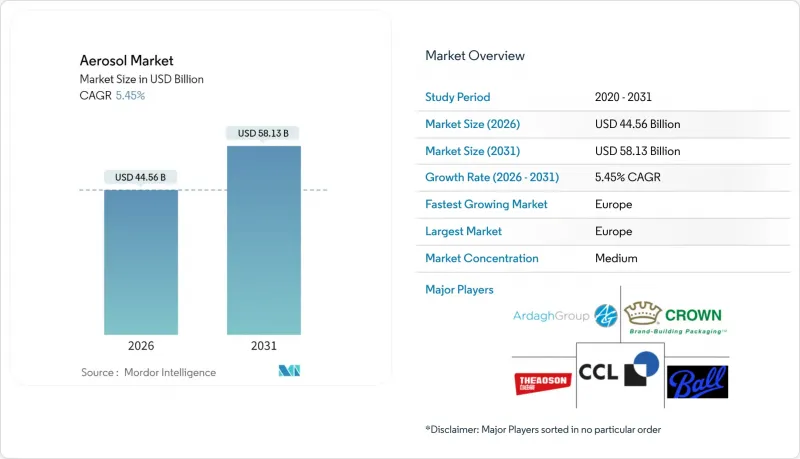

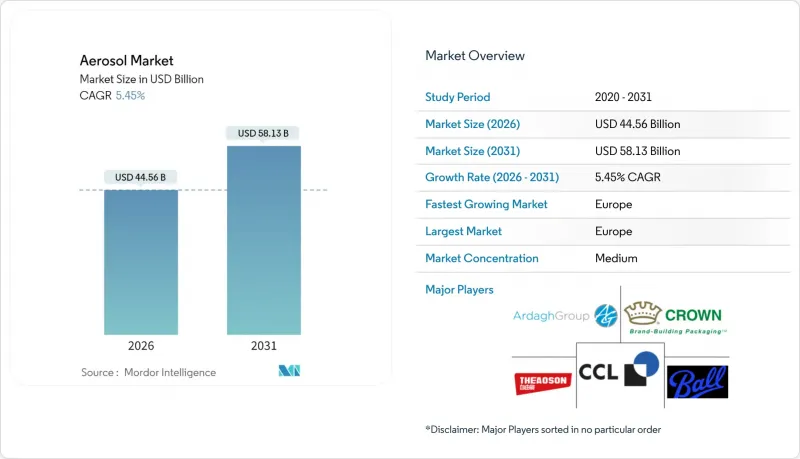

에어로졸 시장은 2025년에 422억 6,000만 달러로 평가되며, 2026년 445억 6,000만 달러에서 2031년까지 581억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 5.45%로 예상됩니다.

이러한 꾸준한 성장은 퍼스널케어, 의료, 산업 분야에서 편리하고 가압된 디스펜싱을 선호하는 소비자의 선호에 기인합니다. 특히 유럽의 프레온 규제에 대한 조기 준수는 하이드로플루오로카본(HFC)에서 하이드로플루오로올레핀(HFO)으로의 전환을 가속화하고 있습니다. 유럽의 규제 주도가 세계 제품 디자인을 형성하는 한편, E-Commerce 및 소비자 직접 판매 채널이 제품 보급 범위를 확대하여 경량 및 재활용 가능한 캔에 대한 수요를 강화하고 있습니다. 알루미늄 가격 변동이 지속되는 가운데 저탄소 포장의 추구는 재료 공급업체 간의 경쟁을 심화시키고 있지만, 재활용 소재 사용과 보편적 폐기물 프로그램 대응을 통한 제품 차별화의 기회도 창출하고 있습니다.

미용 및 그루밍 분야의 프리미엄화가 가압식 용기의 보급을 촉진하고 있습니다. 가압식 용기는 정확한 용량, 위생적인 사용감, 장기 보관성을 제공합니다. 인도 스킨케어 시장에서는 SPF 함유 스프레이와 하이브리드 모이스처라이저의 인기를 바탕으로 성장세를 보이고 있습니다. 전 세계 브랜드 소유주들은 편의성을 유지하면서 VOC 규제에 대응하기 위해 리필용 금속캔과 에어리스 시스템에 대한 혁신 파이프라인을 강화하고 있습니다. 저 VOC 드라이 샴푸의 특허 출원은 주요 기업이 배출 규제 준수와 두피 친화적인 포뮬러를 모두 우선시하고 있음을 보여줍니다. 유럽 제조업체들은 에어로졸이 내용물을 산화 및 오염으로부터 보호하는 능력을 강조하여 브랜드 가치를 높이고 있습니다. 종합적 효과: 프리미엄 가격의 탄력성이 추진제 재제형 비용을 상쇄하여 에어로졸 시장의 성장을 지속하고 있습니다.

