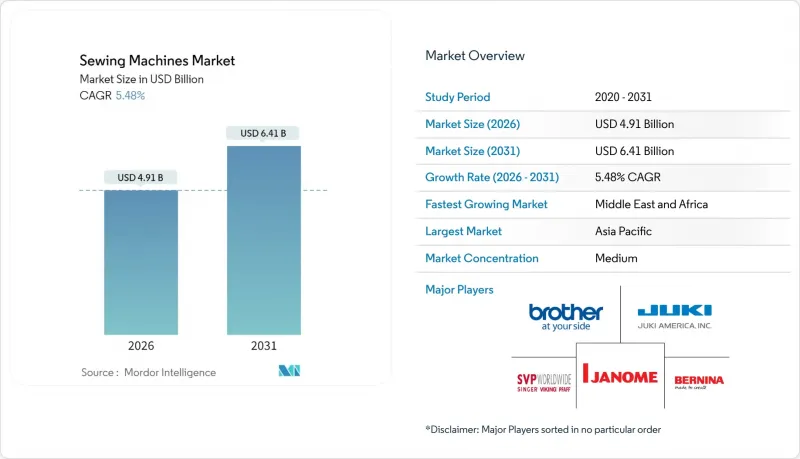

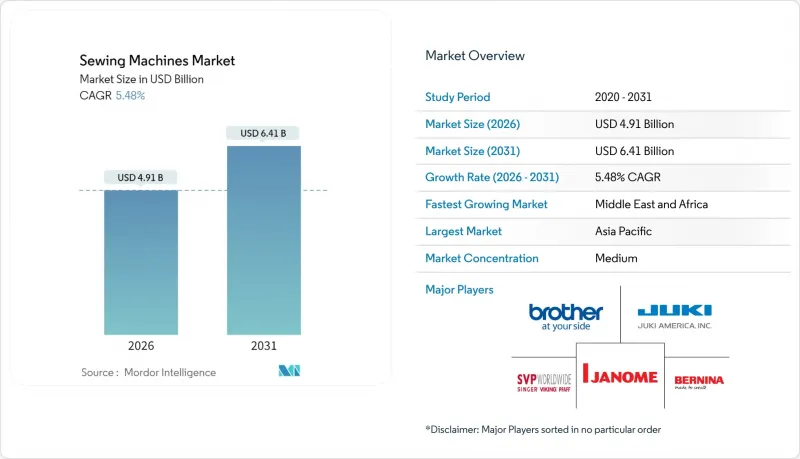

2026년 재봉틀 시장 규모는 49억 1,000만 달러로 추정되며, 2025년 46억 5,000만 달러에서 성장이 전망됩니다.

2031년의 예측에서는 64억 1,000만 달러에 달하며, 2026-2031년에 CAGR 5.48%로 확대할 전망입니다.

산업 자동화에 대한 수요 증가, 제조업체스 운동의 확산, 공장과 가정 모두에서 생산성을 향상시키면서 폐기물을 줄일 수 있는 기능의 빠른 업그레이드가 성장을 주도하고 있습니다. 제조업체는 아시아 지역의 대량 섬유 제품 수출과 북미와 유럽의 '수리 우선' 문화라는 두 가지 혜택을 누리고 있습니다. Wi-Fi 연결성, 다운로드 가능한 스티치 라이브러리, 프로그래머블 로직 컨트롤러(PLC)로의 기술 업그레이드는 교체 주기를 연장시키면서 평균 판매 가격을 높여 판매량이 감소하더라도 수익성을 유지하도록 돕습니다. 의류 생산의 미국 및 서유럽으로의 니어쇼어링은 장기적인 공구 교환 없이 스타일 변경이 가능한 유연한 소량 생산용 산업 시스템의 잠재적 시장을 더욱 확대할 것입니다.

