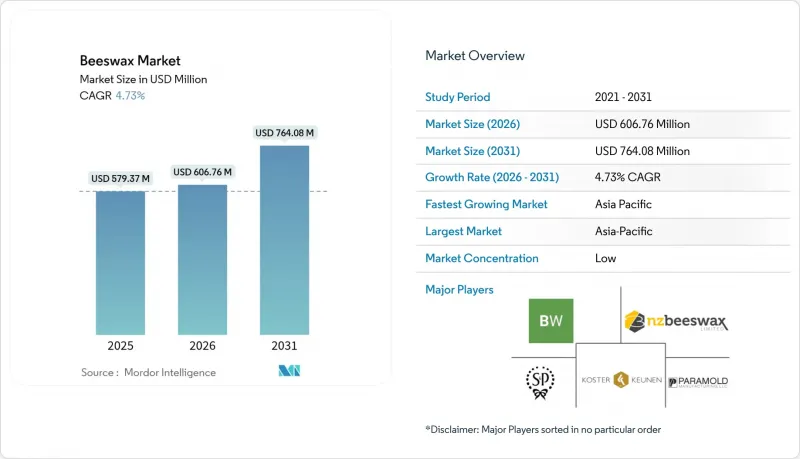

세계의 밀랍 시장은 2025년에 5억 7,937만 달러로 평가되었으며, 2026년 6억 676만 달러에서 2031년까지 7억 6,408만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.73%로 예상됩니다.

시장 확대의 주요 요인은 화장품 배합, 의약품, 천연 식품 코팅에서 밀랍의 채택이 증가했기 때문입니다. 이는 원료의 투명성에 대한 규제 요건의 변화에 대응하기 위한 제조업체의 움직임에 따른 것입니다. 아시아태평양은 생산과 소비 양면에서 선도적인 위치를 유지하고 있으며, 인도가 연간 100만 킬로그램의 큰 기여를 하고 있습니다. 한편, 기존 시장에서는 잔류물 제한 및 제품 진위성에 대한 엄격한 품질 기준을 충족하는 인증된 밀랍 등급을 통해 더 높은 수익을 창출하고 있습니다. 합성 왁스를 대체할 수 있는 합성 왁스 대체품이 등장하고 있지만, 특히 고부가가치 제품 응용 분야에서 천연 밀랍은 규제상의 우위와 광범위한 소비자 수용성으로 인해 여전히 강력한 시장 지위를 유지하고 있습니다.

화장품 업계에서 천연 원료로의 근본적인 전환으로 인해 밀랍은 유화제 및 텍스처 개선제, 특히 립 케어 제품 및 보호 장벽 제형에서 프리미엄급으로 자리매김하고 있습니다. 시장의 요구에 부응하여 주요 화학업체들은 천연 원료 포트폴리오를 강화하고 있으며, 루브 리졸의 카보폴 바이오센스(Carbopol Biosense)와 BASF의 옥수수 유래 필름 형성제인 베르데센스 메이즈(Verdesense Mays)의 도입이 그 증거입니다. 밀랍은 유화 능력, 피막 형성 특성, 그리고 황색포도상구균과 칸디다 알비칸스균에 대한 입증된 항균 효과 등 종합적인 기능성을 겸비한 종합적인 기능성으로 큰 가치를 제공합니다. 이러한 특성은 원료 통합에 대한 배합사의 요구사항에 직접적으로 대응하고, 클린 라벨링에 대한 노력을 지원합니다. 규제 측면에서도 FDA의 GRAS 인증(21 CFR 184.1973)과 EU 식품 첨가물 승인(E-901)을 획득한 밀랍은 화장품과 식품 접촉 용도 모두에 원활하게 통합될 수 있어 시장에서의 입지를 더욱 강화하고 있습니다.

퍼스널케어 제품의 성분 투명성에 대한 소비자의 인식과 수요가 증가함에 따라 밀랍의 시장 지위가 크게 향상되었습니다. 수세기 동안 전통적으로 사용되어 온 천연 성분인 밀랍은 안전성이 입증된 천연 성분으로 현재 소비자의 기호에 완벽하게 부합합니다. 생분해성, 무독성 포뮬러를 중시하는 클린 뷰티 운동의 확산으로 석유 유래 대체품에서 벗어나 밀랍으로 전환하는 제조업체가 증가하고 있습니다. 특히 미세플라스틱 문제로 인한 환경 문제가 대두되면서 규제 당국이 합성 폴리머에 대한 엄격한 관리를 시행함에 따라 이러한 전환은 더욱 가속화되고 있습니다. 시장에서는 화장품용 밀랍(1온스당 2달러)과 양초용 밀랍(1온스당 1.25달러) 사이에 뚜렷한 가격 차이가 존재하며, 이는 화장품 용도의 엄격한 품질 기준과 순도 요구 사항을 반영합니다. 현대의 규제 프레임워크는 종합적인 성분 공개와 지속가능성에 대한 문서화를 의무화하는 방향으로 진화하고 있으며, 밀랍과 같은 기존 천연 원료에 유리한 환경을 조성하고 있습니다. 반면, 새로운 합성 대체품은 오랜 기간과 고비용이 소요되는 안전성 검증 과정에 직면해 있습니다.