산업용 사용자는 정전기 스프레이 기술을 채택하여 오버 스프레이를 최대 30%까지 줄일 수 있습니다. 이를 통해 광범위한 도장에서의 재료 효율이 향상되었습니다. 동남아시아의 인프라 붐(인도네시아의 페인트 수요는 2024년 100만톤 돌파)은 철강, 콘크리트, 복합재 표면 보호용 에어로졸 수요 증가를 지원하고 있습니다. 자동차 수리 분야에서는 색상의 유연성을 갖춘 터치업 에어로졸을 선호하고 있습니다. 보다 엄격한 VOC 상한치를 준수하는 수성 배합제에서도 분무 상태를 유지하는 추진제가 여전히 필요하며, 디메틸에테르와 같은 대체 추진제의 채택을 촉진하고 있습니다. 현재 농업용 드론은 좁은 열 사이에 농약을 균일하게 살포하기 위해 에어로졸 대응 배합제에 의존하고 있으며, 추진제 공급업체에게 새로운 수입원을 개발하고 있습니다. ISO 14001 표준을 준수하여 환경 친화적인 용제 및 첨가제 조달을 주도하고 있습니다.

휘발성 유기화합물에 대한 지역별로 상이한 규제 값으로 인해 지역 특화형 처방이 필요하고, 인증 비용이 두 배로 증가하고 있습니다. 국내에서 시험한 소비자용 탈취제는 1미터 거리에서 총 VOC 13.89 ppm을 방출하고, 특정 벤젠 농도가 ACGIH 제안 기준치를 초과하여 향료를 많이 사용한 에어로졸 제품의 규제 적합성 문제가 대두되고 있습니다. 유럽연합의 CFC 할당량 경매로 인해 GWP가 높은 혼합가스의 가격이 상승하고, 소규모 브랜드도 청정 화학물질을 채택해야 하는 상황에 처해 있습니다. 에어라벨 점수 기준에 따라 저 실내 배출량 증명이 의무화되어 새로운 SKU 시장 출시 기간이 연장되고 있습니다. 구식 추진제 관련 재고는 단계적 폐지 일정이 앞당겨질 경우 평가손실 위험이 있습니다. 전 세계 유통업체들은 복잡한 규칙을 통과해야 하고, 다국적 진출에 따른 물류비용이 증가하고 있습니다.

2025년 에어로졸 분야에서 하이드로플루오로카본(HFC) 시장 점유율은 40.62%를 차지했습니다. 이는 잘 구축된 공급망과 폭넓은 배합 호환성에 의해 지원됩니다. 그러나 단계적 감축 할당량 강화로 인해 고객들은 하이드로플루오로올레핀(HFO)으로 전환하고 있으며, HFO는 2031년까지 연평균 복합 성장률(CAGR) 6.58%를 나타낼 것으로 예측됩니다. 바이오메탄올 유래의 디메틸 에테르는 음의 탄소 강도 특성과 WHO의 의료용 승인으로 주목받고 있습니다. 아산화질소와 이산화탄소는 불연성이 필수인 식용 및 산업 분야에서 여전히 주류입니다. HFO 추진제를 이용한 의료기기 인증을 조기에 완료한 기업은 프리미엄 가격과 장기 계약 기간의 혜택을 받고 있습니다.

지역별로 채택률이 다르며, 유럽은 초기 프레온 규제 시행으로 인해 앞서가고 있습니다. 한편, 북미에서는 주정부 차원의 규제로 인해 전환이 가속화되고 있습니다. 아시아태평양에서는 대형 다국적 퍼스널케어 기업이 세계 배합 기준을 따르는 반면, 로컬 브랜드들은 단계적으로 대체품을 도입하고 있습니다. 추진제와 지속가능성 인증을 함께 제공할 수 있는 공급업체는 안정적인 수요를 확보할 수 있습니다. HFO 생산능력에 대한 투자는 장기적인 공급 리스크를 줄이고, 다운스트림 충전업체들의 비용 구조를 안정화시킬 수 있습니다.