아시아 지역은 정부의 장려책과 수출 지향적 전략에 힘입어 의류 생산량에서 여전히 다른 지역을 능가하고 있습니다. 인도만 하더라도 2030년까지 섬유 수출액 3,500억 달러 달성을 목표로 하고 있으며, 고생산성 재봉틀 라인의 일괄 조달을 추진하고 있습니다. 테크니컬 텍스타일을 대상으로 한 생산 연동형 지원책으로 수작업이 필요 없고 다양한 원단 중량에 대응하는 자동화 기계에 대한 투자 회수 기간이 단축되고 있습니다. 기존 저비용 생산기지의 임금 상승으로 인해 제조업체들은 인건비를 상쇄할 수 있는 서보 모터가 장착된 기계나 프로그램 가능한 스티치 패턴이 있는 기계로 전환할 수밖에 없습니다. 베트남과 방글라데시의 공장 집적화는 애프터서비스 물류를 간소화하여 공급업체가 지역 서비스 거점을 설립하는 데 도움이 되고 있습니다. 주문이 기본 티셔츠에서 고부가가치 운동복 및 정장류로 전환됨에 따라 복잡한 봉제 구조와 디지털 플래튼 조정이 가능한 기계에 대한 수요가 증가하고 있습니다.

Z세대 소비자들에게 가정용 재봉틀은 개인화된 패션을 실현하고 섬유 폐기물을 줄이는 수단이며, SNS의 튜토리얼은 그들의 관심을 구체적인 하드웨어 판매로 연결하고 있습니다. 소매업체는 초보자를 위한 세트를 기획하고, 초보자용 재봉틀과 다운로드 가능한 패턴을 결합하여 학습의 문턱을 낮추었습니다. 재봉틀은 팬데믹 기간 중 취미로 확산된 재봉틀은 록다운 이후에도 스트레스 해소 습관으로 자리 잡았고, 다른 홈 인테리어 카테고리가 정상화되는 와중에도 높은 수준의 소매 판매량을 유지하고 있습니다. 컴팩트한 디자인은 좁은 주거공간에 적합하고, 스마트폰 스타일의 터치스크린은 디지털 네이티브 세대의 공감을 불러일으키며, 제조업체는 기계적인 복잡성보다 직관적인 사용자 경험을 우선시할 수밖에 없습니다. Etsy와 같은 수공예품 재판매 플랫폼의 등장은 취미의 수익화를 촉진하고, 사용자가 기본 기능을 졸업하면 장비의 업그레이드를 촉진합니다.

벤더 파이낸스 옵션은 존재하지만, 하드웨어만을 대상으로 하며, 교육 및 유지보수는 융자 대상에서 제외됩니다. 은행은 종종 담보를 요구하지만, 소규모 공방은 담보가 부족하고, 현대화 주기가 늦어지고, 생산 현장에서는 10년 전의 락 스티치 기계가 계속 사용되고 있습니다. 봉제선의 강도와 디지털 추적성에 대한 브랜드의 요구가 점점 더 엄격해지는 가운데, 투자를 미루는 것은 경쟁력을 약화시키는 요인이 될 수 있습니다. 2024년 JUKI가 도입한 리스 프로그램은 베트남에서 일찍이 도입되었지만, 다른 지역에서는 여전히 생소한 존재입니다. 이는 부분적으로 사업자들이 독점 소프트웨어 생태계에 대한 장기적인 구속을 우려하고 있기 때문입니다.

2025년 전기 모델의 매출 비중은 64.35%를 차지할 것으로 예상되며, 이는 공장과 가정 모두에서 높은 범용성을 입증합니다. 많은 산업용 구매자들은 서보 드라이브와 반자동 실 절단 장치를 추가하여 기계의 수명 주기를 연장하고 완전 자동화를 위한 중간 단계로 이 부문을 포지셔닝하고 있습니다. 한편, 자동화 유닛은 공장들이 안정적인 봉제 품질과 수작업 감소를 추구하면서 2031년까지 연평균 복합 성장률(CAGR) 6.62%로 확대될 것으로 예측됩니다. 자동화 시스템 재봉틀 시장 규모는 스포츠웨어 및 테크니컬 섬유 공장 수요 증가를 반영하여 확대 추세에 있습니다. 수동식 재봉틀은 전력망이 불안정한 지역에서 여전히 존재감을 드러내고 있으며, 촉각적 조작을 중시하는 장인층에서 탄탄한 틈새 시장을 형성하고 있습니다.

