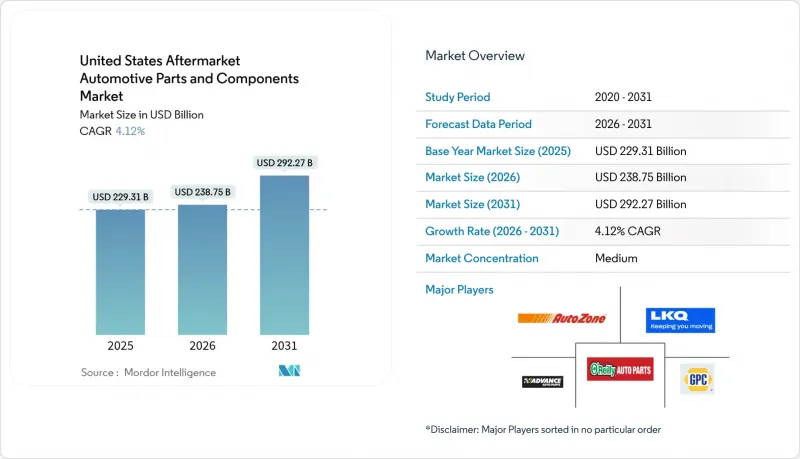

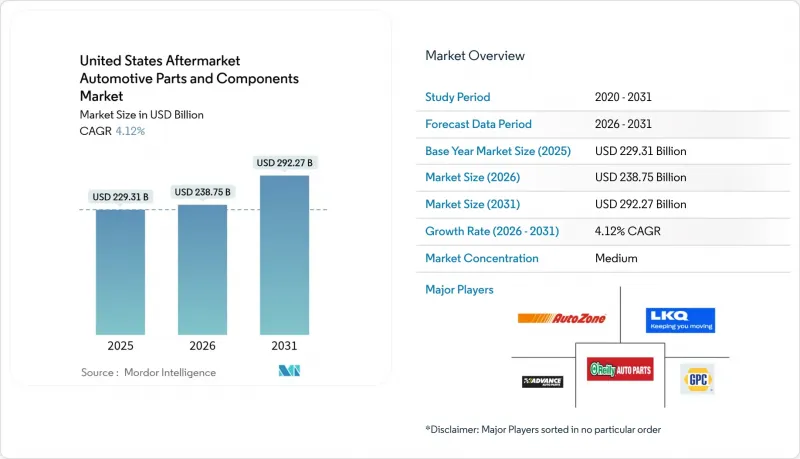

미국의 애프터마켓 자동차 부품 및 컴포넌트 시장은 2025년 2,293억 1,000만 달러에서 2026년에는 2,387억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 4.12%로 추이하며, 2031년에는 2,922억 7,000만 달러에 달할 것으로 예측됩니다.

이러한 확대를 지원하는 요인으로는 평균 차량 사용 연한의 장기화, 경트럭 판매 호조, E-Commerce의 급속한 보급을 들 수 있습니다. 신차 가격 상승, 수리권법 확대, 팬데믹 이후 운전 수요 회복이 교체 수요를 자극하는 한편, 신흥 전동화 개조 키트가 프리미엄 특화 분야를 개발하고 있습니다. 부품 카테고리에 따라 경쟁의 강도는 다르지만, 옴니채널 유통과 전자기기 전문성을 결합한 공급업체는 지속가능한 성장을 위한 토대를 마련하고 있습니다. EPA 배출가스 규제에서 주정부의 EV 의무화까지 규제 구상은 역풍과 순풍의 역할을 모두 수행하며, 규정 준수 요구 사항의 변화를 통해 자동차 애프터마켓 부품 시장을 재구성하고 있습니다.

소형 트럭은 자동차 시장을 휩쓸고 있으며, 2027년까지 신차 판매의 상당 부분을 차지할 것으로 예측됩니다. 이러한 견고한 차량은 기존 승용차에 비해 애프터마켓 지출이 높으며, 이는 고유한 요구사항과 성능을 반영합니다. 이러한 트럭을 구성하는 부품, 즉 서스펜션, 브레이크, 구동계 부품은 견인 및 적재하는 중량물에 따라 훨씬 더 큰 하중을 견뎌내야 합니다.

