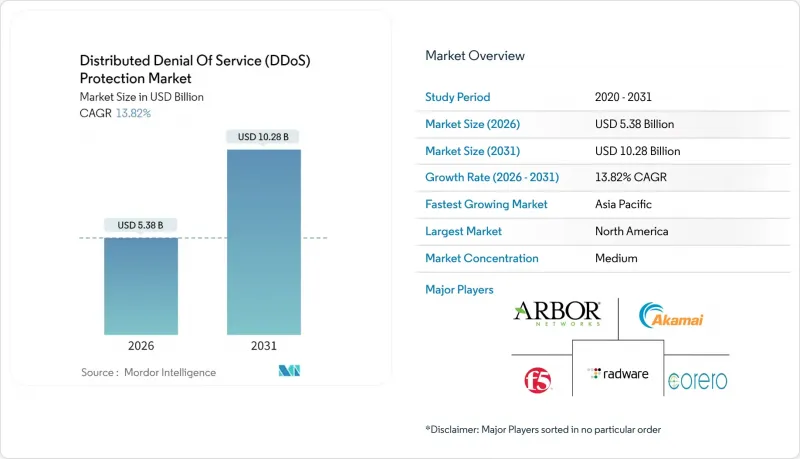

2026년 DDoS 대책 시장 규모는 53억 8,000만 달러로 추정되며, 2025년 47억 3,000만 달러에서 성장이 전망됩니다.

2031년에는 102억 8,000만 달러에 달하며, 2026-2031년에 CAGR 13.82%로 확대할 전망입니다.

이러한 확대는 멀티 벡터 테라비트 규모의 사고 빈도 증가, 강화된 규제 요건, 하이브리드 및 클라우드 기반 완화 모델의 확산에 의해 촉진되고 있습니다. 솔루션 중심 제품군은 2024년 61.23%의 점유율을 유지하며 통합된 프로그래머블 방어에 대한 기업 수요를 지원하고 있습니다. 클라우드 우선 구축이 대상 시장의 거의 절반을 차지했으나, 조직이 지연, 제어, 컴플라이언스의 균형을 맞추기 위해 하이브리드 아키텍처의 영향력이 확대되고 있습니다. 지역별 동향은 여전히 중요하며, 2024년 북미가 39.34%의 매출 점유율로 1위를 유지한 반면, 아시아태평양은 5G의 급속한 확산과 IoT 도입 급증에 힘입어 14.89%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다.

2025년 발생한 사상 최대 규모의 6.3Tbps 공격은 단순한 볼륨 공격에서 복잡한 프로토콜-용도 계층 공격으로의 전환을 보여주었습니다. 이에 따라 기존 규칙 기반 장비는 대응이 불가능해졌고, 적응형 AI 기반 플랫폼의 도입이 가속화되고 있습니다. 통신 서비스 프로바이더와 금융기관은 여전히 고가치 타겟이며, 각국 규제 당국은 중요 인프라 사업자에게 내결함성 증명을 의무화하고 있습니다.

단시간 집중 공격이 증가함에 따라 탄력적인 상시 가동형 클라우드 스크러빙은 필수 불가결한 요소로 자리 잡았습니다. 그러나 지연에 민감한 워크로드에서는 On-Premise 방어의 중요성이 유지되어 하이브리드 수요를 가속화하고 있습니다. 하이퍼스케일 클라우드와 보안 전문 기업과의 파트너십은 중소기업의 기술 격차를 해소하고 새로운 컴플라이언스 의무를 달성할 수 있도록 돕습니다.

자본 집약적인 하드웨어와 지속적인 시그니처 업데이트는 여전히 중소기업의 장벽으로 작용하고 있으며, 이는 구독형 클라우드 스크러빙과 관리형 SOC 서비스의 결합에 대한 수요를 촉진하고 있습니다.

