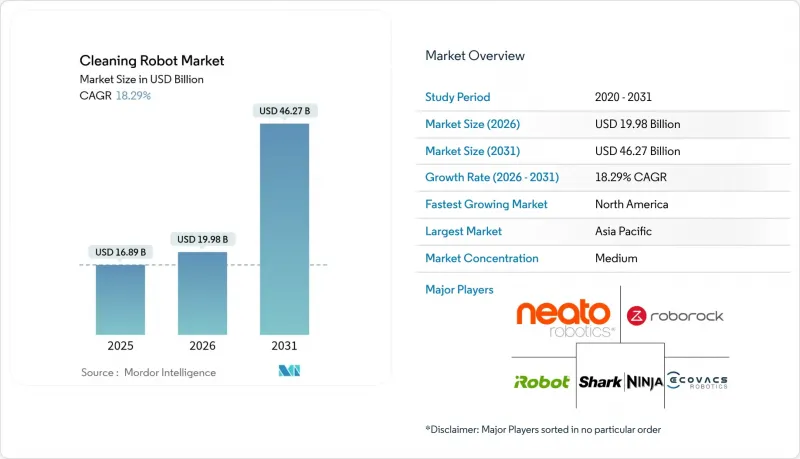

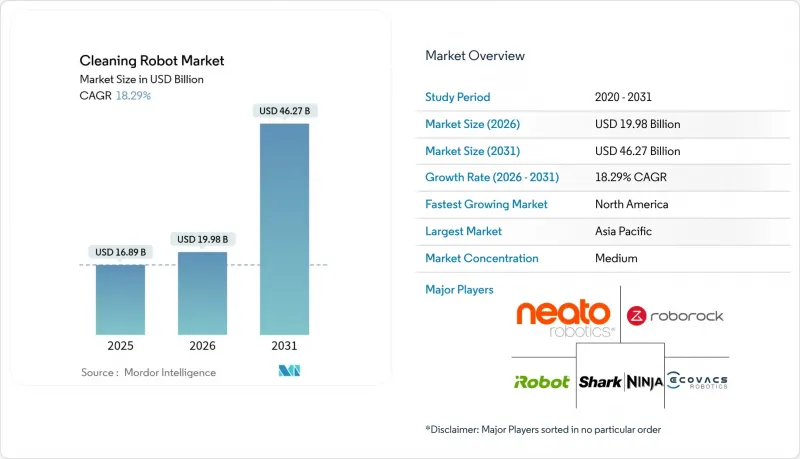

청소 로봇 시장은 2025년 168억 9,000만 달러에서 2026년에는 199억 8,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 18.29%를 기록하며 2031년까지 462억 7,000만 달러에 달할 것으로 예측됩니다.

비접촉식 위생 솔루션에 대한 강한 수요, 스마트홈의 급속한 보급, 센서 부품 비용의 대폭적인 하락으로 청소 로봇 시장은 지속적으로 성장하고 있습니다. 상업시설 관리자들은 자율 청소가 노동력 최적화에 있어 중요한 임무로 인식하는 경향이 증가하고 있으며, 주택 구매자들은 LiDAR 가격 하락과 E-Commerce를 통한 손쉬운 가용성의 혜택을 누리고 있습니다. 고체 LiDAR의 공급 측면의 규모의 경제와 서비스형 로봇(RaaS) 구독이 결합하여 소유 장벽을 낮춤으로써 청소 로봇 시장을 더욱 확대하고 있습니다. 수직적으로 통합된 아시아 제조업체들의 경쟁 심화는 수익률을 압박하고 있지만, 동시에 제품의 다양성과 지역적 가용성을 가속화하고 있습니다.

대부분의 공공 및 민간 시설에서 COVID-19 시대의 청소 프로토콜이 제도화되면서 자율형 바닥 청소 로봇과 UV-C 소독 로봇에 대한 수요가 지속되고 있습니다. 야간 로봇 운영을 실시하는 공항에서는 노동력 절감 효과와 승객의 신뢰도 향상을 입증하고 있습니다. 싱가포르 공공부문의 자율 청소 로봇의 대규모 도입 입찰은 정부가 지속적인 위생 프로그램을 지지하고 있음을 보여줍니다. 의료 사업자들도 인력을 늘리지 않고 감염 위험을 줄이기 위해 ISO 13482 인증 획득 모델에 의존하고 있습니다. 규제 당국의 지속적인 관심과 사용자의 기대가 결합되어 청소 로봇 시장은 높은 성장 경로를 유지하고 있습니다.

