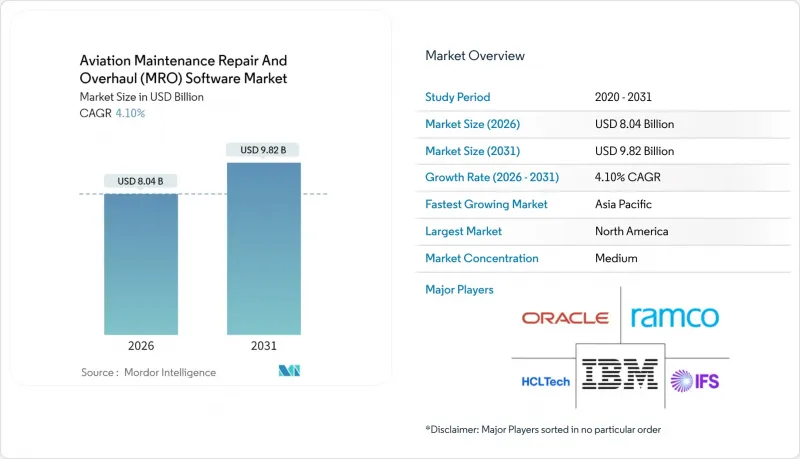

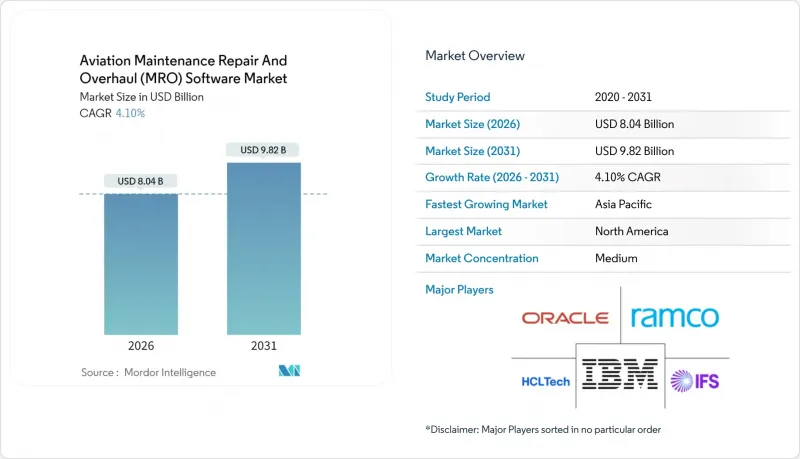

항공 정비·수리·점검(MRO) 소프트웨어 시장은 2025년 77억 2,000만 달러에서 2026년에는 80억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 4.10%로 추이하며, 2031년까지 98억 2,000만 달러에 달할 것으로 예측됩니다.

단기적인 성장 요인으로는 항공사의 클라우드 플랫폼으로의 전환, 노동집약적 업무의 자동화 압력 증가, 예측 분석과 정비, 재고, 컴플라이언스 업무 흐름의 통합 요구 등을 들 수 있습니다. 팬데믹 이후 중정비 수요 급증, 신흥 지역의 지속적인 기체 현대화, 종이 없는 기록 관리 의무화의 급속한 확산이 수요를 견인하고 있습니다. 클라우드 네이티브 신규 진출기업이 빠른 제품 주기로 기존 기업에게 도전장을 내밀면서 경쟁은 더욱 치열해지고 있습니다. 반면 기존 벤더들은 계획, 건강 모니터링, 공급망 모듈을 통합 생태계로 묶는 인수합병에 대응하고 있습니다. 실시간 데이터 시각화, AI 기반 부품 상태 예측, 원활한 규제 보고를 제공할 수 있는 벤더는 운항사가 예기치 않은 다운타임을 줄이고 기술자 리소스의 효율성을 높이기 위해 서두르고 있는 상황에서 분명한 이점을 누릴 수 있습니다.

항공 MRO 소프트웨어 시장에서 저비용항공사(LCC)는 높은 초기 라이선스 비용을 없애고 신속한 장비 확장을 지원하는 구독형 MRO 제품군을 점점 더 선호하고 있습니다. 클라우드 제공은 IT 유지보수 비용을 절감하고, 기능 업데이트를 즉각적으로 가능하게 함으로써 신뢰성을 훼손하지 않으면서도 얇은 이윤의 운영을 유지할 수 있게 해줍니다. SaaS 보급률이 증가함에 따라 공급업체와 서드파티 수리공장은 클라우드 중심의 워크플로우에 대응하기 위해 자체 포털과 API를 통합하고 마이그레이션 주기를 강화하고 있습니다. 지역 규제 당국은 현재 안전한 원격 데이터 저장을 승인하고 있으며, 아시아태평양과 유럽에서 클라우드 배포을 지연시켰던 법적 장벽이 사라졌습니다. 데이터 주권 관리를 인증하고 저장시 암호화를 증명할 수 있는 업체는 LCC 입찰에서 우선적으로 선정되고 있습니다.

