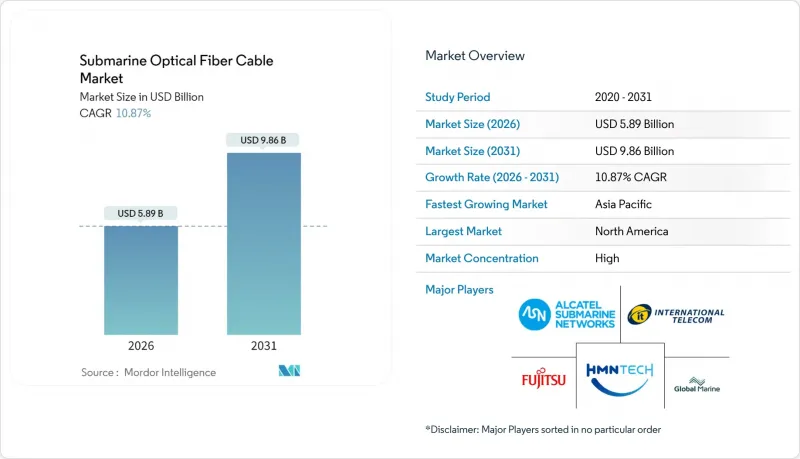

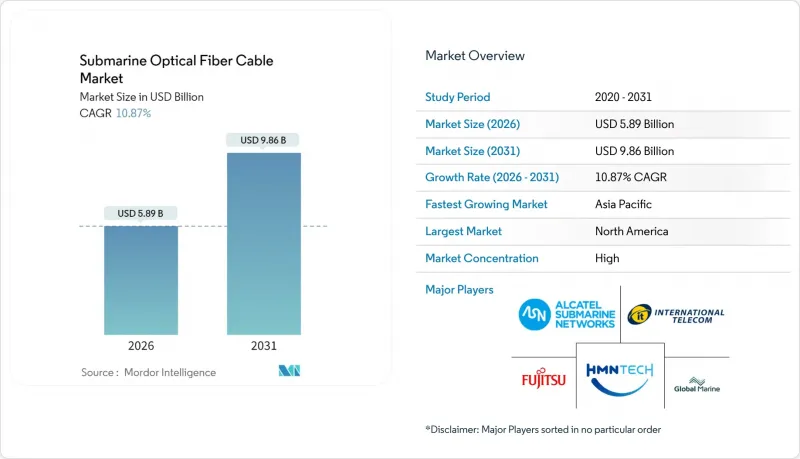

2026년 해저 광섬유 케이블 시장 규모는 58억 9,000만 달러로 추정되며, 2025년 53억 1,000만 달러에서 성장하며, 2031년에는 98억 6,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 10.87%를 나타낼 것으로 예측됩니다.

하이퍼스케일 클라우드 프로바이더들의 투자 확대, 400GbE/800GbE로의 업그레이드 주기 가속화, 공간 분할 다중화(SDM) 시스템의 상용화가 진행되면서 대륙간 연결경쟁 구도와 경제성이 재편되고 있습니다. 60Tbps 이상의 시스템 설계가 표준화되어 단위 대역폭 비용 절감과 AI 집약형 데이터 플로우를 실현할 수 있게 되었습니다. 용량 확장 전략은 국가 안보 관련 규제 수립과 교차하는 경향이 강해지고 있으며, FCC의 2024-2025년 케이블 라이선싱 절차 재검토가 그 좋은 예입니다. 이를 통해 경로 선정과 벤더 인증이 이루어지고 있습니다. 동시에 수리 선박의 병목 현상과 발트해의 반복되는 장애는 지정학적 위험에 대한 노출도가 높아져 운영 비용과 보험료가 증가하는 요인으로 작용하고 있습니다.

5G 및 신흥 AI 워크로드로 인한 대역폭 요구 사항 증가로 인해 대륙 간 트래픽은 2029년까지 연평균 39%씩 증가할 것으로 예측됩니다. 해저 케이블은 1-5밀리초의 지연 시간을 유지하며, 위성 별자리보다 훨씬 낮은 지연 시간을 유지하여 고주파 거래 및 산업용 IoT 이용 사례에서 경쟁력을 유지할 수 있습니다. 1Tbps의 피크 속도를 목표로 하는 향후 6G 규격에 따라 800GbE 파장을 처리할 수 있는 중계기에 대한 수요가 증가하고 있습니다. 남중국해의 미해결된 항로 승인 지연은 신규 용량을 제한하고, 동남아시아로 향하는 트래픽의 가격 프리미엄을 발생시키고 있습니다.