스마트홈 허브는 현재 바닥 청소 로봇의 스케줄 조정, 음성 제어, 원격 진단을 동기화하여 단순한 가제트에서 홈 오토메이션의 핵심 노드로 격상시키고 있습니다. 주요 벤더의 Matter 인증 장치는 상호운용성 장벽을 제거하여 대상 사용자층을 확대하고 있습니다. 중국, 인도, 동남아시아에서는 중산층의 소득 증가로 AI 기반 장애물 인식과 하이브리드 내비게이션이 결합된 프리미엄 제품 구매가 증가하고 있습니다. 이러한 추세는 계속해서 신규 사용자를 청소 로봇 시장으로 끌어들이고 있습니다.

중소기업의 경우, 50-200달러짜리 수동 공구를 300-3,000달러짜리 로봇으로 교체하는 데 여전히 주저하는 모습을 보입니다. 히드로 공항에서는 로봇 도입으로 연간 12만 4,175파운드(15만 5,219달러)의 인건비 절감을 실현했으며, 이사회 차원의 승인을 받기 위해 2년 미만의 투자 회수 기간을 증명해야 했습니다. 서비스로서의 로봇은 설비투자를 운영비용으로 전환하여 초기 비용 부담을 줄여주지만, 벤더는 계약의 매력을 유지하기 위해 배터리 열화 및 재배치 리스크를 관리해야 합니다.

2025년 청소 로봇 시장 규모에서 가정용 유닛, 특히 바닥 청소 로봇이 71.32%의 압도적인 점유율을 차지했습니다. 가격 하락 추세와 잦은 모델 업데이트가 가정용 수요를 견고하게 지탱하고 있으며, 수영장용이나 창문 청소 로봇 등 틈새 분야는 규모는 작지만 안정적으로 유지되고 있습니다. 반면, 산업용 로봇은 측정 가능한 투자 회수율과 시설 유지관리의 인건비 상승을 배경으로 18.42%의 CAGR을 기록할 것으로 예상됩니다. 특히 자외선이나 플라즈마 살균을 의무화하는 병원의 요청도 있어 소독 모델이 다른 모델보다 크게 성장하고 있습니다. 상업용 사용자는 환경 저항성 섀시, 교체 가능한 배터리, 습한 환경에 대한 인증된 보호 등급을 중요시합니다. 벤더 간 차별화는 계획되지 않은 다운타임을 줄이는 차량 관리 대시보드와 예지보전 데이터 분석에 초점이 맞춰지고 있습니다. 연장 서비스 계약은 총소유비용을 더욱 개선하고, 업무용 도입 경로를 확고히 합니다. 도입 가격은 높지만, 회수 기간은 단축되는 추세로 기차역, 쇼핑몰, 정부청사 등 다양한 산업에서 자율형 솔루션에 대한 조달이 진행되고 있습니다.

가정용 분야에서는 다층 매핑, 적응형 흡입 기능 등 전문가용 차량용으로 개발된 기능의 파급효과가 지속적으로 나타나고 있습니다. 건식 및 습식 청소가 가능한 하이브리드 모델은 가정 내에서의 호소력을 확대하고, 소모품 정기 배송 서비스는 고객을 브랜드 생태계에 정착시킬 수 있습니다. 주택 환경에서는 규제의 눈이 상대적으로 느슨하기 때문에 새로운 기능의 시장 출시 기간이 단축되고 있습니다. 전체적으로 두 영역은 서로를 보완하고 있습니다. 소비자 대상의 규모 확대가 하드웨어 비용을 낮추는 한편, 상업용 평균판매가격(ASP)이 고도의 연구개발을 재정적으로 뒷받침하여 청소 로봇 시장의 선순환을 지속하고 있습니다.

2025년 매출에서 주택 사용자가 차지하는 비중은 57.41%로, 스마트홈 통합의 확산과 입소문으로 인한 지지를 반영하고 있습니다. 그러나 병원, 진료소, 노인시설이 18.55%의 CAGR로 가장 빠르게 성장하고 있습니다. 감염 예방 예산이 영업시간 외 가동되는 UV-C 및 과산화수소 소독 로봇의 높은 가격 책정을 정당화하고 있습니다. 시설 관리자는 병원체 부하를 지속적으로 줄이고 직원의 안전을 향상시키는 것이 주요 구매 요인이라고 지적했습니다. 소매 체인점, 호텔, 레스토랑에서는 인력 부족에도 불구하고 서비스 환경을 유지하기 위해 소규모 로봇군을 도입하고 있습니다. 공항에서는 시간외 수당 없이 여객 피크에 대응하기 위해 24시간 가동되는 로봇을 활용하고 있습니다. 유연한 가동률을 실험하는 사무실에서는 IoT 점유 센서에 의해 트리거되는 주문형 청소를 도입하고 있습니다.

