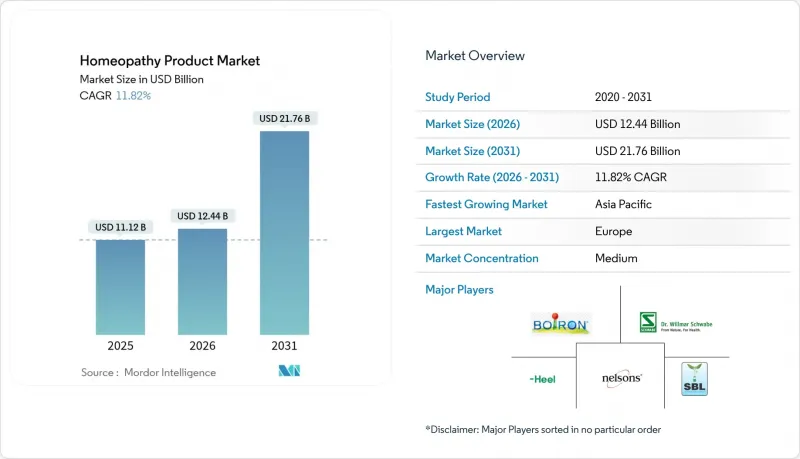

동종요법 제품 시장 규모는 2026년에는 124억 4,000만 달러로 추정되며, 2025년 111억 2,000만 달러에서 성장이 전망됩니다.

2031년에는 217억 6,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 11.82%로 확대될 것으로 전망됩니다.

이러한 확대의 주요 요인으로는 기존 의약품에 대한 소비자 불신 증가, 인도 및 유럽 일부 지역의 규제 통합 진행, 디지털 유통 모델 확산 등을 들 수 있습니다. 프랑스의 헬스케어 시스템에 대한 활발한 논의와 독일의 법정 의료보험 적용 범위 확대는 제도적 도입을 더욱 강화시키고 있습니다. 아시아태평양은 인도의 AYUSH(아유르베다, 유나니, 시다르타, 동종요법, 전통약초요법) 프레임워크와 중국의 대규모 중산층에 의한 자연요법 수요의 가속화로 인해 더욱 가파른 성장 곡선을 그리고 있습니다. 정제, 크림, 개인화된 디지털 치료 플랫폼의 병행 혁신은 제품의 접근성을 향상시키는 동시에 E-Commerce를 통해 소규모 기업이 약국 중개자 없이도 신규 구매자에게 다가갈 수 있도록 하고 있습니다. 성장 모멘텀은 식물 원료의 공급망 리스크와 FDA(미국 식품의약국)의 규제 강화로 인해 억제되고 있습니다.

헬스케어 소비자들은 부작용에 대한 인식이 높아지고 전인적 건강 솔루션에 대한 요구가 높아지면서 합성 의약품보다 자연요법적 접근법을 선호하는 경향이 강해지고 있습니다. 밀레니얼 세대와 Z세대가 지속가능한 식물 유래 솔루션을 건강 습관에 도입하면서 보완대체의학의 채택이 더욱 확대되고 있습니다. 소아과 및 만성질환 관리 분야에서는 안전성이 인정되어 장기 사용이 촉진되고 있으며, 특히 높은 재구매 패턴이 확인되고 있습니다. 소셜 미디어의 강력한 지지와 유명 인사들의 추천으로 동종요법 셀프 케어가 일반화되었고, 소매 체인은 저농도의 일반의약품을 주류 진통제 근처에 배치하여 인지도를 높이고 있습니다. 이러한 요인으로 인해 경기 순환이 헬스케어 관련 지출을 억제하는 경우에도 기준 수요는 유지되고 있습니다.

당뇨병, 심혈관질환, 스트레스 관련 질환 등 현대인의 생활습관 요인으로 인한 만성질환은 증상 관리뿐만 아니라 근본 원인을 해결하는 보완요법에 대한 지속적인 수요를 견인하고 있습니다. 무작위 대조 시험에서 동종요법이 인슐린 저항성 개선과 COVID-19 이후 피로감 완화에 효과가 있는 것으로 나타났으며, 여러 처방약을 복용하는 고령층에게 매력적인 결과입니다. 의료경제학적 검토에 따르면, 21건의 연구 중 14건의 연구에서 동종요법이 기존 치료와 동등하거나 그 이상의 효과를, 동등하거나 그 이하의 비용으로 달성한 것으로 확인되었습니다. 보험회사들이 비용 절감을 위해 노력하는 가운데, 이러한 발견은 파일럿 상환 프로그램 추진과 의사 추천을 촉진하는 촉매제 역할을 하고 있습니다.

