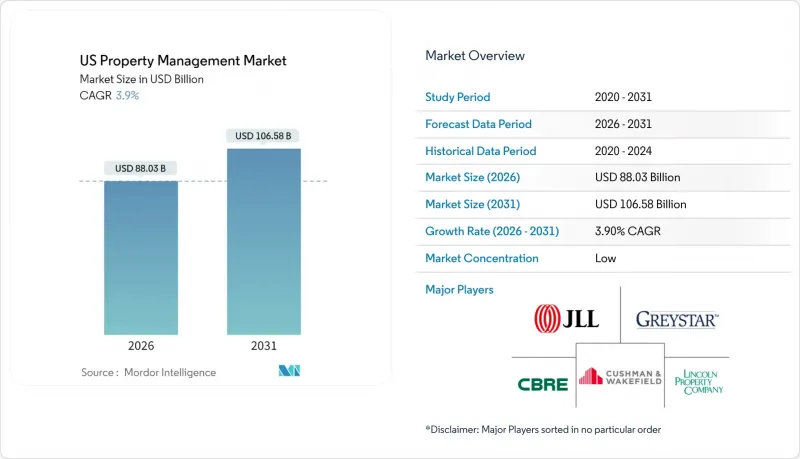

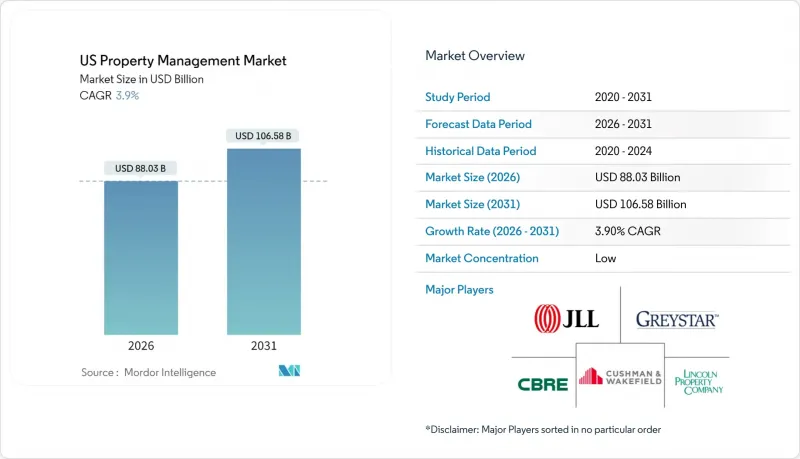

미국의 부동산 관리 서비스 시장은 2025년에 847억 3,000만 달러로 평가되며, 2026년 880억 3,000만 달러에서 2031년까지 1,065억 8,000만 달러에 달할 것으로 예측되고 있습니다. 예측 기간(2026-2031년)의 CAGR은 3.9%로 전망되고 있습니다.

이러한 성장은 탄탄한 임 대 수요, 단독 및 공동주택 자산의 기관투자자 소유, 그리고 고급 오피스 빌딩의 임대 활동 재개에 힘입어 성장세를 보이고 있습니다. 연방준비제도이사회 조사에 따르면 미국 성인의 27%가 주택을 임대하고 있으며, 이는 전문적인 관리가 필요한 대규모 세입자 기반을 지원합니다. 기관투자자들은 규모를 활용하여 전문적 관리를 추진하고, 환경-사회-지배구조(ESG) 규제는 컴플라이언스 중심의 서비스 수요를 가속화하고 있습니다. 기술 도입, 특히 임대 계약, 유지보수, 입주자 참여를 자동화하는 인공지능 툴은 효율성과 입주자 유지에 도움을 줄 수 있습니다. 전국 규모의 기업이 서비스 범위와 지역적 커버리지를 확대하기 위해 기술을 활용한 전문 기업을 인수하는 움직임이 활발해지면서 경쟁이 치열해지고 있습니다.

