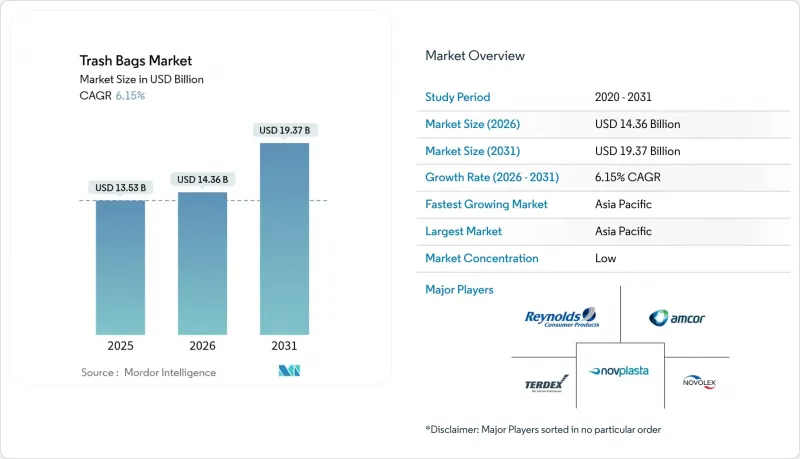

쓰레기봉투 시장은 2025년에 135억 3,000만 달러로 평가되었으며, 2026년 143억 6,000만 달러에서 2031년까지 193억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 6.15%로 예상됩니다.

급속한 도시화로 인해 도시 고형 폐기물의 양이 증가하는 한편, 종량제 쓰레기 처리 제도(PAYT)와 생산자책임제도의 강화로 제품 사양이 재정의되면서 고품질, 규제에 부합하는 라이너에 대한 수요가 증가하고 있습니다. 아시아태평양은 중산층 인구 증가와 인프라 구축의 혜택을 누리고 있는 가장 큰 지역 소비자입니다. 북미와 유럽의 성숙한 시장에서는 일회용 플라스틱 규제에 대한 압력으로 인해 재생 플라스틱 및 바이오 기반 필름 등급으로의 전환이 가속화되고 있습니다. 동시에 에틸렌 가격의 변동은 컨버터의 수익률을 계속 압박하고 있으며, 생산자 간의 통합이 진행되고 있습니다.

도시 고형 폐기물의 양은 2023년 21억 톤에 달할 것이며, 2050년에는 38억 톤에 달할 것으로 예상됩니다. 도시 지역에서는 현재 자동화 수거 차량에 대응하는 펑크 방지 및 균일성 라이너가 지정되어 쓰레기봉투 시장의 성장을 촉진하고 있습니다. IoT 지원 쓰레기통과 AI 경로 최적화를 결합한 파일럿 프로젝트에서 연료 사용량을 28% 절감하고 수거 효율을 41.5% 향상시켰습니다. 이러한 변화로 인해 고온 기후에서도 형태를 유지하고 장기 보관에 따른 열화를 견딜 수 있는 필름에 대한 수요가 증가하고 있습니다.

2024년 병원이 매립을 피한 폐기물은 2억 6,410만 파운드(약 119만 톤)에 달하며, 68%는 지속가능한 조달 규칙을 도입했습니다. 이에 따라 기관 구매 부서에서는 항균 및 탈취 기능이 있는 라이너를 우선시하는 경향이 강해지고 있습니다. 이 수요를 잡기 위해 2025년에는 달걀껍질 배합 EGU 가방과 같은 프리미엄 SKU가 등장했습니다. 호텔 산업에서도 비슷한 추세를 보이며 평균 판매 가격을 끌어올려 기관 부문 CAGR 9.67%를 견인하고 있습니다.

캘리포니아주 SB 54 법안은 2032년까지 일회용 플라스틱을 25% 감축할 것을 의무화하고, 연간 5억 달러의 청소 자금을 요구하고 있습니다. 영국과 유럽연합(EU)의 유사한 규제는 폐기 비용을 생산자에게 전가하고, 재생 가능 재료와 퇴비화 가능한 대체품에 대한 투자를 장려하고 있습니다. 컴플라이언스의 복잡성은 비용을 높이고, 저마진 공급업체의 진입을 제한하며, 쓰레기봉투 시장의 단기적 확장을 억제하고 있습니다.

의료기관, 숙박시설, 교육기관 등 기관 사용자가 주도하고 있으며, 2025년 매출의 63.78%를 차지하는 주거 부문에도 불구하고 2031년까지 연평균 성장률(CAGR)은 9.58%에 달할 것으로 예상됩니다. 병원의 지속가능한 조달 정책과 엄격한 감염 관리 프로토콜은 쓰레기봉투 시장에서 항균 및 누출 방지 라이너에 대한 수요를 주도하고 있습니다. 기관 구매자는 가격보다 성능과 규제 적합성을 중시하며, 재생 소재 및 바이오 기반 소재를 사용한 프리미엄 SKU를 지지하고 있습니다. 주택 수요는 여전히 물량 주도형이며, PAYT 프로그램과 브랜드 로열티에 의해 뒷받침되고 있지만, 높은 가격 민감도에 의해 제약받고 있습니다.