미국 식품의약국(FDA)이 개정한 동종요법 제품 관련 지침은 '미승인 신약' 지정을 통해 시장 제약을 초래하고 있습니다. 이 규제 프레임워크를 통해 FDA는 필요에 따라 동종요법 의약품을 시장에서 퇴출시킬 수 있으며, 제품의 가용성과 시장 확대를 제한할 수 있습니다. 수입 경보와 리콜은 이미 내추럴오퍼머틱스와 같은 일부 제조업체들이 조업을 중단하는 등 규제 집행 조치가 시장에 미치는 즉각적인 영향을 보여주고 있습니다. 유럽 시장도 비슷한 압력에 직면해 있으며, 프랑스와 영국에서는 보완대체의학(CAM) 회의론자들이 동종요법의 공공 의료 시스템 통합에 반대하는 자금 삭감 움직임이 나타나고 있습니다. 특히 GMP 기준의 증명과 과학적 자료의 보관이 요구되는 중소기업의 경우, 컴플라이언스 비용이 상승하는 추세입니다. 갑작스러운 상환 제외 위험은 약국의 재고 수준에 대한 신중한 태도를 가져와 매장 내 노출 기회를 감소시키고 있습니다.

진통제 및 해열제는 2025년 기준 동종요법 제품 시장의 32.85%를 차지했으며, 이는 일상적인 통증과 발열에 대한 확고한 사용을 반영합니다. 한편, 호흡기 분야는 13.25%의 CAGR로 가장 높은 성장률을 보였는데, 이는 COVID-19 이후 폐 기능과 면역력 강화에 대한 소비자의 관심이 높아졌기 때문으로 분석됩니다. 단기간의 증상 완화와 눈에 보이는 효과는 사용자의 신뢰를 강화하고 입소문을 통한 추천을 가속화하고 있습니다. 당뇨병 관리, 심혈관 건강 등 신흥 분야에서의 적용은 대사성 질환 치료에서 동종요법의 역할을 입증하는 임상연구의 확대를 반영하고 있으며, 시장 확대를 위한 새로운 치료 카테고리를 개척할 것으로 기대됩니다.

신경학 분야에서는 지식경제 근로자 계층의 스트레스 관리 및 수면 지원 처방에 대한 수요 확대가 견인차 역할을 하고 있습니다. 피부과학 분야에서는 동종요법의 홀리스틱 브랜딩을 활용하여 습진 등 만성질환에 대응하고 있습니다. 이러한 질환의 경우 환자가 여러 가지 기존 치료법을 시도하는 경우가 많습니다. 소화기 분야는 장뇌 상호작용, 마이크로바이옴 조절 등 기능의학 클리닉의 관심 분야를 연구하는 가운데 꾸준한 성장세를 유지하고 있습니다. 이러한 다양한 적응증이 결합되어 동종요법 제품 시장은 단일 부문의 변동 위험을 완화하는 완충 역할을 하고 있습니다.

유럽은 수십 년간의 문화적 수용과 독일의 유리한 상환제도를 바탕으로 2025년 전 세계 매출의 31.80%를 차지했습니다. 신흥 지역에 비해 성장은 완만하지만, 제품 프리미엄은 높은 수준을 유지하며 수익률을 뒷받침하고 있습니다. 프랑스의 상환제도에 대한 논의는 투자자들의 심리에 영향을 미치지만, 일부 제품의 상장폐지는 수요를 소멸시키는 것이 아니라 환자들을 OTC(일반의약품)의 자가 구매로 유도할 것입니다. 영국의 브렉시트 이후 규제 측면의 독립성은 동종요법 정책의 다양화에 기회를 제공하지만, 의료기관내 과학적 회의론은 시장 확대에 대한 도전으로 작용하고 있습니다.

