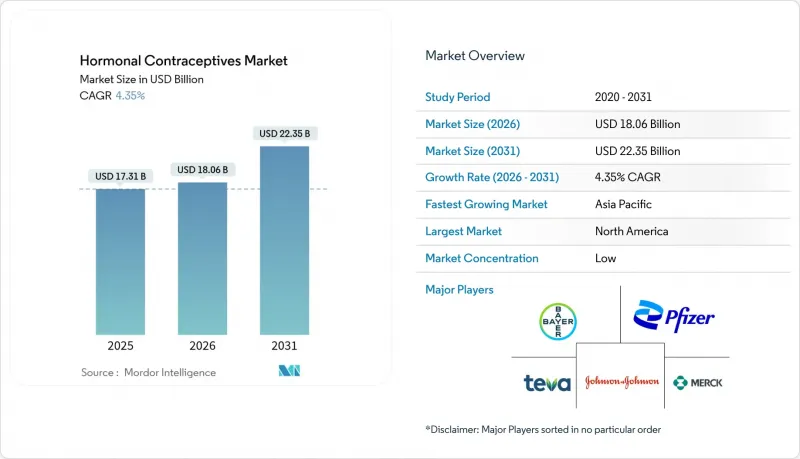

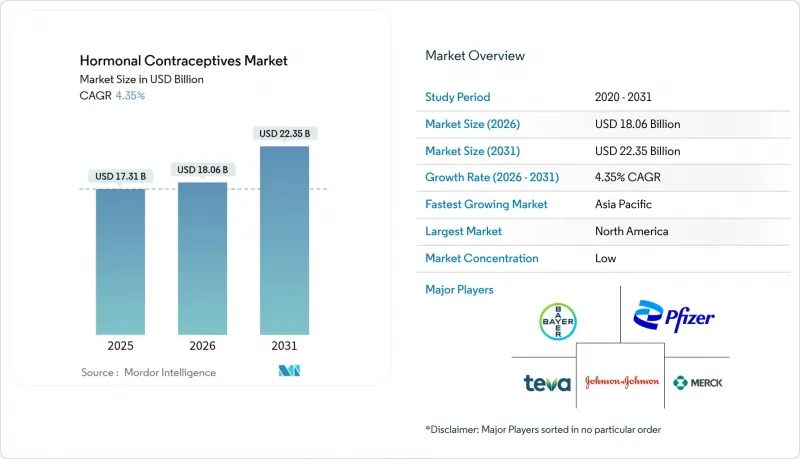

호르몬 피임약 시장은 2025년 173억 1,000만 달러에서 2026년에는 180억 6,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 4.35%를 기록하며 2031년까지 223억 5,000만 달러에 달할 것으로 예측됩니다.

이 확대는 원격의료를 활용한 처방 서비스, 미국 최초의 OTC(일반의약품)로 승인된 매일 복용하는 피임약, 그리고 지속성 피임법에 대한 수요 증가에 의해 촉진되고 있습니다. 온라인 약국은 이미 다른 모든 판매 채널을 능가하며 8.65%의 CAGR로 성장하고 있지만, 병원 약국은 여전히 40.1%로 가장 큰 매출 점유율을 차지하고 있습니다. 북미는 유리한 환급제도로 인해 전 세계 매출의 41.17%를 차지하고 있지만, 아시아 지역의 5.10%의 CAGR은 도시 소비자들이 장기 지속형 가역적 피임법(LARCs)으로 전환하면서 성장 여지가 크다는 것을 보여줍니다. 경쟁의 강도는 여전히 중간 정도입니다. 바이엘 AG 등 기존 기업은 수명주기 연장을 통해 점유율을 지키고, 신규 진입 기업은 친환경 기술로 차별화를 꾀하고 있습니다. 2025년까지 지속가능성, 디지털 접근성, 안전성에 중점을 둔 재처방은 호르몬 피임약 시장에서 가장 뚜렷한 성장 기회가 될 것입니다.

부작용을 최소화하기 위한 저용량 제제가 제품에 대한 기대치를 재정의하고 있습니다. 드로스피레논 3mg/에스트라디올 14.2mg 복합제(60년 만에 처음으로 새로운 에스트로겐을 도입한 복합제)는 생리주기 조절은 유지하면서 응고 작용에 미치는 영향은 거의 없는 것으로 나타났습니다. 각 브랜드가 유효성분 프로파일에 집중하는 가운데, 위험회피 성향의 사용자들에게 매력적인 차별화된 안전성 스토리를 제공하고 있습니다.

