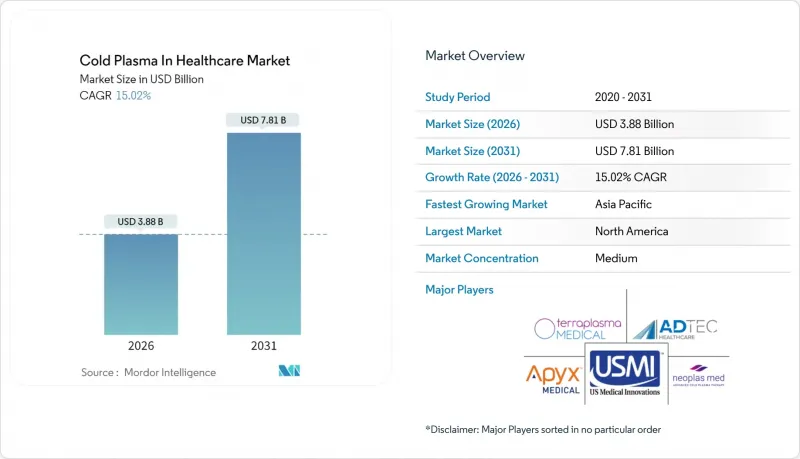

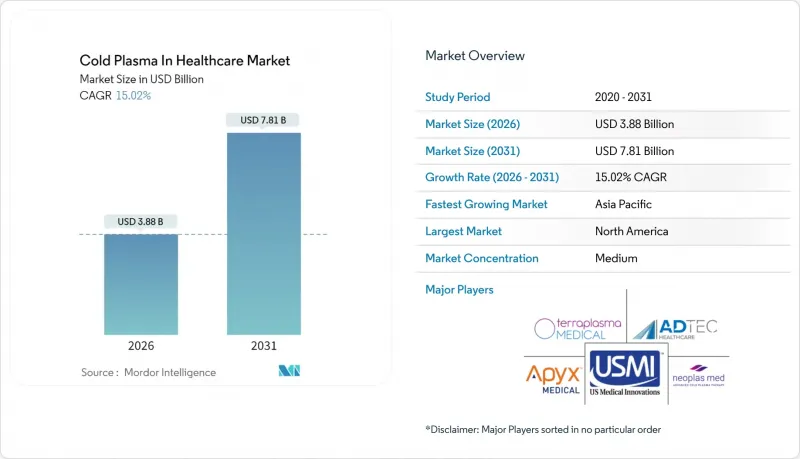

헬스케어용 저온 플라즈마 시장 규모는 2026년에 38억 8,000만 달러로 추정되고 있으며, 2025년 33억 7,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 78억 1,000만 달러에 달하며, 2026-2031년에 CAGR 15.02%로 확대할 것으로 전망되고 있습니다.

현재 이 기술이 확장된 것은 상온에서 독성 잔류물 없이 멸균, 치유, 절제할 수 있는 능력에 기인합니다. 이러한 성능적 우위는 지속가능성을 추구하는 병원들이 중요하게 여기는 부분입니다. 지불 기관들은 빠른 상처 봉합과 감염 감소로 인한 다운스트림 비용 절감 효과를 인식하기 시작했으며, 유리한 상환 프레임워크가 도입될 가능성을 시사하고 있습니다. 2024-2025년 사이 신속한 FDA 승인과 태국 및 베트남에서의 병행 승인으로 제품화 주기를 단축하고 임상적 안전성을 입증했습니다. 현재 대부분의 장비 제조업체는 플라즈마 발생기와 일회용 어플리케이터를 세트로 판매하고 있으며, 이 모델을 통해 자본 비용을 적절히 억제하면서 지속적인 매출을 창출하고 있습니다.

병원에서는 플라즈마 멸균기 도입이 증가하고 있습니다. 그 이유는 에틸렌옥사이드 잔류물을 제거하여 화학 폐기물을 최대 90%까지 줄일 수 있을 뿐만 아니라, 넷 제로 목표에 부합하기 때문입니다. 플라즈마 시스템은 주변 공기 또는 불활성 가스에서 활성산소 및 질소 종을 생성하지만, 처리 후 무해한 분자로 환원되어 시설에서 유해 폐기물 처리 비용을 절감할 수 있습니다. 유럽연합의 의료기기 규정은 환경영향 공개를 의무화하고 있으며, 이는 플라즈마 제조업체들에게 규제 측면의 호재로 작용하고 있습니다. 장비 공급업체는 증기 멸균기 대비 총 탄소발자국을 35% 감소시킨다는 수명주기 평가를 강조하고 있습니다. 독일과 네덜란드의 조달팀은 입찰 평가에 '환경 고려 점수'를 추가하고 있으며, 이러한 정책 전환은 헬스케어 저온 플라즈마 시장에 직접적인 이익을 가져다주고 있습니다.