아시아태평양은 인도 아유르베다 병원의 의사 처방약 보급과 중국의 건강 지향적 중산층이 자연요법을 채택하면서 13.75%의 CAGR을 기록하는 등 물량 확대의 원동력으로 작용하고 있습니다. 일본과 호주는 고도의 규제 체계를 갖춘 선진 시장으로서 기회를 제공하고, 한국에서는 높아진 건강 의식이 천연물 제품 채택을 촉진하고 있습니다. WHO의 전통의학 전략은 지역 정부에 보완의학을 국가 보건정책에 통합할 것을 촉구하고 있으며, 이는 다양한 아시아태평양 경제권에서 시장 발전을 가속화할 수 있습니다.

북미에서는 규제적 역풍에도 불구하고 꾸준한 성장세를 보이고 있습니다. 캐나다의 자연건강 제품 프레임워크는 대부분의 치료법을 저위험으로 분류하여 승인을 신속히 처리하고 있으며, 미국 기업들은 FDA의 변화하는 태도에 대응하고 있습니다. 멕시코에서는 민간 클리닉이 빠르게 성장하고 있으며, 미국 플랫폼의 크로스보더 EC를 통해 멕시코 소비자들은 더 다양한 제품을 접할 수 있는 기회를 얻게 되었습니다. 중동, 아프리카, 남미는 헬스케어에 대한 인식이 높아지고 유통망이 확대되면서 성장 잠재력이 큰 신흥 시장입니다. 그러나 이들 지역은 경제 변동과 규제 불확실성 등의 문제에 직면해 있으며, 단기적으로 시장 발전에 영향을 미치고 있습니다.

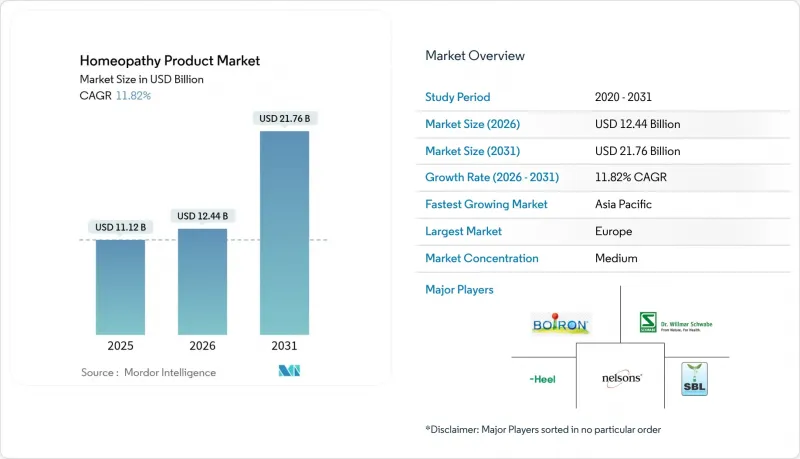

Homeopathy Product Market size in 2026 is estimated at USD 12.44 billion, growing from 2025 value of USD 11.12 billion with 2031 projections showing USD 21.76 billion, growing at 11.82% CAGR over 2026-2031.

Mounting consumer distrust of conventional pharmaceuticals, wider regulatory integration in India and parts of Europe, and the proliferation of digital distribution models are the chief forces behind this expansion. Robust public healthcare debates in France and statutory health-insurance coverage in Germany further strengthen institutional adoption. Asia-Pacific sits on a steeper growth curve as India's AYUSH framework and China's large middle-class accelerate demand for natural therapies. Parallel innovation in tablets, creams, and personalized digital remedy platforms enhances product accessibility, while e-commerce enables smaller firms to reach first-time buyers without pharmacy gatekeepers. Growth momentum is tempered by supply chain risks for botanical inputs and tightening FDA guidance.

Healthcare consumers increasingly prioritize natural therapeutic approaches over synthetic pharmaceuticals, driven by growing awareness of side effects and a desire for holistic wellness solutions. The uptake of complementary medicine has climbed further as millennials and Gen Z align their wellness routines with sustainable, plant-based solutions. Pediatric and chronic-care segments register particularly high repeat purchase patterns because perceived safety encourages long-term use. Strong social media advocacy and celebrity endorsements normalize homeopathic self-care, while retail chains position low-potency OTC remedies near mainstream analgesics, boosting visibility. These factors sustain baseline demand even when economic cycles dampen discretionary healthcare spending.