전동식이 계속 주류를 이루고 있는 배경에는 풍부한 예비 부품과 작업자의 보편적 숙련도에 따른 교육 기간 단축이 있습니다. Singer의 Wi-Fi 지원 M3330은 기존 카테고리가 완전한 CNC의 복잡성에 뛰어들지 않고도 스마트 기능을 흡수하는 좋은 예입니다. 유압식 퀼팅기는 "기타" 범주에 속하며, 매트리스 제조 분야에서 성공을 거두었으며, 튀르키예, 폴란드 등으로 지역적 확장을 확대하고 있습니다. 전동식과 보급형 자동화 시스템 간의 가격 차이는 18%까지 줄어들었으며, 이 수준은 재무 책임자가 업그레이드를 승인하기 시작하는 임계값입니다.

의류 분야는 패스트 패션 대기업과 유니폼 공급업체로부터의 막대한 주문량으로 인해 2025년 매출의 57.85%라는 압도적인 점유율을 유지했습니다. 스포츠웨어 분야에서는 스트레치 원단에 대응하는 차동 이송 오버록 재봉틀에 대한 수요가 증가하면서 OEM 업체들이 전용 노루발을 번들로 제공하는 움직임이 나타나고 있습니다. 커튼과 쿠션 커버를 포함한 홈텍스타일은 주택 소유자의 개인화된 장식에 대한 투자로 인해 CAGR 6.69%로 가장 빠르게 성장하는 틈새 시장입니다. 가정용 재봉틀 시장 점유율은 2024-2025년 사이 120bp 상승하여 가정용 재봉틀 시장 점유율이 지속적으로 가정내 맞춤화로 전환되고 있음을 보여줍니다. 자동차 내장재, 의료용 일회용 제품, 산업용 필터가 비의류 분야를 구성하며, 모두 고부하 대응 바늘과 강화된 작업대를 필요로 합니다.

지속가능한 인테리어에 대한 소비자 선호도가 높아지면서 프리미엄 원사에 대한 수요가 증가하고 있으며, 친환경 염색 원사를 공급하는 American &Efird사 등 자회사에 이익을 가져다주고 있습니다. 자동차 시트 제조업체는 초당 40 스티치 바택 기능을 요구하고 있으며, 고토크 서보 모터를 통합할 수 있는 공급업체에 기회가 생기고 있습니다. 의료용 PPE 분야에서는 초음파 재봉 기술이 경쟁하고 있지만, 규제 감사에서는 여전히 중요한 가운에는 재봉 솔기가 권장되고 있습니다. 인도 도시 지역의 가처분 소득 증가에 따라 가정내 비즈니스에서 수익화가 가능한 자수 전용 기계 시장이 확대되고 있습니다. 이러한 다각화는 의류 제조의 경기 변동성을 완화하고 의류 불황시 OEM 매출에 도움을 주고 있습니다.

2025년 아시아태평양이 50.60%의 매출 점유율을 차지할 것으로 예상되는 배경에는 섬유에서 패션에 이르는 밸류체인의 독보적인 규모와 중산층의 소비 증가가 반영되어 있습니다. 인도에서는 생산 연동형 장려금 제도가 지속적으로 도입되어 자본 투자의 최대 15%를 환급해주기 때문에 공장 현대화가 빠르게 진행되고 있습니다. 중국 OEM 업체들은 세계 브랜드에 서보 부품 및 휴먼-머신 인터페이스 공급을 확대하고 있으며, 기능 업데이트의 리드 타임 단축에 기여하고 있습니다. 베트남의 의류 수출 확대에 따라 공급업체는 호치민시에 서비스 창고를 건설하여 부품 교체에 따른 다운타임을 줄이기 위해 노력하고 있습니다. 또한 자카르타 및 방콕의 소매 체인은 초보자를 위한 가정용 키트 판매량이 두 자릿수 성장을 보고하는 등, 이 지역에서는 공예 취미에 대한 소비자의 열정이 증가하고 있습니다.