기관 시장의 급격한 성장에 따라 공급업체들은 사양 기반의 제품 제공을 정교화하고 다년 계약을 확보하는 데 주력하고 있습니다. 동시에 가정용 구매층에서는 향기나 강화형 봉지로의 교체가 진행되어 평균 단가가 상승하고 있습니다. 지자체에서 분리수거를 추진함에 따라 두 사용자층 모두 인증된 컬러 코드 라이너를 채택하는 움직임이 확산되면서 쓰레기봉투 시장은 더욱 확대되고 있습니다.

2025년 기준, LDPE는 가격 측면과 제조 공정의 숙련도로 인해 쓰레기봉투 시장에서 가장 큰 38.41%의 점유율을 차지했습니다. 그러나 PLA, PHA 등 바이오 기반 플라스틱은 기업들의 순 제로화 약속과 네이처웍스의 태국 내 3억 5,000만 달러 규모의 PLA 공장 건설 등 투자를 계기로 CAGRCAGR 10.42%로 확대될 것으로 예상됩니다. 퇴비화 가능한 등급은 분해 속도가 느린 습한 열대 지역에서는 여전히 보급이 늦어지고 있지만, 규제상의 특혜로 인해 비용 차이가 줄어들고 있습니다. 한편, HDPE와 LLDPE 필름은 시장에서의 입지를 유지하기 위해 사용 후 재생수지의 배합을 추진하고 있습니다.

설비 업그레이드 및 인증 획득 장벽이 소재 전환의 가속화를 억제하고 있으며, 매립세 및 EPR(확대된 생산자책임재활용) 비용 상승으로 인해 화석 유래 수지의 비용 우위성은 지속적으로 감소하고 있습니다. 재활용 가능한 소재와 기계적 강도를 모두 갖춘 공급업체는 지속가능한 대체품으로 확대되고 있는 쓰레기봉투 시장을 선점할 수 있는 가장 유리한 위치를 점하고 있습니다.

아시아태평양은 2025년 세계 매출의 40.32%를 차지했으며, 중국과 인도의 도시 확장 및 중산층 소비 확대에 힘입어 2031년까지 연평균 8.05%의 성장률을 기록할 것으로 전망됩니다. 한국과 일본에서는 AI 탑재 분리수거 로봇이 재생 HDPE 공급량 증가에 기여하는 반면, 열대성 기후는 퇴비화 봉투의 도입을 복잡하게 만들고 있습니다. 각 국가마다 서로 다른 금지 조치와 재활용 목표가 설정되어 있기 때문에 전 세계 공급업체들은 유연한 조달 전략이 요구됩니다.

북미에서는 캘리포니아주 SB54와 같은 생산자책임재활용(EPR) 확대법에 따라 성숙한 인프라가 계속 발전하고 있으며, 재생 소재 및 바이오 기반 라이너로의 전환이 진행되고 있습니다. 6,000개 지자체에서 도입된 종량제 쓰레기 수거 제도(PAYT)는 인증된 봉투의 크기가 규정되어 있어 안정적인 단위 수요를 뒷받침하고 고부가가치 제품의 구성비 향상에 기여하고 있습니다. 2025년 4월에 출시된 Glad사의 2배 강도 가방 등 위생에 대한 의식이 높은 가정을 위한 프리미엄 제품도 등장하고 있습니다.

유럽에서는 순환형 경제정책이 추진되면서 재활용 소재 사용률의 적극적인 의무화가 진행되고 있습니다. 독일의 재사용 풀 제도와 프랑스에서 도입 예정인 보증금 반환 제도는 폐기물 감축을 위한 지역 전체의 움직임을 상징합니다. 사이카 플렉스와 같은 포장재 제조업체들은 현재 최소 5%의 PCR(Post-Consumer Recycled Material)을 포함한 100% 재활용 가능한 필름을 판매하고 있으며, 이는 유럽이 지속가능성 기준의 지표로 자리매김하고 있습니다.

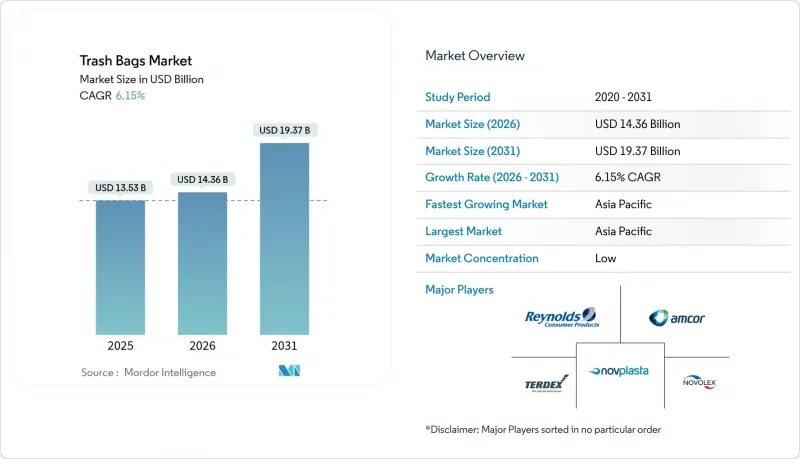

The trash bags market was valued at USD 13.53 billion in 2025 and estimated to grow from USD 14.36 billion in 2026 to reach USD 19.37 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