유럽은 2025년 세계 에어로졸 시장의 32.12%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 6.41%로 확대될 것으로 예측됩니다. 엄격한 프레온 규제와 탄탄한 재활용 인프라가 HFO 추진제와 저탄소 금속캔의 급속한 보급을 촉진하고 있습니다. 독일, 프랑스, 영국은 프리미엄 퍼스널케어 제품 및 산업용 배합 기술에 중점을 둔 R&D 투자를 주도하고 있습니다. 소매업체들은 오염물질이 없는 공급이라는 에어로졸 제품의 장점을 강조하는 에코 라벨이 부착된 제품을 홍보하고 있습니다. 빠른 규제 대응 일정으로 유럽 충전업체들은 해외에서 기술 라이선싱을 획득하고 신흥 시장에서 점유율을 확보할 수 있게 되었습니다.

아시아태평양은 인프라 구축의 진전과 재량지출 증가를 배경으로 가장 빠른 판매량 증가가 예상됩니다. 중국은 알루미늄 생산에서 우위를 점하고 있으며, 공급망에서 비용 우위를 확보하고 있습니다. 그러나 석탄을 많이 사용하는 제련 공정은 탄소발자국에 대한 우려를 불러일으키며 재활용 알루미늄에 대한 수요를 불러일으키고 있습니다. 인도의 경우, 확대되는 스킨케어 시장이 현지 충진 능력을 자극하고, 인도네시아는 100만 톤 규모의 페인트 산업이 산업용 스프레이 수요를 지원하고 있습니다. 일본과 한국은 정밀 밸브와 안전 인증을 중시하며 고성능 부품을 역내로 수출하고 있습니다.

북미는 성숙된 시장이지만 여전히 주요 기여 지역으로, 연간 약 40억 개의 에어로졸 캔 판매로 여전히 주요 기여 지역으로 남아 있습니다. 36개 주에서 채택된 보편적 폐기물 규제는 폐기 장벽을 낮추고, 문전수거 제도를 촉진하고 있습니다. E-Commerce의 확대로 콜드체인을 필요로 하지 않는 휴대용 식품 및 청소용 에어로졸 제품의 보급이 가속화되고 있습니다. 멕시코는 바이어스도르프의 3억 5,000만 유로 규모의 시라오 공장 확장 이후, 지역내 퍼스널케어 수요를 지원하는 전략적 수출 거점으로 부상하고 있습니다. 캐나다의 저 VOC 기준은 미국 규제와 병행하여 여러 국가에서의 제품 출시를 효율화하고 있습니다.

The Aerosol Market was valued at USD 42.26 billion in 2025 and estimated to grow from USD 44.56 billion in 2026 to reach USD 58.13 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031).

Steady gains stem from consumer preference for convenient, pressurized dispensing across personal care, medical, and industrial uses. Early compliance with evolving F-gas regulations, particularly in Europe, is accelerating the transition from hydrofluorocarbons (HFCs) to hydrofluoroolefins (HFOs). Europe's regulatory leadership is shaping global formulations, while e-commerce and direct-to-consumer channels are extending product reach and reinforcing demand for lightweight, recyclable cans. Ongoing aluminum price fluctuations and the pursuit of lower-carbon packaging intensify competition among material suppliers, yet they also create opportunities for product differentiation through recycled content and universal waste program coverage.

Premiumization in beauty and grooming drives the wider use of pressurized formats, which offer precise dosing, hygienic delivery, and longer product shelf life. India's skincare segment is experiencing growth, driven by the popularity of SPF-infused sprays and hybrid moisturizers. Global brand owners are bolstering innovation pipelines around refillable metal cans and airless systems to address VOC caps while retaining convenience credentials. Patent filings for low-VOC dry shampoo underscore how leading firms prioritize both emissions compliance and scalp-friendly formulations. European makers strengthen brand equity by spotlighting aerosols' ability to shield contents from oxidation and contamination. Collective effect: premium price elasticity offsets propellant reformulation costs and sustains aerosol market growth.

