size in 2026 is estimated at USD 7.44 billion, growing from 2025 value of USD 6.93 billion with 2031 projections showing USD 10.59 billion, growing at 7.33% CAGR over 2026-2031.

Growth is propelled by the transition from FinFET to gate-all-around (GAA) transistors, 3D-integration, and the rising use of silicon carbide (SiC) and gallium nitride (GaN) in power devices. Foundries continue large-scale capacity additions, and government incentives in the United States and European Union encourage local CMP supply chains. Tight tool availability constrains production ramps, while sustainability initiatives accelerate demand for low-abrasive and abrasive-free slurries. Geopolitical export controls reshape equipment flows and spur parallel innovation tracks between Western and Chinese vendors.

Gate-all-around transistors alter CMP chemistries by introducing new metal gate stacks that require highly selective removal rates and tighter defectivity thresholds. Leading foundries have scheduled volume production of GAA nodes below 3 nm, driving an equipment refresh cycle for 300 mm single-wafer polishers with advanced endpoint control. Complementary 3D-integration techniques, such as through-silicon vias, demand ultra-flat copper layers across multiple wafer surfaces. CMP platforms, therefore, integrate closed-loop pad conditioning and real-time slurry monitoring to sustain yields at ever-smaller tolerances .

Silicon carbide and gallium nitride wafers exhibit hardness and chemical inertness that multiply polish times and consumable costs. Dedicated slurries using alkaline chemistries and engineered abrasives now achieve removal rates near 1 µm/h while holding surface roughness below 0.05 nm. Automotive electrification accelerates demand for these materials, prompting tool makers to release pad designs resilient to abrasive wear and cross-contamination shielding between SiC and traditional silicon lines.

Cerium oxide, hydrogen peroxide, and other high-purity inputs show price spikes when rare-earth supply tightens or chemical plants undergo maintenance. The U.S. Geological Survey notes China remains the main source of rare-earth imports, leaving global slurry vendors exposed to trade disputes . Vendors respond by reformulating slurries with lower abrasive loads and recycling spent solutions through filtration loops.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Equipment represented 62.78% of the chemical mechanical planarization market size in 2025. Spending concentrates on single-wafer tools that deliver within-wafer non-uniformity below 1 nm and integrate closed-loop conditioning for pad surface health. The segment is forecast to rise at a 7.54% CAGR to 2031 as fabs install new platforms that support GAA processes and wide-bandgap substrates. Cleaning modules undergo concurrent upgrades to remove nanoscale defects at sub-7 nm nodes.

Consumables account for 37.22% of revenue, led by slurries whose recurring nature ensures stable demand. Silica-based dielectric slurries dominate, while niche ceria formulas address glass and sapphire polishing. Pad suppliers release grooved polymer blends that sustain consistent removal rates and minimize defectivity over extended pad life. Sustainability goals accelerate the shift to low-abrasive chemistries, positioning consumables vendors for premium pricing when performance and environmental metrics converge.

The Chemical Mechanical Planarization Market Report is Segmented by Product Type (CMP Equipment, CMP Consumables), Application (Integrated Circuit, Compound Semiconductor, MEMS and NEMS, Advanced Packaging, Other Applications), End-User (Foundries, Idms, OSAT, R&D Institutes/Universities), and Geography (North America, Europe, Asia Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific generated 64.12% of 2025 revenue and is projected to record an 8.41% CAGR through 2031. Mainland China's localization push prompts aggressive wafer-fab construction, while Taiwan retains leadership in cutting-edge logic and advanced packaging. South Korea invests in high-layer count 3D NAND and DRAM, boosting demand for dielectric and metal planarization capacity. Japanese suppliers leverage decades-long expertise in ultrapure chemicals and precision pads, reinforcing the region's vertically integrated ecosystem.

North America ranks second by revenue. Federal incentives have unlocked new fab commitments, and domestic equipment leaders capture significant orders as customers prioritize secure supply chains. Advanced packaging initiatives in Arizona and New York stimulate regional demand for CMP consumables that comply with local content rules. Export controls limit high-end pad shipments to China, creating a bifurcated market and heightening strategic value for North American CMP vendors.

Europe pursues 20% global semiconductor output by 2030, emphasizing manufacturing sustainability. Regional materials firms expand electronics-grade hydrogen peroxide and specialty slurry capacity, while equipment makers in Germany and the Netherlands align CMP offerings with EU environmental directives. Government funding supports pilot lines for heterogeneous integration, driving incremental CMP tool installations across research hubs and specialty foundries.