항공기, 엔진, 환경 데이터를 실시간으로 분석하여 부품 고장을 몇 주 전에 예측하는 알고리즘을 구축하여 항공기 정비 소프트웨어 시장에서 항공사는 계획된 지상 대기 시간 동안 작업 범위를 예약할 수 있게 되었습니다. 데이터 모델이 성숙함에 따라 항공사는 지연 시간이 눈에 띄게 단축되고 가동 수명이 연장되었다고 보고하고 있습니다. 공급자는 AI 모듈을 내장하고 새로운 센서 데이터로 지속적으로 재학습을 시켜 고객은 별도의 데이터 사이언스 투자 없이도 적응형 인사이트를 얻을 수 있습니다. OEM이 보다 상세한 서브시스템 텔레메트리를 공개함에 따라 소프트웨어 업체들은 이러한 데이터를 과거 정비 기록과 중첩하여 열화 곡선을 정교화하고 부품 교체 일정을 최적화하고 있습니다. 비용 절감을 검증 가능한 사건 회피로 연결하는 능력은 Tier 1 항공사의 최우선 구매 기준이 되고 있습니다.

항공 MRO 소프트웨어 시장에서의 디지털 구축에는 항공 규정, SQL 기반 데이터 구조, API 오케스트레이션에 정통한 기술자가 필요합니다. 퇴직자가 신규 인증자보다 많은 상황이 임금 상승 압력을 높이고, 도입 일정이 장기화되고 있습니다. 벤더들은 이를 완화하기 위해 노코드 설정 툴을 패키지화하여 부족한 기술을 보완하는 매니지드 서비스 계층을 제공합니다.

2025년 기준, On-Premise 도입은 항공 MRO 소프트웨어 시장 점유율의 72.85%를 차지할 것으로 예측됩니다. 이는 엄격한 데이터 주권 규정을 충족하는 로컬 호스팅 솔루션에 대한 수년간의 투자가 반영된 결과입니다. 그러나 항공 MRO 소프트웨어 시장은 분명한 전환기를 맞이하고 있습니다. 클라우드 배포이 CAGR 5.98%로 성장을 지속하고, 있으며, 이는 현금 지출을 실제 사용량에 연동하는 구독 가격 체계와 AI 모듈에 대한 빠른 접근성이 지원되고 있습니다. 관리형 클라우드로 전환한 항공사는 5년간 총소유비용을 25-30% 절감하고, 버전업시 다운타임을 단축했다고 보고하고 있습니다. 보안은 과거에는 장벽이었지만, 현재는 대부분의 주요 소프트웨어 제품군이 SOC 2 Type II 및 ISO 27001 인증을 획득하여 규제 당국의 승인을 쉽게 받을 수 있게 되었습니다. 레거시 하드웨어의 갱신 시기가 도래하는 가운데, 예산 제약이 있는 사업자들은 분기별 기능 제공이 가능한 멀티테넌트형 SaaS 계약으로 서버 갱신을 대체하는 사례가 증가하고 있습니다.

공급자는 물리적 데이터 거주를 의무화하는 관할권을 위해 단일 테넌트 버전을 제공하고, 운항 관리, 재무, 승무원 순환 시스템과 원활하게 연동되는 REST API를 공개하여 차별화를 꾀하고 있습니다. 이러한 아키텍처의 개방성을 통해 항공사는 정비 정보를 광범위한 운영 관리 시스템에 통합할 수 있으며, 클라우드 배포의 이점을 더욱 확대할 수 있습니다. 실증사례가 늘어남에 따라 한때 자체 데이터센터를 추진하던 대형 플래그 캐리어조차도 적어도 비실시간 모듈의 단계적 전환을 계획하고 있으며, 항공 MRO 소프트웨어 시장의 전환점을 보여주고 있습니다.

2025년 매출의 58.02%는 MRO 서비스 기업이 차지했습니다. 이는 여러 항공사의 다양한 업무량을 처리하기 위해서는 고객에 의존하지 않는 종합적인 툴 세트가 필수적이기 때문입니다. 그러나 항공사가 슬롯 가용성 및 신뢰성 성과를 확보하기 위해 중정비 수직 통합을 추진함에 따라 항공사의 항공 MRO 소프트웨어 시장 규모는 4.62%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있습니다. 아시아 및 유럽 풀서비스 항공사의 자체 행거 확장은 엔지니어링, 자재, 재무 워크플로우를 통합하는 계획 엔진에 의존하고 있습니다. 항공사는 또한 항공기의 내공성 지침 추적과 예측 건강 대시보드를 통합하여 임무에 특화된 자산 배치를 지원하는 플랫폼을 요구하고 있습니다.