기관투자자의 단독주택 소유는 2010년대 초에 압류된 주택을 대량으로 임베디드하는 것에서 2024년까지 정교한 임대용 주택 건설 프로그램으로 발전했습니다. 미국 감사원(GAO)의 조사에 따르면 2015년 기준 17만-30만 가구의 보유가 확인되었으며, 현재는 펀드의 인수 가속화에 따라 더 큰 규모의 전개가 진행되고 있습니다. 예를 들어 American Homes 4 Rent는 2024년 61,336가구를 관리하며 17억 2,900만 달러의 임대 매출을 창출했습니다. 규모 확대에 따라 개인 임대인이 제공하기 어려운 표준화된 임대차 계약, 유지보수, 컴플라이언스 프로세스에 대한 수요가 증가하고 있습니다. 그 결과, 주택 전문업체와 통합형 REIT 플랫폼은 미국 부동산 관리 서비스 시장에서 가격 결정력과 지속적인 매출을 창출하고 있습니다.

하이브리드 근무 모델을 지원하는 고부가가치 공간을 찾는 기업이 증가함에 따라 프리미엄 오피스가 테넌트들의 주목을 다시 받고 있습니다. CBRE의 기록에 따르면 2024년 임대 수입은 18% 증가했고, 뉴욕의 사무실 임대료는 28% 급증했습니다. 트로피 빌딩의 소유주는 컨시어지 팀, 스마트 빌딩 플랫폼, 엄선된 테넌트 경험을 도입하여 공급 차별화를 꾀하고 있습니다. 이러한 부가 가치 서비스는 일반적으로 대규모 관리 예산이 필요하므로 전문 기업은 더 높은 수수료를 책정할 수 있습니다. 성능 벤치마킹과 어메니티 업그레이드는 에너지 관리 및 워크플레이스 컨설팅으로의 교차 판매 가능성도 창출합니다. 그 결과, 미국 부동산 관리 서비스 시장에서 A급 부동산 포트폴리오에 집중하는 관리회사들은 지속적인 매출 성장을 실현하고 있습니다.

2023년 말 이후 차입금 비용 상승으로 부동산 매각과 신규 개발이 중단된 상태입니다. CBRE에 따르면 기존 포트폴리오가 비교적 안정적임에도 불구하고 투자금액은 급감했습니다. 거래 감소는 온보딩 수수료와 건설관리 수수료로 매출을 창출하는 관리회사에게 부동산 인수 및 신축 개발 건수의 감소를 의미합니다. 거래량에 의존하는 중소기업은 단기적인 매출 압박에 직면해 있습니다. 그러나 지속적인 관리 계약이 그 영향을 완화시켜 미국 부동산 관리 서비스 시장 전체는 금리가 정상화되기 전까지 속도는 둔화되겠지만 지속적으로 확대될 수 있을 것으로 보입니다.

2025년 매출에서 주거용 부동산이 차지하는 비중은 49.35%로 미국 부동산 관리 서비스 시장에서 가장 큰 비중을 차지했습니다. 기관투자자 대상의 단독주택 및 공동주택 포트폴리오는 임대매출에 기반한 예측 가능한 지속적인 매출을 창출합니다. 한편, 편의시설이 잘 갖춰진 커뮤니티에서는 주차장, 수납공간, 스마트홈 구독 등으로 부수적인 수입이 창출되고 있습니다. 상업용 부동산은 4.82%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, A급 오피스 및 체험형 리테일 매장의 임 대 수요 회복에 따라 그 격차가 축소될 것으로 보입니다.

주택 부문은 인비테이션 홈즈(Invitation Homes)와 같은 REIT의 집중 투자로 인해 2024년 4억 2,520만 달러를 부동산 리노베이션에 투자했습니다. 규모 확대는 벤더 가격 협상력, 기술 도입, 대응 시간 개선으로 이어지며, 기관투자자에게 전문적인 관리가 필수 조건임을 입증하고 있습니다. 상업용 부동산의 성장은 기업의 고급 부동산으로의 이전과 기존 건물에 통합된 새로운 유연한 업무 공간 모델에 의해 촉진되고 있습니다. 산업 및 물류 자산은 EC 기업이 소비자와 가까운 위치를 원하고 전문적인 유지보수 및 보안 프로토콜에 의존하는 경향으로 인해 더 많은 성장 여지를 가지고 있습니다. 이러한 추세와 함께 미국 부동산 관리 서비스 시장은 균형 잡힌 성장을 유지하고 있습니다.