메타 분석에 따르면 플라즈마 보조 요법은 표준 드레싱에 비해 상처 봉합을 210% 가속화하고, 치료군의 항생제 사용률을 23%에서 4%로 감소시키는 것으로 나타났습니다. 이러한 성과는 당뇨병성 궤양 1건당 약 3,800달러의 총 치료비 절감 효과를 가져왔으며, 이 수치는 지불자에게 설득력 있는 수치로 작용했습니다. 미국, 일본, 스페인에서 진행된 다기관 임상시험을 통해 궤양의 병인에 관계없이 일관된 유효성을 확인했습니다. 주요 상처 치료 체인은 플라즈마 치료를 주간 치료 프로토콜에 통합하여 장비 사용률을 높이고 있습니다. 외래 진료 모델에서는 한 대의 발생기로 하루 20-30명의 환자를 치료할 수 있으므로 헬스케어 분야 저온 플라즈마 시장은 즉각적인 매출 증가를 기록하고 있습니다.

많은 의사들이 플라즈마 의료에 대한 공식적인 교육을 받지 못했고, 이러한 지식 부족이 프로토콜 도입의 지연 요인으로 작용하고 있습니다. 2025년 조사에 따르면 상처 치료 전문의의 38%만이 플라즈마의 작용기전을 설명할 수 있다고 답했습니다. 제조업체들이 워크숍을 개최하고 있지만, 참가자가 초기 도입자에 편중되어 있으며, 주류 의사들의 확신을 얻지 못하고 있습니다. 학회는 커리큘럼 모듈을 만들고 있지만, 의과대학에 통합하는 데는 2-3년이 걸립니다. 이러한 지식의 부족은 헬스케어 분야에서의 저온 플라즈마 시장의 즉각적인 보급을 억제하고 있습니다.

플라즈마 제트 장비는 2025년 헬스케어 저온 플라즈마 시장의 41.94%를 차지하며 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 10년간의 임상 실적과 상대적으로 낮은 단가가 기여하고 있습니다. 병원에서는 주로 만성 상처 치료에 도입되며, 주변 피부를 보호하기 위해 정밀한 스팟 조사가 중요합니다. 본 장치는 유전체 장벽을 이용하여 에너지 종을 집중시키고, 치료 범위를 시각적으로 제어할 수 있도록 합니다. 현재 전 세계 3,000개 이상의 병원 치료실에는 카트 기반 제트 시스템이 상시 대기 상태로 설치되어 있으며, 이러한 설치 기반은 일회용 칩 주문을 촉진하고 의료용 저온 플라즈마 시장의 지속적인 매출을 주도하고 있습니다.

RF 구동 장치는 외과 의사가 전력, 주파수, 듀티 사이클을 실시간으로 조정할 수 있는 디지털 파형 제어를 통해 17.02%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 보이고 있습니다. 초기 모델은 실린더에 담긴 헬륨이 필요했으나, 차세대 유닛은 아르곤 또는 대기 중 공기를 사용할 수 있으며, 소모품 비용을 40% 절감할 수 있습니다. 이러한 경제적 이점은 많은 지역에서 치료비는 보험 적용 대상이지만 특수 가스는 보험 적용 대상에서 제외되는 상환 코드 체계에서 중요한 의미를 갖습니다. 공급업체는 설정값과 치료 결과를 기록하는 클라우드 대시보드를 번들로 제공하고 있으며, 감염관리위원회에서 환영하는 기능입니다. 종합적으로, RF 기술의 발전은 제품 구성의 부가가치 향상을 약속하며, 헬스케어 저온 플라즈마 시장의 성장 모멘텀을 강화할 것입니다.

상처 치유 분야는 2025년 기준 헬스케어 분야 저온 플라즈마 시장의 34.12%를 차지할 것으로 예상되며, 이는 육아 형성 촉진 및 세균 부하 감소에 대한 확실한 증거를 반영합니다. 표준 프로토콜에서는 주 3회 시술이 이루어지며, 이 빈도는 외래 진료 일정과 일치하여 발생장치의 가동률을 극대화합니다. 독일과 일본의 보험사들은 현재 기존 상처 치료 코드에 따라 플라즈마 드레싱에 대한 보험금을 지급하고 있으며, 의료진의 경제적 부담을 덜어주고 있습니다. 인구 고령화와 당뇨병 발병률 증가로 인해 만성 상처 환자층이 확대되고 있으며, 헬스케어 분야 저온 플라즈마 시장의 모든 지역 계층에서 지속적인 수요가 발생하고 있습니다.