Industrial users adopt electrostatic spray technology to curb overspray by up to 30%, enhancing material efficiency in large-area coatings. Southeast Asian infrastructure booms-Indonesia's paint demand topped 1 million tons in 2024-support higher volumes for protective aerosols used on steel, concrete, and composite surfaces. Auto refinish segments favor touch-up aerosols for color-matching versatility. Water-based formulas compliant with stricter VOC ceilings still require propellants that maintain atomization, thereby driving the uptake of dimethyl ether and other alternatives. Agricultural drones now rely on aerosol-compatible formulations to spread pesticides evenly across narrow rows, opening new revenue streams for propellant suppliers. Compliance with ISO 14001 standards guides the procurement of eco-optimized solvents and additives.

Divergent limits on volatile organic compounds oblige region-specific formulations and double certification costs. Consumer deodorants tested in Korea emitted 13.89 ppm of total VOC at a 1-meter distance, with certain benzene levels exceeding proposed ACGIH limits, indicating compliance hurdles for fragrance-heavy aerosols. The European Union's F-gas quota auction elevates the price of high-GWP blends, compelling even small brands to adopt cleaner chemistries. Air Label Score criteria force proof of low indoor emissions, extending time-to-market for new SKUs. Inventory tied to legacy propellants risks write-downs if phaseout dates accelerate. Global distributors must navigate a patchwork of rules, which raises logistics overhead for multi-country rollouts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hydrofluorocarbons held a 40.62% market share in the aerosol sector in 2025, underpinned by well-established supply chains and broad formulation compatibility. Yet tightening phase-down quotas are steering customers toward hydrofluoro-olefins, which are projected to post a 6.58% CAGR through 2031. Dimethyl ether, produced from bio-methanol, is drawing attention for its negative carbon intensity profile and WHO endorsement for medical uses. Nitrous oxide and carbon dioxide still dominate edible and technical segments where non-flammability is mandatory. Early movers completing medical device validations with HFO propellants enjoy premium pricing and longer contract tenures.

Adoption rates vary by region, with Europe leading due to earlier F-gas restrictions, while North America accelerates the transition through state-level mandates. In the Asia-Pacific region, larger multinational personal care players follow global formulation standards, whereas local brands gradually phase in alternatives. Suppliers capable of offering bundled propellant plus sustainability certification packages capture loyal demand. Investments in HFO capacity mitigate long-term supply risk and stabilize cost structures for downstream fillers.

The Aerosol Market Report is Segmented by Propellant Type (Dimethyl Ether, Hydrofluorocarbons, Hydrofluoro Olefins, and Other Types), Can Type (Steel, Aluminum, Plastic, and Other Can Types), Application (Automotive, Personal Care, Food Products, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Europe accounted for 32.12% of the global aerosol market in 2025 and is forecast to grow at a 6.41% CAGR through 2031. Stringent F-gas legislation and robust recycling infrastructure are spurring the rapid uptake of HFO propellants and low-carbon metal cans. Germany, France, and the United Kingdom lead research and development investments focused on premium personal-care and industrial formulations. Retailers promote products bearing eco-labels that highlight the aerosols' benefits of contamination-free delivery. Earlier compliance timetables enable European fillers to license technology abroad and capture a share in emerging markets.

Asia-Pacific shows the fastest incremental volume gains, driven by infrastructure growth and rising discretionary spending. China's aluminum dominance secures supply-chain cost advantages, although coal-intensive smelting raises concerns about its carbon footprint, which stimulates demand for recycled aluminum. India's expanding skincare market stimulates local filling capacity, while Indonesia's one-million-ton paint sector buoys industrial sprays. Japan and South Korea emphasize precision valves and safety certifications, exporting high-performance components across the region.

North America remains a mature but sizable contributor, buoyed by almost 4 billion aerosol cans sold annually. Universal waste rules adopted by 36 states lower disposal barriers and promote curbside collection schemes. E-commerce accelerates adoption of portable food and cleaning aerosols that bypass cold chains. Mexico emerges as a strategic export platform after Beiersdorf's EUR 350 million Silao expansion, feeding regional personal-care demand. Canada's focus on low-VOC standards parallels U.S. regulations, streamlining multi-country product launches.