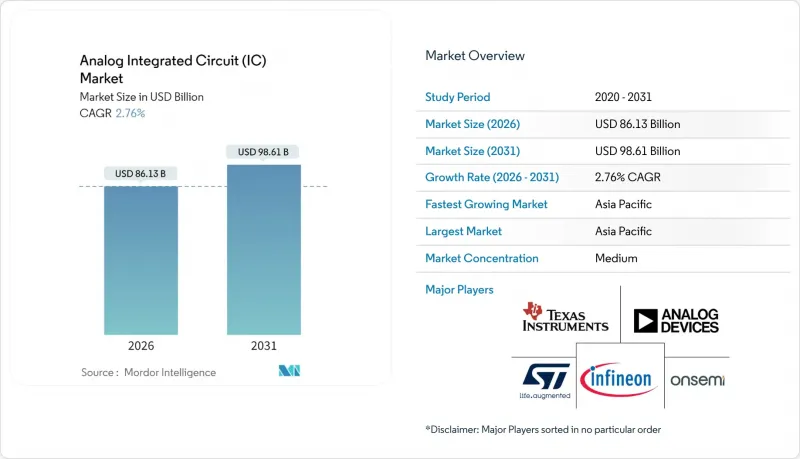

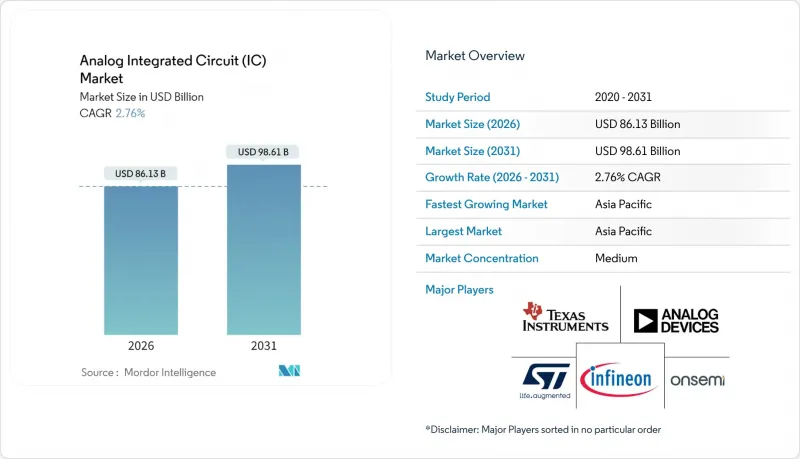

아날로그 집적회로(IC) 시장은 2025년에 838억 2,000만 달러로 평가되며, 2026년 861억 3,000만 달러에서 2031년까지 986억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 2.76%로 예상됩니다.

시장 성장은 자동차 전동화, 5G/6G 구축, 산업 자동화 노력에서 전력 효율적인 신호 조정, 배터리 관리, RF 프론트엔드 솔루션에 대한 안정적인 수요를 반영하고 있습니다. 엣지 AI 추론의 강화로 인해, 고정밀 전력 관리 및 인터페이스 장치에 대한 프리미엄 가격이 상승하고 있습니다. 한편, 성숙한 기술 노드는 낮은 설계 리스크와 높은 수율로 인해 수익성을 지속적으로 유지하고 있습니다. 300mm 팹으로의 생산 전환은 비용 구조의 개선과 아날로그와 디지털 통합의 고도화를 가능하게 하지만, 숙련된 혼합 신호 기술자 부족과 주기적인 소비자 수요는 생산 확대를 계속 억제하고 있습니다. 그러나 아날로그 IC 시장은 정밀 기능이 완전히 상품화되거나 디지털화될 수 없기 때문에 회복력을 보여주고 있습니다.

프리미엄 스마트폰 1대당 아날로그 부품 비용은 4G 단말기 18달러에서 5G 모델은 25달러로 상승했습니다. 이는 Doherty GaAs 증폭기가 34%의 효율로 31dBm 선형 출력을 실현하고 40nm CMOS 수신기가 60GHz에서 39dB의 이득을 달성했기 때문입니다. FinFET 기반 RF 회로는 밀리미터파 빔 포밍을 지원하여 고정밀 위상 시프터 및 저잡음 증폭기 IC에 대한 수요가 증가하고 있습니다. 대규모 MIMO 기지국 구축에는 여전히 아날로그 기술이 필수적인 엔벨로프 트래킹 드라이버와 고선형성 믹서가 필요합니다. 부품의 복잡성은 프리미엄 평균 판매 가격을 정당화하며, 휴대폰 출하량 변동에도 불구하고 아날로그 IC 시장을 지속시키고 있습니다. 아시아태평양공급망 현지화 구상은 이 지역의 아날로그 생산 능력 확대에 박차를 가하고 있습니다.