외과 종양학 분야는 16.9%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 플라즈마 절제술은 미세한 종양 부위를 비활성화시키면서 건강한 여백을 보존하기 위한 것입니다. 내시경 외과 의사들은 플라즈마가 탄화층을 남기지 않고 조직병리학적 판독을 개선하는 점을 높이 평가했습니다. 미국 대형 암센터의 초기 도입 시설에서 플라즈마가 단극소작술을 대체한 결과, 수술 후 배액관 삽입 기간이 12일 단축된 것으로 보고되고 있습니다. 이러한 기능적 이점은 특히 실제 임상 데이터가 축적됨에 따라 프로토콜에 대한 통합을 가속화하고 있습니다. 만성 상처와 종양학은 헬스케어 저온 플라즈마 시장의 응용 다양성과 매출의 지속성을 지원하는 두 개의 큰 축을 구성하고 있습니다.

북미는 2025년 41.25%의 매출 점유율로 헬스케어 저온 플라즈마 시장을 주도할 것으로 예상되며, 임상적 정당성을 확립하는 FDA 승인을 배경으로 성장하고 있습니다. 상처관리에 대한 안정적인 상환제도가 보급을 가속화하고, 통합의료 네트워크는 여러 기관에서 프로토콜 표준화를 위해 여러 대 단위로 주문하고 있습니다. 조지 워싱턴 대학의 플라즈마 센터로 대표되는 산학협력을 통해 근거 기반 구매를 지원하는 연구자 주도 임상시험의 안정적인 파이프라인이 형성되고 있습니다.

아시아태평양은 16.18%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 태국, 베트남, 싱가포르에서는 의료기기 승인이 효율화되고 있습니다. 이들 국가의 보건부는 증가하는 공중 보건 부담인 당뇨병성 궤양에 대한 비용 효율적인 솔루션으로 플라즈마를 포지셔닝하고 있습니다. MIRARI와 같은 휴대용 시스템은 유럽과 미국에 앞서 이들 시장에 진출하여 유연한 규제가 도입 주기를 단축할 수 있다는 것을 입증했습니다. 지역 유통업체들은 서비스 계약과 임상 교육을 패키지로 묶어 의료 종사자들의 부족한 인지도를 보완하면서 헬스케어 저온 플라즈마 시장 확대를 도모하고 있습니다.

유럽은 성숙하면서도 기회가 풍부한 시장입니다. 의료기기 규정(MDR)에 따른 신청 서류 준비 기간이 길어짐에 따라 인증 취득 후 최종사용자 신뢰도 향상에도 기여합니다. 독일 병원에서는 조달 예산을 환경 목표와 연동하여 조달하고 있으며, 이는 플라즈마의 친환경성이 평가받는 배경이 되고 있습니다. 남유럽 보건당국은 약제 내성 위기에 직면하여 플라즈마의 감염 제어 가능성을 검증하는 파일럿 프로그램을 진행 중입니다. 다른 지역에서는 중동과 남미에서 상처 치료 현대화 계획에 따라 플라즈마에 대한 평가가 시작되고 있으며, 헬스케어 분야에서 저온 플라즈마 시장 점유율을 확대할 수 있는 기반이 마련되고 있습니다.

cold plasma in healthcare market size in 2026 is estimated at USD 3.88 billion, growing from 2025 value of USD 3.37 billion with 2031 projections showing USD 7.81 billion, growing at 15.02% CAGR over 2026-2031.

Current expansion stems from the technology's ability to sterilize, heal, and ablate at room temperature without toxic residues, a performance edge that hospitals value as they pursue sustainability mandates. Payers are beginning to recognize downstream savings from faster wound closure and fewer infections, signaling that favorable reimbursement frameworks are likely to follow. Rapid FDA clearances in 2024-2025, combined with parallel approvals in Thailand and Vietnam, shorten commercialization cycles and validate clinical safety. Most device makers now bundle plasma generators with single-use applicators, a model that keeps capital costs moderate while driving recurring revenue.

Hospitals increasingly adopt plasma sterilizers because they eliminate ethylene oxide residues, lower chemical waste by up to 90%, and align with net-zero targets. Plasma systems generate reactive oxygen and nitrogen species from ambient air or inert gases that revert to harmless molecules after treatment, so facilities avoid hazardous-waste fees. The European Union's Medical Device Regulation now requires environmental impact disclosures, giving plasma makers a regulatory tailwind. Device vendors highlight life-cycle assessments that show a 35% reduction in total carbon footprint versus steam sterilizers. Procurement teams in Germany and the Netherlands are adding "green points" to tender evaluations, a policy shift that directly benefits the Cold plasma in healthcare market.