중동 및 아프리카는 이집트의 수에즈 운하 경제구역과 같은 산업단지와 면세 혜택이 결합된 인프라 회랑에 힘입어 6.89%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 보일 것으로 예측됩니다. 에티오피아 하와사 산업단지에는 이미 25개의 의류 제조업체가 입주해 있으며, 세관 데이터에 따르면 2024년에는 총 5,000대 이상의 프로그램 가능한 잠금 재봉틀을 수입할 것으로 예상하고 있습니다. 걸프협력회의(GCC) 회원국들은 비전 2030 계획에 따라 섬유산업에 대한 투자를 장려하고 있으며, 사우디는 통합공장을 위해 5억 달러의 융자금을 배정했습니다. 아프리카의 소비자 시장도 성숙하고, 나이지리아의 E-Commerce 플랫폼에서는 축제 시즌에 매진되는 중급급 휴대용 모델이 판매되고 있습니다. 문제는 교육에 있습니다. OEM 업체는 나이로비와 아크라의 직업 훈련 기관과 협력하여 기본적인 정비에 대한 운영자 인증을 실시했습니다.

북미에서는 현지 생산 의류를 중시하는 소비자와 예측할 수 없는 태평양 횡단 운송에 직면한 브랜드가 원동력이 되어 국내 생산이 부활하고 있습니다. 나이키 등의 브랜드는 오리건 주에서 여러 소재를 재봉할 수 있는 CNC 재봉 헤드를 이용한 자동화 라인을 시범적으로 도입하고 있습니다. 노스캐롤라이나주와 사우스캐롤라이나주에서는 주정부 차원의 보조금을 통해 레거시 공장을 스마트 팩토리로 업그레이드하는 데 필요한 설비 구매를 보조하고 있습니다. 캐나다의 의류 중소기업은 최종사용자가 맞춤형 패턴을 설계할 수 있는 온라인 구성기를 도입하여 디지털 입력 파일 지원 기계에 대한 수요를 간접적으로 증가시키고 있습니다. 멕시코는 미국 바이어들이 신속대응형 소매 모델에 대응하기 위해 인근 조달을 추진하면서 파급효과를 누리고 있습니다.

유럽에서는 성숙한 산업 기반과 첨단인 지속가능성 정책이 융합되어 설비 사양의 재정의가 진행되고 있습니다. 2027년까지 시행되는 에코 디자인 지침은 기계 단위의 정밀한 에너지 소비량 측정을 의무화하고 있으며, OEM 업체들은 고효율 서보 모터로 전환해야 하는 상황에 직면해 있습니다. 독일은 자동차 및 항공우주용 테크니컬 텍스타일 분야에서 선도적인 위치를 유지하고 있으며, 고내구성 프로그래머블 배타커에 대한 수요를 불러일으키고 있습니다. 이탈리아의 고급 패션 브랜드에서는 '메이드 인 이탈리아'의 신뢰성을 유지하기 위해 자동화 설비와 병행하여 수작업으로 자수 장인을 활용하고 있습니다. 루마니아와 불가리아의 동유럽 공장은 물류 불안정으로 인해 아시아에서 전가된 수주를 수주하여 기계군의 급속한 확충이 요구되고 있습니다.

남미에서는 브라질 산타카타리나주의 의류 클러스터가 현대화를 추진하고 전기료 상승에 따른 에너지 절약 대책으로 서보모터 개보수를 도입하는 등 꾸준한 추진력을 보이고 있습니다. 우루과이와 파라과이는 중국 투자자를 대상으로 면화에서 의류까지 통합 생산단지를 유치하고 있으며, 이를 통해 설비 수요의 현지화를 기대하고 있습니다. 한편, 칠레에서는 E-Commerce의 확산과 함께 소형 가정용 재봉틀이 취미로 보급되고 있습니다. 환율 변동이 여전히 주요 역풍 요인으로 작용하고 있으며, 수입 기계 구매 결정은 환율이 안정될 때까지 미루는 경우가 많습니다.