고전압 배터리 관리 IC는 현재 16비트 정밀도로 14셀 스택을 모니터링하고, 최대 31개의 디바이스를 데이지 체인으로 연결할 수 있습니다. 800V 팩의 기능 안전성을 보장합니다. 인피니언의 1200V SiC MOSFET은 상부 냉각을 통해 열 저항을 줄였습니다. 소형 11kW 차량용 충전기를 구현하여 95%의 효율을 달성합니다. 400V에서 800V로의 아키텍처 전환은 게이트 드라이버 IC의 혁신과 고정밀 전류 검출 기술을 추진하고 있습니다. 자동차 제조업체의 인증 주기는 다년간의 아날로그 부품 채택을 확정하여 공급업체의 장기적인 매출 기반을 강화하고, 아날로그 IC 시장의 안정성을 더욱 강화합니다. 중국, 유럽, 미국의 무공해 자동차에 대한 정부 지원책으로 인해 수요가 더욱 확대될 것으로 예측됩니다.

FinFET 및 게이트 올 어라운드 구조의 도입으로 기존의 아날로그 레이아웃 방식으로는 불가능한 가변성이 발생했습니다. 검증 주기가 36개월에 달하고, 마스크 세트 비용이 500만 달러가 넘기 때문에 중소기업의 진입을 제한하고 있습니다. 노드 간 아날로그 IP 마이그레이션을 위해서는 광범위한 실리콘 특성 평가가 필요하며, 이는 비반복적인 엔지니어링 비용을 증가시킵니다. 이러한 투자를 정당화할 수 있는 것은 고액 거래량 플랫폼뿐이며, 자금력이 있는 기업에게 시장 지배력이 집중되어 있습니다. EDA의 한계로 인해 시장 출시 시기가 늦어지고, 첨단 노드에서 아날로그 IC 시장의 성장 속도를 억제하고 있습니다.

2025년 아날로그 집적회로(IC) 시장의 30.65%는 전력관리 제품이 차지할 것으로 예상되며, AI 데이터센터의 수직 전력 공급과 800V EV 구동계가 견인차 역할을 하며 2031년까지 연평균 복합 성장률(CAGR) 3.98%로 확대될 것으로 전망됩니다. 인터페이스 IC는 증가하는 연결 규격으로 인해 매출 2위 자리를 유지합니다. ISO 26262를 준수하는 프로그래머블 PMIC는 진단용 ADC, 워치독 타이머, CAN/LIN 트랜시버가 내장되어 있으며, 단일 칩으로 전원 및 통신 모듈을 구현합니다. 머신러닝 지원 PMIC는 동적으로 에너지를 최적화하고, 아날로그 제어 루프와 임베디드 인텔리전스의 융합을 보여줍니다.

ADC와 DAC를 포함한 신호변환 부품은 산업기기와 민생기기의 센싱 보급으로 수요가 확대되고 있지만, 컨버터 IP를 번들로 제공하는 양산형 마이컴 벤더의 경쟁으로 단가가 압박을 받고 있습니다. 증폭기 및 비교기는 노이즈, 대역폭, 오프셋 파라미터가 설계 결정 요인이 되는 계측기 및 RF 체인 분야에서 여전히 중요한 역할을 하고 있습니다. 다양한 응용 분야가 결합되어 아날로그 IC 시장은 특정 부문의 부진에 영향을 덜 받는 구조로 되어 있습니다.

아시아태평양은 2025년 아날로그 IC 시장 점유율의 49.88%를 차지하며 4.37%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 중국의 국내 판매액은 2016년 5억 달러에서 2023년 17억 3,200만 달러로 증가하여 국가 주도의 자급자족 목표를 반영하고 있습니다. 인도의 2억 2,200만대 규모의 스마트미터 계획은 아날로그 부품의 대규모 공급 파이프라인을 확보하고 있습니다. 한편, 일본은 민관협력을 통해 아날로그 IC 생산능력을 회복하고 있습니다. 지역내 팹은 보조금을 활용하여 공급망 현지화를 촉진하고, 세계 OEM(Original Equipment Manufacturer)의 리드타임 유연성 향상과 물류 리스크 감소를 실현하고 있습니다.

북미는 CHIPS법 특혜를 활용하여 2032년까지 팹 생산능력을 3배로 확대. 아날로그 IC 제조업체는 지역적으로 분산된 공급처를 원하는 방위 및 자동차 분야의 고객을 타겟으로 삼고 있습니다. 유럽은 기능 안전과 환경 규제에 대한 대응력으로 고부가가치 틈새 시장을 유지하고 있습니다. 유럽 칩스법이 정한 '세계 생산 점유율 20%'라는 목표가 이를 지원하고 있습니다. 라틴아메리카와 아프리카의 신흥 시장에서는 전력망 현대화 및 연결성 향상을 위해 비용 최적화된 아날로그 솔루션이 채택되고 있습니다.