오버랜딩, 트레일러 견인, 아웃도어 어드벤처 등 라이프스타일 동향이 확산되면서 성능 향상을 위한 업그레이드에 대한 수요가 증가하고 있습니다. 애호가들은 운전 경험을 향상시키고 험한 지형에 대응하기 위해 리프트 키트, 헤비 듀티 쇼크, 대형 타이어를 요구하고 있습니다. 픽업트럭에 특화된 장비 시장 규모는 이미 연간 160억 달러에 달하며, 각 제조업체들은 이러한 다목적 차량을 위한 전용 제품 라인을 개발하고 있습니다.

경트럭 소유주들은 종종 커스터마이징에 대한 열정을 가지고 있으며, 업그레이드의 평균 거래 금액은 종종 표준 부품 교체보다 높습니다. 이러한 추세는 트럭의 미적 감각과 기능성을 향상시킬 뿐만 아니라 자동차 애프터마켓 부품 부문 전체의 이익률도 향상시켜 무한한 잠재력을 지닌 호황 시장을 상징합니다.

현재 애프터마켓 거래의 대부분은 디지털 채널의 역동적인 환경에서 이루어지고 있으며, 미국 전체 소매 E-Commerce 보급률을 크게 상회하고 있습니다. 이러한 현저한 변화로 인해 온라인 스토어는 기존 오프라인 도매업체가 직면한 재고 비용 부담 없이 전문적인 SKU를 전시할 수 있게 되었습니다. 그 결과, 구하기 어려운 빈티지 모델의 부품을 전국적으로 쉽게 공급할 수 있으며, 애호가와 수집가 모두의 니즈에 부응하고 있습니다. 직배송 물류와 실시간 재고 데이터는 DIY 애호가 및 소규모 차고의 리드 타임을 단축하고 디지털에 정통한 공급업체에 시장력을 재분배하고 있습니다. 그러나 위조품의 유입은 여전히 심각한 위험이며, 연방 정부의 단속 조치는 브랜드 보호 프로그램의 중요성을 강조하고 있습니다. 강력한 인증 기술과 사용자 친화적인 인터페이스를 결합한 기업이 확대되는 디지털 애프터마켓에서 압도적인 점유율을 차지하고 있습니다.

자동 비상 브레이크와 차선 유지 시스템은 충돌률을 낮추고, 범퍼, 펜더, 램프에 대한 수요를 감소시키고 있습니다. 충돌 빈도의 감소는 ADAS의 보급률이 가장 높은 신형 고급차에서 두드러지게 나타나 외장 부품 수요를 압축하고 있습니다. 이러한 감소를 상쇄하기 위해 ADAS 장착 차량의 수리는 필수적인 센서 교정과 긴 작업 시간으로 인해 수리 비용이 더 많이 청구됩니다. 손상된 카메라 및 레이더 모듈의 교체는 전문 전자 부품 하위 부문의 성장을 가속합니다. 충돌 수리 센터는 첨단 스캐닝 툴에 대한 기술 향상과 투자를 통해 OE급 센서 및 교정 지그를 제공하는 부품 공급업체에 이익을 가져다주고 있습니다.

2025년 기준, 승용차는 미국 애프터마켓 자동차 부품 및 부품 시장 전체 매출의 52.74%를 차지할 것으로 예상되며, 그 기반은 방대한 설치 대수를 바탕으로 하고 있습니다. 그러나 상업용 경트럭은 7.05%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 택배 및 서비스 차량의 주행거리 증가에 따라 애프터마켓 자동차 부품 및 부품 시장 규모에 대한 기여도가 높아질 것으로 예측됩니다. 가혹한 사용 주기와 엄격한 가동률 요구 사항이 결합되어 브레이크 어셈블리, 드라이브 트레인 조인트 및 냉각 부품의 교체 빈도가 증가하고 있습니다. 차량 운영자들은 신속한 공급과 효율적인 보증 프로세스를 보장하는 공급업체를 우선순위로 삼기 때문에 부품 제조업체는 창고 수준의 재고와 예측 공급 시스템으로 전환해야 합니다.