Rapid urbanization is swelling municipal solid-waste volumes, while pay-as-you-throw (PAYT) schemes and stricter producer-responsibility rules are redefining product specifications and boosting demand for premium, compliant liners. Asia-Pacific remains the largest regional consumer, benefitting from expanding middle-class populations and infrastructure upgrades. Mature markets in North America and Europe, pressured by single-use-plastic curbs, are accelerating shifts toward recycled and bio-based film grades. At the same time, volatile ethylene pricing continues to squeeze converter margins, reinforcing consolidation among producers.

Municipal solid-waste volumes reached 2.1 billion t in 2023 and are on track for 3.8 billion t by 2050. Cities now specify puncture-resistant, uniform liners compatible with automated trucks, spurring growth of the trash bags market. IoT-enabled bins paired with AI route optimization have cut fuel use 28% and lifted collection efficiency 41.5% in pilot projects. These shifts increase demand for films that hold shape in high-heat climates and resist extended storage degradation.

Hospitals diverted 264.1 million lb of waste from landfills in 2024, and 68% adopted sustainable purchasing rules, pushing institutional buyers toward antimicrobial, odor-neutralizing liners. Premium SKUs such as eggshell-infused EGU bags debuted in 2025 to capture this demand. Similar trends in hospitality are lifting average selling prices and underpinning the institutional segment's 9.67% CAGR.

California's SB 54 compels a 25% cut in single-use plastics by 2032 and requires USD 500 million in annual cleanup funding. Similar mandates in British Columbia and the EU shift disposal costs to producers, forcing investments in recycled content and compostable alternatives. Compliance complexity elevates costs and limits access for low-margin suppliers, restraining near-term expansion of the trash bags market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Institutional users-healthcare, hospitality and education-propelled 9.58% CAGR to 2031, even as the residential segment retained 63.78% of 2025 revenue. Hospitals' sustainable procurement policies and stricter infection-control protocols are driving demand for antimicrobial, leak-proof liners in the trash bags market. Institutional buyers value performance and compliance over price, supporting premium SKUs with recycled or bio-based content. Residential demand remains volume-driven, buoyed by PAYT programs and brand loyalty but constrained by price sensitivity.

The institutional upsurge encourages suppliers to refine spec-based offerings and secure multi-year contracts. At the same time, household buyers increasingly trade up to scented or reinforced bags, expanding average unit values. As city governments introduce differentiated collection streams, both user groups are turning to certified color-coded liners, further enlarging the trash bags market.

LDPE held the largest 38.41% trash bags market share in 2025 thanks to price and process familiarity. Yet bio-based plastics such as PLA and PHA are poised for 10.42% CAGR, catalyzed by corporate net-zero pledges and investments like NatureWorks' USD 350 million PLA plant in Thailand. Compostable grades still lag in humid tropics where degradation rates slow, but regulatory incentives are narrowing cost gaps. HDPE and LLDPE films, meanwhile, are integrating post-consumer resin to maintain market relevance.

Equipment upgrades and certification hurdles are tempering a swift material shift, yet rising landfill levies and EPR fees continue to erode the cost advantage of fossil-based resins. Suppliers that can merge circular content with mechanical strength are best positioned to capture the expanding trash bags market size for sustainable variants.

The Trash Bags Market Report is Segmented by End-User (Residential, Institutional, Commercial and Industrial), Material Type (HDPE, LDPE, LLDPE, Bio-based/Biodegradable Plastics), Capacity/Bag Size (Up To 10 Gallon, 13-30 Gallon, 30-55 Gallon, Above 55 Gallon), Sales Channel (Retail, B2B/Institutional Procurement, Distribution/Wholesale), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated 40.32% of global revenue in 2025 and is on track for an 8.05% CAGR to 2031, driven by urban sprawl in China and India and widening middle-class consumption. AI-enabled sorting robots in South Korea and Japan are lifting recycled-HDPE availability, while tropical climates complicate compostable-bag deployment. Diverse national bans and recycling targets require flexible sourcing strategies for global suppliers.

North America's mature infrastructure is evolving under EPR legislation such as California's SB 54, prompting a pivot to recycled and bio-based liners. PAYT programs in 6,000 communities now dictate certified bag sizes, underpinning stable unit demand and supporting a higher-value mix. Premium innovations, including Glad's 2X stronger bags launched in April 2025, cater to hygiene-aware households.

Europe's circular-economy agenda is spurring aggressive recycled-content mandates. Germany's reuse pools and France's incoming deposit-return schemes exemplify region-wide momentum toward waste reduction. Packaging groups such as Saica Flex now market 100% recyclable films with minimum 5% PCR, consolidating Europe's position as a bellwether for sustainable standards.