2025년에는 L3/4의 볼륨형 플러드 공격부터 L7의 용도 악용까지 포괄하는 통합적이고 프로그램 가능한 방어를 원하는 기업이 증가하면서 솔루션 분야가 전체 매출의 60.65%를 차지할 것으로 예측됩니다. 이 분야에서는 네트워크 계층 보호가 가장 큰 점유율을 유지하고 있지만, 합법적인 사용자 행동을 모방하는 AI 기반 봇의 등장으로 지능형 봇 대응 분야는 15.05%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 각 벤더들은 머신러닝 분류기, 디바이스 핑거프린팅, 실시간 챌린지 메커니즘을 내장하여 크리덴셜 스터핑과 재고 축적 공격을 무력화시키고 있습니다. 서비스 관리형 및 전문 서비스는 컴플라이언스 보고 및 24시간 365일 모니터링을 위한 공급업체 통합이 진행됨에 따라 그 중요성이 계속 증가하고 있습니다. 솔루션과 서비스의 상호 작용은 DDoS 방어 시장 전체에서 성과 기반 계약 형태로의 전환을 강조하고 있습니다.

하이브리드 구성의 도입 확대에 따라 On-Premise 장비, 클라우드 스크러빙 센터, 컨테이너화 네트워크 기능 간의 연계가 요구되고 있습니다. 서비스 제공이 수렴되는 가운데, 차별화 요소는 API 중심의 통합성, 공격 포렌식의 깊이, 제로 트러스트 대응으로 옮겨가고 있습니다. 행동 분석과 실용적인 인텔리전스를 결합하는 벤더는 중요한 분야에서 입증 가능한 탄력성을 요구하는 규제 압력이 증가함에 따라 이를 활용할 수 있는 위치에 있습니다.

클라우드 기반 방어는 2025년 DDoS 방어 시장 규모의 49.02%를 차지할 것으로 예상되며, 탄력적인 대역폭 풀과 세계 애니캐스트 라우팅을 통해 수 Tbps 규모의 공격을 흡수할 수 있습니다. 상시 가동 모델은 몇 초 이내에 대응을 보장하며, 1분 미만의 '펄스' 공격이 빈번하게 발생하는 현재 상황에서 필수적입니다. 한편, 하이브리드 아키텍처는 2031년까지 연평균 복합 성장률(CAGR) 15.25%로 확대될 것으로 예측됩니다. 기업은 급증시 저지연 On-Premise 감지와 클라우드 규모의 스크러빙을 통합하기 위해 노력하고 있습니다. 이러한 유연한 태도는 관할권의 데이터 제약 조건을 충족시키면서 설비 투자 및 운영 복잡성을 최소화합니다.

On-Premise형 어플라이언스는 마이크로초 단위의 완화가 필요한 금융 거래 플랫폼, 국방 기관, 미디어 방송 사업자에서 틈새 수요를 유지하고 있습니다. 그러나 이러한 수직적 시장에서도 대용량 트래픽의 오버플로우에 대한 대책으로 클라우드 용량을 계층화하고 있습니다. 사이트 간, 스크리닝 노드 간, SIEM 플랫폼 간 지속적인 API 기반 텔레메트리 교환은 DDoS 방어 시장 전반에 걸쳐 필수 요건이 되고 있습니다.

DDoS 방어 시장 보고서는 구성요소별(솔루션, 서비스), 도입 형태별(클라우드, On-Premise, 하이브리드), 조직 규모별(중소기업, 대기업), 최종사용자 산업별(정부/국방, 은행/금융 서비스/보험, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

북미의 39.05% 점유율은 성숙하면서도 변동이 심한 시장 환경을 잘 보여주고 있습니다. 금융, SaaS, 에너지 분야가 고부가가치 타겟이 되고 있습니다. CISA(미국 사이버 보안 인프라 보안청)의 지침에 따라 실시간 텔레메트리 공유와 제로 트러스트 대응이 점점 더 요구되고 있으며, 사고 대응에 있으며, 벤더와 고객 간의 긴밀한 협력이 촉진되고 있습니다. 암호화 트래픽 검사 및 머신러닝 기반 이상 징후 점수 부여에 우선순위를 두고 투자하고 있습니다.