이에 대해 서드파티샵은 항공사에 실시간 마일스톤 가시성을 제공하는 고객 포털 기능을 도입하여 대응하고 있습니다. 그럼에도 불구하고 항공사는 부품 수명 분석에 대한 지적 재산을 보호하기 위해 자체 라이선스에 대한 투자를 계속하고 있습니다. OEM은 안정적인 구매자로 남아 있지만, 보증 관리 기능이 단독 시스템이 아닌 광범위한 제품군 내의 또 다른 모듈이 됨에 따라 그 점유율은 약간 감소하고 있습니다. 전체 사용자 그룹에서 외부 컨설턴트에 의존하지 않고 데이터 사이언스 기능을 활용할 수 있는 디지털 리터러시 엔지니어 채용 경쟁이 치열해지면서 항공 MRO 소프트웨어 시장의 서비스 수요 증가 추세를 견인하고 있습니다.

북미는 대규모 도입 기종군, 엄격한 FAA 문서화 규정, 풍부한 정비 기술자 층으로 인해 2025년에도 45.25%의 매출 점유율을 유지했습니다. 성숙한 항공사는 건강 모니터링 대시보드를 기존 기간 업무 시스템에 통합하고, 드롭인 연결 기능을 갖춘 벤더에게 수익성 높은 업그레이드 주기를 제공합니다.

한편, 아시아태평양은 4.70%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있습니다. Narrow Body 기종의 주문 백로그가 납품으로 전환되면서 확장성 있는 정비 IT시스템이 요구되고 있기 때문입니다. 대표적인 사례로 에어인디아가 470여 대의 항공기에 클라우드 전용 AMOS 도입을 선택한 사례와 대한항공이 신인천 정비시설에 AI 기반 엔진 정비 관리 스위트를 도입한 사례를 들 수 있습니다.

유럽에서는 유럽항공안전청(EASA)의 디지털 기록 권장 사항과 자본 위험을 억제하기 위해 SaaS에 의존하는 이 지역의 활발한 LCC 부문이 안정적인 수요를 지원하고 있습니다. 중동 메가 캐리어는 허브 앤 스포크 방식으로 운항하며, 통합 공급망과 중정비 모듈을 도입하여 기체 가동률을 유지하고 있습니다. 남미 항공사는 거시 경제의 변동 속에서 보다 신중한 현대화를 추진하고 있지만, 리스 회사의 반환 조건을 충족시키기 위해 클라우드 기록을 우선시하고 있습니다. 향후에는 언어 팩의 현지화, 관할권별 내항성 규정 대응, 지역 데이터센터 설치를 실현하는 업체가 항공 MRO 소프트웨어 시장의 다음 물결에서 점유율을 차지하게 될 것입니다.

The aviation MRO software market is expected to grow from USD 7.72 billion in 2025 to USD 8.04 billion in 2026 and is forecast to reach USD 9.82 billion by 2031 at 4.10% CAGR over 2026-2031.

Near-term growth comes from airlines shifting to cloud-hosted platforms, mounting pressure to automate labor-intensive tasks, and the need to integrate predictive analytics with maintenance, inventory, and compliance workflows. A post-pandemic jump in heavy-maintenance events, ongoing fleet modernization in emerging regions, and the rapid spread of paperless record-keeping mandates reinforce demand. Competitive intensity has increased as cloud-native entrants challenge incumbents with faster product cycles. At the same time, established vendors respond through acquisitions that bundle planning, health-monitoring, and supply-chain modules into unified ecosystems. Vendors able to deliver real-time data visibility, AI-driven component health forecasts, and seamless regulatory reporting enjoy a clear advantage as operators race to cut unscheduled downtime and stretch technician resources.

Low-cost airlines increasingly favor subscription-based MRO suites in the aviation MRO software market that remove heavy upfront license fees and support rapid fleet expansion. Cloud delivery lowers IT maintenance overhead and permits instant feature updates, allowing carriers to sustain thin operating margins without compromising reliability. As SaaS penetration rises, suppliers and third-party repair shops integrate their portals and APIs to accommodate cloud-centric workflows, reinforcing the migration cycle. Regional regulators now accept secure remote data storage, eliminating the legal barrier that once slowed cloud rollouts in Asia-Pacific and Europe. Vendors that can certify data-sovereignty controls and prove encryption at rest gain priority in LCC tenders.