Sewing machine market size in 2026 is estimated at USD 4.91 billion, growing from 2025 value of USD 4.65 billion with 2031 projections showing USD 6.41 billion, growing at 5.48% CAGR over 2026-2031.

Industrial automation requirements power growth, the widening maker movement, and rapid feature upgrades that allow both factories and households to boost productivity while reducing waste. Manufacturers benefit from dual exposure: large-volume textile exports in Asia and the repair-over-replace culture in North America and Europe. Technology upgrades toward Wi-Fi connectivity, downloadable stitch libraries, and programmable logic controllers lengthen replacement cycles yet raise average selling prices, supporting revenue even when unit volumes plateau. Near-shoring of garment production back to the United States and Western Europe further expands the addressable base for flexible, small-batch industrial systems that can switch styles without lengthy retooling.

Asia continues to outpace every other region in apparel output, fueled by public incentives and export-oriented strategies. India alone targets USD 350 billion in textile exports by 2030, stimulating bulk procurement of high-throughput sewing lines . Production-linked schemes covering technical textiles lower the payback period on automated machines that handle multiple fabric weights without manual intervention. Growing wages in legacy low-cost centers push manufacturers toward units with servo motors and programmable stitch patterns that offset labor costs. Factory clustering in Vietnam and Bangladesh simplifies after-sales logistics, encouraging suppliers to embed regional service hubs. As orders shift from basic tees to higher-value athleisure and formalwear, demand tilts toward machines capable of complex seam constructions and digital platen adjustments.

Gen Z consumers view home sewing as a route to personalized fashion and lower textile waste, and social media tutorials convert that interest into measurable hardware sales. Retailers now curate starter bundles that pair entry-level machines with downloadable patterns, easing the learning curve. Pandemic-era hobby adoption has persisted post-lockdown as a stress-relief habit, keeping retail sell-through high even as other home-improvement categories normalize. Compact form factors that fit small apartments and smartphone-like touchscreens resonate with digital natives, forcing brands to prioritize intuitive UX over mechanical complexity. The rising tide of reseller platforms for handmade items, such as Etsy, further monetizes the hobby, reinforcing equipment upgrades once users outgrow basic functions.

Vendor financing options exist yet cover only the hardware, leaving training and maintenance outside loan packages. Banks often require collateral that small workshops lack, delaying modernization cycles and leaving production stuck with 10-year-old lockstitch units. Deferred investment saps competitiveness when brands demand tight tolerances on seam strength and digital traceability. Leasing programs introduced by JUKI in 2024 showed early adoption in Vietnam but remain a novelty elsewhere, partly because operators fear long-term commitment to proprietary software ecosystems.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Electric models accounted for 64.35% of revenue in 2025, underscoring their versatility for factories and households alike. Many industrial buyers regard the segment as an interim step toward full automation, adding servo drives and semi-automatic thread cutters to stretch machine life cycles. Automated units, meanwhile, are slated to expand at 6.62% CAGR through 2031 as factories chase consistent stitch quality and lower rework. The sewing machine market size for automated systems is growing, reflecting rising demand from sportswear and technical-textile plants. Manual machines linger in regions with unstable electricity grids, carving out a defensible niche among artisans who prize tactile control.

Continued dominance of the electric segment derives from abundant spare parts and universal familiarity among operators, decreasing training periods. Singer's Wi-Fi-ready M3330 illustrates how traditional categories absorb smart features without jumping to full CNC complexity. Hydraulically actuated quilting machines populate the "other" category and find success in mattress manufacturing, expanding geographic penetration into Turkey and Poland. Price gaps between electric and entry-level automated systems have narrowed to 18%, a threshold at which CFOs start green-lighting upgrades.

Apparel retained a commanding 57.85% slice of 2025 revenue due to vast order volumes from fast-fashion giants and uniform suppliers. Sportswear gains traction as stretch fabrics require differential-feed overlockers, prompting OEMs to bundle specialized presser feet. Home textiles, including curtains and cushion covers, represent the fastest-growing niche with a 6.69% CAGR as homeowners invest in personalized decor. The sewing machine market share for home-textile applications rose 120 basis points between 2024 and 2025, signaling a durable shift toward at-home customization. Automotive upholstery, medical disposables, and industrial filters round out the non-apparel group, each demanding heavy-duty needles and reinforced work tables.