Meta, Google, Amazon, Microsoft의 개인 소유는 기존의 컨소시엄 자금 조달을 초과하여 총 투자액이 200억 달러가 넘습니다. 하이퍼스케일러 데이터센터내 직접 종단함으로써 육상 백홀을 없애고 지연과 운영 비용을 절감하는 동시에 데이터 주권 관리를 강화합니다. 구글의 250Tbps 'Dunant'와 Meta의 50,000km 'Project Waterworth'는 이러한 새로운 수직적 통합 모델을 구현하고 있습니다.

단 60척의 전용선이 600개 이상의 가동 시스템을 지원하고 있으며, 여러 장애가 발생할 경우 복구 기간이 길어질 수 있습니다. 북극권 및 태평양 횡단 수리 비용은 건당 100만 달러가 넘고, 계절적 기상 조건으로 인해 연간 보험료가 15-20% 상승하는 등 고위험 지역에서는 연간 보험료가 15-20% 상승하고 있습니다.

2025년 해저 광섬유 케이블 시장 규모의 52.74%를 습식 플랜트 설비가 차지할 것으로 예상되며, 20쌍 이상의 광섬유 설계에 따른 중계기 수요 증가가 견인차 역할을 할 것으로 보입니다. 서브콤의 해양 서비스 역량 확대는 이러한 수요 급증에 대응하기 위한 것입니다. 복잡한 지정학적 혼란으로 인해 수리 주기가 길어지고, 전문 중재 선박의 가치가 높아짐에 따라 보조 및 해양 서비스는 CAGR 11.86%로 성장하고 있습니다.

25년간의 운영 기간 중 지속적인 유지보수 매출은 서비스 프로바이더에게 예측 가능한 현금 흐름을 제공합니다. 육상 설비는 육상국 전력 및 감시 시스템의 노후화에 따라 꾸준한 갱신 수요가 있지만, 해저 광섬유 케이블 시장에 대한 기여도는 여전히 미미한 수준입니다.

2025년 매출에서 단일 모드 광섬유가 67.02%를 차지했으나, SDM 멀티코어 광섬유는 2031년까지 연평균 13.62% 성장할 것으로 예측됩니다. OFS의 TeraWave SCUBA 4X와 같은 SDM 유닛은 용량을 4배 향상시켜 다가오는 섀넌 한계에 대한 압박을 완화합니다. 스미토모전기의 결합형 멀티코어 광섬유는 0.158 dB/km의 감쇠를 실현하여 SDM의 성능이 해양 횡단 구간에서도 유효하다는 것을 입증했습니다.

구글이 듀난에 12 파이버 페어 SDM 아키텍처를 도입한 것은 상업적 타당성을 입증하고 더 광범위한 채택을 가속화하고 있습니다. 멀티모드 광섬유는 여전히 국사내 용도에 국한되어 있습니다.

2025년 해저 광섬유 케이블 시장에서 북미의 36.25%의 점유율은 하이퍼스케일 클러스터와 강력한 규제 프레임워크에 의해 주도되고 있습니다. 구글의 10억 달러 규모의 미일 간 케이블 투자는 태평양 지역 용량 강화에 기여하고, LS전선의 6억 8,100만 달러를 투자한 버지니아 공장은 국내 공급의 탄력성을 확보합니다.

아시아태평양은 디지털 경제 프로그램과 지정학적 긴장 지점을 우회하는 대체 경로의 추진으로 CAGR 11.40%로 확대될 것으로 예측됩니다. 인도의 블루오리진 착륙 계획과 소프트뱅크의 새로운 태평양 횡단 케이블 건설이 이를 상징합니다. 중국 업체인 HMN 테크놀러지스와 ZTT는 생산 확장을 추진하고 있지만, 미국의 제재로 인해 일대일로 시장으로 전환할 수밖에 없는 상황입니다.

유럽은 성숙한 대서양 횡단 회랑을 활용하면서 아시아에 대한 저지연 이점을 추구하는 극북 광섬유 계획을 추진하고 있습니다. EU 전역의 케이블 보안 행동 계획과 프랑스 정부의 알카텔 서브마린 네트워크 인수는 국가 인프라 우선 정책을 강조하고 있습니다. 유럽연합(EU)의 '케이블 보안 행동계획'은 해저 케이블에 대한 위협을 예방, 감지 및 대응하기 위한 강력한 조치를 수립하고, EU가 중요 인프라 보호에 집중하는 자세를 강조하고 있습니다. 해저 케이블 기술의 전략적 중요성을 보여주는 움직임으로, 노키아는 알카텔 서브마린 네트워크(Alcatel Submarine Networks)를 프랑스 정부에 매각을 완료했습니다. 이는 유럽 각국 정부가 이 기술을 국가의 중요한 자산으로 인식하고 주권적 감독이 필요한 기술로 보고 있음을 보여줍니다.

The submarine optical fiber cable market size in 2026 is estimated at USD 5.89 billion, growing from 2025 value of USD 5.31 billion with 2031 projections showing USD 9.86 billion, growing at 10.87% CAGR over 2026-2031.