Real-time analysis of flight, engine, and environmental data feeds algorithms that forecast component failures weeks in advance, letting operators schedule work scopes during planned ground time in the aviation MRO software market. Airlines report material cuts in delay minutes and longer on-wing life as data models mature. Providers embed AI modules that continuously retrain on fresh sensor feeds, giving customers adaptive insight without separate data-science investments. As OEMs release deeper subsystem telemetry, software firms layer those feeds onto historical maintenance records to refine degradation curves and optimize part-replacement schedules. The ability to tie cost savings to verifiable event avoidance is becoming the top buying criterion for tier-one carriers.

Digital rollouts in the aviation MRO software market require technicians versed in aviation regulation, SQL-based data structures, and API orchestration. Retirements outpace new certifications, lifting wage pressure and elongating implementation timelines. Vendors package more no-code configuration tools to mitigate and offer managed-service tiers that backfill scarce skills.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

On-premises installations held 72.85% of the aviation MRO software market share in 2025, reflecting years of investment in locally hosted solutions that satisfy strict data-sovereignty rules. Yet the aviation MRO software market is witnessing an unmistakable pivot as cloud deployments post a 5.98% CAGR, underpinned by subscription pricing that aligns cash outflows with usage and the promise of faster access to AI modules. Airlines migrating to managed clouds report 25-30% lower five-year total cost of ownership and downtime reductions during version upgrades. Security once posed a deterrent, but SOC 2 Type II and ISO 27001 certifications now cover most leading suites, easing regulator sign-off. As legacy hardware refresh cycles come due, budget-constrained operators increasingly swap server renewals for multi-tenant SaaS contracts that deliver quarterly feature drops.

Providers differentiate by offering single-tenant variants for jurisdictions mandating physical data residence and by exposing REST APIs that integrate seamlessly with flight operations, finance, and crew rostering systems. This architectural openness helps airlines weave maintenance insights into broader operational control towers, amplifying cloud adoption benefits. As proof points multiply, even large flag carriers that once championed internal data centers have scoped phased migrations of at least non-real-time modules, signaling a tipping point for the aviation MRO software market.

MRO service companies accounted for 58.02% of 2025 revenue because multi-airline workload diversity necessitates comprehensive, customer-agnostic toolsets. However, the aviation MRO software market size attributable to airlines is expanding swiftly at a 4.62% CAGR as carriers verticalize heavy checks to regain control over slot availability and reliability outcomes. Internal hangar expansions at full-service airlines in Asia and Europe rely on integrated planning engines to harmonize engineering, materials, and finance workflows. Airlines also demand platforms that blend airworthiness-directive tracking with predictive health dashboards to support mission-specific asset deployment.

Third-party shops respond by adopting customer portal functions that give airlines real-time milestone visibility. Still, airlines continue investing in in-house licenses to safeguard intellectual property around component-life analytics. OEMs remain steady buyers, yet their share slips marginally as warranty-management functions become another module inside broader suites rather than standalone systems. Across user groups, the race is on to hire digitally fluent engineers who can exploit data-science features without external consultants, reinforcing the services' upswing in the aviation MRO software market.

The Aviation MRO Software Market Report is Segmented by Deployment (Cloud-Based, and On-Premises), End User (Airlines, Mros, and OEMs), Function (Maintenance Management, Operations and Line Control, Inventory and Supply Chain, and Predictive Analytics and Health Monitoring), Solution (Software and Services), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 45.25% revenue share during 2025 due to a large installed fleet, strict FAA documentation rules, and deep maintenance-technician pools. Mature carriers embed health-monitoring dashboards into legacy enterprise resource-planning stacks, spawning lucrative upgrade cycles for vendors equipped with drop-in connectors.

In contrast, Asia-Pacific is racing ahead at 4.70% CAGR as order backlogs for narrow-body jets convert into deliveries requiring scalable maintenance IT. Flagship examples include Air India choosing a cloud-only AMOS deployment across more than 470 aircraft, and Korean Air contracting an AI-enabled engine-MRO suite for its new Incheon complex.

Europe posts steady demand driven by EASA's encouragement of digital records and the region's active low-cost sector, which leans on SaaS to limit capital exposure. Middle-East mega-carriers, operating hub-and-spoke models, deploy integrated supply chains and heavy-check modules to maintain fleet utilization. South American operators modernize more cautiously amid macroeconomic volatility but prioritize cloud records to satisfy lessor redelivery terms. In the future, vendors that localize language packs, adjust for jurisdiction-specific airworthiness rules, and stand up regional data centers will capture the next wave of the aviation MRO software market share.