중대형 트럭은 수량이 적고, 개별 부품 단가가 높으며, 가동 중단시 손실도 크기 때문에 상대적으로 큰 경제적 가치를 창출합니다. EPA 2027 배출가스 규제는 선택적촉매환원장치(SCR)와 미립자포집필터(DPF)의 사전 구매 활동과 애프터마켓 개조를 촉진하여 일시적으로 대형차 수요를 증가시키고 있습니다. 예측에서 새롭게 분류된 버스-코치 분야는 대용량 열 관리 제품 및 서스펜션 제품 전문 공급업체에게 부수적인 가능성을 열어줍니다. 승용차 부문은 여전히 중요하지만, 하이브리드 시대에 가구가 여러 대의 차량을 소유할 필요성에 의문을 제기하는 가운데, 판매량 기준은 감소하는 추세입니다. 반면, 화물차는 물류 확대와 연동된 성장 궤도에 고정되어 있는 것으로 보입니다.

엔진 부품은 2025년 기준 미국 애프터마켓 자동차 부품 및 부품 분야의 31.45%를 차지할 것으로 예상되며, 이는 여전히 내연기관(ICE)이 주류임을 반영합니다. 반면, ADAS 센서는 CAGR 7.52%로 예측되며, 기계적 가치에서 전자적 가치로의 전환을 시사하고 있습니다. 카메라 모듈, 레이더 유닛, 제어용 ECU는 경미한 충돌로 고장나거나 환경오염물질의 영향을 받는 경우가 많아 고매출을 창출하는 교체 주기가 길어지고 있습니다. 콘티넨탈이 2024년에 700개의 새로운 엔진 관리 SKU를 도입한 것은 공급업체가 기계 분야의 기반을 지키면서 전자기기 포트폴리오를 확장하는 양면 전략을 보여주고 있습니다.

서스펜션, 브레이크, 타이어 분야에서는 대형 SUV와 픽업트럭의 성장세가 지속적인 수요 증가를 가져오고 있습니다. 전기 시스템 및 인포테인먼트 하위 부문은 드라이버의 연결성 향상과 무선 업데이트 기능에 대한 수요 증가에 따라 확대되고 있으며, 애프터마켓에서 하드웨어와 소프트웨어 서비스의 경계가 모호해지고 있습니다. 차체 및 외장 부품은 상대적으로 복잡한 상황에 처해 있습니다. ADAS로 인한 충돌 빈도의 감소가 있는 반면, 맞춤형 문화와 지역적 기후 변화로 인한 손상이 기초 수요를 지원하고 있습니다. 공구, 진단 장비, 공장 소모품은 독립형 정비 공장이 복잡한 소프트웨어 구동 차량 시스템의 정비 체계를 갖추면서 확대되고 있습니다.

The United States aftermarket automotive parts and components market is expected to grow from USD 229.31 billion in 2025 to USD 238.75 billion in 2026 and is forecast to reach USD 292.27 billion by 2031 at 4.12% CAGR over 2026-2031.

A longer average vehicle age, strong light-truck sales, and rapid e-commerce uptake underpin this expansion. Elevated new-vehicle prices, wider right-to-repair statutes, and post-pandemic driving recovery stimulate replacement demand, while emerging electrified retrofit kits carve out premium specialty niches. Competitive intensity varies by component category, yet suppliers that pair omnichannel distribution with electronics expertise are positioning for durable growth. Regulatory initiatives, from EPA emissions rules to state EV mandates, act as simultaneous headwinds and tailwinds, reshaping the aftermarket automotive parts market through shifting compliance requirements.

Light trucks are poised to take the automotive market by storm, likely capturing a substantial share of new-vehicle sales by 2027. Each of these robust vehicles commands a higher aftermarket expenditure compared to traditional passenger cars, reflecting their unique demands and capabilities. The components that comprise these trucks, suspension, braking, and drivetrain parts, must endure considerably greater stress due to the hefty loads they tow and carry.

As lifestyle trends like overlanding, trailering, and outdoor adventures gain popularity, the appetite for performance-enhancing upgrades swells. Enthusiasts are seeking out lift kits, heavy-duty shocks, and oversized tires to elevate their driving experiences and tackle rugged terrains. The market for specialty equipment tailored to pickups has already surpassed an impressive USD 16 billion annually, prompting manufacturers to roll out dedicated product lines for these versatile vehicles.