공장이나 창고에서는 분진이나 휘발성 화학제품을 안전하게 처리할 수 있는 ATEX 인증 획득 기계가 요구되고 있으며, 이는 청소 로봇 시장에서 틈새시장이면서 고수익을 올릴 수 있는 분야입니다. 최종사용자가 다양해짐에 따라 공급업체는 적재 용량, 탐색 알고리즘, 항균 소재의 선택을 개별 사용 사례에 맞게 조정해야 하므로 세분화의 복잡성이 증가하고 있습니다.

북미는 2025년에도 39.45%의 매출 점유율을 유지했습니다. 이는 미국 정부가 공항, 교통 거점, 학교 등을 대상으로 자율형 바닥 청소기를 조달한 데 따른 것입니다. 캘리포니아와 뉴욕주 병원에서는 병원내 감염 감소 효과를 정량화한 후 도입에 박차를 가하고 있습니다. 캐나다의 규제 정합성과 미국 벤더와의 지리적 근접성은 국경 간 확장을 용이하게 하고, 멕시코의 마킬라도라 집적지는 관세 리스크를 헤지하는 조립 투자를 유치하고 있습니다. 현재 이 지역의 성장은 신규 구매보다는 갱신 주기와 서비스 계약에 의해 뒷받침되고 있으며, 이는 청소 로봇 시장에서 성숙하면서도 수익성이 높은 부문임을 보여줍니다.

아시아태평양이 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)은 18.76%로 예측됩니다. 중국은 방대한 내수 수요와 수직 통합형 공급망을 결합하여 납기를 크게 단축하고 있습니다. '중국제조 2025' 구상에 따른 정부 보조금은 국내 브랜드가 동남아시아 및 중동 지역으로 수출하는 데 도움이 되고 있으며, 다른 지역에서의 경쟁력을 높이고 있습니다. 싱가포르에서는 여러 기관의 입찰을 통해 공공 공간에서 로봇 기술의 신뢰성을 입증했으며, 일본에서는 고령화가 진행되면서 간병인의 부담을 줄이기 위한 간병 보조 기기에 대한 수요가 증가하고 있습니다. 호주와 한국은 고급형 모델의 조기 도입 국가로 남아 있는 반면, 인도는 도시 중산층 가정을 타겟으로 한 가성비 중심의 SKU로 시장에 진입하고 있습니다.

유럽은 규제가 엄격하지만 꾸준한 성장세를 보이고 있습니다. 독일과 프랑스는 엄격한 위생 기준을 배경으로 산업 및 접객업 분야에서의 적용을 추진하고 있습니다. 영국에서는 서비스업이 주도적인 역할을 하고 있으며, 관세의 불확실성 속에서도 공항과 소매점에서 도입이 진행되고 있습니다. EU 기계 지침 2006/42/EC 및 EN 60335 안전 표준을 준수하는 것은 인증 비용을 증가시켜 시험 예산이 풍부한 기존 브랜드에 유리하게 작용할 수 있습니다. 에너지 비용과 노동력 부족이 자동화 투자를 지속적으로 촉진하고 있으며, 이 지역의 청소 로봇 시장 점유율은 두 자릿수 성장세를 유지하고 있습니다.

The cleaning robot market is expected to grow from USD 16.89 billion in 2025 to USD 19.98 billion in 2026 and is forecast to reach USD 46.27 billion by 2031 at 18.29% CAGR over 2026-2031.

Strong demand for touch-free hygiene solutions, rapid smart-home adoption, and sharp declines in sensor bills of material continue to propel the cleaning robot market. Commercial property managers increasingly view autonomous cleaning as mission-critical for labor optimization, while residential buyers benefit from lower LiDAR prices and easy e-commerce access. Supply-side economies of scale in solid-state LiDAR, coupled with robots-as-a-service subscriptions, further expand the cleaning robot market by lowering ownership barriers. Intensifying competition from vertically integrated Asian manufacturers is compressing margins, yet it also accelerates product variety and regional availability.

Most public and private facilities have institutionalized COVID-19-era cleaning protocols, sustaining demand for autonomous floor-care and UV-C disinfection robots. Airports that run robots overnight report measurable labor savings and better passenger confidence. Singapore's public-sector tenders for large fleets of autonomous cleaners underscore the government's endorsement of continuous hygiene programs. Healthcare operators also lean on ISO 13482-certified models to mitigate infection risks without adding staff. Sustained regulatory attention and user expectations together keep the cleaning robot market on a high-growth path.

Smart-home hubs now synchronize scheduling, voice control, and remote diagnostics for floor-care bots, elevating them from gadgets to integral home-automation nodes. Matter-certified devices from leading vendors remove interoperability friction and broaden the addressable base. In China, India, and Southeast Asia, rising middle-class income fuels premium purchases that bundle AI-based obstacle recognition and hybrid navigation. These dynamics continue to funnel new users into the cleaning robot market.