기후변화로 인한 식민지 손실은 전 세계 밀랍 공급망에 심각한 영향을 미치고 있습니다. 라틴아메리카의 종합적인 연구 결과에 따르면, 멕시코의 경우 16.2%, 콜롬비아의 경우 47.7%의 우려할 만한 연간 식민지 사망률을 보이고 있습니다. 자연 서식지의 지속적인 손실, 계절적 개화 패턴의 교란, 잦은 기상 이변 등 여러 가지 환경적 문제로 인해 군락의 생산성과 왁스 생산능력이 크게 저하되고 있습니다. 밀랍 생산 공정은 특히 민감하며, 일벌은 12-18일간의 중요한 밀랍 분비 기간에 정밀한 환경 조건을 필요로 합니다. 전 세계 꿀벌 군집의 가장 심각한 생물학적 위협은 여전히 꿀벌 벼룩(Varroa destructor)의 기생이며, 심각한 기생은 군집의 생존율과 왁스 축적량을 극적으로 감소시킵니다. 이러한 공급 측면의 불확실성으로 인해 안정적인 고품질 밀랍은 프리미엄 가격이 요구되는 시장 환경이 조성되고, 가격에 민감한 업계 제조업체들은 합성 대체품으로 전환하는 경향이 있습니다. 규제 당국이 공급망의 투명성과 탄력성에 대한 관심을 높이고 있지만, 꿀 시장에서 확립된 표준과 비교할 때 업계에는 여전히 종합적인 품질 표준이 부족합니다.

천연 밀랍은 천연 유래 및 생분해성 성분에 대한 소비자의 요구가 증가함에 따라 2025년에도 84.65%의 점유율을 차지할 것으로 예상됩니다. 이 시장에서의 선도적 지위는 제품 안전과 천연 유래가 가장 중요한 이슈인 식품, 화장품, 의약품 등 여러 산업 분야에서 이미 확립된 규제 승인을 통해 더욱 강화되고 있습니다.

합성 왁스 부문은 안정적인 공급과 고감도 애플리케이션을 위한 무공해 특성으로 인해 5.70%의 CAGR로 견조한 성장세를 보이고 있습니다. 특히 사솔의 제품 포트폴리오에서 눈에 띄는 피셔 트로프쉬 합성 왁스는 파라핀, 미결정, 합성 경질 왁스의 각 종류에서 강화된 열 안정성과 조절 가능한 융점을 특징으로 합니다. 이 제품들은 화장품부터 산업용 코팅에 이르기까지 다양한 산업에 활용되고 있습니다. 합성 부문은 농업과 기후변화의 영향을 받지 않기 때문에 천연 밀랍 시장에 영향을 미치는 공급망의 불확실성을 제거합니다. 합성 왁스 제조업체는 성분을 정밀하게 관리하고 농약 잔류물이 없는 제품을 보장할 수 있기 때문에 엄격한 순도 기준이 요구되는 의약품 및 식품 접촉 응용 분야에서 특히 가치가 높습니다.

아시아태평양은 현재 세계 밀랍 시장에서 가장 큰 점유율을 차지하고 있으며, 2025년에는 37.84%를 차지했습니다. 이 우위는 주로 세계 최대 생산국인 인도가 연간 2,460만kg의 세계 공급량을 차지하고 있는 데서 기인합니다. 중국은 주요 소비시장으로 부상하고 있지만, 정확한 생산 수치는 여전히 얻기 어렵습니다. 일본의 꿀 생산 자급률이 6%에 불과한 것에서 알 수 있듯이, 일본은 수입에 크게 의존하고 있으며, 다양한 산업 용도를 위해 많은 양의 밀랍을 수입해야 합니다.