전 세계 임신의 약 40%는 의도하지 않은 임신이며, 이는 가족계획 프로그램에 대한 공적 자금 투입을 촉진하고 있습니다. 미국에서는 2025년 2,100만 명의 여성이 공공 지원 피임 서비스를 받게 될 것이며, 그 비용은 21억 달러에 달할 것으로 예상됩니다. 1달러를 지출하면 4.26달러의 의료비 절감 효과가 있습니다. FDA 승인 방법의 무상 제공을 의무화하는 연방 규정이 기초적인 수요를 강화하고 있습니다.

피임 관련 소셜 게시물의 약 5분의 1이 부작용에 대해 언급하고 있어 사용 중단의 위험을 증폭시키고 있습니다. 수많은 팔로워를 보유한 인플루언서들은 고립된 사례를 몇 시간 만에 전 세계 이슈로 발전시킬 수 있고, 규제 당국은 예정보다 일찍 안전에 대한 표현을 재검토해야 하며, 브랜드는 실시간 평판 모니터링에 대한 투자를 확대할 수밖에 없습니다.

경구용 피임약은 수십 년간의 임상적 성과로 인해 2025년에도 42.82%의 점유율을 유지했습니다. 오필의 일반의약품화로 소비자층이 확대되어 2025년 경구피임약 시장 점유율 상승에 기여할 수 있을 것으로 보입니다. 임플란트는 수익 기반은 작지만 우수한 컴플라이언스로 인해 7.57%의 CAGR로 가장 빠르게 성장하고 있습니다. BMI 30kg/m2 미만 사용자를 위한 저용량 에스트로겐 패치 '투왈라'가 경피 투여에 대한 관심을 다시 불러일으키고 있습니다. 미레나 등 호르몬 IUD는 FDA 승인으로 최대 8년간 착용이 가능해져 가치 제안이 심화되고 있습니다.

2세대 질 내 링, 저용량 주사제, 응급 피임약은 다양한 사용자 니즈에 대응하며 틈새시장에서의 존재감을 유지하고 있습니다. 이러한 투여 형태가 결합되어 호르몬 피임약 시장을 뒷받침하는 방법의 다양성을 강화하고 있습니다.

2025년 매출에서 에스트로겐-프로게스틴 복합제제는 60.58%를 차지했습니다. 그러나 심혈관 위험에 대한 논의가 프로게스틴 단독 제제로의 전환을 촉진하고 있으며, 이 분야는 6.44%의 CAGR로 성장할 것으로 예상됩니다. 드로스피레논/에스테트롤 복합 정제는 응고 작용을 최소화하면서 복합 제제가 진화할 수 있다는 것을 보여줍니다. 한편, 프로게스틴 단독 피임약의 OTC 승인으로 이 하위 부문은 보다 안전한 일상적 선택으로 재편되어 호르몬 피임약 시장 규모의 점진적인 증가를 뒷받침하고 있습니다.

북미는 2025년 매출의 35.98%를 차지했습니다. FDA의 OTC 알약 승인 결정과 보험 적용 의무화로 인해 사용이 증가하고 있습니다. 타이틀 X 자금에 대한 정치적 불안정성이 진료소 보급을 억제할 수 있지만, 디지털 대응이 잠재적 후퇴를 상쇄할 수 있습니다.

아시아태평양은 6.04%의 CAGR을 보이며 인도, 인도네시아, 중국 도시 지역의 잠재적 수요를 흡수하고 있습니다. 대도시와 지방의 피임 격차는 인프라 구축의 필요성을 강조하고 있으며, 대상별 공공 프로그램이 격차 해소를 목표로 지역 전체 호르몬 피임약 시장 규모를 확대하고 있습니다.

유럽은 보편적 의료보험제도 하에서 안정적인 보급을 유지하고 있지만, 보다 엄격한 반독점법 감시로 인해 가격 설정의 유연성이 떨어지고 있습니다. 라틴아메리카는 공공 정책의 혜택을 받고 있지만, 경제성 문제와 문화적 규범이 급속한 확장을 억제하고 있습니다. 중동 및 아프리카에서는 보급률이 고르지 않은 가운데, 남아프리카공화국과 나이지리아가 지원 단체의 공급망 지원을 받아 중점 시장으로 부상하고 있습니다. 오세아니아는 안정적인 물량 기여를 하고 있지만, 인구 규모에 비해 절대적인 가치는 작습니다.