The analog IC market was valued at USD 83.82 billion in 2025 and estimated to grow from USD 86.13 billion in 2026 to reach USD 98.61 billion by 2031, at a CAGR of 2.76% during the forecast period (2026-2031).

Market growth reflects steady demand for power-efficient signal conditioning, battery management, and RF front-end solutions across automotive electrification, 5G/6G roll-outs, and industrial automation initiatives. Intensifying edge-AI inference pushes premium pricing for high-accuracy power-management and interface devices, while mature technology nodes remain profitable owing to lower design risk and strong yields. Capacity shifts toward 300 mm fabs improve cost structure and enable tighter analog-digital integration, yet skilled mixed-signal talent shortages and cyclical consumer demand continue to temper output expansion. Nevertheless, the analog IC market demonstrates resilience because its precision functions cannot be fully commoditized or digitized.

Analog content per premium smartphone climbed from USD 18 in 4G devices to USD 25 in 5G models as Doherty GaAs amplifiers now deliver 31 dBm linear power with 34% efficiency, while 40 nm CMOS receivers achieve 39 dB gain at 60 GHz. FinFET-based RF circuits support millimeter-wave beamforming, increasing demand for precision phase-shifter and low-noise amplifier ICs. Massive-MIMO base-station roll-outs require envelope-tracking drivers and high-linearity mixers that remain firmly analog. Component complexity justifies premium average selling prices, sustaining the analog IC market despite handset unit volatility. Supply-chain localization initiatives in Asia-Pacific accelerate regional analog capacity additions.

High-voltage battery-management ICs now monitor 14-cell stacks with 16-bit accuracy and daisy-chain up to 31 devices, ensuring functional safety in 800 V packs. Infineon's 1200 V SiC MOSFETs with top-side cooling lower thermal resistance, enabling compact 11 kW onboard chargers that reach 95% efficiency. Transition from 400 V to 800 V architectures drives gate-driver IC innovation and precision current sensing. Auto OEM qualification cycles lock-in multiyear analog content, anchoring long-term revenue streams for suppliers and reinforcing analog IC market stability. Government incentives for zero-emission vehicles in China, Europe, and the United States further magnify demand.

FinFET and gate-all-around structures introduce variability that invalidates classical analog layout heuristics; verification cycles now span 36 months and mask sets exceed USD 5 million, limiting entry for small firms. Analog IP migration across nodes demands extensive silicon characterization, raising non-recurring engineering costs. Only high-volume platforms justify such investment, concentrating market power among cash-rich players. EDA limitations delay time-to-market, suppressing analog IC market velocity in advanced nodes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Power-management products account for 30.65 of % analog IC market share in 2025 and will grow at a 3.98% CAGR through 2031, propelled by AI data-center vertical-power delivery and 800 V EV drivetrains. Interface ICs remain second in revenue thanks to proliferating connectivity standards. Programmable PMICs with ISO 26262 compliance now embed diagnostic ADCs, watchdog timers, and CAN/LIN transceivers, enabling single-chip power and communication modules. Machine-learning-enabled PMICs optimize energy dynamically, illustrating the convergence of analog control loops with embedded intelligence.

Signal-conversion components, including ADCs and DACs, benefit from ubiquitous sensing in industrial and consumer devices, but unit ASPs face competitive pressure from high-volume microcontroller vendors bundling converter IP. Amplifiers and comparators retain relevance in instrumentation and RF chains where noise, bandwidth, and offset parameters drive design-in decisions. Collectively, diversified applications insulate the analog IC market from segment-specific downturns.

The Analog Integrated Circuits (IC) Market Report is Segmented by Type (General-Purpose IC Including Interface, Power Management, Signal Conversion, Amplifiers/Comparators; Application-Specific IC Including Consumer, Automotive, and More), Technology Node (>65 Nm, and More), Wafer Size (150 Mm, 200 Mm, 300 Mm), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific captured 49.88% of the analog IC market share in 2025 and is forecast to expand at a 4.37% CAGR. China's domestic sales rose from USD 500 million in 2016 to USD 1.732 billion in 2023, mirroring state-backed self-sufficiency goals. India's 222 million-unit smart-meter program secures sizable analog content pipelines, while Japan revives analog IC capacity via public-private partnerships. Regional fabs capitalize on subsidies to localize supply chains, enhancing lead-time agility and lowering logistics risks for global OEMs.

North America leverages CHIPS-Act incentives to triple fab capacity by 2032; analog IC producers target defense and automotive customers seeking geographically diversified sources. Europe's regulatory acumen in functional safety and environmental compliance sustains high-value niches, buttressed by the European Chips Act's ambition for a 20% global output share. Emerging markets in Latin America and Africa adopt cost-optimized analog solutions for grid modernization and connectivity upgrades, albeit from a smaller base.