Light-truck owners are often passionate about customization, leading to an average transaction value for upgrades that frequently eclipses that of standard replacements. This trend not only enhances the aesthetics and functionality of their trucks but also elevates profit margins across the aftermarket automotive parts sector, signaling a thriving market with boundless potential.

The vast majority of aftermarket transactions now traverse the dynamic landscape of digital channels, far surpassing the overall adoption of retail e-commerce across the United States. This remarkable shift allows online storefronts to showcase specialized SKUs without the burdensome costs of inventory that traditional brick-and-mortar wholesalers encounter. As a result, they can effortlessly provide nationwide access to hard-to-find parts for vintage models, catering to enthusiasts and collectors alike. Drop-shipment logistics and real-time inventory data reduce lead times for DIYers and small garages, redistributing market power toward digitally savvy suppliers. Yet counterfeit inflow remains an acute risk; federal enforcement actions underscore the importance of brand-protection programs . Firms that combine robust authentication technology with user-friendly interfaces are capturing a disproportionate share of the expanding digital aftermarket.

Automatic emergency braking and lane-keeping systems are cutting crash rates, trimming demand for bumpers, fenders, and lamps. Collision frequency declines most among late-model premium vehicles, where ADAS penetration is highest, compressing volumes for cosmetic body parts. Offsetting this decline, repairs on ADAS-equipped vehicles command higher invoice values due to mandatory sensor calibration and longer labor hours. Replacement of damaged cameras or radar modules fosters growth in specialized electronics sub-segments. Collision-repair centers are upskilling and investing in advanced scan tools, benefiting parts suppliers that offer OE-grade sensors and calibration fixtures.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passenger cars accounted for 52.74% of the United States Aftermarket Automotive Parts and Components Market overall revenue in 2025, anchored through an expansive installed base. Nevertheless, commercial light trucks are projected to post a 7.05% CAGR, elevating their contribution to the aftermarket automotive parts market size as parcel delivery and service fleets log higher daily mileage. Combining intensive duty cycles and stringent uptime requirements lifts replacement frequency for brake assemblies, driveline joints, and cooling components. Fleet operators' procurement practices favor suppliers that guarantee rapid availability and streamlined warranty processes, nudging parts makers toward depot-level inventory and predictive fulfillment systems.

Medium and heavy trucks yield outsized monetary value, while smaller in volume, because individual components carry higher price tags and downtime penalties. EPA 2027 emissions rules motivate prebuy activity and aftermarket retrofits of selective catalytic reduction and particulate filters, temporarily boosting heavy-duty demand. Buses and coaches, newly segmented in the forecast, open ancillary potential for specialist providers of high-capacity thermal-management and suspension products. Passenger-car segments remain relevant but confront a plateauing unit base as households question the need for multiple vehicles in the era of hybrid work, whereas fleet vehicles appear locked into growth trajectories tied to logistics expansion.

Engine components retained 31.45% of the United States Aftermarket Automotive Parts and Components Market in 2025, mirroring the still-dominant ICE parc. Yet ADAS sensors are forecast for a 7.52% CAGR, signaling the pivot from mechanical to electronic value. Camera modules, radar units, and control ECUs often fail in minor collisions or succumb to environmental contaminants, creating high-margin replacement cycles. Continental's 2024 launch of 700 new engine-management SKUs illustrates suppliers' dual strategy of defending mechanical strongholds while scaling electronics portfolios.

Suspension, brake, and tire categories see ongoing lift from the trend toward heavier SUVs and pickups. Electrical and infotainment sub-segments increase as drivers seek connectivity upgrades and over-the-air functionality, blurring the line between aftermarket hardware and software services. Body and exterior parts face mixed fortunes: ADAS reduces collision frequency, yet personalization culture and regional climate damage sustain baseline demand. Tools, diagnostics, and shop consumables are expanding as independent garages gear up to service complex, software-driven vehicle systems.

The United States Aftermarket Automotive Parts and Components Market is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component Type (Engine Components, Transmission and Driveline, and More), Sales Channel (Online and Offline), Propulsion Type (ICE Vehicles, and More), and by Service Channel (DIY, DIFM Independent Garages, and More). The Market Forecasts are Provided in Terms of Value (USD).