Small businesses still hesitate to replace USD 50-200 manual tools with bots priced from USD 300 to USD 3,000. Even at Heathrow, where robots saved GBP 124,175 (USD 155,219) in annual labor, board-level approval required proof of sub-two-year payback. Robots-as-a-service mitigates sticker shock by converting capex into opex, but vendors must manage battery depreciation and redeployment risk to keep contracts attractive.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Domestic units, notably floor-vacuum robots, held a commanding 71.32% share of the cleaning robot market size in 2025. Consistent price erosion and frequent model refreshes keep household demand buoyant, while niche segments, such as pool and window cleaners, remain smaller yet stable. In contrast, professional robots are expected to book an 18.42% CAGR, driven by measurable ROI and rising labor costs in facility maintenance. Disinfection models are outpacing all others, thanks in part to hospital mandates for ultraviolet or plasma sterilization. Commercial buyers also value ruggedized chassis, replaceable batteries, and certified ingress protection for wet environments. Vendor differentiation is increasingly centered on fleet-management dashboards and predictive-maintenance data analytics that reduce unplanned downtime. Extended service contracts further improve the total cost of ownership, solidifying professional adoption pathways. Despite higher acquisition prices, payback periods are shrinking, tilting procurement toward autonomous solutions across various industries, including rail stations, shopping malls, and government buildings.

The domestic sphere continues to benefit from feature spillovers originally developed for professional fleets, such as multi-floor mapping and adaptive suction. Hybrids capable of wet and dry cleaning broaden household appeal, while subscription consumable deliveries lock customers into branded ecosystems. Regulatory attention is minimal in residential contexts, accelerating time-to-market for new features. Overall, both domains reinforce each other: the consumer scale reduces hardware costs, while commercial ASPs finance advanced R&D, sustaining a virtuous cycle for the cleaning robot market.

Residential users accounted for 57.41% of 2025 revenue, reflecting the widespread adoption of smart-home integration and word-of-mouth advocacy. Yet hospitals, clinics, and elder-care centers are the fastest movers with an 18.55% CAGR. Infection-prevention budgets justify premium pricing for UV-C or hydrogen-peroxide disinfection robots that operate after visiting hours. Facility managers cite consistent pathogen load reduction and enhanced staff safety as prime purchase triggers. Retail chains, hotels, and restaurants now deploy smaller fleets to maintain service ambiance amid staffing shortages. Airports leverage 24-hour robot operation to match passenger peaks without overtime premiums. Offices experimenting with flexible occupancy adopt on-demand cleaning triggered by IoT occupancy sensors.

Industrial plants and warehouses seek ATEX-certified units that safely handle dust and volatile chemicals, a niche yet high-margin segment of the cleaning robot market. As end-users diversify, vendors must tailor payload capacity, navigation algorithms, and antimicrobial material choices to distinct use cases, reinforcing segmentation complexity.

The Cleaning Robot Market is Segmented by Type (Domestic/Household Robots, Professional Robots), End-User (Residential, Commercial, Industrial), Navigation Technology (LiDAR SLAM, Visual SLAM, Hybrid, Random/Infrared, AI Sensor-Fusion), Sales Channel (Online, Offline), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 39.45% revenue share in 2025, led by the United States government's procurement of autonomous floor cleaners for airports, transit hubs, and schools. Hospitals in California and New York accelerated rollouts after quantifying reductions in hospital-acquired infections. Canada's regulatory alignment and proximity to U.S. vendors smooth cross-border expansion, while Mexico's maquiladora clusters attract assembly investments that hedge tariff exposure. Growth here now stems less from first-time purchases and more from refresh cycles and service contracts, signaling a maturing yet lucrative segment of the cleaning robot market.

The Asia-Pacific region is the fastest climber, with a 18.76% CAGR outlook to 2031. China blends massive domestic demand with vertically integrated supply chains, slashing delivery lead times. Government subsidies under the "Made in China 2025" initiative encourage domestic brands to export across Southeast Asia and the Middle East, thereby increasing competitive pressure elsewhere. Singapore's multi-agency tenders validate the credibility of robotics in public settings, while Japan's aging demographics elevate demand for caregiver adjuncts that relieve nursing staff. Australia and South Korea remain early adopters of premium models, whereas India is entering the market through value-oriented SKUs targeting urban middle-class households.

Europe demonstrates steady but regulation-heavy growth. Germany and France champion industrial and hospitality applications, leveraging stringent hygiene norms. The United Kingdom's service-sector dominance drives airport and retail deployments, even amid tariff uncertainties. Compliance with the EU Machinery Directive 2006/42/EC and the EN 60335 family of safety standards adds certification overhead, favoring established brands with deep testing budgets. Energy costs and tight labor pools continue to motivate automation investment, maintaining double-digit growth in the region's slice of the cleaning robot market.