아시아태평양은 14.65%의 연평균 복합 성장률(CAGR)로 가장 강력한 성장세를 보이고 있습니다. 디지털 경제권에서 매년 수천만 명의 신규 광대역 모바일 가입자가 증가하면서 봇넷의 모집 가능성이 확대되고 있습니다. 지역 통신사들은 보안 업체와 협력하여 5G 코어 네트워크 전체에 에지 스크러빙 노드를 배치하여 홉 지연을 줄이고 고객 경험을 개선하고 있습니다. 일본과 호주의 규제 당국은 현재 중요 인프라 사업자에게 분기별 복원력 보고를 의무화하고 있으며, 이는 DDoS 방어 시장 전체에 대한 수요를 강화하고 있습니다.

유럽에서는 엄격한 프라이버시 규제와 고도화되는 공격의 균형을 맞추는 것이 과제입니다. NIS2 지침에 따라 미흡한 방어 체계에는 전 세계 매출액의 최대 2%의 벌금이 부과되어 인증된 멀티테넌트형 대책 서비스로의 전환이 가속화되고 있습니다. 중동 및 유럽의 유틸리티 사업자들은 정치적 동기에 의한 홍수 공격에 직면하고 있으며, AI를 통한 트래픽 분류와 주권적 데이터 호스팅 보장의 조합이 도입을 촉진하고 있습니다. 라틴아메리카, 중동 및 아프리카은 봇넷의 발원지이자 표적형 공격의 새로운 경로로 부상하고 있으며, DDoS 방어 시장에서 지역 특성을 고려한 상황 인식형 방어 전략이 요구되고 있습니다.

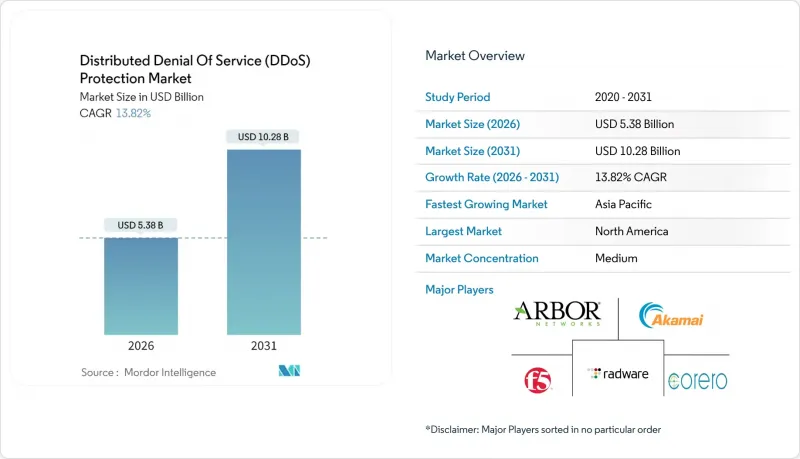

DDoS protection market size in 2026 is estimated at USD 5.38 billion, growing from 2025 value of USD 4.73 billion with 2031 projections showing USD 10.28 billion, growing at 13.82% CAGR over 2026-2031.

This expansion is fueled by the mounting frequency of multi-vector, terabit-scale incidents, strengthened regulatory mandates, and the widespread embrace of hybrid and cloud-based mitigation models. Solution-centric offerings maintained dominance with 61.23% share in 2024, underscoring enterprise demand for integrated, programmable defenses. Cloud-first deployments accounted for nearly half the addressable opportunity, yet hybrid architectures are gaining ground as organizations balance latency, control, and compliance. Regional dynamics remain pivotal: North America led with 39.34% revenue share in 2024, while Asia Pacific is advancing at a 14.89% CAGR, driven by rapid 5G rollouts and surging IoT adoption.