Consumer preference for sustainable interiors boosts premium thread demand, benefiting subsidiaries like American & Efird that supply eco-dyed yarns. Car seat makers specify bar-tacking capabilities at 40 stitches per second, creating opportunities for providers that can integrate high-torque servo motors. In medical PPE, ultrasonic sewing alternatives compete, yet regulatory audits still favor stitched seams for critical gowns. Rising disposable income in urban India grows the market for embroidery-only machines that let users monetize home businesses. This diversification smooths cyclical dips in garment manufacturing, cushioning OEM revenue during apparel slowdowns.

The Sewing Machines Market Report is Segmented by Machine Type (Manual, Electric, and More), by Application (Apparel, Non-Apparel Textiles, and More), by End-User (Residential and Industrial), by Distribution Channel (B2C/Retail and B2B/Directly From the Manufacturers), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's 50.60% revenue leadership in 2025 reflects its unmatched scale in fiber-to-fashion value chains and ascending middle-class consumption. India continues to roll out Production Linked Incentives that reimburse up to 15% of capital investment, prompting mills to modernize quickly . Chinese OEMs increasingly supply servo components and human-machine interfaces to global brands, shortening lead times for feature updates. Vietnam's apparel export growth encourages suppliers to build service warehouses in Ho Chi Minh City, reducing downtime for spare-part replacements. The region also witnesses swelling consumer enthusiasm for craft hobbies, as retail chains in Jakarta and Bangkok report double-digit sales lift for entry-level home units.

The Middle East and Africa grows the fastest, projected at 6.89% CAGR, supported by infrastructure corridors like Egypt's Suez Canal Economic Zone that bundle industrial parks with duty exemptions. Ethiopia's Hawassa Industrial Park already houses 25 apparel manufacturers that collectively imported more than 5,000 programmable lockstitch machines in 2024 according to customs data. Gulf Cooperation Council states encourage textile investments under Vision-2030 plans, with Saudi Arabia earmarking USD 500 million loans for integrated mills. African consumer markets also mature; Nigeria's e-commerce platforms now list mid-range portable models that sell out during festival seasons. The challenge lies in training; OEMs partner with vocational institutes in Nairobi and Accra to certify operators on basic maintenance.

North America experiences a revival in domestic making, powered by consumers who value locally produced garments and by brands facing unpredictable trans-Pacific freight. Brands such as Nike pilot automated lines in Oregon that rely on CNC sewing heads capable of multi-material stitching. State-level grants in North Carolina and South Carolina subsidize equipment purchases for legacy mills upgrading to smart factories. Canada's apparel SMEs embrace online configurators that allow end-users to design custom patterns, indirectly boosting demand for machines that accept digital input files. Mexico secures spill-over benefits as US buyers near-source to comply with quick-response retail models.

Europe blends mature industrial bases with avant-garde sustainability policies that redefine equipment specifications. Eco-design directives coming into force by 2027 will require precise energy-consumption metrics at the machine level, nudging OEMs toward high-efficiency servo motors. Germany continues to lead in technical textiles for automotive and aerospace, prompting demand for heavy-duty programmable bartackers. Italy's luxury fashion houses employ specialized hand-guided embroiderers alongside automated equipment to uphold "Made in Italy" authenticity. Eastern European factories in Romania and Bulgaria win orders redirected from Asia due to logistics volatility, necessitating rapid scale-up in machine fleets.

South America exhibits steady momentum as Brazil's garment cluster in Santa Catarina modernizes, deploying servo-motor retrofits to capture energy savings under rising electricity tariffs. Uruguay and Paraguay court Chinese investors for integrated cotton-to-apparel complexes that could localize equipment demand. Meanwhile, Chile's e-commerce penetration fosters hobbyist uptake of compact home machines designed for small apartments. Currency fluctuations remain the principal headwind, often delaying purchase decisions for imported machines until exchange rates stabilize.