이 지역의 성장률은 5.24%의 CAGR로 다른 모든 지역 부문을 능가하는 놀라운 성장률을 보였습니다. 이러한 가속화된 성장은 380만 킬로그램에 달하는 한국의 대규모 생산능력에 힘입어 세계 5위의 생산국으로 자리매김하고 있습니다. 그러나 최근 한국 화장품의 미국 시장 수출에 대한 관세 압력으로 인해 밀랍을 포함한 화장품 포뮬러의 수요 패턴에 새로운 움직임이 생겨 향후 성장률에 영향을 미칠 수 있습니다.

다른 지역에서는 북미와 유럽이 성숙한 시장으로 자리매김하고 있으며, 규제 프레임워크가 확립되어 있고 천연 성분에 대해 프리미엄 가격을 지불하려는 소비자의 의지가 특징입니다. 미국 시장은 벌집 수입 및 가축 사료용으로 제한되어 있으며, APHIS 승인을 받은 정제 밀랍 수출 경로를 통해 EU로의 수출이 가능합니다. 유럽 시장에서는 지속가능성과 오염 감시가 중요시되며, 영국의 카테고리 3 물질 기준과 같은 특정 수입 프로토콜이 존재합니다. 남미에서는 아르헨티나(500만kg)와 브라질(180만kg)이 주요 생산국이지만, 16.2%에서 47.7%에 이르는 높은 식민지 손실률이라는 도전에 직면해 있습니다. 아프리카는 풍부한 양봉 전통을 가지고 있지만, 기술 및 시장 접근성의 제약으로 인해 생산량이 잠재력을 밑돌고 있으며, 전 세계 밀랍 생산량의 25% 미만을 차지하고 있습니다.

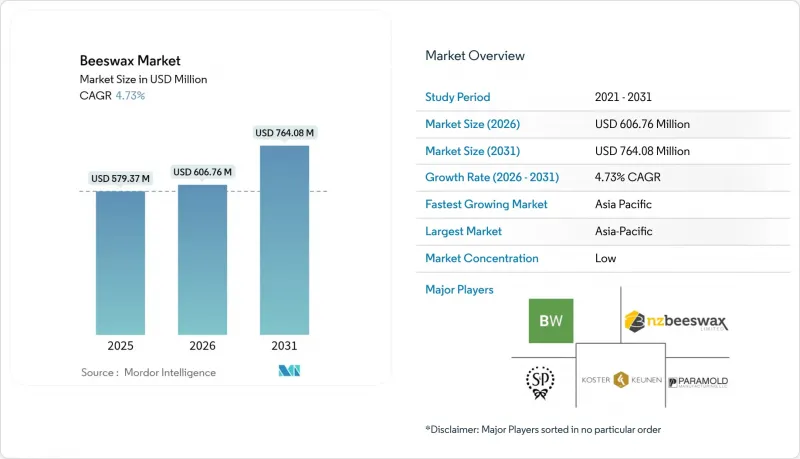

The global beeswax market was valued at USD 579.37 million in 2025 and estimated to grow from USD 606.76 million in 2026 to reach USD 764.08 million by 2031, at a CAGR of 4.73% during the forecast period (2026-2031).

The market expansion is primarily driven by the increased adoption of beeswax in cosmetics formulations, pharmaceutical products, and natural food coatings, as manufacturers respond to evolving regulatory requirements for ingredient transparency. The Asia-Pacific region maintains its position as the dominant force in both production and consumption, with India's substantial contribution of one million kilograms per year. Meanwhile, established markets generate higher revenues through certified beeswax grades that satisfy stringent quality standards for residue limits and product authenticity. Although synthetic wax alternatives are emerging with benefits such as quality consistency and reduced contamination risks, natural beeswax continues to hold a strong market position due to its favorable regulatory status and widespread consumer acceptance, particularly in high-value product applications.

The cosmetics industry's fundamental transformation toward natural ingredients has elevated beeswax to a premium status as an emulsifier and texture enhancer, particularly benefiting lip care and protective barrier formulations. In response to market demands, major chemical suppliers have strengthened their natural ingredient portfolios, evidenced by Lubrizol's introduction of Carbopol BioSense and BASF's launch of Verdessense Maize as corn-derived film-formers. Beeswax brings significant value through its comprehensive functional properties, combining emulsification capabilities, film formation characteristics, and proven antimicrobial effectiveness against Staphylococcus aureus and Candida albicans. These attributes directly address formulators' growing requirements for ingredient consolidation while supporting clean-label initiatives. The regulatory framework further reinforces beeswax's market position, with FDA GRAS status (21 CFR 184.1973) and EU food additive approval (E-901) enabling manufacturers to incorporate it seamlessly across both cosmetics and food-contact applications.