A record 6.3 Tbps event in 2025 highlighted the jump from volumetric floods to blended protocol and application-layer campaigns, overwhelming legacy rule-based appliances and escalating procurement of adaptive, AI-driven platforms. Communication service providers and financial institutions remain high-value targets, and global regulators now require demonstrated resilience for critical infrastructure operators.

Elastic, always-on cloud scrubbing has become indispensable as short-burst attacks spike; however, latency-sensitive workloads keep on-premises defenses relevant, accelerating hybrid demand. Partnerships between hyperscale clouds and security specialists are bridging skills gaps for SMEs while meeting emerging compliance obligations.

Capex-heavy hardware plus ongoing signature updates remain prohibitive for smaller enterprises, steering demand toward subscription-based cloud scrubbing paired with managed SOC services.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions commanded 60.65% revenue in 2025 as enterprises sought unified, programmable defenses capable of spanning L3/4 volumetric floods and L7 application abuses. Within this umbrella, network-layer protection retained the largest slice, yet advanced bot mitigation is forecast to rise at a 15.05% CAGR, driven by AI-enabled bots that mimic legitimate user behavior. Vendors are embedding machine-learning classifiers, device fingerprinting, and real-time challenge mechanisms to blunt credential-stuffing and inventory hoarding. Services-managed and professional-continue to gain relevance as organizations consolidate suppliers for compliance reporting and 24X7 monitoring. The interplay of solutions and services underscores a shift toward outcome-based contracting across the DDoS protection market.

Growing adoption of hybrid topologies demands orchestration between on-premises hardware, cloud scrubbing centers, and containerized network functions. As offerings converge, differentiation pivots on API-centric integration, attack-forensics depth, and zero-trust alignment. Solution vendors that blend behavioral analytics with actionable intelligence are positioned to capitalize on rising regulatory pressure for demonstrable resiliency across critical sectors.

Cloud-based defenses captured 49.02% of the DDoS protection market size in 2025, offering elastic bandwidth pools and global anycast routing to absorb multi-Tbps assaults. Always-on models ensure response within seconds, a necessity amid sub-minute "pulse" attacks. Meanwhile, hybrid architectures are projected to expand at a 15.25% CAGR through 2031 as enterprises merge low-latency, on-premises detection with cloud-scale scrubbing during surge periods. This flexible posture satisfies jurisdictional data constraints while minimizing capex and operational complexity.

On-premises appliances retain niche traction among financial trading platforms, defense agencies, and media broadcasters that demand micro-second mitigation. However, even these verticals are layering cloud capacity for volumetric overflow. Continuous API-driven telemetry exchange between sites, scrubbing nodes, and SIEM platforms is becoming table stakes across the DDoS protection market.

The Distributed Denial of Service (DDoS) Protection Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Government and Defense, Banking, Financial Services and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD),

North America's 39.05% share underscores a mature yet volatile landscape. High-value targets include finance, SaaS, and energy. CISA directives increasingly require real-time telemetry sharing and zero-trust alignment, prompting deeper vendor-customer collaboration on incident response. Investments prioritize encrypted-traffic inspection and machine-learning-driven anomaly scoring.

Asia Pacific exhibits the strongest growth trajectory at 14.65% CAGR. Digital economies are onboarding tens of millions of new broadband and mobile subscribers annually, amplifying botnet recruitment potential. Regional telcos partner with security vendors to deploy edge scrubbing nodes across 5G core networks, reducing hop latency and improving customer experience. Regulatory agencies in Japan and Australia now mandate quarterly resilience reporting for critical infrastructure operators, reinforcing demand across the DDoS protection market.

Europe balances stringent privacy mandates with elevated attack sophistication. NIS2 imposes fines up to 2% of global turnover for inadequate defenses, accelerating migration toward certified, multi-tenant mitigation services. Central and Eastern European utilities face politically motivated flood attacks, driving adoption of AI-guided traffic classification coupled with sovereign data-hosting guarantees. Latin America, the Middle East, and Africa represent emerging vectors both for botnet origination and targeted campaigns, necessitating localized, context-aware defense strategies within the DDoS protection market.