The hormonal contraceptive market is expected to grow from USD 17.31 billion in 2025 to USD 18.06 billion in 2026 and is forecast to reach USD 22.35 billion by 2031 at 4.35% CAGR over 2026-2031.

Expansion is propelled by telehealth-enabled prescription services, the first U.S. OTC daily pill approval, and rising demand for long-acting methods. Online pharmacies already outpace every other channel, expanding at an 8.65% CAGR, while hospital pharmacies still hold the largest 40.1% revenue share. North America commands 41.17% of global revenue thanks to favorable reimbursement frameworks, whereas Asia's 5.10% CAGR underscores significant headroom as urban consumers pivot to long-acting reversible contraceptives (LARCs). Competitive intensity remains moderate; incumbents such as Bayer AG defend share through lifecycle extensions, while newer entrants differentiate on eco-friendly technologies. Throughout 2025, sustainability, digital accessibility, and safety-driven reformulations remain the clearest opportunity lanes for the hormonal contraceptive market.

Lower-dose formulations aimed at minimizing side effects are redefining product expectations. The drospirenone 3 mg/estetrol 14.2 mg pill-the first combination to feature a novel estrogen in six decades-shows negligible impact on coagulation while preserving cycle control. As brands refocus on active-ingredient profiles, they deliver a differentiated safety narrative attractive to risk-averse users.

Roughly 40% of global pregnancies are unintended, driving public funding for family-planning programs. In the United States, 21 million women received publicly supported contraceptive services in 2025 at a cost of USD 2.1 billion; every dollar spent saves USD 4.26 in healthcare outlays. Federal rules mandating no-cost coverage of FDA-approved methods strengthen baseline demand.

Nearly 1 in 5 contraceptive-related social posts discuss adverse events, amplifying discontinuation risk. Influencers with large followings can turn isolated incidents into global talking points within hours, prompting regulators to revisit safety language sooner than planned and compelling brands to invest more in real-time reputation monitoring.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Oral pills retained a 42.82% share in 2025, powered by decades of clinical familiarity. OTC status for Opill widens consumer reach and could lift the hormonal contraceptive market share for pills in 2025. Implants, though accounting for a smaller revenue base, grow quickest at 7.57% CAGR on superior compliance. Twirla, a low-dose estrogen patch for users with BMI < 30 kg/m2, revitalizes interest in transdermal delivery.Hormonal IUDs such as Mirena now benefit from FDA-approved use up to eight years, deepening value propositions.

Second-generation vaginal rings, lower-dose injectables, and emergency pills maintain niche relevance by addressing diverse user needs. Collectively, these modalities reinforce method mix depth that sustains the hormonal contraceptive market.

Combined estrogen-progestin products represented 60.58% of 2025 revenue. However, cardiovascular risk dialogues encourage pivot toward progestin-only choices, expected to outpace at 6.44% CAGR. The drospirenone/estetrol pill shows the combined category can still evolve with minimal coagulation effect. Meanwhile, the OTC approval of a progestin-only pill repositions that sub-segment as the safer everyday option, underpinning incremental hormonal contraceptive market size gains.

Hormonal Contraceptives Market Report is Segmented by Product (Hormonal Implants, Vaginal Rings and More), Hormone (Combined and Progestin Only), Usage Duration (SARCs and LARCs), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and More), End-User (Home Use, Community Health Centers and More), Age Group (15 - 24 Years, 25 - 34 Years and More) and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

North America held 35.98% of 2025 revenue. The FDA's OTC pill decision and insurance mandates bolster usage. Political uncertainty around Title X funding could temper clinic reach, yet digital fulfillment offsets potential setbacks.

Asia-Pacific, posting a 6.04% CAGR, captures latent demand in urban India, Indonesia, and China. Contraceptive disparities between metropolitan and rural counties highlight infrastructure needs; targeted public programs aim to close gaps, enlarging the hormonal contraceptive market size across the region.

Europe maintains stable uptake under universal coverage, yet stricter antitrust scrutiny challenges pricing flexibility. Latin America benefits from public initiatives, but affordability issues and cultural norms restrain rapid acceleration. The Middle East and Africa display uneven penetration; South Africa and Nigeria emerge as focus markets, aided by donor-supported supply chains. Oceania contributes steady volumes but small absolute value due to the population scale.