Heightened investment by hyperscale cloud providers, accelerating 400 GbE/800 GbE upgrade cycles, and the commercial roll-out of Space Division Multiplexing (SDM) systems are reshaping the competitive landscape and economics of intercontinental connectivity. Systems designed for 60 + Tbps are now routine, lowering unit bandwidth costs and enabling AI-intensive data flows. Capacity expansion strategies increasingly intersect with national-security rule-making, exemplified by the FCC's 2024-2025 overhaul of cable-licensing procedures, which is steering route selection and vendor qualification. At the same time, repair-ship bottlenecks and repeated Baltic-Sea disruptions reveal a growing exposure to geopolitical risks that elevate operating expenditure and insurance premiums.

Intercontinental traffic is projected to climb 39% annually through 2029 as 5G and emerging AI workloads multiply bandwidth requirements. Submarine links sustain 1-5 millisecond latency, an order of magnitude lower than satellite constellations, preserving competitiveness for high-frequency trading and industrial IoT use cases. Forthcoming 6G specifications targeting 1 Tbps peak rates intensify the call for repeaters able to handle 800 GbE wavelengths. Unresolved route-approval delays in the South China Sea restrict new capacity, creating price premiums for Southeast-Asian traffic.

Private ownership by Meta, Google, Amazon, and Microsoft now eclipses traditional consortium funding and exceeds USD 20 billion in aggregate commitments. Direct termination inside hyperscaler data centers eliminates terrestrial backhaul, trimming latency and OPEX while tightening data-sovereignty control. Google's 250 Tbps Dunant and Meta's 50,000 km Project Waterworth exemplify the new vertical-integration model.

Just 60 specialized vessels support more than 600 active systems, extending restoration timelines when multiple outages occur. Arctic and trans-Pacific repairs exceed USD 1 million per incident and face seasonal weather windows, elevating insurance premiums by 15-20% annually in high-risk zones.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Wet-plant equipment contributed 52.74% of the submarine optical fiber cable market size in 2025 and benefits from 20 + fiber-pair designs that intensify repeater demand. SubCom's expansion of marine fulfillment capabilities is aligned with this demand surge. Auxiliary and marine services are scaling at a 11.86% CAGR as complex geopolitical disruptions lengthen repair cycles and raise the value of specialized intervention vessels.

Continued maintenance revenue over a 25-year operational life adds predictable cash flows for service providers. Dry-plant equipment enjoys steady replacement demand as landing-station power and monitoring systems age, though it remains a smaller contributor to the submarine optical fiber cable market.

Single-mode fiber represented 67.02% of 2025 revenue; however, SDM multi-core fiber is forecast to grow at an annual rate of 13.62% to 2031. SDM units such as OFS's TeraWave SCUBA 4X deliver fourfold capacity improvements, mitigating the looming Shannon-limit crunch. Sumitomo Electric's coupled multi-core fiber achieves 0.158 dB/km attenuation, validating SDM performance over trans-oceanic spans.

Google's deployment of 12 fiber-pair SDM architecture on Dunant proves commercial viability and accelerates broader adoption. Multimode fiber remains limited to intra-station applications.

The Submarine Optical Fiber Cable Market Report is Segmented by Component (Wet-Plant Equipment, Dry-Plant Equipment, and More), Cable Type (Single-Mode Fiber, Multimode Fiber, and More), Client Type (Telecom Operators, Content and Hyperscale Cloud Providers, and More), Capacity Design (less Than or Equal To 16 Tbps Systems, 16-60 Tbps Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America's 36.25% share of the submarine optical fiber cable market in 2025 is driven by a hyperscale cluster and strong regulatory frameworks. Google's USD 1 billion US-Japan cable commitment reinforces Pacific capacity while LS Cable's USD 681 million Virginia plant secures domestic supply resilience.

The Asia Pacific is projected to expand at a 11.40% CAGR, driven by digital economy programs and alternative routes that circumvent geopolitical flashpoints. India's Blue Origin landing and SoftBank's new trans-Pacific build typify this activity. Chinese vendors HMN Technologies and ZTT scale up production, although U.S. sanctions prompt them to shift toward Belt-and-Road markets.

Europe leverages mature trans-Atlantic corridors while championing the Far North Fiber project for Asia latency advantages. EU-wide cable-security action plans and the French State's acquisition of Alcatel Submarine Networks highlight sovereign-infrastructure priorities. The European Union's Action Plan on Cable Security establishes robust measures for preventing, detecting, and responding to threats against submarine cables, underscoring the EU's commitment to safeguarding its critical infrastructure. In a move highlighting the strategic importance of submarine cable technology, Nokia finalized the sale of Alcatel Submarine Networks to the French State, signaling European governments' view of this technology as a vital national asset warranting sovereign oversight.