Chronic diseases linked to modern lifestyle factors, including diabetes, cardiovascular conditions, and stress-related disorders, drive sustained demand for complementary therapeutic approaches that address root causes rather than merely managing symptoms. Randomized trials indicate homeopathy can lower insulin resistance and relieve post-COVID-19 fatigue, outcomes that appeal to an aging population managing multiple prescriptions. Health-economic reviews show that 14 out of 21 studies found that homeopathic care produced similar or better results at an equal or lower cost than conventional treatment. As insurers seek cost control, such findings catalyze pilot reimbursement programs and foster physician referrals.

The U.S. Food and Drug Administration's revised guidance on homeopathic products creates market constraints through its "unapproved new drug" designation. This regulatory framework enables the FDA to remove homeopathic medicines from the market when necessary, limiting product availability and market expansion. Import alerts and recalls have already forced some manufacturers like Natural Ophthalmics to cease operations, demonstrating the immediate market impact of regulatory enforcement actions. European markets face similar pressures, with France and England experiencing defunding initiatives from Complementary and alternative medicine (CAM) skeptics who challenge homeopathy's integration into public health systems. Compliance costs rise, especially for small firms required to prove GMP standards and retain scientific dossiers. The threat of sudden delisting also makes pharmacies cautious about inventory levels, dampening shelf exposure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Analgesic & antipyretic solutions controlled 32.85% of the homeopathy products market size in 2025, reflecting entrenched use for everyday pain and fever. Respiratory applications, however, register the highest pace at a 13.25% CAGR as consumers prioritize lung health and immune resilience after COVID-19. Short relief cycles and observable symptom relief strengthen user confidence and accelerate word-of-mouth referrals. Emerging applications in areas like diabetes management and cardiovascular health reflect expanding clinical research that validates homeopathy's role in metabolic disorder treatment, potentially opening new therapeutic categories for market expansion.

Neurology categories benefit as stress-management and sleep-support formulas gain traction among knowledge-economy workers. Dermatology leverages homeopathy's holistic branding to address chronic conditions such as eczema, where sufferers often cycle through multiple conventional therapies. Gastroenterology keeps a steady growth trajectory as research explores gut-brain interaction and microbiome modulation, areas that resonate with functional-medicine clinics. Together, these diversified indications buffer the homeopathy products market against single-segment volatility.

The Homeopathy Product Market Report is Segmented by Product Type (Tinctures, Dilutions, Tablets, Ointments & Creams, Others), Application (Analgesic & Antipyretic, Respiratory, and More), Source (Plant-Based, Animal-Based, Mineral-Based), Distribution Channel (Retail Pharmacies & Drugstores, Homeopathic Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe commanded 31.80% of global revenues in 2025 on the back of decades-long cultural acceptance and favorable reimbursement in Germany. Growth here is slower than in emerging regions, yet product premiums remain high, preserving profit margins. France's reimbursement debate shapes investor sentiment; partial delisting would nudge patients toward OTC self-purchase rather than eliminate demand. The United Kingdom's post-Brexit regulatory independence creates opportunities for divergent homeopathy policies, though scientific skepticism within medical establishments continues challenging market expansion.

Asia-Pacific is the engine of volume expansion, moving at a 13.75% CAGR as India's AYUSH hospitals normalize doctor-prescribed remedies and China's wellness-focused middle class adopts natural therapies. Japan and Australia present developed market opportunities with sophisticated regulatory frameworks, while South Korea's growing wellness consciousness drives natural product adoption. The WHO's Traditional Medicine Strategy encourages regional governments to integrate complementary medicine into national health policies, potentially accelerating market development across diverse Asia-Pacific economies.

North America demonstrates steady growth despite regulatory headwinds. Canada's Natural Health Product framework classifies most remedies as low-risk, expediting approvals, while U.S. firms navigate the FDA's evolving stance. Mexico experiences a burgeoning private-clinic scene, and cross-border e-commerce from U.S. platforms exposes Mexican consumers to a wider assortment. The Middle East, Africa, and South America represent emerging markets with significant growth potential due to increasing healthcare awareness and expanding distribution networks. However, these regions face challenges such as economic volatility and regulatory uncertainty, which affect market development in the short term.