The US Property Management Services Market was valued at USD 84.73 billion in 2025 and estimated to grow from USD 88.03 billion in 2026 to reach USD 106.58 billion by 2031, at a CAGR of 3.9% during the forecast period (2026-2031).

Growth rests on resilient rental demand, institutional ownership of both single-family and multifamily assets, and renewed leasing activity in premium office buildings. Federal Reserve surveys show 27% of U.S. adults rent their homes, underpinning a large tenant base that requires professional oversight. Institutional investors use scale to drive professional management, while environmental, social, and governance (ESG) regulations accelerate demand for compliance-oriented services. Technology adoption, especially artificial-intelligence tools that automate leasing, maintenance, and resident engagement, further supports efficiency and tenant retention. Competitive intensity is rising as national firms buy tech-enabled specialists to widen service breadth and geographic reach.

Institutional ownership of single-family homes grew from bulk foreclosure purchases in the early 2010s to sophisticated build-for-rent programs by 2024. The GAO traced holdings of 170,000-300,000 homes by 2015, with larger footprints today as funds accelerate acquisitions. American Homes 4 Rent, for example, managed 61,336 homes and generated USD 1.729 billion rental revenue in 2024. Scale drives demand for standardized leasing, maintenance, and compliance processes that individual landlords rarely provide. Consequently, residential specialists and integrated REIT platforms gain pricing power and recurring revenue inside the US property management services market.

Premium office assets are regaining tenant attention as employers seek high-amenity space to support hybrid work models. CBRE recorded 18% leasing revenue growth in 2024, including a 28% jump in office leasing in New York. Owners of trophy buildings deploy concierge teams, smart-building platforms, and curated tenant experiences to differentiate supply. These value-added services typically require large management budgets, allowing professional firms to command higher fees. Performance benchmarking and amenity upgrades also create cross-selling potential for energy management and workplace consulting. The result is durable revenue growth for managers focused on Class-A portfolios within the US property management services market.

Elevated borrowing costs since late 2023 have caused a pause in property sales and ground-up development. CBRE noted that investment volume fell sharply even as existing portfolios remained relatively stable. Less trading means fewer property takeovers and new-build assignments for managers who earn onboarding and construction-management fees. Smaller firms that rely on deal flow face near-term revenue stress. Nonetheless, recurring management contracts cushion the impact, allowing the broader US property management services market to continue expanding, albeit at a slower clip until rates normalize.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Residential properties accounted for 49.35% of 2025 revenue, making them the largest slice of the US property management services market share. Institutional single-family rentals and multifamily portfolios deliver predictable, recurring fees based on rent rolls, while amenity-rich communities drive ancillary income from parking, storage, and smart-home subscriptions. Commercial properties are projected to register a 4.82% CAGR and will narrow the gap as leasing rebounds in Class-A offices and experiential retail.

The residential segment benefits from concentrated holdings by REITs such as Invitation Homes, which invested USD 425.2 million in property upgrades in 2024. Scale improves vendor pricing, technology adoption, and response times, reinforcing professional management as table stakes for institutional owners. Commercial growth is fueled by corporate flight to quality and new flexible-workspace models integrated into traditional buildings. Industrial and logistics assets add further upside as e-commerce firms seek proximity to consumers and rely on specialized maintenance and security protocols. Together, these dynamics sustain balanced momentum in the US property management services market.

The US Property Management Services Market Report is Segmented by Property Type (Commercial, Residential, Industrial & Logistics, and More), by Service Type (Marketing & Leasing, Property Evaluation & Due Diligence, Tenant & Resident Services, Maintenance & Facility Management, and More), and by Geography (Northeast, Midwest, Southeast, West and Southwest). The Market Forecasts are Provided in Terms of Value (USD).