Meta-analyses report 210% faster wound closure with plasma adjunct therapy relative to standard dressings, while antibiotic use falls from 23% to 4% in treated cohorts. Those outcomes lower overall treatment cost per diabetic ulcer episode by nearly USD 3,800, a figure that resonates with payers. Multicenter trials across the United States, Japan, and Spain confirm consistent efficacy regardless of ulcer etiology. Leading wound-care chains now embed plasma sessions into weekly care protocols, boosting device utilization rates. The Cold plasma in healthcare market registers immediate revenue gains because one generator can treat 20-30 patients per day under outpatient scheduling models.

Physicians often lack formal training in plasma medicine, a gap that slows protocol adoption. Surveys in 2025 show only 38% of wound-care specialists can describe plasma's mechanism of action. Manufacturers host workshops, yet attendance skews toward early adopters, leaving the mainstream unconvinced. Academic societies are drafting curriculum modules, but integration into medical schools will take two to three years. This knowledge deficit tempers immediate uptake in the Cold plasma in healthcare market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plasma Jet Devices represent the largest slice of the cold plasma in healthcare market at 41.94% in 2025, benefiting from a decade of clinical familiarity and relatively low unit cost. Hospitals deploy them chiefly for chronic wounds where fine-point application is critical to spare periwound skin. The devices use dielectric barriers to focus energetic species, granting operators visible control over treatment contours. Over 3,000 hospital treatment rooms worldwide now keep a jet system on cart-based standby, an installed base that reinforces ordering of single-use tips and drives recurring revenue inside the Cold plasma in healthcare market.

RF-Powered Devices deliver the fastest expansion at a 17.02% CAGR, propelled by digital waveform control that lets surgeons tune power, frequency, and duty cycle in real time. Early models required bottled helium, but next-generation units accept argon or ambient air, cutting consumable cost by 40%. This economic edge matters because reimbursement codes in many regions cover therapy but not specialty gas. Suppliers bundle cloud dashboards that log settings and outcomes, a feature welcomed by infection-control committees. Altogether, RF upgrades promise to shift product-mix value upward, reinforcing growth momentum in the Cold plasma in healthcare market.

Wound Healing holds 34.12% of the cold plasma in healthcare market share as of 2025, reflecting robust evidence of accelerated granulation and bacterial load reduction. Typical protocols administer three sessions per week, a cadence that dovetails with outpatient clinic schedules and maximizes generator utilization. Insurers in Germany and Japan now reimburse plasma dressings under existing wound-care codes, reducing financial friction for providers. The aging demographic and rising diabetes incidence enlarge the chronic-wound cohort, sustaining baseline demand across every geographic tier of the cold plasma in healthcare market.

Surgical Oncology grows at 16.9% CAGR because plasma ablation spares healthy margins while inactivating microscopic tumor nests. Endoscopic surgeons appreciate that plasma leaves no char layer, improving histopathology reads. Early adopters at large U.S. cancer centers reported a 12-day reduction in postoperative drain duration when plasma replaced monopolar cautery. These functional benefits accelerate protocol inclusion, especially as real-world data accumulate. Together, chronic wounds and oncology compose dual pillars that underpin application diversity and revenue resilience in the Cold plasma in healthcare market.

The Cold Plasma in Healthcare Market Report is Segmented by Product Type (Plasma Jet Devices, and More), Application (Wound Healing, and More), End User (Hospitals, and More), Plasma Gas Type (Helium, Argon, Air/Oxygen Mix, Other Plasma Gas Types), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America leads the cold plasma in healthcare market with 41.25% revenue share in 2025, riding on FDA clearances that establish clinical legitimacy. Stable reimbursement for wound management accelerates uptake, and integrated delivery networks place multi-unit orders to standardize protocols across campuses. Academic-industry collaborations, exemplified by George Washington University's plasma center, produce a steady pipeline of investigator-sponsored trials that underpin evidence-based purchasing.

Asia-Pacific advances at a 16.18% CAGR as Thailand, Vietnam, and Singapore streamline device approvals. Ministries of health in those countries view plasma as a cost-effective solution for diabetic ulcers, a growing public-health burden. Handheld systems like MIRARI entered these markets ahead of Western rollouts, proving that agile regulation can shorten adoption cycles. Regional distributors bundle service contracts and clinical training, tactics that counteract limited practitioner awareness and expand the cold plasma in healthcare market.

Europe occupies a mature yet opportunity-rich position. While MDR demands lengthen dossier preparation, they also heighten end-user confidence once certificates are issued. Hospitals in Germany link procurement budgets to environmental goals, a context that plays to plasma's green strengths. Southern European health authorities, facing antibiotic resistance crises, run pilot programs to validate plasma's infection-control potential. Elsewhere, the Middle East and South America begin to evaluate plasma under wound-care modernization schemes, setting the stage for incremental share gains inside the cold plasma in healthcare market.