The increasing consumer awareness and demand for ingredient transparency in personal care products has significantly enhanced beeswax's position in the market. As a natural component with well-documented safety records and centuries of traditional use, beeswax aligns perfectly with current consumer preferences. The clean beauty movement, which prioritizes biodegradable and non-toxic formulations, has created a substantial shift toward beeswax as manufacturers move away from petroleum-based alternatives. This transition has gained momentum as regulatory bodies implement stricter controls on synthetic polymers, particularly due to growing environmental concerns about microplastics. The market demonstrates clear price differentiation between cosmetic-grade beeswax, which commands USD 2.00 per ounce, and candle-grade beeswax at USD 1.25 per ounce, reflecting the stringent quality standards and purity requirements for cosmetic applications. Modern regulatory frameworks have evolved to mandate comprehensive ingredient disclosure and sustainability documentation, creating a favorable environment for established natural ingredients like beeswax, while new synthetic alternatives face lengthy and costly safety validation processes.

Climate-driven colony losses significantly impact the global beeswax supply chain, as evidenced by comprehensive studies from Latin America that reveal concerning annual colony mortality rates ranging from 16.2% in Mexico to 47.7% in Colombia. Multiple environmental challenges, including the ongoing loss of natural habitats, disruptions in seasonal flowering patterns, and the increasing frequency of extreme weather events, have substantially reduced both colony productivity and wax production capabilities. The process of wax production is particularly sensitive, as worker bees require precise environmental conditions during their critical 12-18 day wax-secretion phase. The Varroa destructor mite infestation continues to pose the most significant biological threat to colonies worldwide, with severe infestations dramatically decreasing both colony survival rates and wax accumulation. These supply uncertainties have created a market environment where premium prices are commanded for consistent, high-quality beeswax, consequently pushing manufacturers in price-sensitive industries toward synthetic alternatives. While regulatory bodies have increased their focus on supply chain transparency and resilience, the industry still lacks comprehensive quality standards compared to the well-established specifications in the honey market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Natural beeswax continues to dominate the market with an 84.65% share in 2025, as consumers increasingly gravitate toward natural and biodegradable ingredients. This market leadership is further reinforced by well-established regulatory approvals across multiple industries, including food, cosmetic, and pharmaceutical applications, where product safety and natural origin remain paramount considerations.

The synthetic wax segment demonstrates robust growth with a CAGR of 5.70%, primarily due to its ability to deliver consistent supply and contamination-free properties for sensitive applications. Fischer-Tropsch synthetic waxes, particularly notable in Sasol's product portfolio, offer enhanced thermal stability and adjustable melting points across paraffin, microcrystalline, and synthetic hard wax varieties. These products serve diverse industries from cosmetics to industrial coatings. The synthetic segment's independence from agricultural and climatic variables addresses the supply chain uncertainties that affect natural beeswax markets. Manufacturers of synthetic waxes can maintain precise composition control and ensure products free from pesticide residues, making them particularly valuable for pharmaceutical and food-contact applications where stringent purity standards must be met.

The Beewax Market Report is Segmented by Product Type (Natural, and Synthetic), Form (Blocks, Pellets / Pastilles, and Sheets / Beads), Application (Cosmetics, Pharmaceuticals, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region currently commands the largest share of the global beeswax market, accounting for 37.84% in 2025. This dominance is primarily attributed to India's position as the world's largest producer, contributing 24.6 million kg annually to the global supply. China has emerged as a significant consumption market, although precise production figures remain unavailable. Japan's heavy reliance on imports, reflected in its mere 6% self-sufficiency in honey production, indicates substantial beeswax import requirements for various industrial applications.

The region's growth trajectory stands at an impressive 5.24% CAGR, outpacing all other geographical segments. This accelerated growth is supported by South Korea's substantial production capacity of 3.8 million kg, positioning it as the fifth-largest global producer. However, recent tariff pressures on Korean beauty exports to the US market have introduced new dynamics in the demand patterns for beeswax-containing cosmetic formulations, potentially influencing future growth rates.

In other regions, North America and Europe maintain their positions as mature markets, characterized by well-established regulatory frameworks and consumer willingness to pay premium prices for natural ingredients. The US market benefits from APHIS-approved refined beeswax export pathways to the EU, despite facing limitations on honeycomb imports and livestock feeding applications. European markets emphasize sustainability and contamination monitoring, with specific import protocols such as the UK's Category 3 material standards. South America contributes significantly through Argentina (5.0 million kg) and Brazil (1.8 million kg), though facing challenges from high colony loss rates ranging from 16.2% to 47.7%. Africa's production remains below its potential, contributing less than 25% of global beeswax output despite its rich beekeeping heritage, primarily due to technological and market access limitations.